Peak Cheap: The AI Boom Isn't 2000, It's 2008

Anatomy of the GPU-collateralized earnings bubble and the coming credit unwind

Look at the AI boom through the only lens most investors trust - the P/E multiple - and nothing screams bubble. Nvidia trades in the low thirties on forward earnings, a hair above the broad market for a company compounding at rates the broad market can only envy. The hyperscalers - Microsoft, Alphabet, Amazon, Meta - sit in the low-to-high twenties, roughly where mega-cap quality has always sat. CoreWeave, the purest pick-and-shovel play in the group, changes hands at about nine times sales while growing its top line 112% a year. By the standard of 2000, this is sobriety itself. In March of that year Cisco traded near 150 times earnings and Microsoft near 70 times earnings. There is none of that here.

That is precisely the problem.

The bull and the bear are looking at the same screen and reading opposite stories, and the reason is that they disagree - without quite saying so - about what kind of top this is. The bull sees reasonable multiples on real, growing, GAAP earnings and concludes there is no bubble. The bear should see reasonable multiples on real, growing, GAAP earnings and ask the only question that matters: are those earnings real in the sense of durable, or real only in the sense of reported?

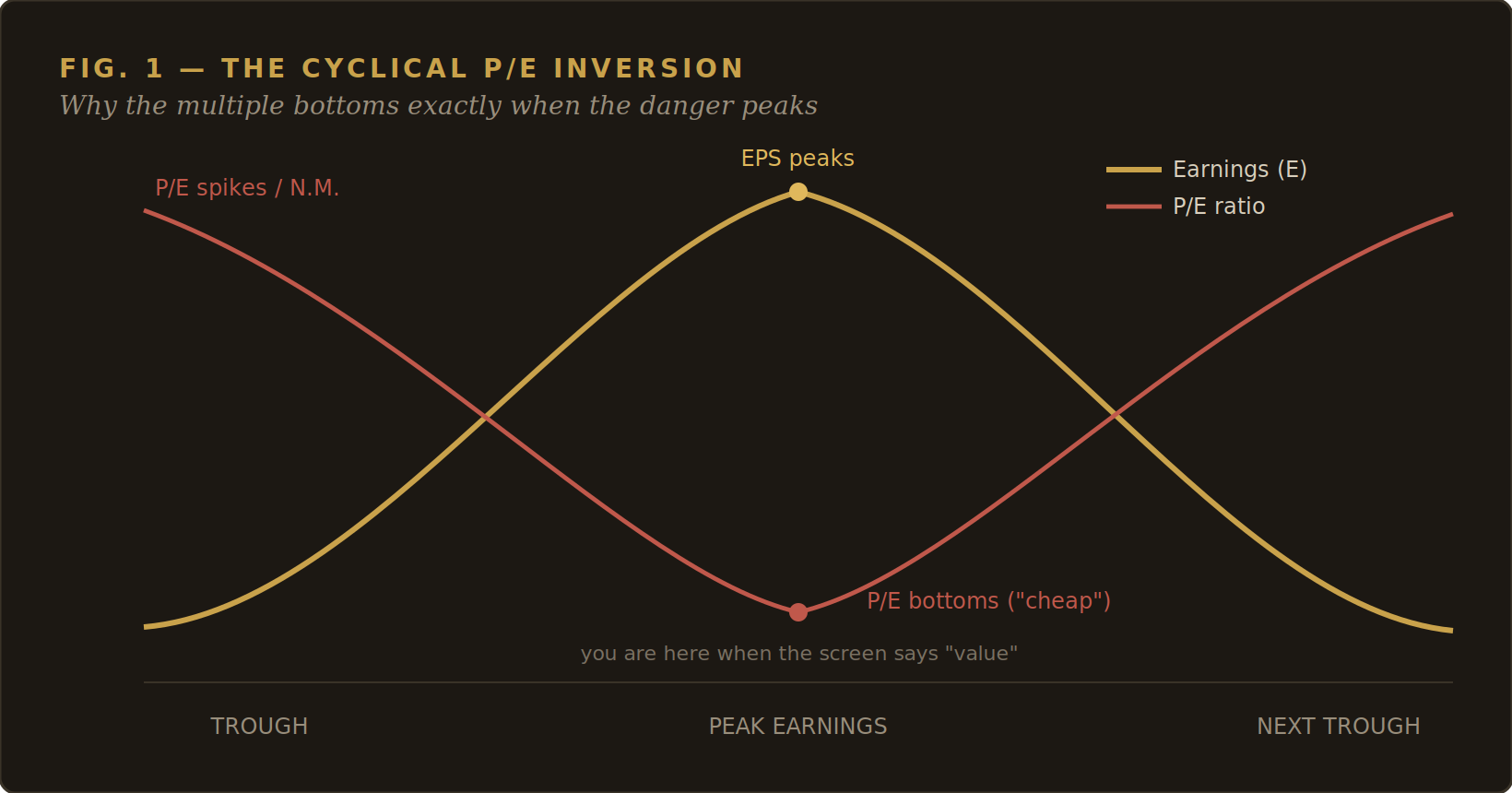

They are not the same thing. They were not the same thing in 2007, when the most profitable, most admired, most heavily owned sector in the S&P 500 was the banks - and the banks traded at single-digit P/Es. Citigroup, Lehman, Bear Stearns, Washington Mutual, the housing agencies: all of them looked cheap, and all of them were cheap, on reported earnings. The earnings were GAAP-compliant, audited, signed. They were also the product of a credit cycle at its peak - gain-on-sale accounting that booked years of profit at origination, loan-loss provisions held at cyclical lows because almost nobody was defaulting yet, and a securitization machine that paid a fee at every node. The multiple was low because the E was high, and the E was high because it was borrowed from a future that had not yet arrived.

Moody’s traded mid-twenties times earnings growing EPS 30% - about where the hyperscalers sit - and fell more than 75%; the homebuilders changed hands at roughly six times, where chip names trade now, and fell about 80%. The danger never looked expensive.

This is the single most counterintuitive fact in markets, and it is the spine of everything that follows: for a business whose earnings are cyclical, the multiple bottoms exactly when the danger peaks. At the top of the cycle, earnings are maximized, so price divided by earnings is minimized. The stock has never looked cheaper on the screen and has never been more expensive on the through-the-cycle math. Peter Lynch put it plainly a generation ago - with cyclicals you buy at high P/Es and sell at low ones, because a low P/E on a cyclical is not a margin of safety. FIG 1 is that idea in a single picture.

The argument of this article is that the AI and semiconductor complex is an earnings bubble of exactly this kind - that its earnings are not merely cyclical but partly circular and partly an accounting choice - and that, like 2008 and unlike 2000, the whole structure is being financed with debt against collateral that does not behave the way the debt assumes. Get the diagnosis wrong and you will buy the cheap multiple and call it value. It’s not value. It’s peak cheap.

Two Anatomies of a Top

To see why the distinction matters so much, set the two great tops of the modern era side by side as clinical specimens.

2000 was a numerator bubble. The excess lived in the price. Companies with no earnings, sometimes no revenue, occasionally no product, were handed valuations that made sense only if you ignored arithmetic. Price-to-sales ratios of twenty and thirty were ordinary; price-to-earnings was frequently undefined, because there were no earnings to divide by. The bubble was visible to anyone willing to look, which is why the people who called it - Julian Robertson, who refused to play and closed his fund; Jeremy Grantham, defensive years early - were early, right, and unpopular for being both. When it broke, the mechanism was simple: multiples compressed toward fundamentals, and where there were no fundamentals, the price went to zero. The Nasdaq fell 78%. It was brutal for equity holders. But - and this is the part that matters - it was mostly an equity event. The dot-coms were financed with equity: IPO proceeds, venture money, stock. When the equity evaporated, the people who owned the equity lost, and the banking system was barely scratched. A numerator bubble deflates. It does not detonate.

2008 was a denominator bubble. The excess lived in the earnings - and the headline financials looked cheap, which was the disease, not the symptom. What inflated the E was a combination of leverage (a dollar of equity supporting thirty of assets), accounting that pulled future income into the present (gain-on-sale, mark-to-model, Level 3 marks that only ever went up), and provisions for loss held at levels that made sense only if the good times were permanent. The bank that earned a record profit in 2006 had not become a better bank; it had ridden a credit cycle and booked the upswing as if it were permanent income. And the whole edifice was debt-financed. The mortgages were debt; the structures stacked on top - RMBS, CDOs, CDO-squared - were debt sliced and re-sliced; the institutions holding the paper were leveraged. So when the E reversed - when provisions had to triple, the marks had to come down, and the gains-on-sale became losses-on-everything - the debt did not reverse with it. It stayed at par, sitting on collateral now worth a fraction of the loan, owned by entities that had to sell because they were leveraged and the margin clerk was calling. That is a solvency event. It does not deflate. It cascades.

Here is the fork, then, stated as plainly as I can. A bubble in price, financed with equity, produces a painful but contained deflation. A bubble in earnings, financed with debt against impaired collateral, produces a credit cascade. In a 2000 you wait, you survive, and you buy the survivors - the Amazons - for the next twenty years. In a 2008 you worry about who is solvent, because the question is no longer what a thing is worth but whether the entity that owns it will be forced to sell it into a market with no bid.

So which is the AI complex? The multiple cannot tell you - that is the whole point. The answer lives in two questions the multiple cannot answer. First: are the earnings durable, or are they peak-cycle earnings boosted by accounting and by demand the sellers are themselves funding? Second: how is the build financed - with equity that absorbs a loss quietly, or with debt against assets that depreciate faster than the loans amortize? The rest of this note works through both. The short version is that the earnings are boosted on at least three fronts at once, and the financing has, over the past eighteen months, migrated decisively from equity toward debt - toward delayed-draw term loans secured by GPUs, toward investment-grade rated bonds issued by bitcoin miners against neo-cloud leases, toward project finance near 100% loan-to-cost. The complex is acquiring, deliberately and at speed, exactly the qualities that made 2000 a footnote and 2008 an epoch.

The Overearning Engine

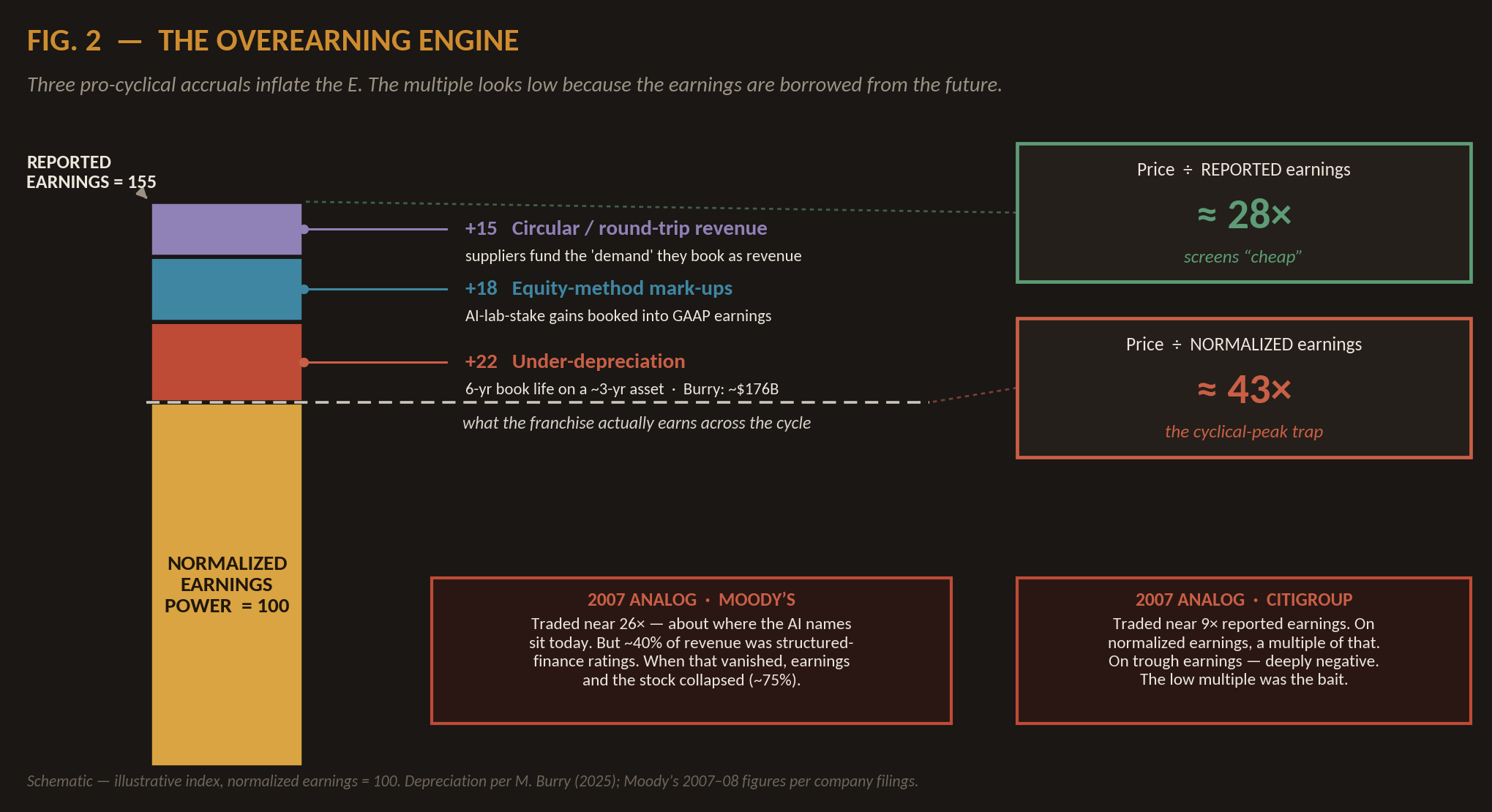

If the earnings are the problem, we should be specific about how they are inflated. Three mechanisms are operating at once, and the important thing about all three is that they are pro-cyclical accruals - they boost reported earnings in the good times and reverse, often violently, in the bad.

The first is under-depreciation - the asset-side accrual, and the cleanest. When a company buys a forty-thousand-dollar GPU it does not expense it at once; it spreads the cost over the asset’s “useful life” as depreciation. Choose a longer life and each year’s charge is smaller, so reported profit is larger - for the identical asset, the identical cash outlay, the identical economic reality. Between 2020 and 2024 the hyperscalers, almost in unison, extended the assumed life of their servers from three or four years to five or six. By one industry estimate the change saved the group on the order of $18 billion a year in depreciation - $18 billion of additional reported pretax profit conjured by an assumption. The trouble is that the assumption is, on the evidence, wrong. Nvidia ships a materially faster, more power-efficient architecture every eighteen to twenty-four months, and each generation makes the last one economically obsolete long before it is accounting-obsolete. You can watch it in the rental market, the closest thing to a live quote on a GPU’s economic value: an H100 that rented for roughly $8 an hour in 2023 rents for something closer to $2.35 today. That is the asset shedding more than 40% of its earning power a year while the books mark it down at about 17% - one-sixth a year on a six-year line. The gap between those two numbers is pure overstatement of profit, deferred until reality forces the reckoning.

We are no longer speculating about this. In 2025 the practice cracked into open disagreement - the “great divergence.” Amazon, to its credit, shortened the life on a subset of its fleet and took a roughly $700 million charge for the privilege of telling the truth. Meta went the other way and extended again, toward five and a half years. Microsoft’s Satya Nadella, asked about it, all but said the quiet part: that he did not want to be “stuck with four or five years of depreciation on one generation.” Michael Burry, who has some standing on the question of whether the consensus can be comfortably and profitably wrong, put a number on it - shorten the industry’s GPU lives from the five-to-six years now assumed toward the two-to-three the replacement cycle implies, and you understate depreciation, and therefore overstate profit, by something like $176 billion across 2026 to 2028, enough to leave reported operating income at firms like Oracle and Meta more than 20% above economic reality. His analogy was not Enron. It was Cisco at the 2000 peak - not fraud, but exuberant spending and optimistic assumptions that later unwind. In 2008 terms this is under-provisioning for loan losses. A bank in a boom takes minimal provisions because nobody is defaulting yet, and reports fat earnings; when the cycle turns it must provision for all the losses at once, and years of “earnings” reverse into a single quarter’s charge. Under-depreciating a GPU is the same move - deferring a known, eventual cost to flatter the present - performed on the asset side of the ledger instead of the liability side.

The second accrual is equity-method and fair-value mark-ups on AI-lab stakes - the non-cash GAAP accrual. The hyperscalers own large positions in the model labs: Microsoft in OpenAI, Alphabet and Amazon in Anthropic. When a lab raises a new round at a higher valuation, the holder books a gain - often a very large, entirely non-cash gain - that flows through to GAAP earnings. Tens of billions of dollars of reported “profit” across recent periods has this character: it is not cash from selling a product, it is the mark-to-market of a private holding that has only ever marked up. The trouble, again, is symmetry. The mark that rises on the way in falls on the way out, and it falls precisely when the lab’s prospects dim - which is precisely when everything else in the complex is dimming too. In 2008 terms it is gain-on-sale and mark-to-model - the CDO desk that booked a structure’s projected lifetime profit at the moment of creation, on a model, and watched the “gain” become a loss when the model met the world.

The third accrual is the hardest to see and the most important: circular, round-trip revenue - the demand-side accrual. A meaningful and rising share of the “demand” in this complex is funded by the same companies that book it as revenue. Nvidia sells chips to CoreWeave and separately invests two billion dollars of equity into CoreWeave. Microsoft invests in OpenAI, and OpenAI commits to spend hundreds of billions at Microsoft’s cloud. Google funds Anthropic, Anthropic commits fifty billion dollars to a neocloud, and Google guarantees that neocloud’s leases. In each case capital flows out from one node and returns as another node’s revenue - revenue the market then capitalizes as if it were ordinary, exogenous, end-customer demand. It is real, it is contracted, it is legal. It is not exogenous. It is the capital cycle feeding itself, and the margin earned on that circular flow is the third layer of inflation in reported earnings. In 2008 terms this is the fee income of the originate-to-distribute machine - origination, securitization, structuring fees, all booked on volume that the next node in the chain was funding, the whole apparatus manufacturing its own throughput. The fees were real until the day the end-borrower stopped paying, at which point the volume - and the fees - vanished.

Stack the three and you have the overearning engine. Reported earnings are normalized earning power, plus an under-depreciation layer, plus a mark-up layer, plus a circular-revenue layer. The market sees the top of the stack, divides the price by it, and gets a multiple that looks reasonable - cheap, even. But the franchise’s durable earning power is the bottom of the stack, and the multiple that will matter when the accruals reverse is far higher. Put illustrative figures on it - index normalized earnings at 100 and let the accruals add a further 55 - and a stock that screens at 28 times reported earnings is really trading near 43 times what it earns through the cycle. And 43 is the optimistic case, because it assumes the accruals merely stop. In a real downturn they do not stop; they reverse, trough earnings go negative, and the multiple on trough earnings is not 43 or 143 but undefined - which is exactly the number Citigroup printed when its turn came.

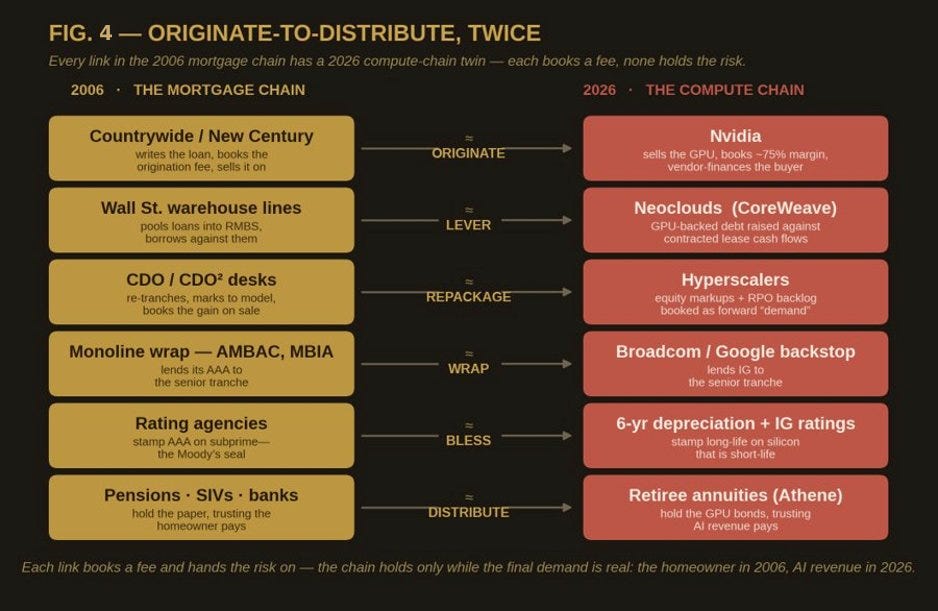

Originate-to-Distribute, Twice

If the earnings are inflated and the cash is draining, the next question is structural: how is the risk arranged? Here the resemblance to 2006 stops being an analogy and becomes a blueprint. The defining financial innovation of the last credit bubble was originate-to-distribute - the idea that the institution making a loan need not hold it. It could originate, book a fee, and pass the risk down a chain of intermediaries, each of whom took a clip and handed the parcel on, until the ultimate risk came to rest with someone - a pension fund, an insurer, a savings vehicle - who trusted the paper precisely because so many sophisticated hands had touched it. The chain worked beautifully as long as the thing at the very end - the homeowner’s ability to pay - held. When it didn’t, every link discovered it had distributed the fee and kept more of the risk than it knew.

The compute economy has rebuilt this chain link for link, and FIG 4 sets the two side by side. Start at origination. Countrywide and New Century wrote the loan, booked the origination fee, and sold it onward. Nvidia is the originator of this cycle - it sells the GPU at a gross margin near 75%, books the profit immediately, and, increasingly, finances the buyer, taking equity in the very neoclouds that purchase its chips. The originator that funds its own customers is not a new character; it is Countrywide extending the borrower credit so the borrower can take out the Countrywide loan.

Next, the warehouse. Wall Street’s warehouse lines pooled the loans and borrowed against them. The neoclouds - CoreWeave foremost - do the literal equivalent, raising GPU-backed debt against the contracted cash flows of their customer leases, levering the asset the moment it lands on the dock. Then the repackaging desk. The CDO and CDO-squared desks re-tranched the pools, marked the result to model, and booked the gain on sale. The hyperscalers play this part with their AI-lab markups and, above all, with their backlogs - remaining performance obligations booked and presented as forward “demand,” a pipeline marked to an optimistic model of the future.

Then the wrap. The monolines - AMBAC, MBIA - sold their AAA rating to the senior tranche so subprime risk could wear a triple-A coat; Google, as we are about to see in detail, plays the wrapper here, lending investment-grade credit to structures that could not stand on their own. And the rating agencies, who stamped AAA on subprime because the models said house prices could not fall nationwide, have a direct heir: the six-year depreciation schedule and the investment-grade rating that together stamp “long-lived” on silicon that is demonstrably short-lived. Finally, distribution: in 2006 the paper came to rest with pensions, SIVs, and banks who trusted the homeowner would pay; in 2026 it comes to rest with retiree annuities reaching for yield, who hold the GPU-backed bonds and trust that AI revenue will pay.

Every link in both chains books a fee and hands the risk on. And both chains hold only as long as the demand at the very end is real - the homeowner’s paycheck in 2006, the end-customer’s willingness to pay for AI in 2026. Everything upstream is plumbing. The plumbing does not generate the water.

The Circular Loop, and the Sponsor on Every Side

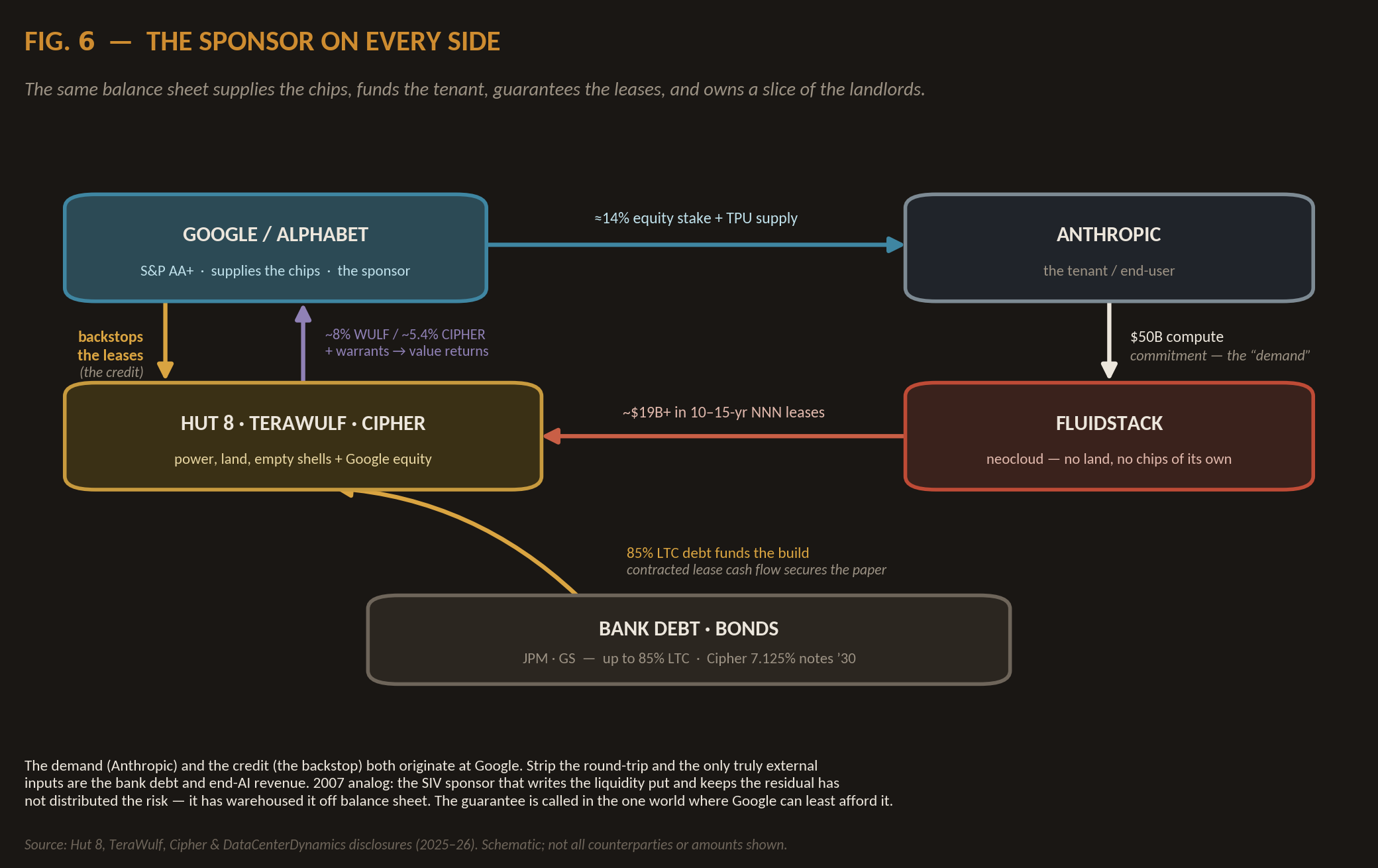

The most important link - the wrap - deserves opening up: it is where the circular and the leveraged meet, and the structure now operating around Google is as clean an illustration of warehoused risk as the last cycle produced.

Begin with the demand. Google holds roughly a 14% stake in Anthropic and supplies it with TPUs. Anthropic, in turn, has announced an approximately $50 billion partnership with Fluidstack to build data-center capacity in Texas and New York. That $50 billion is the demand that anchors everything downstream - and a meaningful part of the capital behind it traces back to Google’s own investment in Anthropic.

Now the supply. Fluidstack is a neocloud: it operates GPU clusters but owns neither the land nor, at this scale, the power and shells it needs. So it leases them, on long-dated triple-net terms, from a most unlikely set of landlords - bitcoin miners repurposing their power-and-real-estate footprints into AI hosting. Hut 8 signed a fifteen-year, 245-megawatt lease at its River Bend campus in Louisiana: $7 billion of contracted base rent, rising to as much as $17.7 billion if the extension options are exercised, with an expected cumulative net operating income of $6.9 billion over the base term and a right of first offer on a further 1,000 megawatts. TeraWulf signed for more than 200 megawatts over ten years at Lake Mariner in New York, then added a 168-megawatt joint venture at Abernathy in Texas. Cipher Mining leased the entirety of its 300-megawatt Barber Lake site - a deal that could total $9 billion of revenue - plus a further 39-megawatt slice. Run the leases together and Fluidstack has contracted on the order of $19 billion-plus of capacity, from companies that a year ago mined Bitcoin.

Here is where the wrap comes in, and here is the heart of it. None of these miners could finance multi-billion-dollar AI build-outs on their own credit, and their tenant, Fluidstack, is a private neocloud without an investment-grade balance sheet. So Google steps in as guarantor. It is backstopping Fluidstack’s lease obligations - agreeing, in effect, to assume the capacity or pay a fee if Fluidstack fails: roughly $1.8 billion of the TeraWulf obligations, about $1.3 billion of the Abernathy joint venture, around $1.4 billion of the original Cipher lease plus another $333 million as the Barber Lake deal expanded, and the full base-term backstop on Hut 8’s $7 billion River Bend lease. And Google is not doing this at arm’s length or for free: it is taking equity in the landlords too - warrants for roughly 8% of TeraWulf, about 5.4% of Cipher. The reporting on the Louisiana deal is explicit that the Google backstop was the thing that made the financing possible at all.

Only now do the lenders appear, and they appear comfortable. J.P. Morgan, as lead-left underwriter, and Goldman Sachs are expected to fund up to 85% of project cost as debt at River Bend. Cipher has issued senior secured notes - $333 million at 7.125%, due 2030 - against its piece. The banks and bond buyers are lending against contracted cash flows that look, on paper, like an investment-grade tenant’s obligations. They look investment-grade because Google made them so.

Step back and see where Google actually sits in this structure, which is everywhere at once. FIG 6 draws it. Google supplies the chips that go in the racks. It funds the tenant - through its Anthropic stake - that generates the demand. It guarantees the leases that make the projects financeable. And it owns equity in the landlords that build them. Strip out the round-trip and the only genuinely external inputs to the entire apparatus are the bank debt and the eventual AI revenue. The demand and the credit both originate at the same balance sheet.

This is the structure that did the most damage in 2008, and it did the damage precisely because it looked as though risk had been distributed when it had only been moved off the balance sheet to a place where it could be ignored until it couldn’t. The structured investment vehicle - the SIV - was a sponsor’s off-balance-sheet conduit, funded in the short-term market, holding long-term paper, supported by a liquidity put the sponsor had written and a residual the sponsor had kept. The risk looked gone. It wasn’t. When the conduits could not roll their funding, the puts were exercised and the paper came home - Citigroup alone took more than $25 billion back onto its balance sheet from vehicles it had supposedly sold. The monoline insurers were the same idea in reverse: they had written AAA wraps on tranches correlated to a single national factor, house prices, and when that factor turned the wraps were worthless at exactly the moment they were needed.

That is the term of art the Google backstop should bring to mind - wrong-way risk, a guarantee most likely to be called in precisely the scenario where the guarantor can least afford to honor it. If end-AI economics disappoint badly enough to sink Fluidstack’s ability to pay its leases, the same shock will be sinking Anthropic’s ability to pay for compute and Google’s own AI returns at the same moment. The guarantee comes due in the one world where Google least wants the bill. Correlation, when it matters, goes to one.

And lest this read as a story about one company, the same architecture is everywhere. Microsoft carries $627 billion of commercial remaining performance obligations - a backlog presented as proof of durable demand - and roughly 45% of it, about $281 billion, is a single counterparty: OpenAI, an unprofitable startup in which Microsoft itself owns 27%. Oracle has a $300 billion OpenAI commitment of the same kind; Amazon a $38 billion one. The backlog edifice the whole complex points to as evidence of real demand is, to a remarkable degree, one bet - on AI’s eventual return - wearing a great many costumes. In 2008 the costumes were tranches and the single bet was house prices. The lesson did not change: diversification across instruments that share one underlying factor is not diversification at all.

GPU Finance 101: a Three-Year Asset on a Six-Year Loan

We have established that the demand is partly circular and the earnings partly an accounting choice. The remaining question is the one that decides whether this is a 2000 or a 2008: the financing. Specifically, what happens when you lend long against an asset that depreciates short.

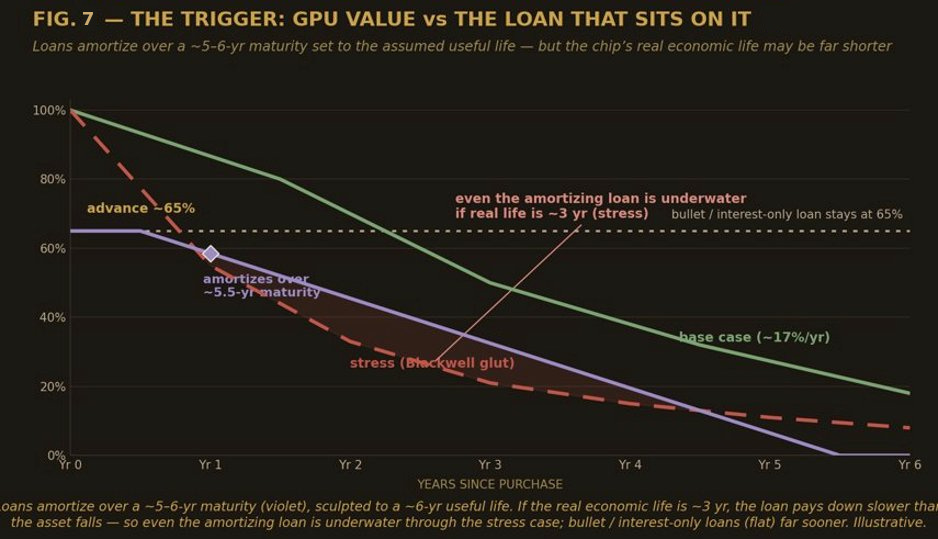

Start with the mechanics of GPU-backed debt - they are the whole game. A lender advances money against a pool of GPUs and the customer contracts those GPUs serve. A typical structure advances perhaps 65% of cost - the borrower funds the rest as equity - and the loan amortizes over a maturity set to the asset’s assumed useful life, on the order of five-and-a-half to six years. It is secured by three things: the chips, the customer contract that pays for the chips, and the data-center lease that houses them. And it carries a financial covenant - a minimum debt-service coverage ratio, the ratio of the cash the contract throws off to the debt service the loan demands. As long as the chips hold their value and the contract pays, the structure is sound.

The problem is the word assumed. The loan amortizes on a schedule sculpted to a six-year life, but the chip’s economic value - what it earns in the rental market, what it would fetch resold - declines on a different and steeper curve. FIG 7 draws the two against each other. In the base case, value erodes at roughly 17% a year, the book rate, and the asset line stays comfortably above the amortizing loan balance: the loan is covered for its whole life. But run the stress case - a Blackwell-driven glut that compresses the economic life of a Hopper-class chip toward three years, value falling nearer 40% a year - and the asset curve plunges below even the amortizing loan balance by around year three. The loan is underwater: the collateral is worth less than the debt it secures, with years left to run. And that is the amortizing case, the responsible one. A bullet or interest-only loan, which pays down no principal and sits flat at the 65% advance, goes underwater far sooner - it never builds the equity cushion that amortization slowly creates.

This is the structural error at the center of the whole complex, and it is precisely the error of 2006. A GPU is, economically, a piece of fast-obsolescing electronics - closer to a laptop than to a building. It is being financed like a building: long amortization, modest haircut, the implicit assumption that the collateral holds its value over the life of the loan. The 2006 mortgage made the same assumption about houses - that prices would rise, or at worst not fall, over the loan’s life - and built the 2/28 ARM, the option-ARM with negative amortization, and the interest-only loan on top of it. Those products were sized to an asset assumed durable or appreciating. When house prices fell 30%, the borrower had no equity, no reason to keep paying, and the collateral could not cover the loan at foreclosure. The interest-only GPU loan is the interest-only mortgage of this cycle: it works only if the asset behaves like real estate, and the asset behaves like a laptop.

No one embodies this more completely than CoreWeave, the public laboratory for GPU-backed credit. In the first quarter of 2026 CoreWeave reported $2.078 billion of revenue, up 112% year on year - and a net loss of $740 million, interest expense of $536 million, total debt of $24.859 billion, a debt-to-equity ratio near 8.9, and a current ratio of 0.46, meaning its near-term obligations exceed its liquid assets. Its backlog is a much-cited $99.4 billion, but only 36% of that is scheduled to convert to revenue within twenty-four months and 75% within four years - a long-dated promise resting on counterparties honoring multi-year commitments. The chip supplier, Nvidia, bought $2 billion of CoreWeave equity during the quarter: the vendor financing the buyer’s equity, the circular loop in miniature. And a detail easy to miss - CoreWeave’s construction-in-progress, infrastructure not yet in service, is in the company’s own words “not yet being depreciated,” which means the depreciation freight train, already undercounted per unit by the long-life assumption, has not even fully left the station. The reported loss is set to widen mechanically as the fleet comes online, before any demand shock at all.

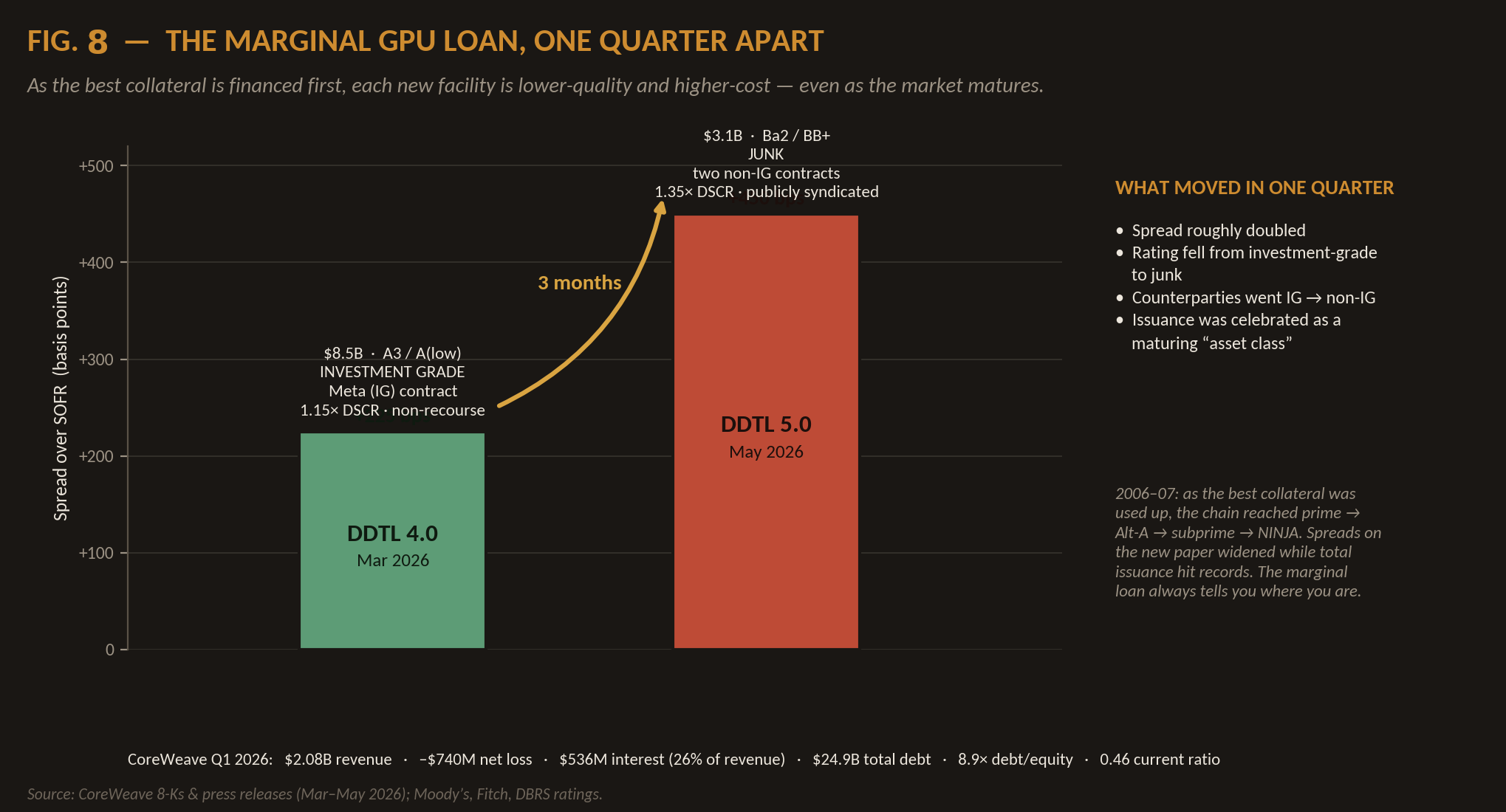

Now watch the financing, because the most damning single fact in this note is hiding in the sequence of CoreWeave’s delayed-draw term loans. A delayed-draw term loan - a DDTL - lets the borrower draw committed capital in stages as it takes delivery of chips and signs contracts, matching the funding to the deployment. CoreWeave has issued them in a ladder, and FIG 8 shows the two most recent rungs. On March 31, 2026 it closed DDTL 4.0: $8.5 billion, rated A3 / A-low - the first GPU-backed financing ever to reach investment grade - priced at SOFR plus 225 basis points, secured by GPUs and a roughly $19 billion Meta contract, structured non-recourse through a bankruptcy-remote subsidiary with a poetic name, CoreWeave Compute Acquisition Co. VIII, LLC, carrying a minimum 1.15x coverage covenant. The market hailed it, fairly, as a milestone: AI infrastructure had become an institutional asset class.

Seven weeks later, on May 18, CoreWeave closed DDTL 5.0 - and here is the tell. DDTL 5.0 was $3.1 billion, rated Ba2 / BB+, which is to say junk, not investment grade; priced at SOFR plus 450 basis points, double the spread of 4.0; secured by “two large non-investment-grade customer contracts,” a clear step down in counterparty quality; with a tighter 1.35x covenant for the privilege. In three months the marginal GPU-backed loan went from investment grade to junk, its spread doubled, and the quality of the collateral behind it deteriorated - even as the whole exercise was celebrated, again, as proof the asset class was maturing.

That pattern - issuance accelerating while the marginal deal gets worse - is the single most reliable signature of a late-stage credit cycle, and 2006 ran the same film frame for frame. As the supply of prime borrowers was exhausted, the originators reached further out the risk curve: prime gave way to Alt-A, Alt-A to subprime, subprime to no-documentation NINJA loans. Spreads on the new, riskier paper widened even as total issuance set records, because the demand for product had outrun the supply of sound collateral. The marginal loan always tells you where you are in the cycle. The marginal GPU loan is now rated junk and priced at SOFR plus 450 against non-investment-grade tenants. The best collateral has been financed. What is left is the Alt-A.

The ROI Wall

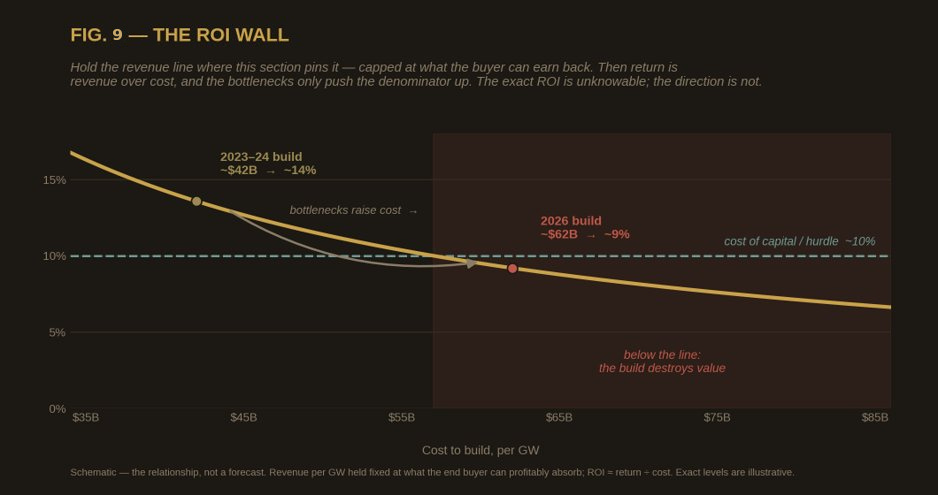

There is a counter to everything above, and it is the bull’s strongest card: yes, the financing is aggressive and the accounting generous, but it is all underwritten by demand so enormous and so real that the returns will swamp the risks. So ask the demand-side question directly - can the buildout actually earn its cost of capital? FIG 9 frames the arithmetic. Return on an AI buildout is, at bottom, the revenue the end-customer can profitably pay divided by the cost to build the capacity that serves them. The numerator is capped - not by ambition but by economics, by what the buyer of AI services can actually earn and therefore afford to spend. The denominator is rising, and rising fast, because the binding constraints are no longer chips but the physical bottlenecks around them: power, transformers, grid interconnection, skilled labor, land. The cost to build a gigawatt of capacity has gone from something like $42 billion in the 2023–24 vintage toward $62 billion in 2026, and the bottlenecks only push it higher.

Hold the numerator where economics pins it and let the denominator climb, and the return falls - through the roughly 10% cost of capital the marginal dollar must clear, and below it. Past that line the build does not earn a low return; it destroys value outright. The exact level at which this happens is unknowable, and I will not pretend to a precision the inputs do not support - FIG 9 is a schematic of a relationship, not a forecast of a number. But the direction is not in doubt. Each incremental gigawatt costs more than the last and earns no more, because the end-demand that pays for it is bounded. At some level of cumulative spend the marginal project is value-negative, and the complex appears to be approaching that level rather than retreating from it. Microsoft alone intends to spend $190 billion of capital this year.

The 2008 parallel is the marginal subprime borrower. By 2006 the housing machine had run out of people who could afford a house at an economic interest rate, so it kept the volume up by lending to people who could only “afford” the teaser rate - the artificially low introductory payment that would reset upward in two years. The demand was real in the sense that the loan got made and the house got bought; it was not real in the sense that it could survive contact with a normal cost of money. The marginal AI dollar is in the same position. A great deal of the demand is real only in the sense that one company’s capital expenditure is another’s revenue - real until the capex normalizes, which it must, because spending that cannot earn its cost of capital is, eventually, spending that gets cut. When it resets, the demand that was off the charts gets re-planned, and the revenue that justified the build goes with it.

How It Unwinds

If the trigger is not a price but a turn in returns, what does the turn actually look like? Not, I think, like 2000 - not a single dramatic day with a visible top everyone later agrees was the peak. An earnings bubble does not ring a bell, because there is no absurd price to point at; the multiple looks reasonable right up until the E that anchors it gives way. The unwind is a sequence, and because the demand was partly circular, the same circularity that manufactured earnings on the way up unmanufactures them on the way down. It is reflexive, in George Soros’s sense: the financing and the fundamentals feed each other, both ways. FIG 10 traces the forward sequence; let me walk it as a causal chain.

It begins where FIG 10 ends: end-AI return disappoints relative to the capex assumption, and the marginal circular dollar stops circulating. It shows up first as a deceleration. Then the marks reverse. Alphabet and Amazon mark their AI-lab stakes down, and the tens of billions of non-cash GAAP “earnings” those markups contributed run in reverse - the very line, identified in section three, that flattered reported profit on the way up. Lower earnings and a weakening return story together undercut the justification for the capital budgets, and the hyperscalers trim capex; the demand that was off the charts gets quietly re-planned. That re-planning hits the chip order book - Nvidia’s growth decelerates, days-sales-outstanding lengthen as customers take longer to pay, and tens of billions in supply commitments and rising inventory turn into write-down risk. With the buildout’s anchor demand softening, the rental market - built out for circular demand that is now receding - meets a normalizing market, and GPU rents fall. And GPU rents are the load-bearing variable for every neocloud loan.

Here the structure of section seven detonates. As rents fall, neocloud cash flow drops below debt service; the coverage covenant breaks; “negative NOI” forces prepayment or default, and the GPUs are dumped into a thin secondary market. Each forced sale marks down resale values and rental rates for everyone, which cuts the collateral value and coverage on every other loan in the system - tripping the next covenant, forcing the next sale. This is the forced-seller cascade, and it is 2008 exactly: the margin call that forces the sale that lowers the price that triggers the next margin call. In the last cycle the collateral was mortgage paper and the leverage sat in the banks and the SIVs; in this one the collateral is GPUs in a market with few buyers and the leverage sits in the neoclouds and the project-finance structures. The mechanism is identical. And at the end of the chain, the feature that makes an earnings bubble so much worse than a price bubble: valuations fall, the labs cannot raise their next round or honor their cloud commitments, and the backlogs - Microsoft’s $281 billion, Oracle’s $300 billion - are revealed as contingent promises rather than contracted certainties. The backlog goes to fiction. The debt stays real. That asymmetry - equity and backlog evaporate, debt does not - is the whole difference between a deflation and a cascade.

The reason this can run a long way before it is widely recognized is the same reason the diagnosis matters. We are trained by 2000 to look for a bubble in the price, and there isn’t one in the price - so the screens stay calm and the value investors, reading low multiples, step in to buy what looks cheap, providing the marginal bid that lets the insiders and the early lenders step back. By the time the earnings are visibly impaired, the cascade is already running, because the financing decisions were made years earlier against collateral that was always going to depreciate. The bell, such as it is, does not ring at the top. It rings on the way down, in the form of a covenant breach.

What It Means, and What Would Make Me Wrong

Pull it together. The AI and semiconductor complex does not look expensive on the only metric most investors trust, and that is not reassurance - it is the diagnosis. This is an earnings bubble, not a price bubble: the excess is in the denominator, in earnings flattered by under-depreciation, by non-cash markups, and by demand the sellers are funding themselves; and unlike the equity-financed mania of 2000, this one is being built with debt - DDTLs, neocloud and miner bonds, project finance at 85% loan-to-cost - against collateral that depreciates like electronics and is documented like real estate. Overstated earnings, financed with debt, against impaired collateral, with the demand and the credit circling back to the same few balance sheets: that is not the architecture of 2000. It is the architecture of 2008. And the cruelest feature of an earnings bubble is the one we began with - it is mispriced precisely because it is cheap-looking. The low multiple is the trap. Do not buy peak earnings at a peak multiple of true earnings and call it value.

Intellectual honesty requires stating the other side as strongly as I can, because a thesis you cannot argue against is a position, not an analysis. Here is what would make this wrong. First, end-AI revenue could inflect - if enterprises and consumers begin paying for AI output at a scale and margin that clears the ROI wall, the “circular” dollar becomes genuinely exogenous, the backlogs convert to cash, and what looks like round-tripping is revealed as ordinary early-stage demand financing, the way every platform was once seeded. Second, the chips could hold their value - if inference demand grows fast enough to soak up older GPUs and keep rental rates firm, the six-year assumption is roughly right, the collateral holds, and the amortization-mismatch argument loses its force. Third, the debt could be better-structured than the bears fear - more termed-out, better-covenanted, with more equity beneath it and less forced-seller reflexivity than 2008, so that even a downturn produces orderly losses rather than a cascade. Fourth, the balance sheets behind the backstops are genuinely enormous - Google can in fact absorb its lease guarantees, and the hyperscalers can write down their stakes and keep spending, so the wrong-way risk, while real, is survivable without contagion. Each of these is plausible. The most important is the first: this entire bearish edifice rests on the proposition that end-demand will not arrive fast enough to validate the capex, and if that proposition is wrong, the thesis is wrong.

But notice where even the bull case sends you. Every one of those bullish outs runs through physical reality - through power and land and transformers and the cost to build a gigawatt. The ROI wall is a denominator problem, and the denominator is made of atoms whose costs are rising faster than the returns meant to justify them.

Here is where the 2008 rhyme actually finishes - and it isn’t with the neoclouds. In 2008 the losses didn’t stay with the brokers who wrote the bad loans; they were packaged, tranched, stamped investment-grade, and sold to institutions that believed they were buying safety. The same machine is running. The buildout is financed off balance sheet, through special-purpose vehicles and triple-net leases; the debt is securitized into data-center asset-backed bonds - a market up roughly eightfold in five years, data centers now behind the majority of new issuance - and the marginal buyer of the senior, “investment-grade” paper is the life-insurance and annuity complex, funding it with sticky retirement money. Athene anchored Meta’s $29 billion data-center financing before Apollo syndicated the rest to other insurers and pensions. That is the AIG seat of this cycle: the regulated, levered, “safe” holder of senior exposure to collateral that depreciates faster than the loan against it and is worth little if the demand it was built for proves circular. A structured-finance lawyer who litigated the last crisis would call these structures déjà vu.

And the loudest tell is who’s preparing. Apollo - which built the model - is running off its CLO book and sitting on a $40 billion cash pile, CEO Mark Rowan says they are preparing its balance sheet for a period of systemic instability. They are probably right about themselves. That is the point. The risk was never that the smartest underwriter blows up; it is that the model went systemic, the paper was distributed to holders far less nimble than the originator, and the one firm that understands the collateral best is quietly raising cash for the day it impairs. When the originator is hoarding dry powder against the assets it just sold you, that is the tell.

See through what only looks safe - the distributed carry, the investment-grade tranche on circular demand, the bottleneck dressed as a hedge; hyperscaler growth, the data center, the transformer, the chipmaker - all long the same boom, diversification that diversifies nothing.

The screen says value. It is worth remembering that in 2007 the screen said the same thing - about Citigroup, at nine times earnings, weeks before the earnings that anchored the multiple turned out to be the most expensive cheap stock in the market. The multiple was never the margin of safety. It was the bait. Peak cheap.

This is not investment advice, not a recommendation to buy or sell any security, and not a solicitation. The author may or may not hold positions in companies or themes discussed. Do your own work.

Excellent analysis. Berkshire Hathaway recently bought 10B worth of Google shares at 350/share in private placement. Surely they are aware of everything mentioned here. Are they betting that this will all work out for them in the long run? Or, did the new CEO succumb to AI FOMO?

Very thorough and well founded analysis. Another interesting aspect is the evaluation of the limits of possible AI demand. My fear is that AI may turn out be a giant machine that converts energy and matter into waste heat, slop, shitty code, and porn. There will be some real value of course, but the EROI of the whole system may turn out to be negative, limiting demand and usefulness. On the other hand, if AI turns out to be ultimately useful, it will lead to severe unemployment,, which in turn will decrease consumer demand and feed back into limited end demand - corporations can save labor costs, but who will they sell their products to, if they destroy consumer demand in the process?