U-Haul (UHAL) | Part 1: Misunderstood Self Storage Portfolio

40%+ NAV Discount | The Self-Moving Business is Free

U-Haul Holding Company (UHAL) is one of the most misunderstood large-cap equities in the U.S. market. Trading at approximately $49.84 per share as of March 2026, representing a market capitalization of roughly $9.8 billion (across ~196 million total equivalent shares including both voting and non-voting classes), the stock trades at a significant discount to the replacement cost and private-market value of its underlying assets. The company sits at the intersection of three powerful economic themes: self-storage real estate, the American mobility ecosystem, and portable storage disruption. Yet the market prices it as if it were merely a cyclical truck rental company suffering through a temporary earnings trough.

The core thesis is straightforward: the market is anchoring on GAAP earnings that are depressed by a temporary fleet depreciation cycle, while ignoring the massive real estate empire U-Haul has assembled over the past several years. The company has grown its self-storage portfolio from approximately 50.4 million net rentable square feet in 2022 to 98.0 million square feet as of December 2025, a near-doubling that represents billions of dollars in embedded real estate value that does not appear on the income statement at stabilized economics. Meanwhile, the self-moving business, which generates over $3.7 billion in annual revenue, functions as a massive customer acquisition engine that feeds the storage business at near-zero customer acquisition cost.

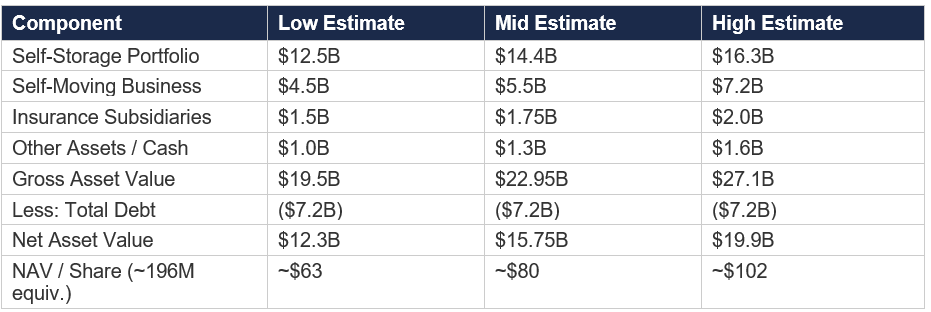

Our sum-of-the-parts net asset value analysis, conducted on an asset-by-asset basis, yields a fair value range of approximately $85 to $120 per share, representing 70% to 140% upside from the current price. The primary sources of value are the self-storage portfolio (valued at $12.5 to $16.3 billion using conservative cap rates), the self-moving franchise (valued at $4.5 to $6.0 billion on normalized EBITDA), the insurance subsidiaries ($1.5 to $2.0 billion), and the U-Box portable storage business ($1.0 to $1.5 billion), net of approximately $7.2 billion in debt.

This is not a momentum trade or a macro bet. It is a fundamental re-rating opportunity driven by the passage of time as new storage properties lease up, fleet depreciation normalizes, and the market begins to appreciate the quality and scarcity of U-Haul’s combined platform.

I. Company Overview & Business Architecture

U-Haul Holding Company, formerly known as AMERCO, was founded in 1945 by Leonard Shoen in Ridgefield, Washington. The company operates through three reportable segments: Moving and Storage (the dominant segment, contributing over 95% of revenue), Property and Casualty Insurance (through Repwest Insurance Company), and Life Insurance (through Oxford Life Insurance Company). The Moving and Storage segment itself contains several distinct businesses that are deeply synergistic.

The Self-Moving Equipment Rental Business

U-Haul is the undisputed number one do-it-yourself moving company in North America, operating through a network of more than 25,000 locations across all 50 U.S. states and 10 Canadian provinces. The fleet as of the most recent reporting period includes approximately 203,800 trucks, 137,400 trailers, and 45,900 towing devices. In fiscal year 2025 (ending March 31, 2025), self-moving equipment rental revenues totaled approximately $3.77 billion, representing roughly 65% of consolidated revenue.

What makes the self-moving franchise particularly valuable is its network density and brand recognition. U-Haul’s 25,000+ locations mean there is almost always a convenient pickup and drop-off point within a few miles of any customer in the United States or Canada. This dense network creates a powerful network effect: the more locations U-Haul has, the more convenient it is for customers, which drives more transactions, which justifies more locations. No competitor has come close to replicating this network. The closest competitor, Penske, operates fewer than 2,700 locations.

The self-moving business also benefits from an asset-light distribution model. Only about 2,300 of U-Haul’s 25,000+ locations are company-operated centers. The vast majority are independent dealers, from gas stations to hardware stores, that earn commissions for renting U-Haul equipment. This means U-Haul achieves enormous geographic coverage without bearing the full cost of real estate and staffing at every location.

The Self-Storage Real Estate Portfolio

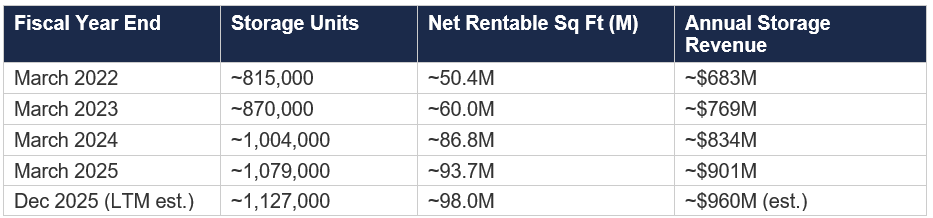

This is where the most significant embedded value lies. U-Haul is now the third-largest self-storage operator in North America, behind only Public Storage and Extra Space Storage. As of December 31, 2025, the company operates approximately 1,126,800 rentable storage units comprising roughly 98.0 million net rentable square feet. The growth trajectory has been extraordinary:

The critical insight is that much of this new square footage has been developed internally at costs far below current replacement values, and a large portion has not yet reached stabilized occupancy. Management disclosed in its FY2025 earnings call that non-same-store locations, when stabilized to 90% occupancy, are expected to generate an additional $238 million in annual revenue. Projects currently in development are projected to add another $124 million, and pending projects another $129 million. This represents approximately $491 million in embedded revenue potential that is not yet reflected in current financial results.

Same-store metrics have remained resilient despite the wave of new supply being added. Same-store occupancy was 91.9% as of fiscal year-end 2025, with revenue per square foot increasing 3.0% year-over-year. Total portfolio occupancy is lower, around 77-78%, precisely because of the flood of newly opened locations that take 24 to 36 months to stabilize. This dilution effect on total portfolio metrics is temporary and mechanical, not indicative of demand weakness.

The U-Box Portable Storage Business

U-Box is U-Haul’s portable moving and storage container product, analogous to PODS but integrated into U-Haul’s distribution network. This business has been growing at over 20% annually in recent years in both moving and storage transaction categories. Revenue from U-Box is reported within ‘Other revenue’ in the Moving and Storage segment, which grew 8.5% in FY2025 to over $500 million. The U-Box business benefits from the same distribution advantages as the self-moving business: U-Haul can deliver, store, and transport U-Boxes through its massive network of locations and warehouses. Furthermore, U-Boxes stored in company warehouses can be stacked, increasing revenue density per square foot beyond what traditional storage achieves.

Insurance Subsidiaries

Repwest Insurance Company underwrites the Safemove, Safetow, and Safestor protection packages offered to U-Haul customers. AM Best has affirmed Repwest’s Financial Strength Rating at A (Excellent) with a stable outlook as of September 2025. Repwest benefits from a captive customer base and low claims ratios.

Oxford Life Insurance Company offers life and health insurance products, primarily Medicare supplement and annuity policies marketed to the senior market. AM Best has affirmed Oxford’s Financial Strength Rating at A (Excellent), though with a negative outlook reflecting broader industry headwinds in the senior insurance market. Oxford’s investment portfolio includes significant mortgage loans on self-storage facilities, which perform well given the essential nature of the underlying assets.

II. Sum-of-the-Parts Net Asset Value Analysis

The market prices UHAL on a consolidated P/E or EV/EBITDA basis, which obscures the true value of the individual business lines. A sum-of-the-parts analysis reveals the extent of the discount. Below we value each major asset on its own merits.

A. Self-Storage Portfolio Valuation

This is the single most important piece of the valuation puzzle and where the market mispricing is greatest.

Estimating Self-Storage NOI

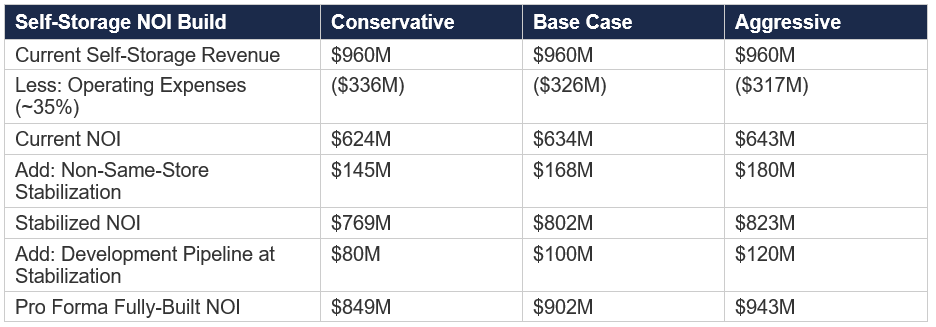

U-Haul does not disclose self-storage segment NOI directly, so we must estimate it from disclosed data. For fiscal year 2025, self-storage revenues from owned locations totaled approximately $901 million. Based on industry-standard operating expense ratios for large self-storage operators (typically 30-40% of revenue for well-managed portfolios), and adjusting for U-Haul’s lower operating cost structure due to shared overhead with the moving business, we estimate operating expenses of approximately $315 to $360 million, yielding estimated self-storage NOI of $540 to $585 million.

However, this understates the true earning power because it includes newly opened properties operating below stabilized occupancy. If we adjust for the $238 million in additional revenue expected from non-same-store locations reaching 90% occupancy (at an incremental margin of approximately 70-75%, given the largely fixed cost structure of self-storage), stabilized NOI would be approximately $710 to $765 million.

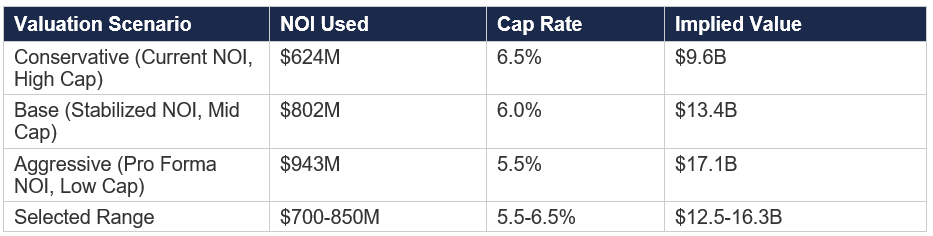

Applying Cap Rates

Self-storage cap rates have stabilized around 5.8% on average across the industry as of mid-2025, with Class A assets trading in the 5.0-5.5% range and Class B assets in the 5.5-6.5% range. Public Storage’s implied cap rate based on its market valuation is approximately 4.8-5.2%. Extra Space Storage trades at an implied cap rate of roughly 5.0-5.5%. Given U-Haul’s portfolio is a mix of newer, well-located facilities and older converted properties, we apply a blended cap rate range of 5.5% to 6.5%.

At the midpoint of our range ($14.4 billion), the self-storage portfolio alone is worth approximately 1.5x the company’s entire current enterprise value. This is the core of the investment thesis: the market is either unaware of or heavily discounting the value of U-Haul’s rapidly expanding self-storage platform.

For additional context, the industry average transaction valuation for self-storage assets has been approximately $152 to $159 per square foot over the past nine quarters. At 98 million square feet, even a conservative $130 per square foot valuation would yield $12.7 billion for U-Haul’s storage portfolio. At the more recent average of $155/sqft, the value would be $15.2 billion.

B. Self-Moving Business Valuation

The self-moving equipment rental business generated approximately $3.77 billion in revenue in FY2025, growing 2.8% year-over-year, with the growth rate accelerating through the year (4.1% in Q4). The challenge in valuing this business is the temporary depression of earnings from elevated fleet depreciation and reduced gains on equipment sales, which together reduced earnings by approximately $260 million in FY2025 versus FY2024.

Normalized EBITDA for the self-moving business (including ancillary products/services and U-Box but excluding self-storage) is estimated at $900 million to $1.1 billion. Applying an EV/EBITDA multiple of 5.0x to 6.5x (conservative relative to United Rentals at ~10x and Avis at ~4-5x, reflecting the quasi-monopoly nature of the franchise and its real asset backing) yields a valuation of $4.5 to $7.2 billion. We use a midpoint of approximately $5.5 billion.

C. Insurance Subsidiaries

Repwest and Oxford Life together hold substantial investment portfolios and generate underwriting income. Based on AM Best’s ‘A’ ratings, book values, and comparable insurance company acquisition multiples (typically 1.0-1.3x book for well-rated P&C and life companies), we estimate a combined value of $1.5 to $2.0 billion.

D. Other Assets

U-Haul holds approximately $989 million in cash and equivalents as of FY2025 year-end. The company also owns substantial real estate used for its company-operated moving centers, repair shops, and administrative facilities. We include the net cash position and assign a nominal value of $500 million to $800 million for these other real estate and business assets.

E. Consolidated NAV

At the midpoint NAV of ~$80 per share, the stock is trading at a 38% discount to intrinsic value. Even at our conservative low-end estimate of $63, the stock offers approximately 26% upside. On our most aggressive assumptions, the upside exceeds 100%. Note that these estimates do not assign any terminal growth premium to the self-storage portfolio, nor do they assign value to the development pipeline beyond what we have included in the pro forma NOI calculations.

III. What the Market Is Missing

The Depreciation Illusion

The single largest reason the stock has been under pressure is the collapse in reported GAAP earnings. Net income fell from $924.5 million in FY2023 to $628.7 million in FY2024 to $367.1 million in FY2025. In the first nine months of FY2026, net income was just $210.9 million (with a $37 million loss in Q3). Earnings per share for the non-voting class have gone from peaks above $5 to approximately $1.09 for the trailing nine months.

But the earnings decline is almost entirely explained by two temporary, non-cash factors. First, fleet depreciation surged because U-Haul paid significantly higher prices for replacement trucks during a period when OEM manufacturers were raising prices to subsidize their EV programs. Chairman Joe Shoen has been explicit about this: fleet acquisition costs over the past 30 months were elevated by what he described as artificial price increases from manufacturers. Depreciation was approximately $260 million higher in FY2025 than it would have been at normalized acquisition costs.

Second, gains on sale of retired equipment declined sharply. As the used truck market softened from its pandemic-era highs, U-Haul realized $140 million less in gains from equipment disposals in FY2025 compared to FY2024. Together, these two items account for approximately $400 million in pre-tax earnings pressure, explaining nearly all of the earnings decline.

Critically, both of these headwinds are temporary and self-correcting. Management has indicated that OEM pricing is beginning to improve as automakers refocus on their core competencies. Fleet capex is budgeted to decline by $500 million in FY2027. The used truck market will normalize. When these factors reverse, the earnings power of the self-moving business will revert to something much closer to historical norms.

The Storage Ramp Is Invisible in Headline Numbers

When total portfolio occupancy is reported at 77-78%, the headline looks weak. But this masks a two-tier reality: same-store occupancy is a healthy 91-92%, while newly opened locations are still leasing up. The industry standard for self-storage lease-up is 24-36 months to reach stabilization. U-Haul has added nearly 48 million net rentable square feet since 2022. Much of this space is still early in its lease-up curve. As these properties stabilize, they will contribute hundreds of millions in additional NOI that is not yet reflected in financial results.

The Cross-Selling Machine Is Underappreciated

Nearly 50% of U-Haul self-storage transactions are associated with a moving transaction. This means U-Haul acquires roughly half its storage customers through its truck rental business at near-zero incremental customer acquisition cost. Public Storage, Extra Space, and CubeSmart spend hundreds of millions annually on marketing and promotions to attract customers. U-Haul’s integrated model provides a structural cost advantage that is difficult to replicate and almost never discussed by the sell-side.

Conglomerate Discount Obscures Value

Because UHAL is not a REIT and does not report as one, it does not appear on the screens of the largest pool of dedicated self-storage capital. REIT-focused investors who own PSA and EXR typically do not analyze UHAL. Transportation and industrial analysts who cover truck rental companies are poorly equipped to value a 98-million-square-foot self-storage portfolio. The result is a classic analytical orphan: the stock falls between investment categories, leading to systematic undervaluation by the investment community.

1-Year Price Lock Guarantee Disruption

U-Haul recently introduced a 1-Year Price Lock Guarantee for self-storage customers, positioning itself against the industry-standard practice of advertising low introductory rates followed by aggressive rent increases. While competitors like Public Storage and Extra Space rely heavily on existing-customer-rate-increases (ECRI) to drive same-store revenue growth, U-Haul is betting on customer loyalty and lower churn. If successful, this could drive superior occupancy rates and customer lifetime values while differentiating U-Haul in a commoditized market.

IV. Catalysts for Re-Rating

1. Fleet Depreciation Normalization (FY2027-FY2028): As OEM truck prices moderate and the current high-cost vintage rolls through the fleet, depreciation expense will decline materially. Management has already announced plans to reduce fleet capital expenditures by $500 million in FY2027. This alone could add $2-3 per share in EPS.

2. Self-Storage Lease-Up (FY2026-FY2029): The 48 million square feet added since 2022 will progressively stabilize, contributing an estimated $300-500 million in incremental annual NOI. This is a high-visibility, high-certainty catalyst that plays out over 2-4 years.

3. Housing Market Recovery: U.S. existing home sales have hovered near 40-year lows. The entire self-storage industry has cited the frozen housing market as the top headwind. When mortgage rates decline and housing turnover recovers toward historical norms of 5.0-5.5 million annualized sales, U-Haul will benefit from increased moving activity and storage demand simultaneously.

4. Interest Rate Cuts: Lower rates would compress self-storage cap rates (increasing the value of U-Haul’s portfolio), reduce the company’s interest expense on variable-rate debt, and stimulate housing activity. Industry operators expressed confidence that 2025 represented the cyclical low, with fundamentals expected to strengthen through 2026.

5. Potential REIT Conversion or Spinoff: If management were to spin off the self-storage portfolio as a REIT or reclassify the company, the re-rating would be immediate and dramatic. While the Shoen family has historically shown no interest in this, the growing size of the storage portfolio (now generating nearly $1 billion in annual revenue) may eventually make such a move financially compelling. A REIT structure would allow the storage business to trade at public REIT multiples of 18-22x EV/EBITDA rather than U-Haul’s current consolidated multiple of ~6x.

6. Insider Buying: The Shoen family has been actively purchasing shares. Willow Grove Holdings LP acquired 459,030 shares in September 2025. Insiders have consistently bought at these price levels over the past five years, while sales have been limited. This is a strong alignment signal.

7. Supply Contraction in Self-Storage: New self-storage construction has slowed dramatically due to elevated construction costs, construction debt illiquidity, and potential tariffs on building materials. Development pipelines across the industry are shrinking well below historical averages. This supply discipline will support rent recovery and occupancy gains for existing operators like U-Haul.

V. Management Assessment

U-Haul is a controlled company. Edward J. Shoen (Joe Shoen) serves as Chairman, President, and CEO, and together with his brother Mark V. Shoen, controls approximately 50.1% of the voting common stock through Willow Grove Holdings LP. This dual structure gives the Shoen family near-absolute control over corporate decisions.

Strengths

Joe Shoen is one of the most unconventional CEOs in corporate America, and one of the most aligned with long-term value creation. His compensation is modest by public company standards. He does not manage for quarterly earnings, as evidenced by the willingness to accept near-term earnings pain from fleet replacement and aggressive self-storage development. His stated philosophy of shared use and specialization of ownership reflects a genuinely long-term, capital-efficient mindset. The company has historically avoided dilutive equity issuances, preferring to fund growth through operating cash flow and asset-backed debt. Share count has remained remarkably stable at approximately 19.6 million voting shares.

Management’s capital allocation track record in self-storage has been excellent. Much of the portfolio was assembled through internal development at costs of $60-120 per square foot, well below the current replacement cost of approximately $200-300 per square foot and current transaction prices of $150-160 per square foot. The decision to aggressively build storage during 2022-2025, while painful for near-term earnings, will likely prove to be enormously value-creative as these assets stabilize.

Weaknesses & Risks

The Shoen family control creates governance risks. The company is classified as a controlled company, with combined Chairman/President roles and no lead independent director. Related-party transactions are extensive: the company paid $37.1 million in management fees to Blackwater/Mercury entities in FY2025, and $106.2 million in independent dealer commissions to Blackwater/Mercury affiliates. While these appear to be at market rates, the sheer volume warrants monitoring.

Compensation practices are opaque. Bonuses are discretionary and not tied to disclosed quantitative performance targets. The company explicitly does not benchmark pay against peers. There are no mandatory stock ownership guidelines for officers. Alignment is driven more by the family’s 50%+ ownership than by incentive structures.

There is also limited investor communication. Earnings calls are brief, guidance is non-existent, and management provides minimal forward-looking information. This opacity contributes to the valuation discount but also means that patient investors who do the work have an informational edge.

VI. Scarce Assets or Overhyped? The Moat Analysis

The bear case on U-Haul’s assets is that trucks and storage units are commodities. Anyone can buy a fleet of trucks or build a storage facility. This argument is superficially compelling but fundamentally wrong, for several reasons.

Network Density Is the Moat

U-Haul’s competitive advantage is not the truck or the storage unit. It is the 25,000-location network that allows one-way rentals between any two points in North America. A customer renting a truck from Austin to Portland needs confidence that there will be a convenient drop-off location. Only U-Haul can make that promise at scale. This network was built over 80 years and would cost billions of dollars and decades to replicate. Budget Truck, the only other national one-way truck rental network, was acquired by Avis and subsequently exited the one-way rental market, effectively leaving U-Haul as a near-monopoly in nationwide DIY one-way moving.

Self-Storage Locations Are Increasingly Scarce

While self-storage units themselves are commodity-like, the locations are not. Zoning restrictions have become progressively more onerous in desirable suburban and urban markets. Many municipalities have imposed moratoriums on new self-storage construction. The best sites, those with high visibility, easy access, and proximity to residential density, are largely taken. U-Haul’s strategy of repurposing existing retail locations (Kmart, Sears, etc.) gave it access to irreplaceable infill locations at low costs. New entrants face much higher land costs, stricter permitting, and longer development timelines.

The Integrated Platform Cannot Be Replicated

No competitor operates across moving trucks, trailers, portable containers, self-storage, trailer hitches, propane, and insurance with U-Haul’s breadth and scale. The cross-selling flywheel, where moving customers become storage customers at near-zero acquisition cost, is unique in the industry. Public Storage cannot offer customers a moving truck. Penske cannot offer customers a storage unit. Only U-Haul does both, and the resulting customer economics are superior.

Not a Beta Play

A pure beta play would rise and fall mechanically with the market or the economy. U-Haul’s value drivers are substantially idiosyncratic: self-storage lease-up, fleet depreciation normalization, and potential structural changes. The stock has underperformed the S&P 500 dramatically over the past three years despite the broader market surging, suggesting that the current price reflects company-specific concerns rather than macro positioning. If anything, the stock offers anti-beta characteristics: the sum-of-the-parts discount should narrow regardless of the economic cycle, providing a margin of safety.

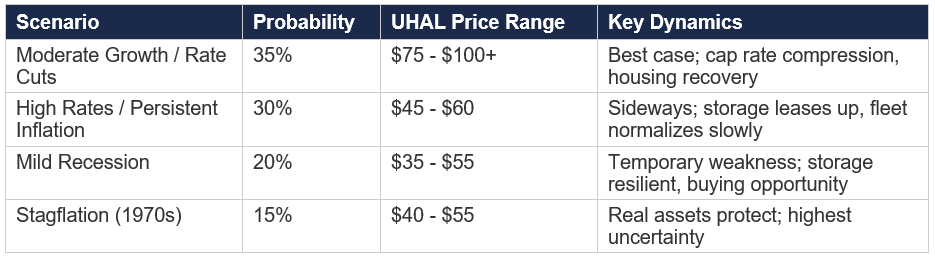

VII. Scenario Analysis: Economic Environments

Scenario 1: Moderate Growth / Rate Cuts

This is the base case and most favorable scenario. GDP growth of 2-3%, the Federal Reserve cutting rates 100-200 basis points, and housing activity gradually recovering toward 5 million annualized sales. In this environment, self-storage demand strengthens as mobility increases, cap rates compress by 50-100 basis points (increasing portfolio value), interest expense declines, and moving transaction volumes inflect higher. This scenario supports our $80-100+ per share NAV and likely triggers a re-rating over 18-24 months.

Scenario 2: High Rates / Persistent Inflation

If rates remain elevated (10-year above 4.5%) and inflation persists at 3-4%, the self-storage sector faces extended pressure from a frozen housing market and elevated cap rates. However, U-Haul is better positioned than peers because its self-moving business is less rate-sensitive (people must move regardless of rates, for jobs, family, and life events), and inflation actually supports storage pricing power as replacement costs rise. U-Haul’s fixed-rate debt structure (the majority of its $7.2 billion in debt is fixed-rate, asset-backed) limits refinancing risk. In this scenario, the stock likely trades sideways in the $45-60 range, but the underlying NAV continues to build as new storage properties lease up.

Scenario 3: Recession

Self-storage has historically been one of the most recession-resistant real estate asset classes. During the 2008-2009 financial crisis, same-store self-storage NOI declined only 2-5% while office and retail REITs saw declines of 15-30%. People in financial distress often need more storage, not less, as they downsize, move in with family, or face foreclosure. U-Haul’s moving business would see some volume pressure in a severe recession, but the company’s balance sheet ($989 million in cash, $1.35 billion in cash and available credit in the Moving and Storage segment) provides significant cushion. Debt coverage is adequate at 2.6x interest coverage, and operating cash flow of $1.5 billion provides substantial breathing room. In a mild recession, the stock could decline to the $35-45 range, but this would represent an exceptional buying opportunity as the recovery would drive both earnings normalization and multiple expansion.

Scenario 4: 1970s-Style Stagflation

A high inflation, high interest rate, low growth environment would be the most challenging. However, U-Haul’s real assets (trucks, real estate, storage facilities) serve as natural inflation hedges. Storage rents, truck rental rates, and propane prices all rise with inflation. The company’s assets have replacement values that increase with construction costs, supporting NAV even as cap rates rise. During the actual 1970s, self-storage was a nascent industry, but real assets generally outperformed financial assets. The key risk in this scenario is the interest expense on any variable-rate debt and the difficulty of refinancing maturing fixed-rate debt at much higher rates. However, U-Haul’s long average debt maturity and predominantly fixed-rate structure mitigate this risk. Estimated impact: stock flat to modestly down, but real purchasing power of the underlying assets would be preserved or enhanced.

Probability-weighted expected value: ~$60-75 per share, representing 20-50% upside from current levels with downside protection from asset backing and the passage of time.

VIII. The Company in Five Years

Projecting U-Haul’s trajectory to fiscal year 2030 (ending March 31, 2030), we envision a company that looks quite different from today:

Self-Storage Portfolio: The portfolio will have grown to approximately 110-120 million net rentable square feet, with current development projects completed and leased up. Total portfolio occupancy will have recovered to 85-90% as the massive 2022-2025 development wave reaches stabilization. Annual self-storage revenue will likely exceed $1.3-1.5 billion, with NOI approaching or exceeding $1 billion. At that point, U-Haul’s self-storage portfolio alone, valued at a conservative 5.5-6.0% cap rate, would be worth $17-18 billion, substantially more than the company’s current entire enterprise value.

Self-Moving Business: Fleet depreciation will have normalized as the high-cost vintage cycles through. The self-moving business will return to generating $1.0-1.3 billion in EBITDA. The fleet will be newer, more efficient, and more technologically advanced (Truck Share 24/7 penetration will be substantially higher). Revenue may reach $4.0-4.5 billion.

U-Box: At 20%+ growth rates, the U-Box business could be generating $1.0-1.5 billion in annual revenue by 2030, making it a significant profit contributor in its own right. The portable storage market is still in early innings of adoption.

Consolidated Picture: Total revenue of $7.5-8.5 billion, consolidated EBITDA of $2.5-3.0 billion, and net income of $800 million to $1.2 billion. Free cash flow generation will be substantial as the capital-intensive growth phase winds down. The company will face increasing pressure to return capital through dividends (currently only $0.05/quarter on UHAL.B) or consider structural alternatives like a storage REIT spin.

IX. Key Risks

1. Extended Housing Freeze: If mortgage rates remain above 6.5% and existing home sales stay below 4 million annualized for another 2-3 years, the storage lease-up timeline extends and moving volumes remain depressed.

2. Self-Storage Oversupply: While construction has slowed nationally, some Sunbelt markets (Florida, Arizona, Atlanta, Phoenix) remain pressured by recent deliveries. U-Haul’s exposure to these markets could produce below-average returns.

3. Governance / Related-Party Risk: The Shoen family’s control creates the risk of value-destructive capital allocation decisions or excessive related-party transactions. Minority shareholders have limited recourse.

4. Debt Load: Total debt of $7.2 billion against trailing EBITDA of approximately $1.6-1.7 billion represents roughly 4.0-4.5x leverage. While most debt is fixed-rate and asset-backed, the absolute level leaves limited margin for error if operating performance deteriorates significantly.

5. EV Transition Costs: Regulatory pressure for emissions compliance and potential EV mandates could continue to elevate fleet acquisition costs beyond historical norms.

6. No Catalyst Timeline: There is no identifiable event that forces the market to re-rate the stock. The Shoen family is under no pressure to unlock value through structural changes. This could remain a ‘value trap’ for an extended period.

X. Conclusion

U-Haul Holding Company is a rare combination of a near-monopoly operating business and a rapidly growing, high-quality real estate portfolio, available at a significant discount to intrinsic value because the market is fixated on temporarily depressed GAAP earnings and does not properly value the sum of the parts.

The self-storage portfolio alone is likely worth more than the company’s current enterprise value. The self-moving franchise is a unique, irreplaceable asset with no meaningful national competitor. The development pipeline provides years of visible organic growth. The fleet depreciation headwind is temporary and self-correcting. Insider buying confirms management’s confidence in long-term value.

The risk/reward is compelling: downside is limited by the hard asset backing (trucks, real estate, insurance reserves), while upside is substantial if any of several plausible catalysts materialize. We believe the stock offers 50-100%+ upside over a 2-4 year horizon, making it one of the more attractive risk-adjusted opportunities in the mid-cap value space.