The Second Derivative: Why No One Understands the AI Boom

The market misremembers 2008. That same blind spot sits at the center of the AI boom.

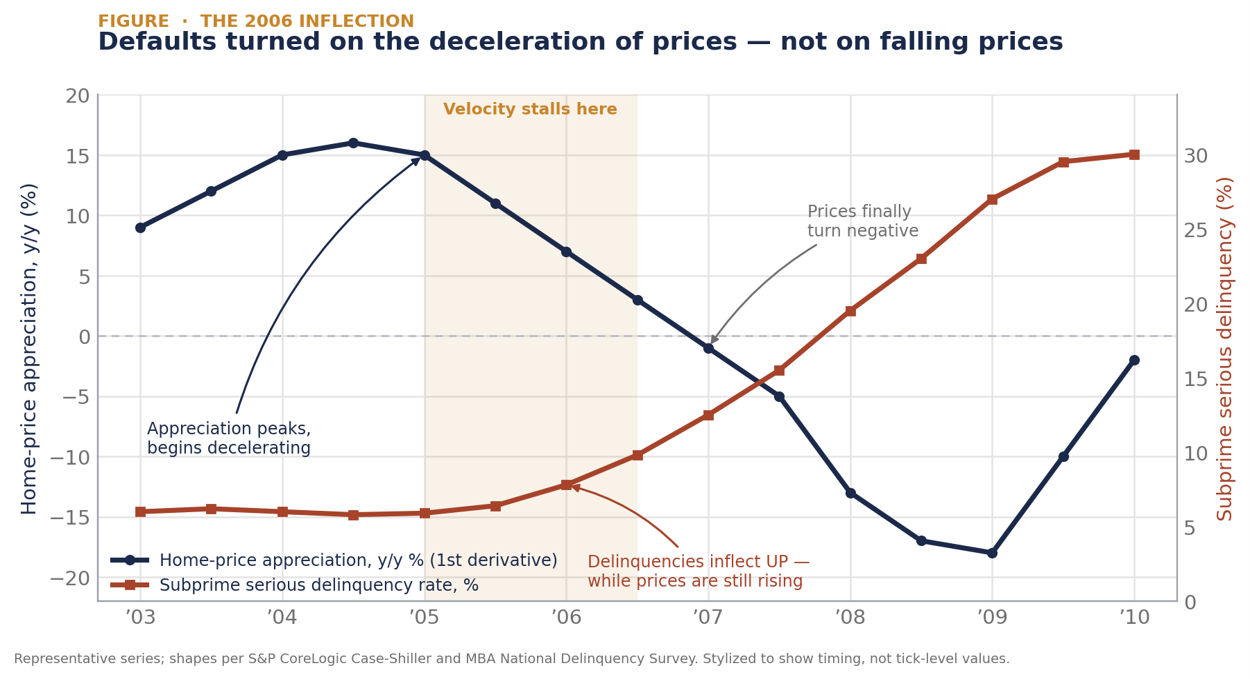

Ask a portfolio manager what caused the 2008 mortgage crisis and you will hear a tidy causal chain: lax underwriting produced loans that should never have been made, home prices crashed, borrowers found themselves underwater, they defaulted, and the securities written on top of those loans detonated. Prices fell, therefore borrowers defaulted. It has the great virtue of sounding obvious. It is also, as a matter of sequence, wrong. It is the same error the market is making right now about the AI boom.

The subprime machine did not run on prices. It ran on the change in prices, and more precisely on the change in that change. The canonical product of the era - the 2/28 and 3/27 hybrid adjustable-rate mortgage - was not designed to be repaid on its stated terms. It was designed to be refinanced.

A borrower took a low “teaser” rate for two or three years. The implicit underwriting assumption, shared by originator and borrower alike, was that the loan would never reach its reset: rising home values would manufacture equity, the borrower would refinance into a fresh teaser and the clock would start again. The structure was a treadmill, and the treadmill was powered by appreciation. It worked spectacularly while it worked. Nearly four in five subprime hybrid ARMs originated in 2003 had been refinanced away by the end of 2006.

Now watch the timing. National home-price appreciation did not crash in 2006. It decelerated. The year-over-year rate of gain, which had run in the mid-to-high teens through 2004 and into early 2005, began bleeding off - still positive, still printing green, but slowing. Prices were higher than they had ever been. And yet, with prices at their peak and still rising, subprime delinquencies inflected upward.

This is why the popular causal story is, in economist Didier Sornette’s phrase, “right mechanically” but “wrong because it takes the fall in house prices as exogenous” - as though the decline simply arrived one day, a meteor from outside the system. It did not arrive from outside. The deceleration was endogenous to the structure; the structure required ever-accelerating prices to keep refinancing its way out of its own reset schedule, and no series accelerates forever.

The second derivative was always going to roll over. When it did, the first derivative followed it down through zero, negative equity spread from the margin inward, and the defaults the market insisted were caused by “falling prices” had in fact begun a year earlier, when prices were still rising but had stopped rising faster.

II. A Short Theory of Derivatives

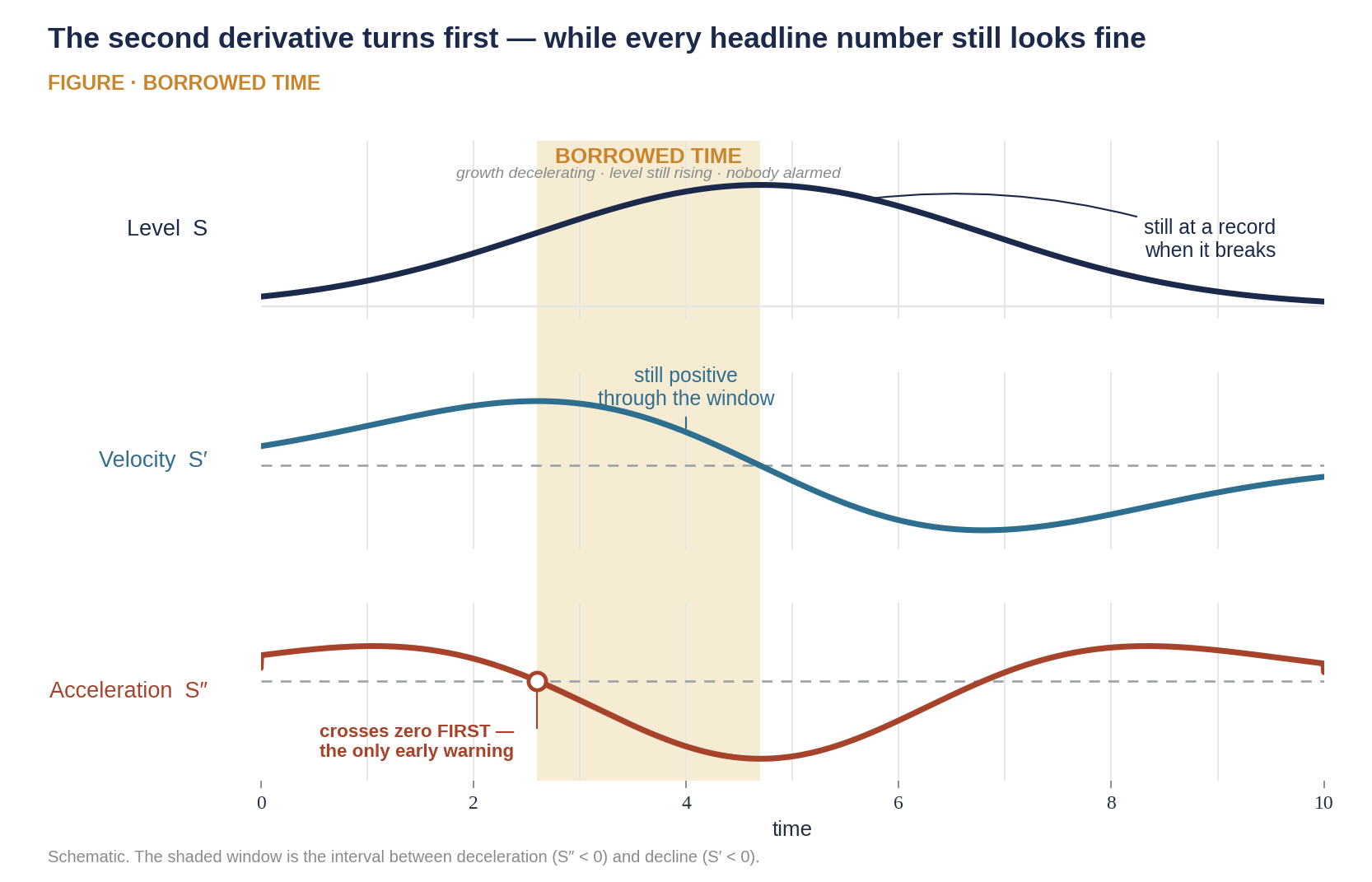

Let the relevant quantity be S. Three numbers describe it. The level is S itself: how big the thing is. The first derivative is the velocity, S′: how fast it is growing. The second derivative is the acceleration, S″: whether that growth is itself speeding up or slowing down. Markets are instrumented to observe the first two and almost entirely blind to the third. Sell-side models forecast levels. Momentum strategies trade the first derivative. Virtually nobody builds a position around the second derivative.

Yet the second derivative is precisely where information about regime change lives, for a structural reason. When financing embeds a growth assumption - a reset that presumes refinancing, a covenant that presumes rising cash flow, a commitment sized to presumed expansion - the assumption is satisfied not by the level being high but by growth being sustained. Sustained growth at a declining rate still satisfies the headline (“revenue grew 40%!”) while quietly violating the embedded premise (“…but the incremental capacity we committed to assumed it would grow 70%”). The gap between what the headline shows and what the structure needs opens silently.

There is a window - call it borrowed time - between the moment the second derivative rolls over and the moment the first derivative crosses zero. During that window everything looks fine. Revenue is at record highs. Growth is still positive. The press releases are triumphant. And the machine is already broken; it simply has not been told yet.

Borrowed time is dangerous in exact proportion to the convexity of the instruments riding on top of S. A long-dated equity multiple is roughly linear in expectations; it can deflate slowly and reflate, the way the dot-com index took two years to bottom and many survivors simply de-rated. A leveraged credit structure is negatively convex: it earns a fixed coupon on the way up and absorbs unbounded loss on the way down, and its covenants are step functions, not smooth curves. This distinction - between an equity story that can drift and a credit story that snaps - is the difference between 2000 and 2008. It is also the difference between what the market thinks AI is and what AI actually is.

III. The AI Boom is a Credit-Driven Real Estate Cycle

Open any AI bull or bear note and observe what it argues about. It argues about levels - how many billions of revenue, how many gigawatts, how large the total addressable market - and about the first derivative - is growth 200% or 150%, is enterprise inflecting, are tokens-per-minute rising. The bears say the levels are unsustainable; the bulls say the growth justifies them. Both camps are staring at S and S′. Neither is watching S″. And the entire financing architecture erected over the past twenty-four months is a bet on S″ - on the acceleration of demand continuing - dressed up as a bet on the level.

This matters because the dominant analogy in everyone’s head is the wrong one. “Is AI a bubble like dot-com?” is the question being asked, and it produces dot-com answers: maybe the leaders survive and the laggards wash out; maybe multiples compress; maybe we get a 50% drawdown and a recovery. That framing is a category error.

The year 2000 was an equity-multiple event - too much optimism priced into stocks with thin balance sheets and almost no debt. The pain was real but it was equity pain, and equity is patient capital that can simply be marked down and held. The AI build-out is structurally different. It is increasingly financed not by selling overpriced equity but by contracting future cash flows and borrowing against hardware - take-or-pay capacity deals, GPU-collateralized term loans, off-balance-sheet vehicles, asset-backed notes sold to insurers. That is not the architecture of 2000. That is the architecture of 2008.

There is a deeper misclassification beneath the 2000-versus-2008 question, and it is the one that does the real damage. The market is pricing AI as a technology cycle when its actual anatomy is that of a credit-driven real estate cycle - which is precisely why the 2008 mechanics apply - and the two break for entirely different reasons.

Technology cycles are driven by innovation and adoption; their risks are obsolescence and competition; they live or die on whether the product is wanted, and they can de-rate slowly as the future is repriced.

Real estate cycles are mechanical: leverage, hard assets, occupancy - debt-financed construction at scale, commercial leases disguised as take-or-pay contracts, and long construction lags that guarantee supply arrives after demand has turned. Walk down the AI build-out and every feature is a property development in disguise: a data center on entitled land, financed with debt against the structure and leased to tenants on take-or-pay terms. This is not a software business that happens to own servers. It is a real estate business that happens to compute.

Real estate cycles break the same way every single time. Not when demand collapses - it rarely does - but when the rate of demand growth decelerates against the fixed supply the boom has just finished building. The second derivative again, in the one asset class where it has been studied for a century.

And the credit machine does not de-rate gently. It refinances or it seizes. The instruments that seize - take-or-pay leases, GPU-collateralized term loans, asset-backed notes - are each negatively convex. Within this machine, the financing mechanics diverge: the pure-play neoclouds borrow non-recourse debt against a specific tenant’s take-or-pay and collapse into seizure when the tenant can’t pay. The hyperscalers fund with corporate bonds and operating cash flow; for them, a tenant default means impairment and margin compression, not seizure. Oracle sits between them: corporate-funded but dangerously concentrated.

The distinction matters because the seizure and the impairment are two different wounds, inflicted by the same deceleration, and both are hiding inside the same $2.1 trillion backlog. But to price the credit quality of that book, we must look past the total headline RPO to the core structural exposure. Across the big four platforms, the RPO that Wall Street values as forward revenue is, in reality, a concentrated credit exposure to a handful of cash-burning frontier model labs and specialized AI tenants.

The hyperscaler has, in economic substance, extended a concentrated infrastructure credit facility to tenants with no independent operating income. If those tenants default, the backlog evaporates into non-cash impairments, leaving the corporate balance sheet to absorb the fixed costs of customized, rapidly depreciating capital assets.

IV. The Loan Book Nobody Calls a Loan Book

Look past the compute scarcity narrative and see these agreements for what they really are. A frontier lab signs a contract promising to pay a counterparty tens of billions of dollars, over several years, for compute it has not yet consumed. The counterparty - Oracle, CoreWeave, a hyperscaler - books that promise as backlog and borrows against it, raising debt to pour concrete and rack GPUs. Reduce the arrangement to its skeleton and it is a loan: the counterparty advances capital in kind - a building full of chips - against the borrower’s commitment to pay it back, with interest and principal amortization baked directly into the take-or-pay rate. The data center is the collateral. The lab’s contracted payments are the debt service. And the structure performs only so long as the borrower can keep funding those payments - which, for a company with no profits, means only so long as it can keep raising money.

This is precisely why the analogy is 2008, not 2000. AI capital expenditure is not a capital budget. It is a loan book. Leases in form; debt in substance. The capex is the funded principal; the contracted backlog - the remaining performance obligation, in the filings - is the lease receivable. When a hyperscaler or a neocloud reports a record capex figure, the financial press reads it as confidence, as proof of demand. Read it instead as origination volume. Each gigawatt of committed build is a loan extended to whichever tenant has signed the take-or-pay beneath it, and the credit quality of that loan is precisely the credit quality of the tenant. The market is celebrating loan growth and calling it revenue growth.

V. The Borrower With No Income

Every subprime cycle has a borrower who could only refinance, never repay. In this one, that borrower is OpenAI.

OpenAI has committed to pay for compute on a scale without precedent in corporate history: multi-year, take-or-pay capacity contracts whose aggregate obligations run to the hundreds of billions of dollars. Against them sits an operating business that does not yet earn a profit - revenue real, large, and growing quickly, but short of covering the company’s own cash burn and nowhere near covering the contracted payments.

Those payments are therefore not serviced out of earnings. They are serviced out of financing, and financing, for a borrower in this position, is available on a single condition: that each new round price above the last.

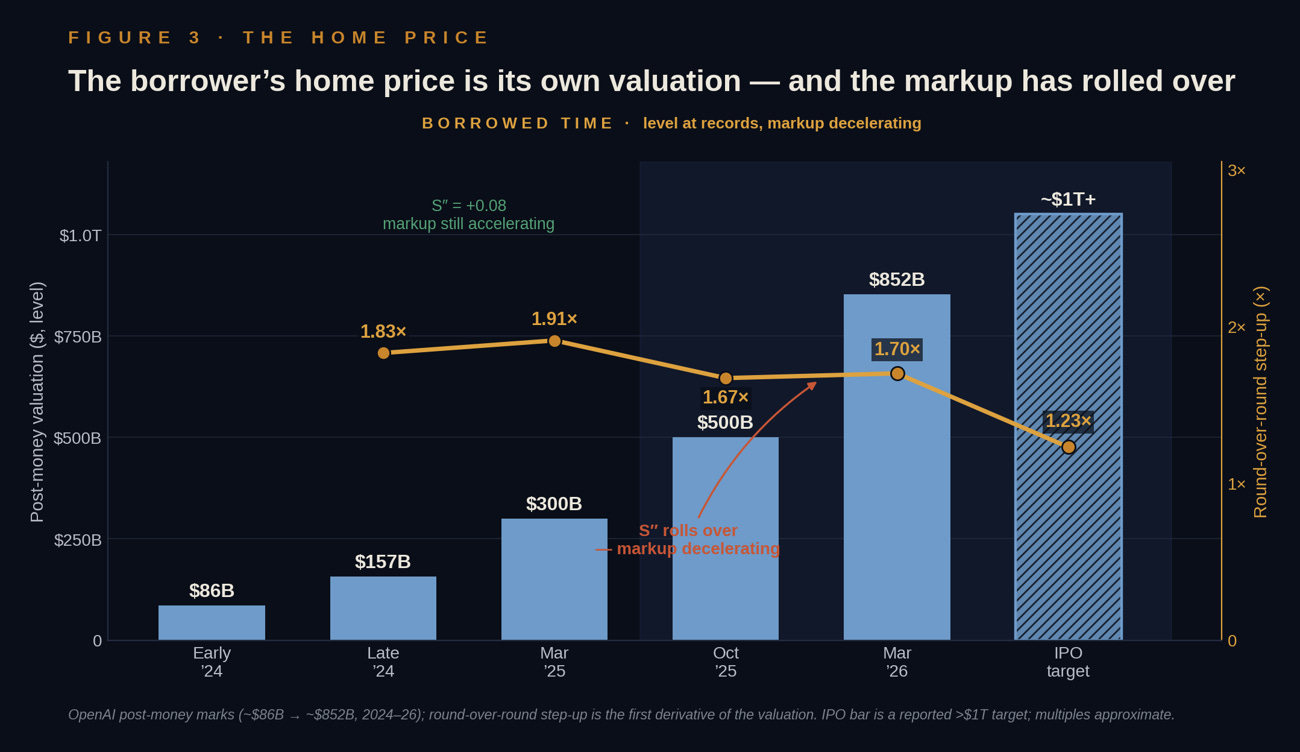

For OpenAI the up-round is not a measure of progress; it is the funding event itself -the mechanism by which the prior period’s commitments are paid and the next period’s are made signable. The markup is the cash flow.

A company funded by its own appreciation is solvent not in proportion to how high the mark stands but in proportion to how fast it is still rising - because a burn rate is an accelerating schedule, indifferent to the size of the last round. Each new phase of compute expansion demands an exponentially larger cash injection. When the step-up compresses from 1.91× down to 1.23×, the math breaks: the valuation can print a record at the precise moment the company’s capacity to fund its structural deficit is contracting. This is not a paradox; it is the arithmetic of a borrower whose liquidity is bound to the first derivative of its own price.

And that value is set by the very capital providers who need it to keep rising. OpenAI’s most recent round - reported at roughly $122 billion of fresh capital - set its valuation near $852 billion, with the same names underneath it: Microsoft, SoftBank, Nvidia, Amazon. These are the counterparties whose compute the proceeds will buy. The mark goes up because money came in; more money comes in because the mark went up. The appraiser, the lender, and the buyer are the same three people, passing the same dollar in a circle and marking it higher on each pass. It works gloriously - for a while - for exactly the reason the 2/28 worked: as long as the mark keeps rising, the lab can refinance.

Measured as a level, OpenAI’s valuation is the most remarkable appreciation in the history of private markets - roughly $86 billion in early 2024, then about $157 billion, $300 billion, $500 billion, and approximately $852 billion by the spring of 2026. Measured as a rate of change, the same series inverts: the round-over-round step-up ran 1.83×, 1.91×, 1.67×, 1.70×, and falls to roughly 1.23× implied by the reported public-offering target. Private marks are inherently lumpy - negotiated, episodic, set by a handful of insiders - so no single step is decisive. But the trend is unmistakable: it bends down, and it bends hardest at the one mark set by the deepest, most unforgiving pool of capital - the public market. The implied IPO step-up is both the lowest in the sequence and the hardest to negotiate, and it is the one the structure must actually clear. This arithmetic is also the most probable explanation for OpenAI’s recent IPO delay.

This deceleration is not arbitrary. It reflects the two structural headwinds directly attacking the revenue growth the marks require: token efficiency and Chinese open weights. The industry’s central optimization project - routing simple queries to cheap models and trimming ‘thinking’ tokens - has eroded the token-per-task tailwind that padded revenue. Meanwhile, Chinese open-weight models have repriced the commodity middle of inference to near-zero, capturing over 60% of OpenRouter tokens at a fraction the price. Revenue still grows - adoption is real - but the rate of growth is precisely what is under attack, and the rate is what the next mark needs to clear.

VI. The Lender’s Backlog

Move up one level, from the borrower to the lenders. The credit they’ve extended takes a specific form: remaining performance obligations - RPO - the contracted revenue a company has under signed agreement. The backlog. Wall Street loves backlog; it reads as visibility, as demand pulled forward and locked in.

On the hyperscaler balance sheets that backlog has swelled into the hundreds of billions apiece, and every quarter the growth in RPO is presented as proof that the demand is real and the buildout justified. The larger the backlog, the more secure the story: a company does not build a gigawatt on a hope, it builds it against a contract.

An RPO is not a liquid asset; it is a forward contractual commitment - a promise of future payment in exchange for future compute. And a multi-year commitment is worth exactly the creditworthiness of the entity on the other end of it. When that entity is investment-grade and cash-generative, the backlog is what it claims to be: high-quality visibility, merely deferred. When that entity is a pre-profit company that loses tens of billions a year and can pay only by continuously refinancing its own equity valuation, the backlog is something else entirely. It is a subprime commitment, used to justify massive, un-depreciated capital expenditure, reported to shareholders as structural strength.

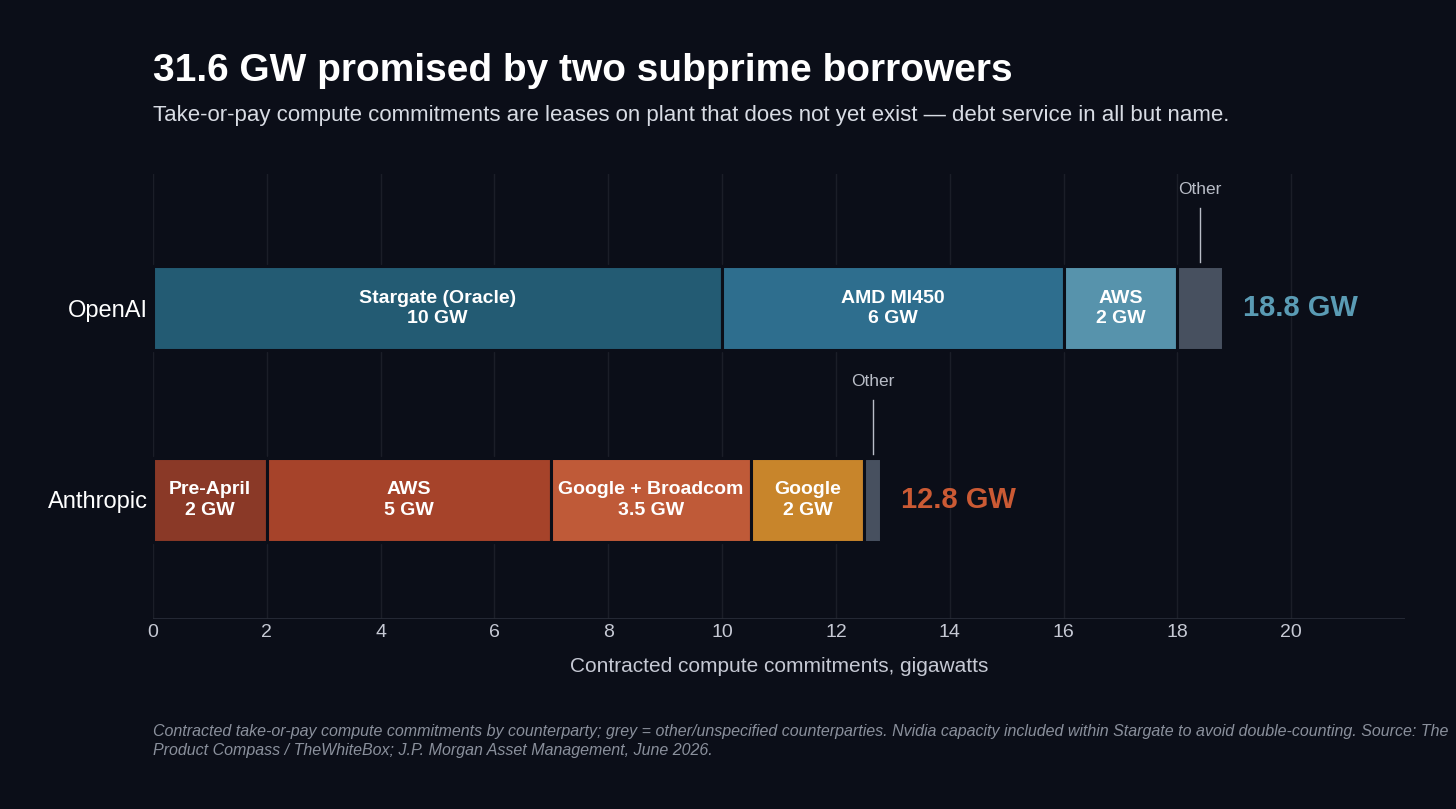

Now price the credit quality of that book. Of roughly $2.1 trillion in aggregate contracted backlog across the four big platforms, about half - on the order of $1.05 trillion - is owed by OpenAI and Anthropic. Microsoft’s book is about 49% these two names; Oracle’s is 54%, with roughly $300 billion owed by OpenAI alone; Google’s is 43%; Amazon’s is 51%.

The hyperscaler has, in economic substance, extended a concentrated, unsecured loan to cash-burning tenants. The RPO that Wall Street values as forward revenue is, in reality, a credit exposure to borrowers with no operating income.

Here the bulls raise their strongest objection. Yes, they say, the frontier labs burn cash now - but so did Amazon, so did every great compounding business in its infrastructure-building phase. Burn is investment; the labs will grow into profitability; the borrower of today is the cash machine of tomorrow. Half right. There is no single frontier-lab borrower. There are at least two, and they are not the same credit.

Anthropic is a speculative-grade, but highly insulated, credit. Its revenue is ~80% enterprise - sticky, recurring, contracted seats - and its unit economics are firmly above water, generating $1.70 of revenue for every dollar of compute. Burn converges to a manageable ~9% of revenue by 2027 as gross margins normalize.

More importantly, Anthropic’s liabilities are protected by a classic 2008 “monoline wrap” maneuver. In the ~$35B Apollo/Blackstone TPU facility, Anthropic’s paper borrows the rating of its investment-grade backers: Google guarantees lease shortfalls, and Broadcom guarantees the residual value of the silicon on the ~$31B senior tranche. The co-signers are standing behind the bills and protecting Anthropic’s counterparties.

OpenAI is the “naked” borrower, making it the weakest and most volatile credit in the ecosystem. Its revenue mix is fragile - ~60% consumer. With burn hovering at a crushing ~57% of revenue through 2027 and cumulative cash destruction marching toward $115B by 2029, OpenAI has no path to positive cash flow this decade.

Worse, OpenAI has no real co-signer. While the market long priced in an implied Microsoft backstop, Microsoft stripped away every structural strut in April 2026 - ending the revenue share, dropping exclusivity, and surrendering its right of first refusal to supply compute. Microsoft kept its 27% equity upside but walked away from OpenAI’s bills. SoftBank, the other great OpenAI backer, is itself now trying to raise a $10B margin loan against its OpenAI stake - offering a personal guarantee after lenders balked at the collateral. Even the co-signer has no co-signer.

Microsoft’s own behavior is the signal. The most informed counterparty in the complex - the one that saw OpenAI’s books from the inside for years - has recognized the credit risk. Rather than building its own compute on fifteen-year leases that outlast the chips, it foresaw the commoditization of frontier models and committed over $60B to neocloud providers through shorter, five-year capacity agreements: renting at the peak to avoid owning through the trough. That is not a bet on OpenAI’s durability. It is a lender shortening duration on a borrower it has decided not to underwrite - the same subprime credit this section describes, priced by the party that knows it best.

The critical divergence here is counterparty risk. When an investor or lessor underwrites Anthropic, they are ultimately looking through the structure to underwrite the pristine balance sheets of Google and Broadcom. The credit risk is synthetically lifted to investment-grade. When underwriting OpenAI, there is no look-through. Counterparties are exposed to a naked, standalone start-up sitting on an underwater unit economic model. Without a parental balance sheet, OpenAI is entirely dependent on a continuous refinancing treadmill - servicing each old obligation with the proceeds of the next, larger equity raise. That is the counterparty risk hiding inside roughly half of the $2.1 trillion backlog the market has priced as bankable.

VII. The Reflexive Flip

The take-or-pay contracts are the structural foundation - the collateral that makes the borrowing possible. But they are not a passive constraint. The Nash equilibrium is what pushes the hyperscalers to sign those contracts in the first place, and to sign them at ever-larger scales. The race does not bypass the loan book; it writes the loan book. To justify the next gigawatt of spend, a hyperscaler needs the next gigawatt of backlog - so it pushes its tenants to commit further forward. The $2.1 trillion backlog is not a pre-existing limit on the arms race; it is the arms race’s own paper trail. The contracts are the collateral; the race is the demand for more collateral.

Once that collateral is signed, it must be converted into infrastructure before the cash arrives. That conversion - the act of turning a signed contract into a live data center - is what drives the capex machine. And that machine is now consuming cash faster than the backlog can validate it.

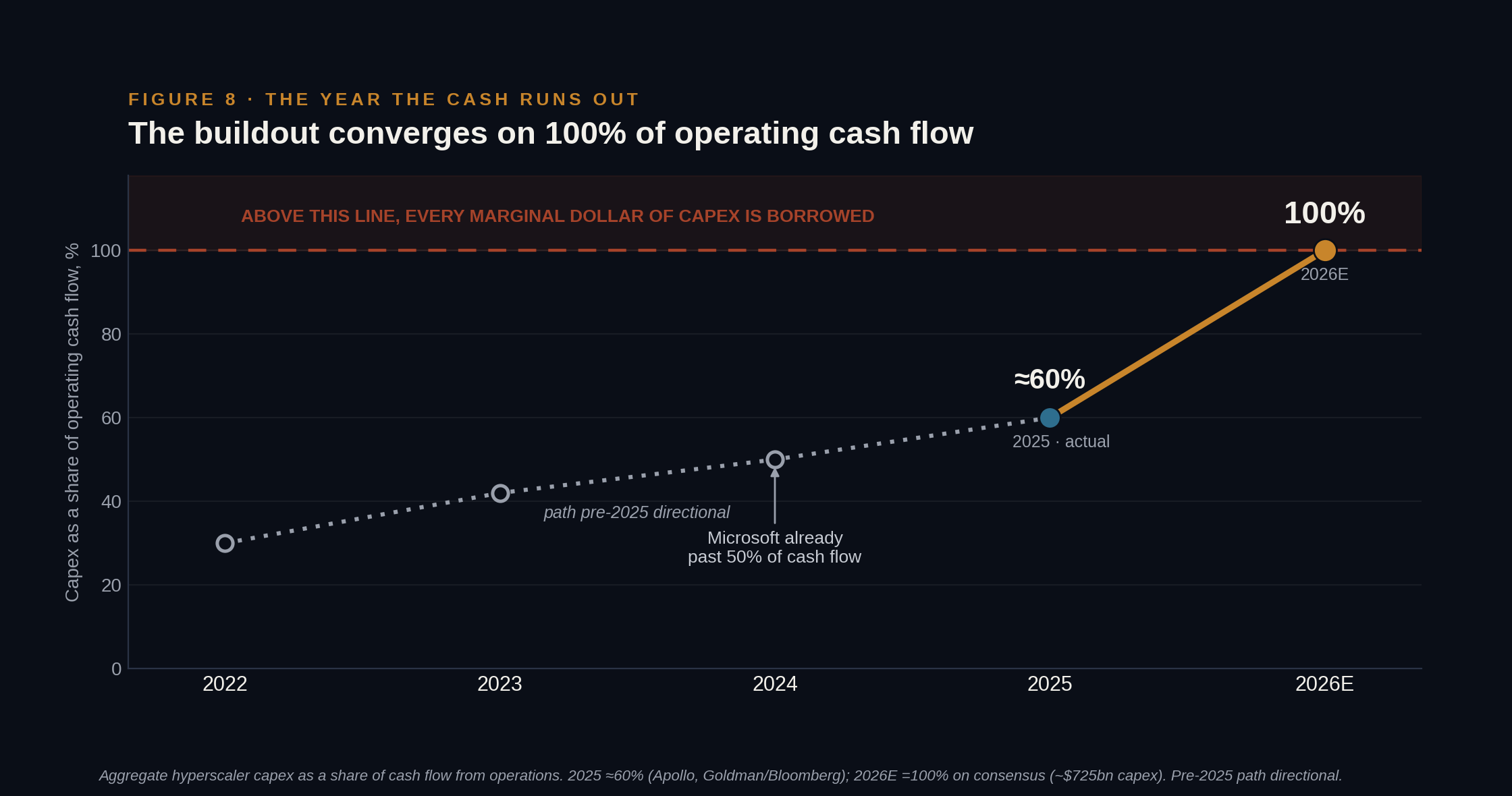

Aggregate capex as a share of operating cash flow ran near 30% in 2022, roughly 42% in 2023, about 50% in 2024, and approximately 60% in 2025; on consensus spending it reaches 100% in 2026. Above that line, by definition, every marginal dollar of capacity is funded not from internal cash but from the balance sheet - debt or equity. The “fortress balance sheet, self-funded” story is true only below 100%, and the consensus path crosses 100% this year. The fortress is not being defended; it is being spent.

Past 100% of cash flow, accelerating capex means borrowing more, faster, every quarter, against a rating that only has so many notches left. Hyperscaler debt issuance has to climb steeply over the coming year - the bond market becomes the marginal funder of the entire build.

Why are hyperscalers betting over 100% of operating cash flow on an uncertain return?

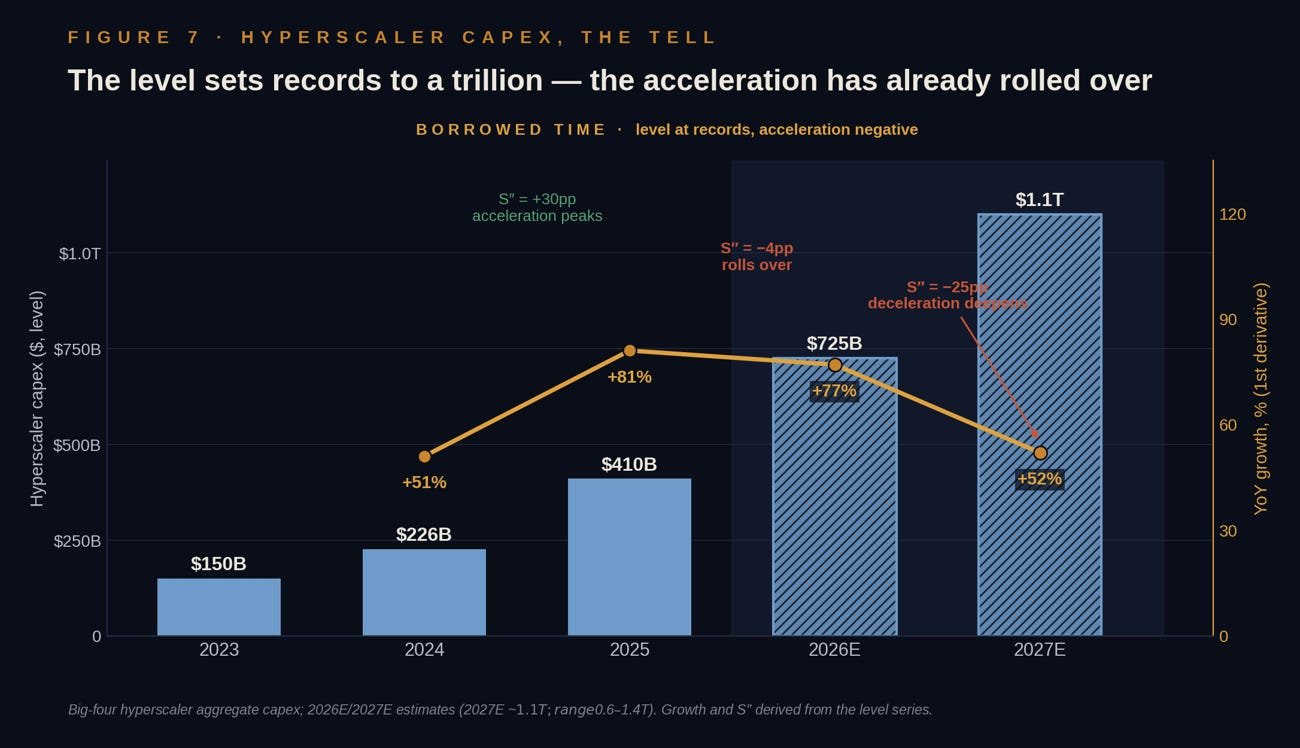

Because, until now, they have been paid to. Capital expenditure has gone vertical: roughly $150 billion in 2023, $226 billion in 2024, $410 billion in 2025, an estimated $725 billion in 2026, and approaching $1.1 trillion in 2027. As a level, it is the largest private capital-formation event in history. As a first derivative, the growth rates read +51%, +81%, +77%, +52%. And as a second derivative, the acceleration peaked at roughly +30 percentage points into 2025 and has turned negative: about −4 points, then about −25. The level is at records. The velocity is still high. The acceleration has already rolled over.

There is a recursion here that the headline numbers obscure. Hyperscaler capex in this cycle is not primarily a response to AI demand. To a substantial degree, it is the demand. The labs’ revenue is, in large part, hyperscaler spending recycled - cloud credits, compute commitments, equity-funded consumption. Nvidia’s revenue is hyperscaler capex. The neoclouds’ revenue is hyperscaler capex, levered.

Strip out the spending and the demand it manufactures, and the organic, capex-independent demand is a fraction of the headline figure. Which means the single most important growth rate in the system is the second derivative of hyperscaler capex - and it has already gone negative while every level chart still points to the sky.

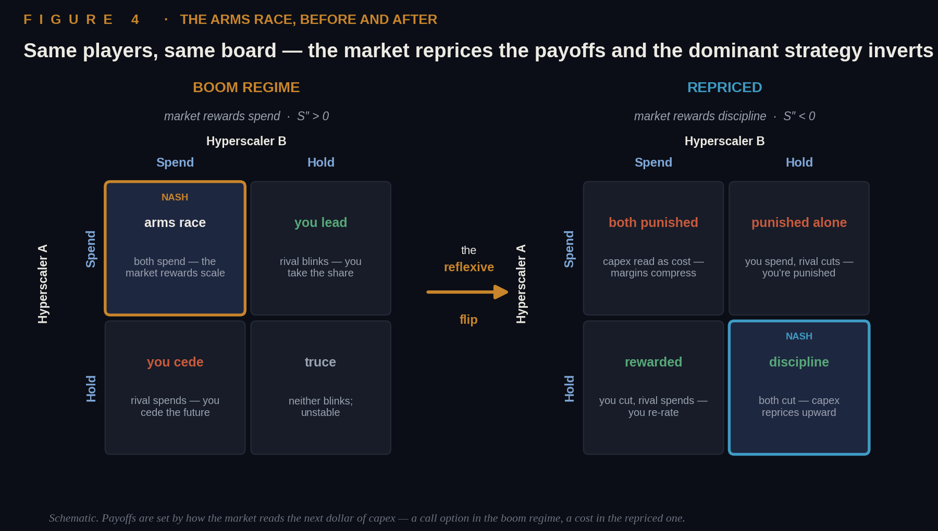

The capex arms race is a Nash equilibrium, but a conditional one: it holds only while the market rewards the next dollar of spending as a call option on growth. In that regime - the boom regime - the dominant strategy for every hyperscaler is to spend, because the alternative is to be the one player who blinked and ceded the future. Mutual escalation is stable precisely because the market applauds it. Each CFO spends because every other CFO is spending and the multiple rewards the spender.

Morgan Stanley caught the psychology exactly when it described 2027 capex estimates leaping thirty percent in a single quarter, toward $1.1 trillion, as the dynamics of an auction. An auction is the right frame, because in an auction the price is set by the most optimistic bidder and the act of bidding is itself the signal - the applause, the proof of seriousness. Keynes’s beauty contest, with chips: you are not spending on what you think the compute is worth; you are spending on what you think the market will reward you for being seen to spend.

That equilibrium is not anchored to anything physical. It is anchored to a belief - the market’s reading of what the next dollar of capex means - and beliefs reprice. The flip comes the first time a hyperscaler announces a capex cut and its multiple expands on the news rather than contracting. The instant discipline is rewarded instead of punished, every payoff on the board rewrites. Spending, formerly the dominant strategy, becomes the move that gets you punished alone; holding, formerly surrender, becomes the move that gets you re-rated. The Nash equilibrium inverts from “everyone spends” to “everyone cuts” - and because it is a coordination equilibrium, the inversion is not gradual. The first mover rewarded for cutting gives every other CFO both the cover and the incentive to follow, and discipline cascades as fast as the spending it replaces. The day the market cheers a cut is the day the arms race ends.

Goldman’s head of Delta One trading put it as plainly as it can be put:

“The first hyperscaler to signal that it can slow the pace of spending will likely see its share price rewarded (and will crush semiconductor stocks). If that happens, others will take notice. That is the reflexivity that ultimately stalls the capex cycle - not a lack of demand, but investors deciding that incremental returns on the next dollar of spend are no longer attractive.”

The cruelty of the flip is what it does to the contracts. In the boom regime, a signed take-or-pay commitment is an asset to everyone who touches it: forward demand for the hyperscaler, bankable backlog for the neocloud, collateral for the lender. In the repriced regime, the identical contract is a liability for all of them simultaneously.

The lab cannot fund the payments it locked in; the hyperscaler holds a receivable from a visibly distressed counterparty; the neocloud is left servicing debt against data centers it financed on a contract now worth less than the debt. This is negative convexity wired directly into the demand side: the same instrument is an asset on the way up and a liability on the way down, and the transition between the two states is a repricing of belief, not a change in the underlying hardware. Nothing physical has to break. The market only has to change its mind.

It lands hardest on the frontier labs, who can carry these contracts only by raising more capital - and the flip closes that window. What follows is not a clean default but a negotiation - volumes cut, schedules stretched, contracts restructured. The contracts do not vanish; they reprice - beginning with the borrower who needs the next round most.

VIII. Who Blinks First

Every reflexive cascade needs a first mover. So which hyperscaler cuts first? Who blinks?

The instinct is to say the weakest balance sheet, and the instinct is wrong. The first to cut will be the one with the best information, the credibility to reframe the cut as strength, and the balance-sheet room to be rewarded rather than punished for it.

Zuckerberg holds dual-class control. He has run this exact playbook before and was rewarded with a tripling of the stock; and of all the hyperscalers Meta has the weakest direct monetization of its AI capex - no public cloud to sell the capacity into - which makes its spend the hardest to defend and the easiest to cut. The only reason it has not cut yet is the Nash equilibrium - Zuckerberg is waiting for the market to tell him it is safe to stop spending.

The others array predictably. Google will not blink - it builds TPUs at a structural cost advantage and reports a cloud backlog north of $460 billion, so it benefits if rivals retrench. Oracle cannot blink: at roughly 86% of sales going to capex, with a balance sheet stretched around Stargate, its stress will surface as a credit event. Amazon may have its hand forced from the other direction - free cash flow already turning negative under the build. Negative free cash flow is the kind of thing capital markets eventually vote on, whether management calls the election or not.

The numbers tell the same story. Morgan Stanley pegs hyperscaler investment-grade leverage at roughly 1.8 turns of gross debt - double what it was a year ago and now higher than the entire energy sector. That figure does not count the hundred-billion-plus parked off the balance sheet in the vehicles. What stands in its place is a leveraged, hard-asset, refinance-dependent balance sheet - and the marginal gigawatt, the thing cut first, is the most discretionary line on it.

IX. The Blast Radius

Let’s say OpenAI is subprime, the regime shifts, belief reprices, the capital window slams shut, and a hyperscaler cuts that marginal gigawatt to protect its own leverage. Who is exposed?

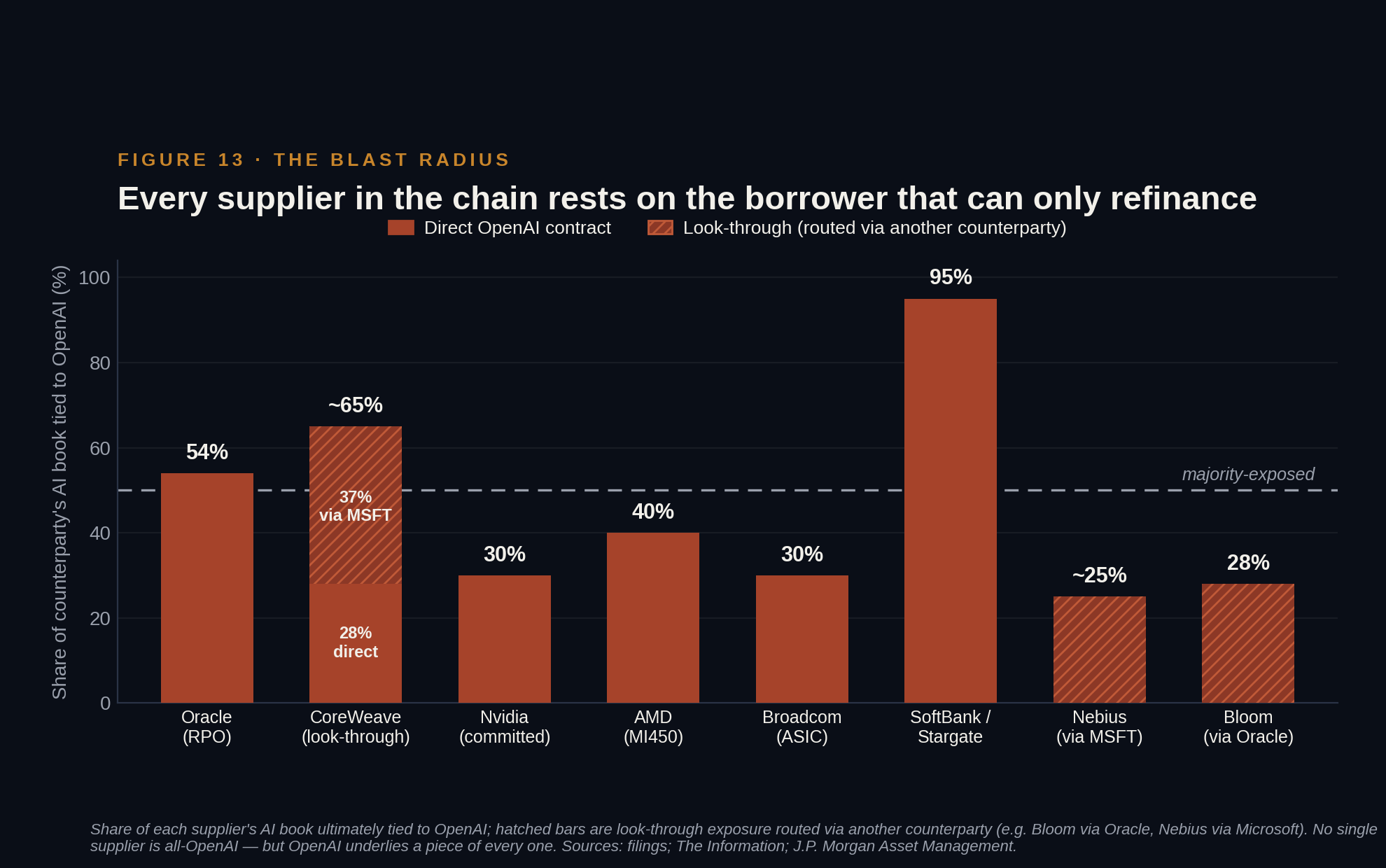

OpenAI is the single largest customer - by direct contract or one counterparty removed - of very nearly every name that sells into the AI build. Oracle’s contracted backlog is more than half OpenAI; CoreWeave’s book - once its Microsoft-routed capacity is traced through to the underlying tenant - runs to roughly two-thirds OpenAI; SoftBank’s commitments, through Stargate, are almost entirely OpenAI.

This is precisely the structure that made 2008’s senior tranches lethal: thousands of individual mortgages, geographically dispersed, statistically independent - until the one macro variable they all depended on, national home prices, turned, and the correlation the models had assumed away revealed itself to be one. Here the single variable is not home prices. It is whether OpenAI can clear its next mark. That is why chip stocks fell when OpenAI signaled it may delay its IPO from 2026 to 2027.

A correlation of one is invisible until it is tested. Then it is a transmission line. When the borrower at the center cannot clear its next mark, the loss does not stay put - it runs the length of the chain, into every counterparty that booked its commitment as demand. The naked borrower is not merely the weakest credit in the complex. It is the credit the complex is wired to.

That correlated exposure is now being securitized. In May 2026, CoreWeave closed its DDTL 5.0 facility - $3.1 billion, issued through a bankruptcy-remote financing subsidiary. CoreWeave disclosed that the underlying capacity serves two large, non-investment-grade customers: OpenAI and Cohere. But the distinction that matters is structural: DDTL 5.0 was the first publicly syndicated GPU-backed facility, built to trade in the secondary market. The paper has left the originator’s balance sheet and entered the broad credit complex - the distribution step, the moment originate-to-distribute stops being a metaphor.

The DDTL isn’t serviced by OpenAI’s earnings; it’s serviced by OpenAI’s ability to keep raising, which is underwritten by the AI capex narrative continuing to compound.

X. The Refinance of Last Resort

Trace the refinancing chain to its end and you arrive at the public market. Private capital is deep but finite: SoftBank, the sovereign funds, the hyperscalers, the megafunds - each can absorb a round or two, but the labs’ burn is measured in tens of billions a year and compounding, and at some point the only pool of capital large enough to keep refinancing it is the one the index funds and the retail bid sit in.

The IPO is not an exit in this structure. It is the refinancing of last resort - the final, deepest teaser into which the whole edifice expects to roll once the private rounds can no longer carry the burn. Which is why news of OpenAI’s delayed IPO matters far more than the market initially understood.

The terminal refinance carries a trap the private rounds did not. To reach the public pool the borrower must file an S-1 - and the S-1 discloses exactly the fragility that made the refinance necessary: audited losses, customer concentration, the full $600 billion-plus of take-or-pay obligations laid out for any reader. The document that unlocks the capital is the same document that prices the risk.

OpenAI needs the market’s money and cannot fully afford the market’s scrutiny - the bind of a company whose story is better than its statements.

Now do the arithmetic the delay is hiding. The step-up from roughly $852 billion to the reported >$1 trillion target is the next hurdle - barely 1.23×, the lowest step-up in the entire sequence, and far below the 1.7×–1.9× multiples that funded the prior burns. It must do two incompatible things at once: clear at a level the public market will actually pay, and raise enough to retire a cumulative burn approaching $115 billion. The implied step-up cannot do both: the price that clears the market does not retire the burn, and the price that retires the burn does not clear the market. The refinance of last resort is failing quietly - pricing below the mark the structure requires, and waiting.

XI. How It Breaks

The trigger is narrow and specific: the next mark fails to clear at the required step-up - not a collapse, merely a deceleration below the threshold the structure needs. This is the 2006 dynamic replayed: the velocity rolled over while the level was still climbing.

From there the sequence runs in order:

(1) The terminal refinance prices below the required mark - the step from about $852 billion to more than $1 trillion does not clear, or clears at a level that cannot retire the burn; the delay is the signal. (2) The borrower pulls back on compute commitments to conserve cash - and a pull-back on a take-or-pay obligation is a covenant breach against the provider whose debt is collateralized by that commitment. (3) The breach lands first and hardest on the neoclouds - CoreWeave, Lambda, Crusoe - whose entire business is the spread between borrowed money and resold compute. A neocloud is not a business so much as a spread trade with no balance sheet to warehouse the risk: when the spread inverts, it is insolvent by definition, not by choice. Oracle, corporate-funded but dangerously concentrated, takes the next blow - its impairment deeper than the hyperscalers’, but it does not seize; it bleeds. A hyperscaler can fund a missed payment out of Search, or Windows, or Retail; the neocloud has no second cash flow. (4) Credit freezes across the complex: RPO reprices from forward demand to counterparty risk, GPU-backed notes cannot roll, the originate-to-distribute machine seizes. (5) Equity decimates - negative convexity in reverse, capex repriced from option to cost, multiples compressing across every name in the chain. (6) The strong survive: the best-capitalized actors with the least exposure buy stranded data centers for pennies and backstops the leases that must endure.

A necessary concession: I do not know when. The trigger could be quarters away or further; the borrowed-time window between the second derivative rolling over and the first derivative crossing zero can stretch further than any short-seller’s patience. There are three stretches that can extend it: a larger-than-expected private round, a sovereign or strategic backstop that postpones the terminal refinance (like an Intel-style federal equity stake), and the hyperscalers’ continued ability to lever up - borrowing against the very backlog this article has described.

The last of these is the most powerful near-term stabilizer, because the hyperscalers have real balance sheets, real cash flows, and real access to debt markets. But it is not infinite. Investment-grade leverage across the group has already doubled in a year and the rating agencies have only so many notches left. The sequence above is not a calendar; it is a mechanism, conditioned on a single variable - whether growth decelerates below the rate the refinance requires. But with OpenAI’s IPO already delayed, the clock is ticking.

XII. The Strongest Case Against This

Grant the bulls their strongest case: demand is real, backlogs are exploding, inference is in its infancy, and the risk of underbuilding a generational platform is acute. Supply is locked years out, and even skeptics see paths to $1.4 trillion in annual capex. I take this case seriously - but it does not save the structure.

Every bull claim is about the level or the first derivative: backlogs, inference ramping, supply growth. Not one speaks to the second derivative. I do not need demand to fail. I need the rate of capex growth to flatten - and a structure this levered and dependent on perpetual acceleration breaks on the flattening alone. Grant every level argument. Housing demand was real in 2006 - and the financing detonated on deceleration, not the level.

There are three bull cases to address.

First, the fortress balance sheet. Hyperscalers generate enormous cash flow; a tenant impairment is absorbable. This misses the wound. The impairment is accounting; margin collapse is structural. AI capacity carries a massive fixed-cost base - depreciation, power, interest - that does not flex when a tenant defaults. Utilization drops, but opex does not. Revenue falls, yet costs remain anchored to the peak build. The same operating leverage that supercharged profits now destroys margins on the way down.

Second, the cross-subsidization defense. If AI margins crater, Search and Windows cash flows carry the division. The rebuttal is the conglomerate discount. Investors buy hyperscalers for growth, not to subsidize perpetual losses. If AI consumes tens of billions without profitability, consolidated ROIC declines. A high-ROIC growth compounder that becomes a low-ROIC capital-intensive operator loses its growth premium and trades down to a utility multiple. Worse, legacy cash cows are not infinite engines. Search faces structural erosion; Retail operates on thin margins; Windows is mature. Using shrinking profits from declining units to fill vacancies is not patient capital - it is value destruction. The conglomerate trades as a utility with a venture capital problem, commanding a lower multiple.

Third, the physical rebuttal: if OpenAI defaults, the provider re-leases the capacity. This is the “housing never loses value” argument of 2006. An OpenAI default will not occur in isolation - it will coincide with a broader deceleration, meaning hyperscalers bring gigawatts online into a softening environment. You do not re-lease into a glut; you compete on price, and the clearing price falls below the debt-service coverage ratio. The replacement tenant, facing the same decelerating demand, will demand a 30–50% discount and a shorter commitment, turning a long-duration, high-yield asset into a distressed instrument. Re-leasing merely transforms a clean default into a prolonged vacancy crisis - the same mechanism that turned 2007’s subprime “re-performance” hopes into a five-year grind.

The bulls and I do not disagree about AI. We disagree about which derivative the structure is written on. They are watching the level. I am watching its acceleration. That is not a difference about technology. It is a difference about arithmetic - and arithmetic, eventually, does not take opinions.

XIII. The Number Nobody Watches

Three errors, stacked, recreate 2008. The market is pricing AI as a technology cycle when its financing is the machinery of a credit-and-real-estate cycle. It is watching the level and the velocity while the structure breaks on the acceleration. And it is treating a concentrated, single-borrower loan book as though it were diversified forward demand. Each error alone might be survivable. Together they reconstruct, feature for feature, the conditions of the last great credit event - the same negatively convex structures, the same originate-to-distribute plumbing, the same correlation-of-one hiding inside the appearance of diversification, the same blindness to the one derivative that matters.

The law from the opening sections holds, unchanged: any structure whose serviceability depends on refinancing into growth does not need a decline. It needs only a deceleration. That deceleration is already happening.

The market remembers 2008 backwards. The defaults didn’t come when prices fell. They came when prices stopped rising faster - and this build-out is engineered, with exquisite precision, to break on the one number nobody watches.

The Second Derivative.

Read Our Most Popular Posts Here:

This is not investment advice, not a recommendation to buy or sell any security, and not a solicitation. The author may or may not hold positions in companies or themes discussed.

Another brilliant one. I thought "Peak Cheap" was real good and you just raised the bar higher. Thank you, I am learning so much 🙏

And right on cue, OpenAI proposes a 5% stake by the federal government.