Hard Asset Reckoning: The End of the Asset-Light Era

How a generation of underinvestment, the death of SaaS moats, and the physics of scarcity are creating the greatest reallocation from bits to atoms in modern market history

— Electric Choice")

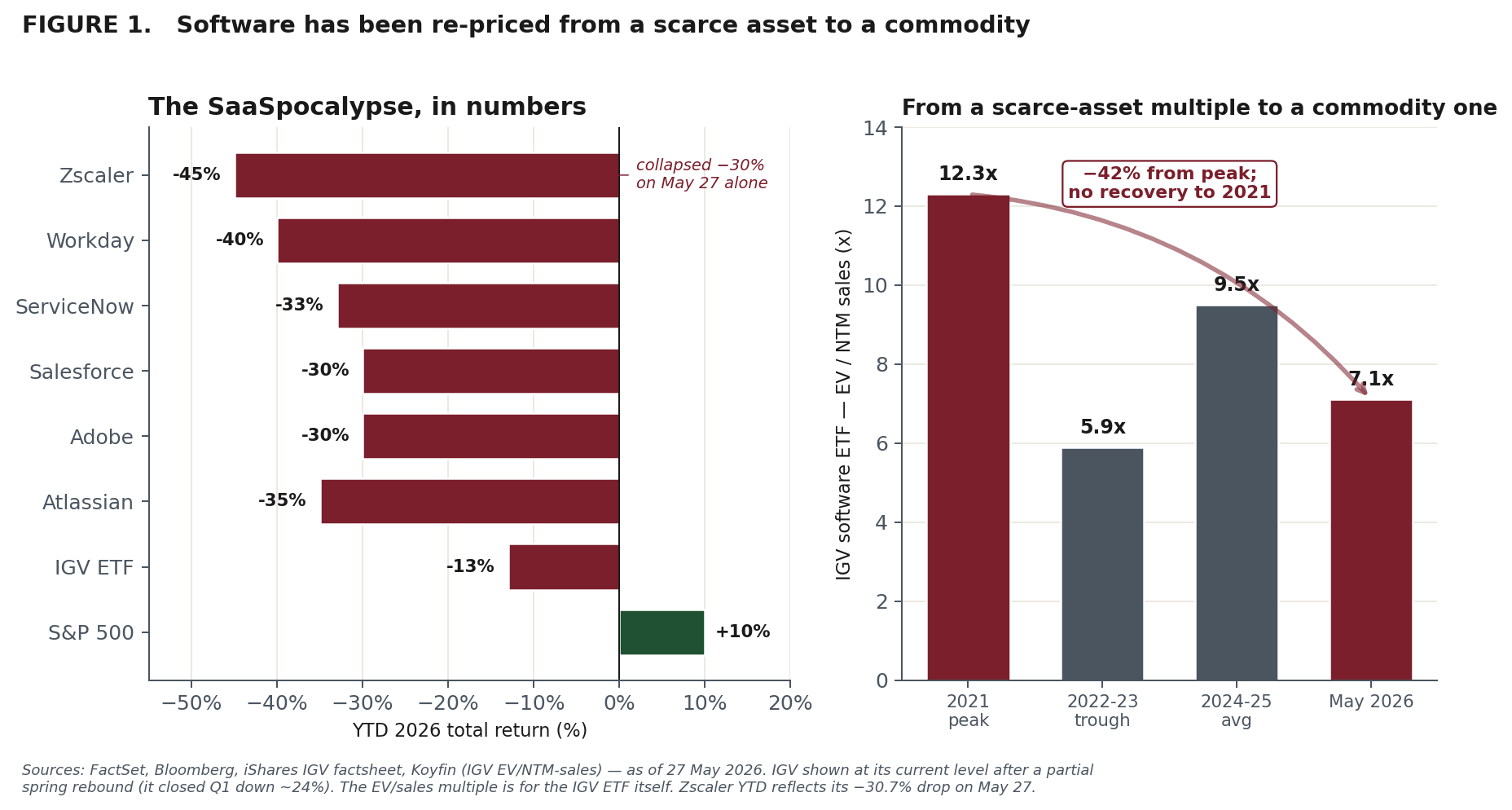

On February 3, 2026, roughly $285 billion in market capitalization evaporated from the software sector in a single trading session. Salesforce was down 30% on the year. Workday had dropped more than 40% from its twelve-month high. Atlassian had lost 35%. The iShares Expanded Tech-Software ETF (IGV) entered a technical bear market, off more than 20% for the year - in five weeks. Analysts coined a term for it: the SaaSpocalypse.

The catalyst was not a recession, a credit event, or a geopolitical shock. It was the proliferation AI. Two assumptions the entire software industry had been priced on broke at once: that producing useful software was hard, and that the number of humans using it would only grow. AI broke both.

For thirty years, building enterprise software at scale required engineering teams, multi-year roadmaps, and tens of millions of dollars of capital. AI-assisted code generation has collapsed that cost curve. A motivated team can now ship a credible internal tool or feature that a $20B SaaS incumbent charges handsomely for - in weeks, not years. When the production function for software is commoditized, the premium collapses with it - most steeply for the companies whose moat was the software itself rather than the system of record beneath it.

And as recently as yesterday - Zscaler stock collapsed roughly 30% in a single session after beating Q3 on both lines but guiding softer for the next quarter. Wall Street treated a single soft guide as confirmation that demand itself, not just multiples, is now the story. Even strong cybersecurity names are no longer being granted the benefit of the doubt.

The clearest single statistic: the IGV software index now trades at roughly 7x forward EV/sales, down from a 2021 peak above 12x. The premium the market once paid for software being scarce and defensible has been structurally re-rated away.

On the same days software cratered, Caterpillar, Deere, Southern Copper, and Constellation Energy traded at or near record highs. The market was not panicking. It was reallocating - away from business models built on the assumption that code is scarce and atoms are cheap, toward business models built on the recognition that code is becoming free and atoms are becoming priceless.

This article is about that reallocation: why the thirty-year dominance of asset-light business models is ending, why the next ten to twenty years will belong to owners of hard, physical, scarce assets, and why the investors who understand this shift earliest will capture some of the most asymmetric returns of their careers.

I. The Asset-Light Orthodoxy: How We Got Here

The intellectual origin

The preference for asset-light business models did not emerge from nowhere. It was a coherent response to conditions that prevailed from roughly 1995 to 2020. The internet made distribution free. Cloud computing made infrastructure rentable by the hour. Software-as-a-service made enterprise tools accessible without capital expenditure. The rational strategy was obvious: own the code, rent the atoms. Build the platform, let someone else build the data center. Design the marketplace, let someone else own the inventory.

The financial logic was seductive. Asset-light companies posted higher returns on invested capital because there was less capital to invest. They carried wider margins because they had fewer physical costs. They scaled faster because scaling code costs nothing at the margin, and they were more resilient in downturns because variable costs could be cut instantly while asset-heavy competitors were stuck paying for fixed infrastructure. During the 2020 shock, asset-light companies recovered roughly 2.5x faster than asset-heavy peers.

The market rewarded the strategy lavishly. At the 2021 peak, the median enterprise-software company traded at 12–13x revenue. The entire venture-capital industry was oriented around the model: build a SaaS product, acquire customers at a loss, demonstrate recurring revenue, point to a land-and-expand trajectory, and raise at an ever-higher multiple. By 2021 there were over 15,000 SaaS companies globally. Software had, as Marc Andreessen famously declared, eaten the world.

The hidden consequence: systematic underinvestment in physical assets

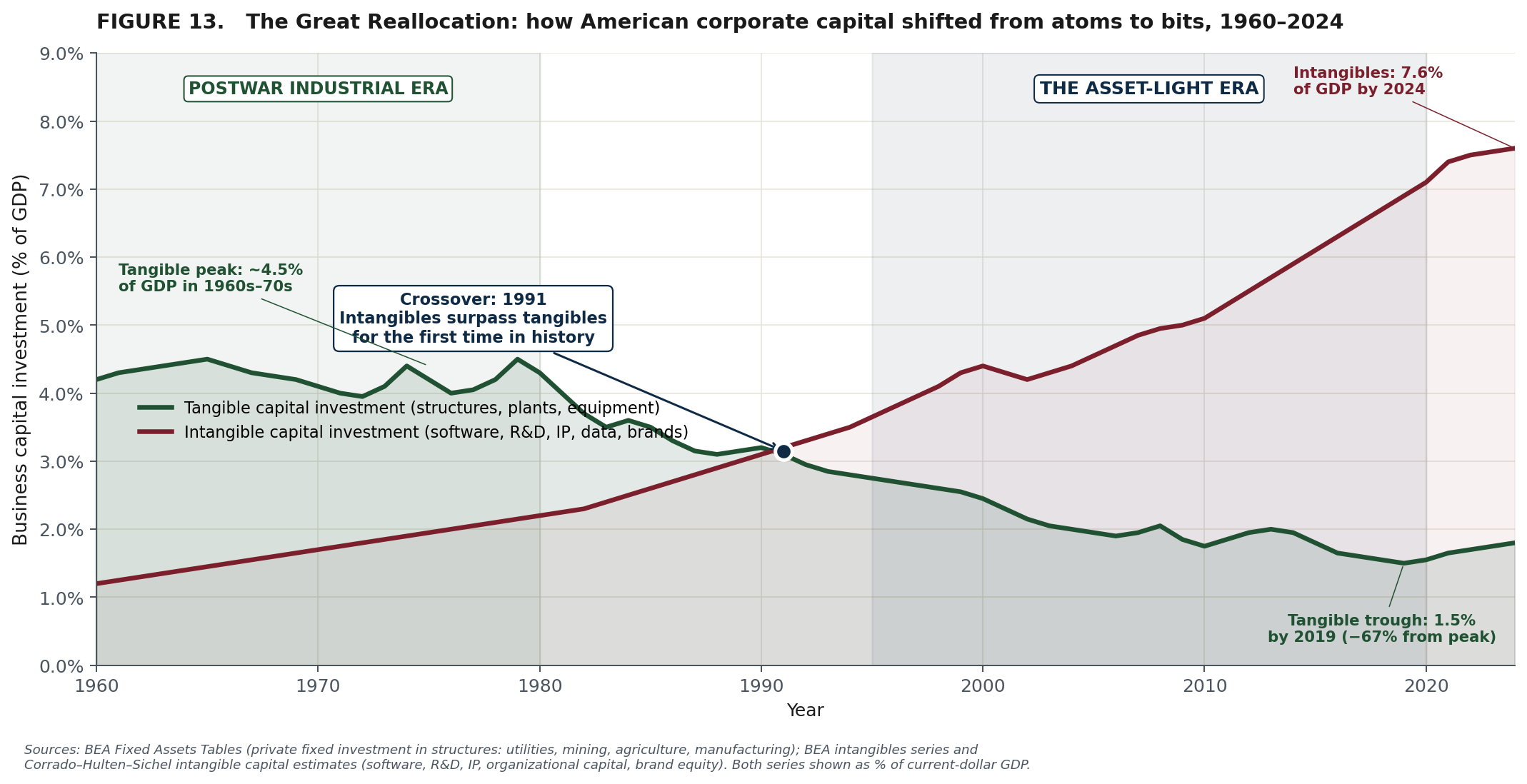

But while the smartest capital in Silicon Valley poured into code, something else was happening - or precisely, not happening - in the physical world. Capital expenditure on hard assets across the American economy was declining as a share of GDP. Infrastructure was aging. Bridges deteriorated. Power grids strained. Water systems corroded. Mines closed. Farmland was converted to suburbs. Refineries shut down. Pipelines went unbuilt.

The numbers are stark. The American Society of Civil Engineers has graded U.S. infrastructure a D+ or C− for over two decades. More than $1 trillion in water-infrastructure upgrades are needed; the power grid requires an estimated $2.5 trillion to meet projected demand. The U.S. lost an average of 4.3 acres of farmland every minute from 2000 to 2022. Domestic mining capacity for critical minerals declined for decades. Since 2020, the housing-construction shortfall has grown to an estimated 3–5 million units.

This underinvestment was not accidental. It was the logical consequence of a capital-allocation regime that systematically rewarded asset-light models and punished capital intensity. Every dollar that went into a SaaS startup was a dollar that did not go into a power plant, a water-treatment facility, a mine, a pipeline, or a farm. The market was extremely efficient at funding the highest-return, lowest-capital-intensity opportunities - and extremely inefficient at maintaining the physical substrate on which everything else depends.

The result is a paradox only now becoming visible: three decades of optimizing for asset-light models created the conditions under which hard assets are more valuable than they have been in a generation. The scarcity was manufactured by the orthodoxy itself.

II. The AI Inflection: Why Asset-Light Moats Are Dissolving

What AI can replicate - and what it cannot

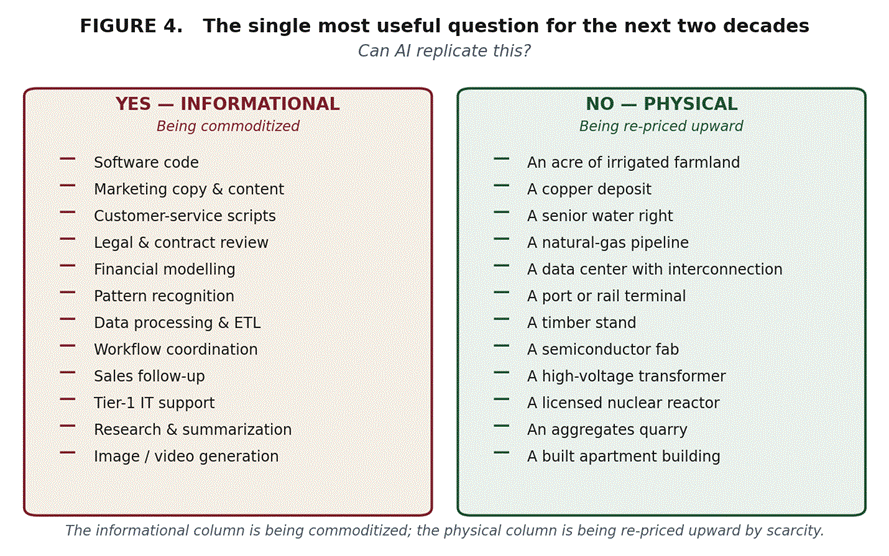

This is the critical analytical framework for the next decade. AI can replicate anything fundamentally informational: code, content, analysis, pattern recognition, workflow coordination, data processing, customer-service scripts, marketing copy, legal review, financial modeling. These are the activities asset-light businesses are built upon. When AI produces 90% of the quality at 1% of the cost, the moat of being the best software tool for a task dissolves.

What AI cannot replicate is anything fundamentally physical: an acre of irrigated farmland, a copper deposit, a water right, a natural-gas pipeline, a data center with power interconnection, a port terminal, a timber stand, a semiconductor fab, a rail network, a transmission line. These assets exist in the physical world, are constrained by geology, geography, regulation, and physics, and cannot be conjured by an algorithm regardless of how intelligent it becomes.

The market is beginning to reflect this. As of mid-2026, infrastructure-investment volumes are outpacing global GDP growth, the utilities sector has entered what analysts describe as a capital-expenditure super-cycle, and the irony is complete: AI - the most powerful informational technology ever created - is the greatest catalyst for physical-asset revaluation in modern history, because AI itself requires staggering quantities of electricity, cooling, land, water, and physical infrastructure to operate.

Big Tech is no longer buying bits - it is buying atoms

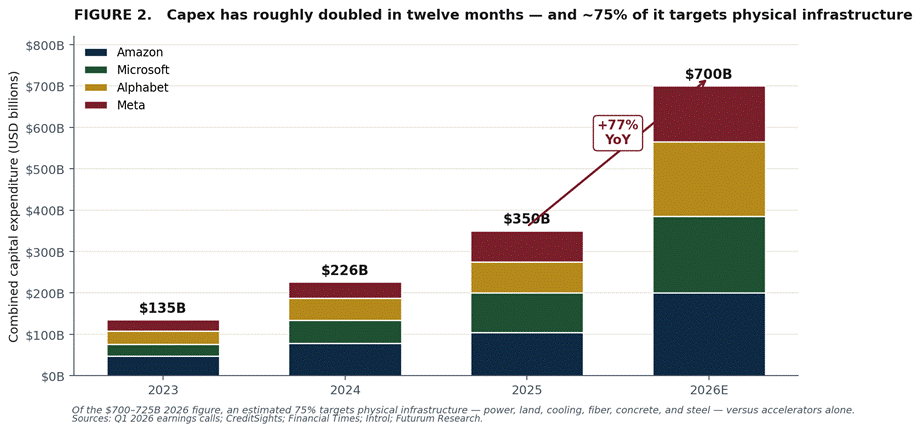

Nothing illustrates the inversion more vividly than the hyperscalers’ own balance sheets. At the beginning of 2026, the five largest cloud providers were guiding to $660–$690 billion of 2026 capital expenditure. Then first-quarter earnings landed in late April. Every major hyperscaler raised its guide. Microsoft set calendar-2026 capex near $185 billion; Alphabet raised toward $180–$185 billion; Meta lifted its range to $125–$145 billion; Amazon held at roughly $200 billion. Together, the four largest now plan to spend on the order of $700–$725 billion this year - up roughly 77% from 2025’s record $410 billion, and more than triple 2024.

Approximately 75% of that spend targets physical infrastructure rather than chips alone. Microsoft attributed about $25 billion of its 2026 figure to component-price inflation; Amazon’s free cash flow is expected to turn negative on the build-out; Alphabet’s CEO described the company as “compute-constrained.” Every dollar is demand for electrons, copper, fiber, water, and land. AI is not dematerializing the economy. It is rematerializing it at unprecedented scale.

AI is the most asset-heavy technology ever deployed

This deserves to be stated plainly, because it inverts thirty years of intuition. Every prior wave of computing was celebrated for dematerializing the economy - the PC, the internet, mobile, the cloud, and SaaS all promised to do more with fewer atoms, replacing warehouses with websites and filing cabinets with servers somewhere out of sight. AI breaks the pattern. It is the first major general-purpose technology in modern history that is more physically intensive than what it displaces, by orders of magnitude. The “cloud” was always made of concrete, copper, and water; AI simply makes that physicality impossible to ignore.

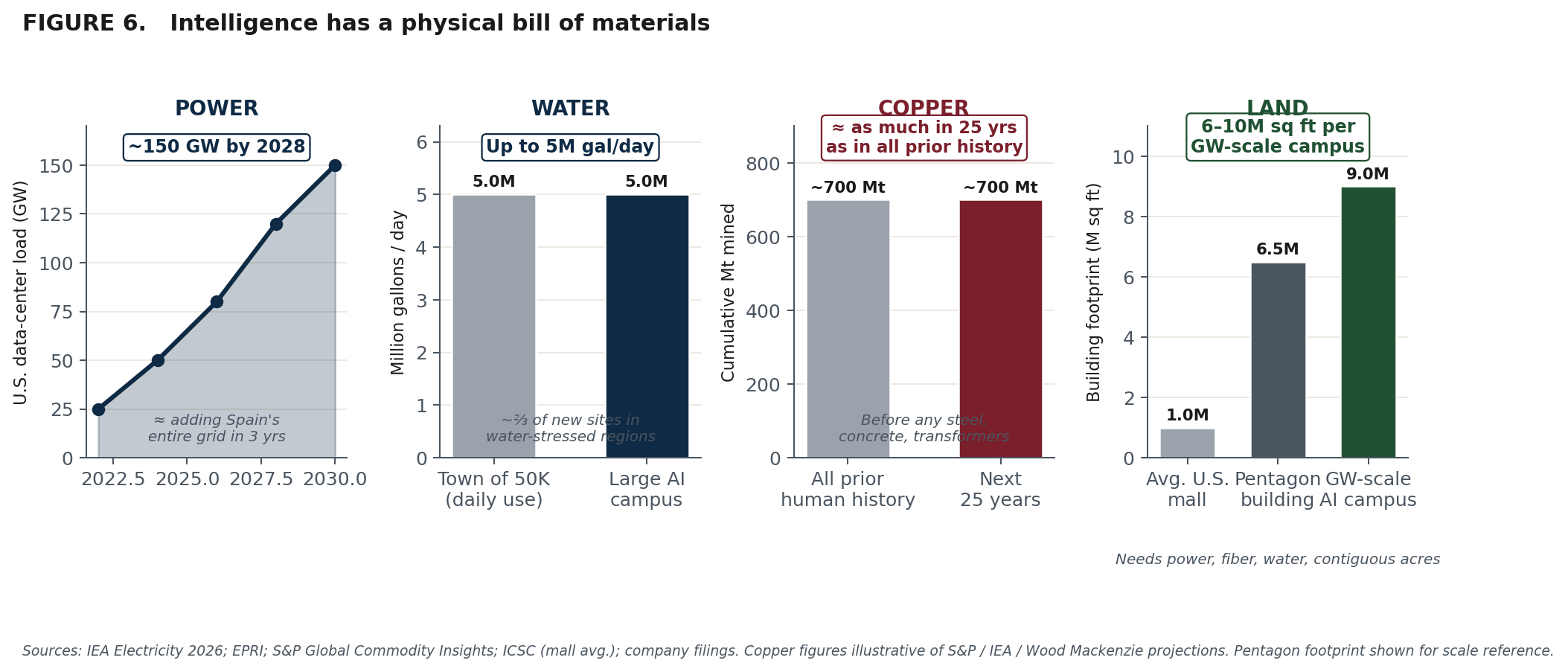

Consider the bill of materials:

On power, U.S. data-center demand is projected to climb from roughly 80 gigawatts toward 150 by 2028 - the equivalent of bolting Spain's entire electricity system onto the grid in three years. Meta's Louisiana campus is expected to consume more than twice the power of New Orleans.

On water, a single large campus can evaporate up to five million gallons a day - the draw of a town of fifty thousand - and roughly two-thirds of new sites are being built in already water-stressed regions.

On materials, the copper alone required to wire AI and the broader electrification it accelerates may oblige the world to mine as much copper in the next twenty-five years as has been mined in all of recorded human history - before counting the steel, concrete, fiber, transformers, and switchgear now on multi-year backorder.

On land, the campuses themselves are becoming small cities: gigawatt-scale sites now run six to ten million square feet of building footprint on thousands of acres of contiguous, fiber-connected, power-served real estate - a combination of attributes that exists in very few places in the United States and cannot be manufactured by zoning reform alone.

And this doesn’t even include the power generation. A single gigawatt of solar requires roughly five to ten thousand acres of land. A gigawatt of nuclear, can evaporate hundreds of millions of gallons of cooling water annually. Even natural gas requires upstream pipeline corridors, water for cooling, and decade-scale permitting timelines for new long-haul capacity. The implication is that AI’s physical footprint is recursive: each new gigawatt of data-center load compounds into thousands of acres of generation footprint and millions of gallons of additional water draw.

This is the deepest reason the bits-to-atoms reallocation is structural rather than cyclical. The dominant technology of the era does not merely coexist with hard assets; it is the largest new source of demand for them. The same force commoditizing the informational economy is, by physical necessity, the most powerful bid for the physical one.

III. The Winners: Hard Assets in the Age of Digital Abundance

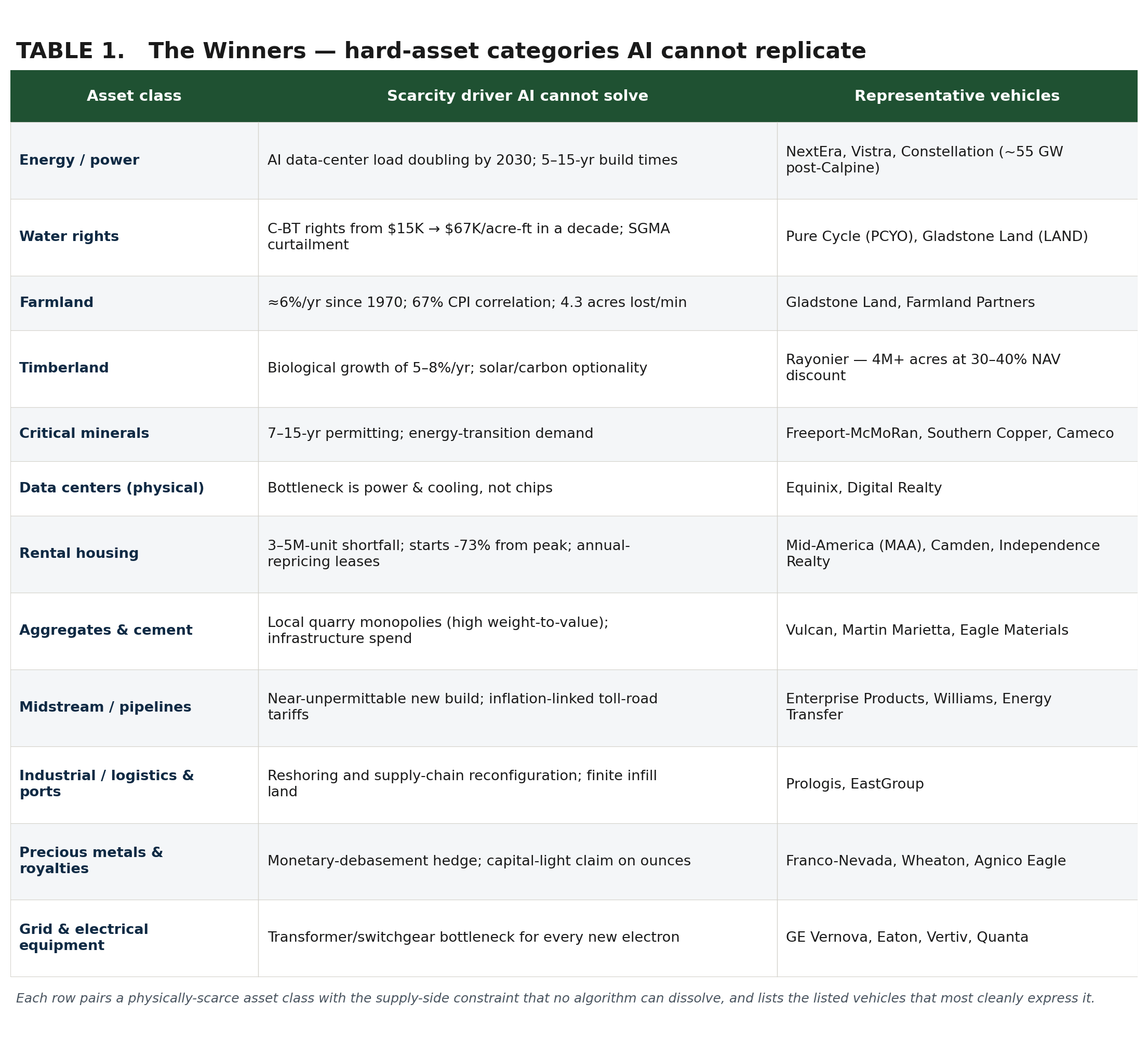

If AI commoditizes the informational and re-prices the physical, the winners are the owners of irreproducible, supply-constrained, replacement-cost-protected assets. The table below maps the principal categories, the scarcity driver that no model can solve, and representative listed vehicles - several of which still trade at meaningful discounts to private-market value.

Energy infrastructure

AI data centers are the single largest new source of electricity demand in the developed world; a large training cluster can consume as much power as a small city, and U.S. data-center demand is projected to roughly double by 2030. That demand is arriving into a grid underinvested in for decades, creating a structural shortage of generation, transmission, and interconnection that cannot be resolved quickly because building power infrastructure takes 5–15 years. Owners of existing generation - gas, nuclear, interconnected renewables - are being re-priced as the market recognizes that electrons are the new oil. Constellation’s January 2026 combination with Calpine creates a roughly 55-GW platform, and its multi-decade agreement to restart Three Mile Island for Microsoft has become the emblem of the era.

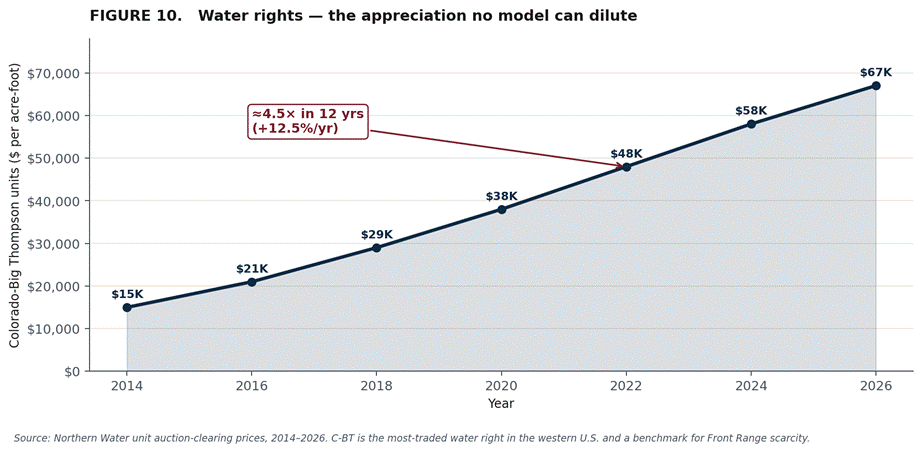

Water rights and water infrastructure

Water is required for data-center cooling, semiconductor manufacturing, hydrogen production, irrigation, and human consumption - while supply is constrained by climate, aquifer depletion, and regulatory curtailment. Colorado-Big Thompson rights have appreciated from roughly $15,000 to $67,000 per acre-foot in a decade; in California, SGMA is curtailing groundwater pumping and making stored water exponentially more valuable. No model can create an acre-foot of water.

Water Rights are the AI power trade’s inevitable second derivative - and the market hasn’t recognized it.

Farmland, timberland, and minerals

U.S. farmland has appreciated at roughly 6% annually since 1970 with near-zero correlation to equities and about 67% correlation to inflation; the U.S. loses 4.3 acres per minute to development while global food demand is set to rise 50% by 2050. Yet farmland REITs trade at 50–70% discounts to replacement cost because the market cannot categorize them. Rayonier’s post-merger entity controls over four million acres of timberland at a 30–40% discount to private NCREIF valuations - trees compound 5–8% biologically each year, a coupon that never appears in quarterly earnings, while solar leasing and carbon optionality can lift per-acre value severalfold. And the energy transition requires copper, lithium, nickel, cobalt, rare earths, and uranium in quantities current mining cannot supply, with U.S. permitting taking 7–15 years - a moat immune to digital replication.

Rental housing

Housing sits on a structural shortage of 4–5 million units. The case is doubly compelling because the lease re-prices every year: unlike a fixed-rate bond, an apartment owner marks rents to market annually, so in-place cash flows track inflation rather than lagging it. The supply side has now snapped shut - Q1 2026 multifamily starts at roughly 55,000 units were the lowest since 2011 and down 73% from the early-2022 peak - even as the cost of buying a home keeps a record share of households renting. The owner of an existing, well-located, modestly-levered apartment portfolio holds precisely the asset a language model cannot manufacture and a developer can no longer afford to build.

Aggregates, cement, and the “boring” physical economy

Few assets are more quietly defensible than a sand-and-gravel quarry. Aggregates have a punishing weight-to-value ratio - it is uneconomic to truck crushed stone more than roughly 50 miles - so each quarry is effectively a local monopoly that no software, and no distant competitor, can disintermediate. Layer on permitting that takes years and zoning that communities fight, and the existing reserve base becomes irreplaceable infrastructure feeding every road, bridge, data center, and transmission project in its radius.

FRP Holdings (FRPH), Vulcan Materials, and Eagle Materials are the unglamorous, inflation-protected backbone of the reindustrialization trade.

Midstream, industrial real estate, and the picks-and-shovels of the grid

Three further categories round out the physical-winner universe. Midstream energy - pipelines and storage - behaves like a toll road with inflation-linked tariffs, and the political near-impossibility of permitting new long-haul capacity turns the installed base of Enterprise Products, Williams, and Energy Transfer into a widening moat. Industrial and logistics real estate (Prologis, EastGroup) is the physical settlement layer of reshoring and e-commerce, constrained by a shrinking supply of well-located infill land. And the most direct “picks-and-shovels” play on the entire AI-power build-out is the electrical hardware that connects an electron to a chip: there is a multi-year backlog for the transformers, switchgear, and high-voltage equipment that GE Vernova, Eaton, Vertiv, and Quanta supply. Finally, for investors who want the debasement hedge in its purest form, precious-metals royalty and streaming companies (Franco-Nevada, Wheaton) offer a capital-light claim on physical ounces - exposure to scarcity without the operating risk of running a mine.

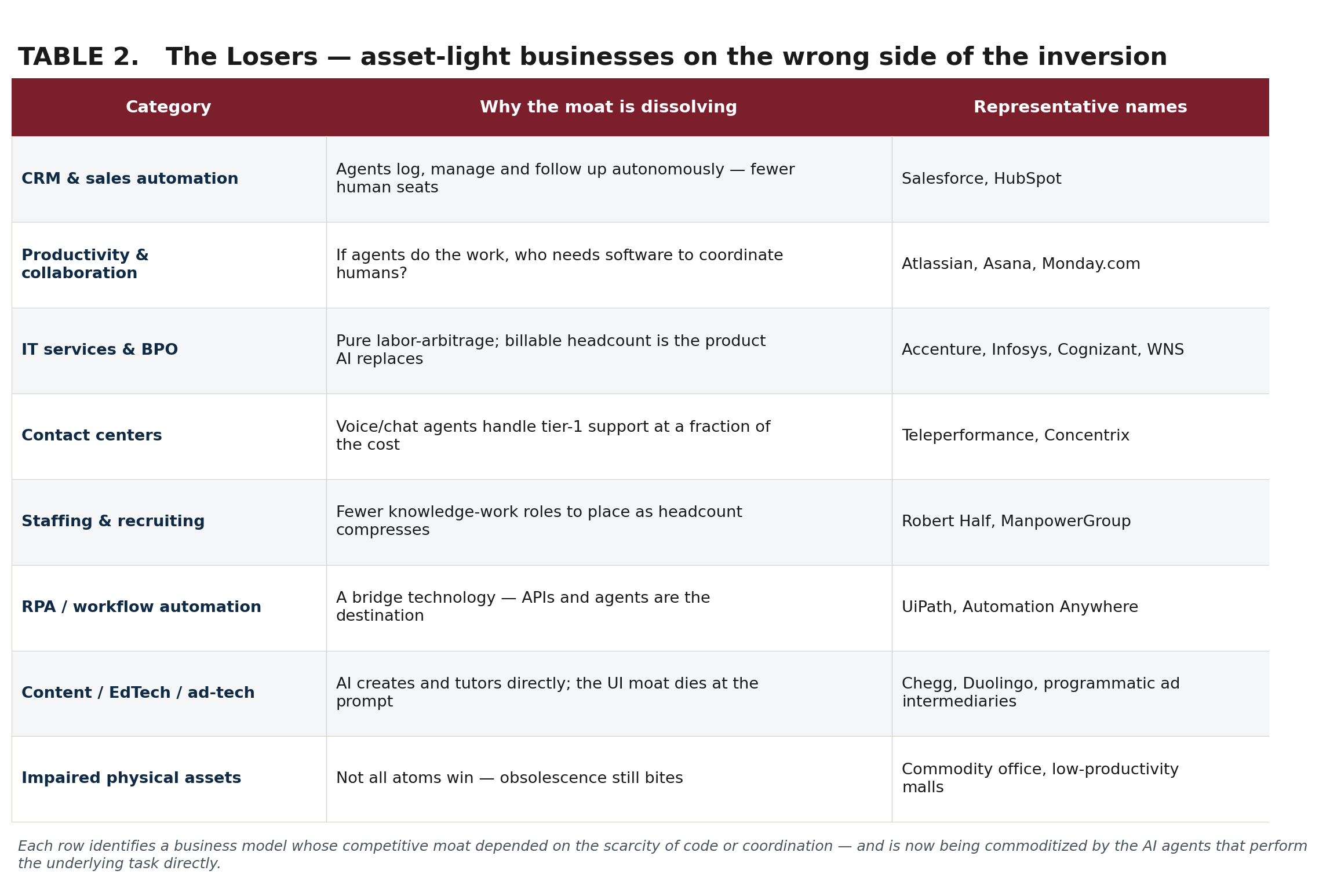

IV. The Losers: Asset-Light Models in the Blast Radius

The blast radius is wider than software alone. The common thread among the vulnerable is that their value is proportional to the quantity of human cognitive labor they intermediate - and AI is collapsing the price of exactly that. The categories below sit at progressively greater distance from the SaaS epicenter, but each is exposed to the same force

The SaaS epicenter: CRM, productivity, and content tooling

The center of the crater is any tool whose value scales with the number of human seats. Project-management and collaboration platforms - Atlassian, Asana, Monday.com - face an existential question when agents execute tasks rather than merely track them: if agents do the work, who needs software to coordinate humans doing the work? Salesforce, the iconic SaaS company, has become the poster child of the selloff; its peak valuation was built on ever-expanding seat count, an assumption now under direct assault. Content and code generators, marketing-automation suites, EdTech, and programmatic ad intermediaries share the vulnerability: any product whose proposition is “helping humans create things” is exposed to AI that creates things directly. The moat of a well-designed interface is worthless when natural language becomes the interface. One caveat preserves nuance - a genuine system of record (the database other systems trust) is stickier than a workflow layer, so the most durable incumbents may retain the data even as they lose the seats.

The labor-arbitrage complex: IT services, BPO, and staffing

If software is the epicenter, the labor-arbitrage economy is the largest adjacent structure in the blast zone - and the market has been slower to price it. The IT-services and business-process-outsourcing model (Accenture, Infosys, Cognizant, WNS) is built on billing clients for hours of human cognitive labor at a margin over cost; when an agent performs the ticket, the document review, or the reconciliation, the billable headcount that is the product is exactly what gets automated away. The same logic flows downhill to contact centers (Teleperformance, Concentrix), where voice and chat agents already handle tier-one support at a fraction of the cost, and to staffing and recruiting (Robert Half, ManpowerGroup), whose volumes shrink as the knowledge-work roles they place are compressed. These are not technology stocks, so they have not yet been swept into the SaaSpocalypse narrative - which is precisely why the repricing may still be ahead of them.

RPA, asset-light intermediaries, and the impaired-atom exception

Robotic Process Automation (UiPath, Automation Anywhere) was a bridge technology; agents are the destination, and entire categories may be obsolete within five years once an API can act directly. The platform economy faces a subtler erosion: Airbnb, Uber, and DoorDash built trillion-dollar narratives on capturing value without owning the assets, but as their sectors mature, value migrates back to the owners - a hotel with owned real estate has pricing power that a host competing on a commoditizing platform does not. A final and important caveat keeps the framework honest: not every physical asset is a winner. Commodity office towers and low-productivity malls are intensely physical and still structurally impaired - scarcity protects assets the world still wants, not those it is abandoning. The thesis is about irreplaceable, in-demand physical assets, not about “atoms” as an undifferentiated category.

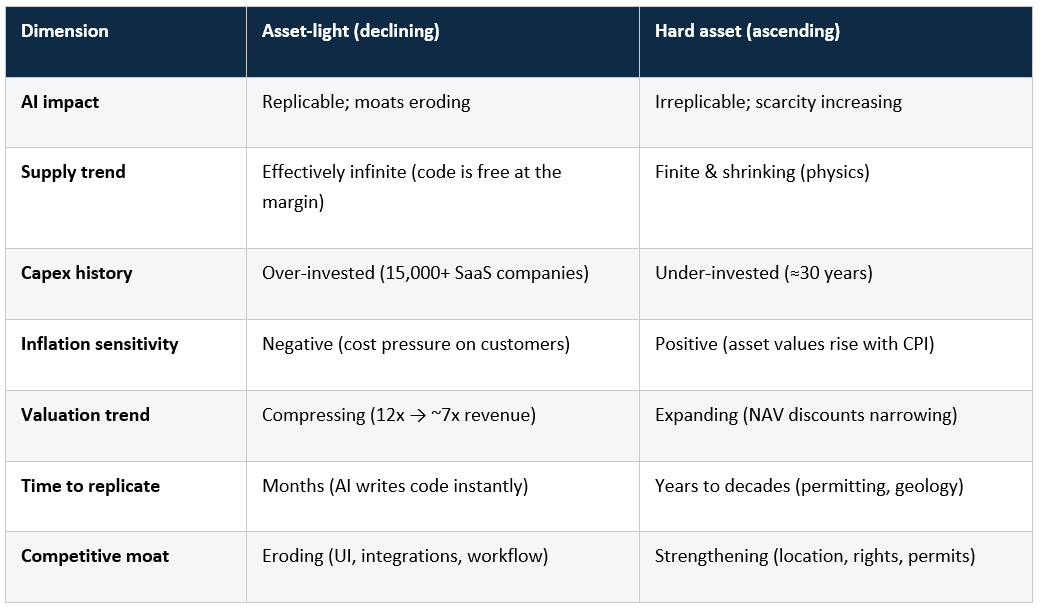

V. The Investment Framework: A Taxonomy of the Shift

The framework reduces to one question asked of any business: can AI replicate what this company does? If the answer is yes - even partially - the business model is under structural pressure. If the answer is no, because the value is embedded in physical assets constrained by geography, geology, regulation, or physics, the moat is strengthening rather than eroding. The market has spent thirty years paying premiums for the first column and discounting the second. That regime is reversing.

VI. The Macro Convergence: Why This Time Is Different

The hard-asset thesis is not merely a reaction to a software selloff. It is the convergence of at least six independent structural forces, each significant alone, which together constitute the most powerful shift in capital allocation in a generation.

• AI is the most capital-intensive technology ever deployed. Hyperscalers will spend on the order of $700–$725 billion on infrastructure in 2026, with roughly 75% targeting physical assets. Every dollar is demand for electricity, land, water, copper, fiber, concrete, and steel.

• Geopolitical fragmentation rewards domestic physical assets. Tariffs, export controls, friendshoring, and the One Big Beautiful Bill Act (2025) provide tax incentives for domestic manufacturing and capital-intensive infrastructure while penalizing globally-distributed, asset-light models.

• Inflation is persistent and structural. Fiscal deficits, reshoring costs, climate-adaptation spending, and defense buildups are all inflationary. April 2026 CPI reaccelerated to 3.8%, a near-three-year high. Farmland (67% CPI correlation), timberland, and water rights (10–15% annual appreciation) are the natural beneficiaries; software, facing customer budget pressure, is the natural victim.

• Climate change is destroying physical assets faster than they are replaced. Hurricanes, wildfires, droughts, and floods degrade infrastructure, farmland, and water systems - and every physical asset destroyed raises the scarcity value of those that survive.

• Demographic and food-security pressures are permanent. 9.7 billion people by 2050; food demand up 50%; farmland shrinking; water depleting. There is no technological substitute for eating.

• Institutional capital is massively under-allocated to real assets. Pension funds hold 1–3% in farmland versus 10–15% in commercial real estate; timberland is a rounding error and water rights are not even an asset class in most frameworks. As the 60/40 portfolio strains, the reallocation into hard assets will drive repricing at a magnitude few investors are positioned for.

VII. The Cost-of-Capital Paradox: Why Higher-for-Longer Tightens the Screw

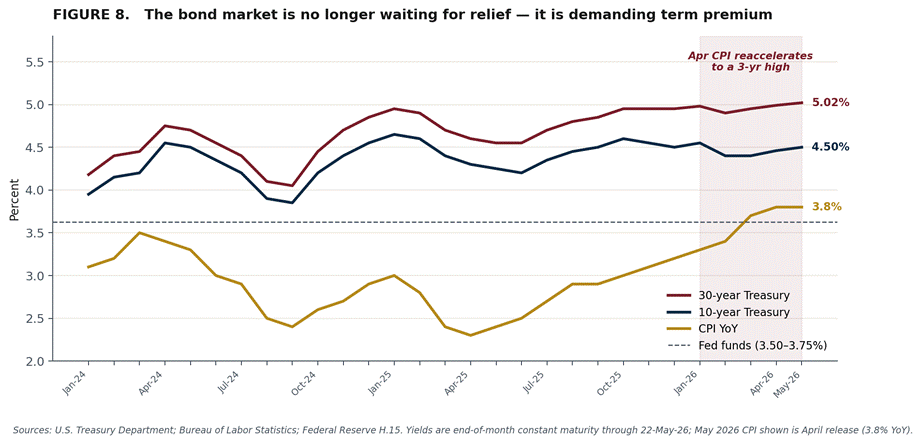

A year ago the consensus expected an easing cycle. The opposite has happened. As of late May 2026 the 10-year Treasury sits near 4.50% and the 30-year has pushed above 5% - its highest in more than a decade - after April CPI reaccelerated to 3.8%, the hottest reading in nearly three years. The Fed funds rate is still 3.50–3.75%, but the two-year yield has climbed above the lower bound of that range and futures markets have flipped from pricing cuts to pricing a possible hike by December. The bond market is no longer waiting for relief; it is demanding a higher term premium to fund persistent deficits. For most of the equity market this is a threat. For the hard-asset thesis it is the enforcement mechanism.

The supply channel: today’s high rates are tomorrow’s scarcity

Capital-intensive assets - power plants, apartments, mines, pipelines - are financed at the margin, so when the cost of capital rises the economics of building new supply collapse first. A project that pencils at a 5% cost of debt does not pencil at 8%; starts fall, pipelines empty, and the future supply that would have competed away tomorrow’s pricing power simply never gets built.

Set that frozen supply curve against demand that keeps growing - households form, data centers draw power, the world keeps eating - and the balance tightens for the existing stock, letting in-place owners raise rents, tariffs, and prices faster than before.

Higher rates also lift replacement cost directly, since financing and construction both cost more, which widens the discount at which an existing asset trades below the cost of building a new one. That replacement-cost gap is the moat. So the core claim holds: higher-for-longer suppresses new hard-asset investment, and that suppression is itself the source of future hard-asset inflation.

The one exception: why data centers are immune to the supply channel

There is one corner of the physical-asset universe where the supply-channel logic above breaks down, and it is worth being honest about it. Data centers are not behaving like a normal capital-intensive sector under higher-for-longer. In a normal sector, an 8% cost of debt would kill marginal projects, choke deliveries, and reward the patient holder of existing stock. In data centers, deliveries are accelerating into the highest cost of capital in fifteen years, lease rates are still climbing, and the build-out is racing to outpace permitting and power interconnect rather than financing. The reason is that the marginal buyer of data-center capacity is not a developer modeling a project IRR - it is a hyperscaler with a $200 billion annual capex budget, a balance sheet generating tens of billions in operating cash flow, and a strategic mandate that has detached almost entirely from project-level economics.

The five largest cloud platforms are guiding to a combined $700–$725 billion of 2026 capex - up 77% year-over-year and running at 45–57% of revenue, capital intensities historically reserved for railroads in the 1880s and oil majors in the 1970s. These are not numbers that survive a discounted-cash-flow exercise. They survive a different exercise entirely: if a competitor secures the GPU capacity, the data-center site, and the power interconnect, and we do not, we lose the next decade of AI. That logic - competitive parity, optionality on a winner-take-most platform - does not bend to interest rates. It barely bends to ROI.

That makes data-center pure-plays a flow trade - own them while the capex wave is still cresting - rather than a scarcity trade. It also means the structurally tighter play in the AI-power complex is not data centers themselves but the inputs they consume: power generation, transformers and switchgear, water rights for cooling, and the trades and grid hardware whose supply curves do obey the cost of capital. Hyperscaler indifference to economics is precisely what creates the scarcity rent outside it.

The double edge: a wealth transfer to the patient owner

The same high rates that choke new supply also compress the value of existing assets in the near term - a higher discount rate lowers the present value of any long-duration cash flow - and they punish leveraged owners through higher debt service. Higher-for-longer is therefore not a uniform tailwind; it is a wealth transfer. It moves value away from the marginal developer and the over-levered owner who bought at the peak, and toward the patient, modestly-levered owner of an irreplaceable asset who can hold through the air pocket and collect the re-accelerating cash flows on the far side. The losers and the winners both sit inside the hard-asset universe - the rate regime simply decides which is which.

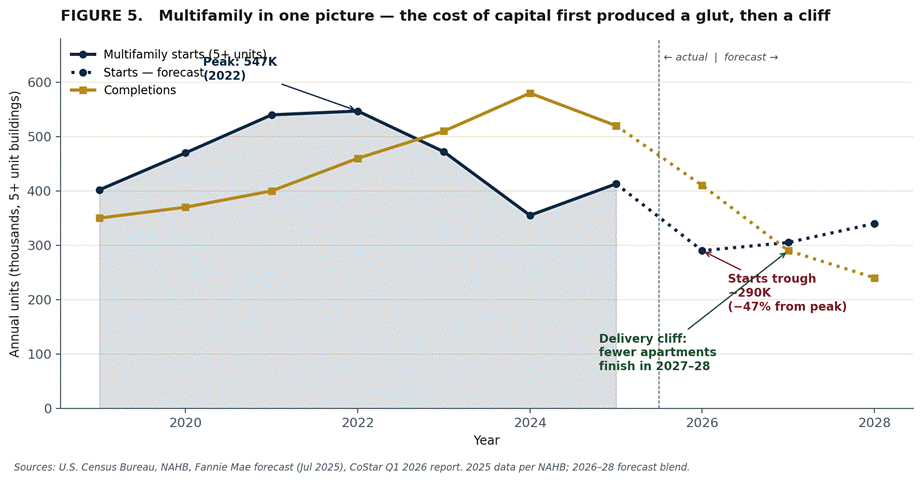

Multifamily is the textbook case, and the right one to reach for. Higher rates, construction costs, and tight financing have driven multifamily starts to roughly 55,000 units in Q1 2026 - the lowest quarterly pace since 2011 and down 73% from the early-2022 peak. Because deliveries lag starts by 18–24 months, the record wave of 2024–25 first produced a glut: national vacancy rose, rents briefly turned negative year-over-year, and 2021–23-vintage deals bought at ~4.5% cap rates and refinanced into higher debt service began clearing 15–25% below peak values.

That is the painful near edge of the double-edged sword. But the pipeline behind the glut has fallen off a cliff, and as the wave is absorbed through 2026–28 - into the same 4–5-million-unit structural shortage - rent growth is set to re-accelerate for the owners who survived. Higher rates created both the distress and the scarcity; the only question was ever who could hold long enough to land on the right side of it.

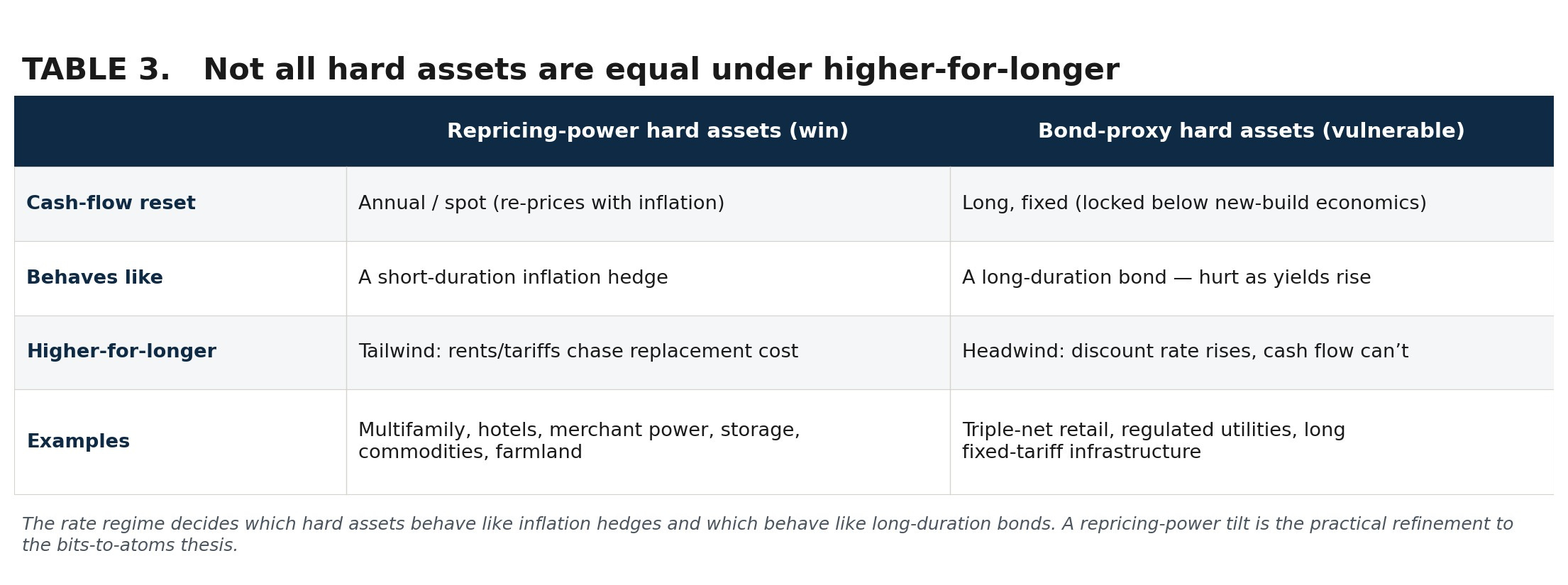

Not all hard assets are equal under higher-for-longer

This is the discernment the rate regime forces, and it is the most important practical refinement to the thesis. The hard assets that win are those whose cash flows re-price quickly - annually or at spot - so they chase inflation upward: multifamily, self-storage, commodities, short-lease farmland. The hard assets that suffer are the bond proxies, whose cash flows are locked into long fixed leases or regulated returns: triple-net retail, classically-regulated utilities, long fixed-tariff infrastructure. The latter trade like the long-duration bonds whose yields are rising, and they fall for the same reason. A hard-asset allocation built for higher-for-longer is therefore not a generic basket of “real estate” or “infrastructure” - it is a deliberate tilt toward repricing power

The fiscal-dominance loop: why the regime ultimately favors atoms

There is a final, reflexive turn. The very forces that demand hard assets - reshoring, the energy transition, defense rebuilds, and the AI capex super-cycle - are themselves inflationary and largely deficit-financed, which is part of why the term premium and long rates are rising in the first place.

The bond market is now pricing this openly: a Bank of America survey in May found 62% of fund managers expecting a 6% thirty-year yield. Yet there is a ceiling on how high real rates can go, because U.S. interest expense already runs at several percent of GDP. Past some point, servicing the debt forces the authorities toward financial repression - holding nominal rates below the rate of inflation.

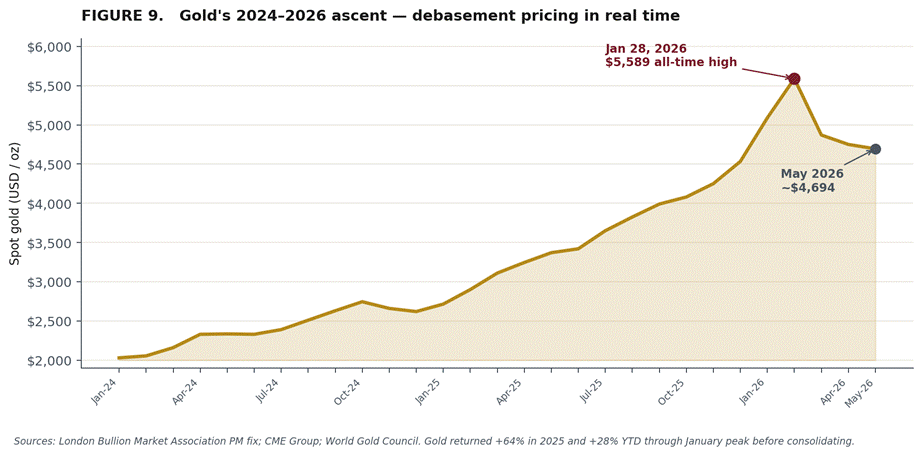

In that endgame real rates turn low or negative even as nominal rates stay “high,” and negative real rates are the single most powerful tailwind a non-yielding, scarce, physical asset can have. It is precisely why gold printed an all-time high of $5,589 on January 28, 2026 alongside rising nominal yields - a combination that bewilders anyone still using the old playbook.

The cost of capital is not this thesis’s enemy. Higher-for-longer is the discipline that starves new supply, the sieve that separates patient owners from levered speculators, and - through the fiscal-dominance loop - the force that ultimately drives real rates toward zero and below. It is not the threat to the hard-asset trade. It is its enforcement.

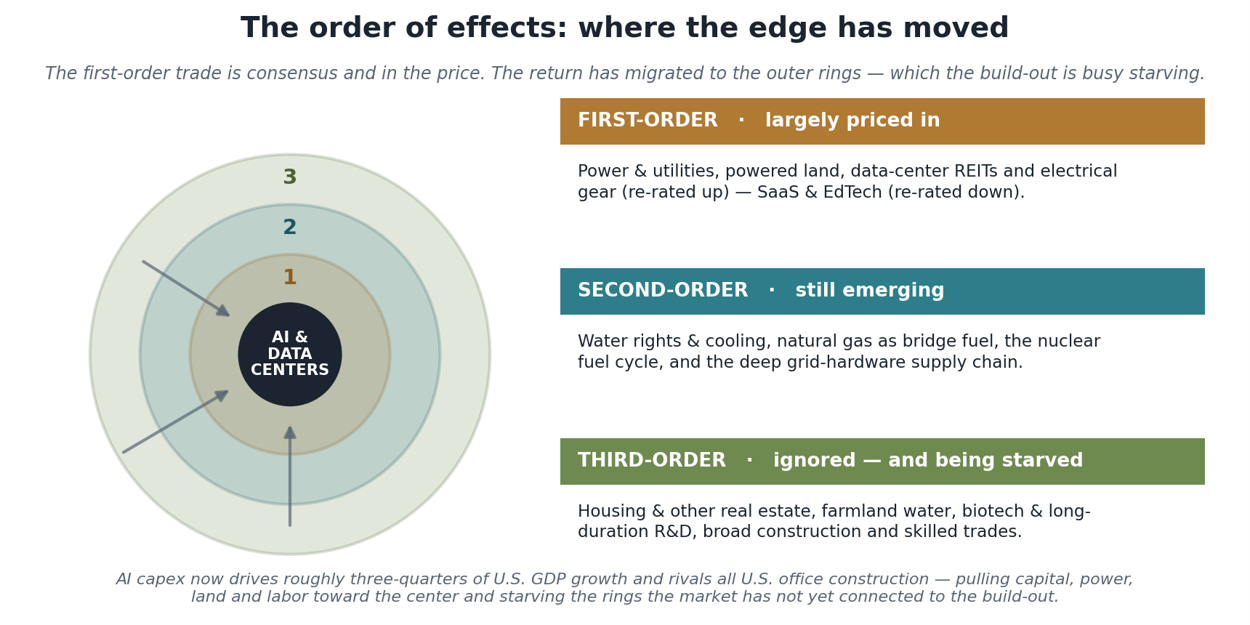

VIII. The Order of Effects: Where the Edge Has Moved

A thesis is only worth money to the extent it is not yet in the price. By mid-2026 the first-order version of the bits-to-atoms trade is largely consensus - and largely priced. The edge has migrated outward, to the second- and third-order beneficiaries the market has not yet wired to the AI build-out. And there is a twist that makes the outer rings more interesting still: the build-out is not merely creating demand for them; it is actively starving them of capital and inputs, which is precisely the supply-suppression dynamic that seeds the next scarcity.

First-order: already in the price

The first ripple has been fully absorbed. Owners of power and “powered land” - generation with firm capacity and, above all, a position in the interconnection queue - have re-rated dramatically: Constellation, Vistra, and NextEra; the data-center REITs Equinix and Digital Realty; and the electrical-equipment makers GE Vernova, Eaton, and Vertiv. “Powered land” has become a recognized, premium-priced asset class in its own right. On the short side, SaaS and EdTech have de-rated just as violently. The trouble with a consensus trade is that the asymmetry is gone: buying a utility in mid-2026 because “AI needs power” is buying into a story the market already recognizes. The first-order trade has done its work.

Second-order: the inputs the market has only half-noticed

The market has priced AI’s appetite for power. It has not fully priced its thirst for water, nor the deep supply chains that power itself depends on. Every megawatt of compute is also a draw on cooling water and, upstream, on the water used to generate the electricity and fabricate the chips - a large campus can consume the supply of a small town, and two-thirds of new sites sit in water-stressed regions. Yet water rights and water infrastructure remain illiquid, fragmented, and cheap relative to power: the market connected AI to electrons but not to acre-feet.

The same half-noticed quality attaches to natural gas as the bridge fuel; to the nuclear fuel cycle (enrichment, conversion, and uranium) sitting behind the reactor-restart headlines; and to the unglamorous deep supply chain of the grid itself - transformers, grain-oriented electrical steel, switchgear, and copper, now on multi-year backorder. Owning the bottleneck two steps upstream of the obvious winner is where second-order return lives.

Third-order: what the build-out is crowding out

Here is the part almost no one is modeling, and it is the most important. The build-out is not happening in a vacuum. It is competing, in the same economy and frequently the same counties, for a finite pool of capital, power, land, construction materials, and skilled labor. AI-related capex now drives roughly three-quarters of U.S. GDP growth, runs near 4% of GDP, and is on track to rival the entire U.S. office-construction market - and every interconnection slot, every transformer, every electrician, every cubic yard of concrete, and every dollar of risk capital that flows to a data center is one that does not flow to a house, a factory, a farm, or a laboratory.

That redirection lands hardest on the assets no one is connecting to AI at all. Other real estate and housing compete with data centers for the same trades, same land, same equity and debt capital; the housing supply cliff is being deepened by a build-out that out-bids homebuilders for the marginal electrician and the marginal megawatt. Farmland and agricultural water lose the bidding war for water in stressed basins, raising the scarcity value of secure agricultural rights. The skilled-trades wage premium - electricians, pipefitters, HV linemen - has compounded faster than any equity index over the last three years and is being capitalized into every infrastructure project the build-out forces into existence. None of these show up on a screen of AI beneficiaries; all of them are downstream of the same demand.

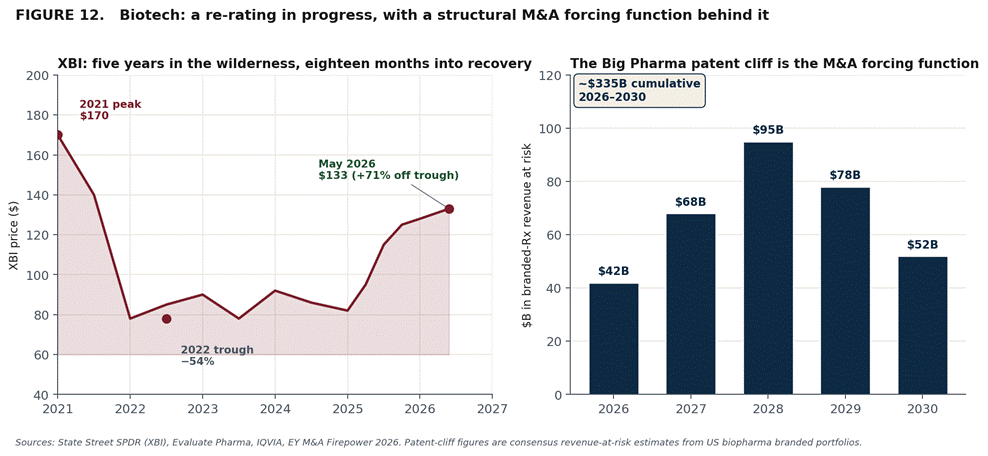

Biotech: the third-order story worth pulling on its own thread

Biotech deserves a paragraph of its own, because the third-order logic is unusually clean. The XBI sits roughly 22% below its 2021 peak in absolute terms despite a furious 71% rally off the 2022 trough - a re-rating that is already happening but has barely closed half the gap to the prior cycle high. Behind that recovery sits a structural forcing function the market has not fully priced: the Big Pharma patent cliff is set to put roughly $335 billion of branded-prescription revenue at risk between 2026 and 2030, concentrating in 2028, which leaves the incumbents only one rational response - buy the pipeline they cannot grow. EY’s 2026 M&A Firepower report puts industry deployable capital above $1.4 trillion.

The bits-to-atoms reading is the interesting part. AI-enabled drug discovery does exactly what AI does to every informational task - it commoditizes the discovery side, lowering the cost of generating viable compounds, expanding the candidate funnel, and accelerating the rate at which molecules reach the clinic. The physical pieces of the chain, however, are not commoditized at all. Wet-lab capacity in Cambridge and South San Francisco is fixed by zoning, permitting, and a decade of build time; FDA-approved biomanufacturing capacity (large-molecule cell-culture, fill-and-finish, cell-and-gene therapy) is bottlenecked at a handful of CDMOs (Lonza, Catalent, Samsung Biologics, WuXi) whose facilities take three to five years to bring online; cold-chain logistics for biologics is its own thin supply chain. AI makes more compounds; only physical capacity can manufacture, test, and distribute them.

Alexandria Real Estate (ARE) - the dominant landlord of irreplaceable U.S. life-sciences lab space - trades roughly 55% below its 2021 peak even as its rents reset upward and replacement cost of its Cambridge/Mission Bay/Triangle assets is structurally rising. That gap is not an indictment of the business; it is the third-order trade waiting to be made.

It is worth being honest that the crowding-out story above is a forward thesis, not yet a settled fact: some strategists read the same data as a rational, proportionate redirection of capital toward higher-return projects rather than a starving of the periphery. But that is exactly the disagreement that creates the opportunity.

The first-order trade rewarded those who saw, early, that AI needs power. The second- and third-order trades will reward those who see what power itself needs - water, fuel, solar, and grid hardware - and what the entire build-out is quietly bleeding dry: housing, farmland water, long-duration R&D, and the physical infrastructure of the life sciences. The edge is no longer at the center. It is in the outer rings.

IX. The Inversion

For thirty years the market operated under a simple hierarchy: bits over atoms, code over concrete, platforms over pipes. It made sense in a world where digital distribution was the scarce resource and physical assets were abundant and cheap. That world is ending - not because the great platforms are failing, but because the marginal value of informational innovation is declining while the marginal value of physical scarcity is rising. AI is the inflection point: by making information processing essentially free, it has commoditized the very capability asset-light businesses were built to monetize; and by requiring massive physical infrastructure to operate, it has made power, cooling, land, water, minerals, and data centers the binding constraint on growth.

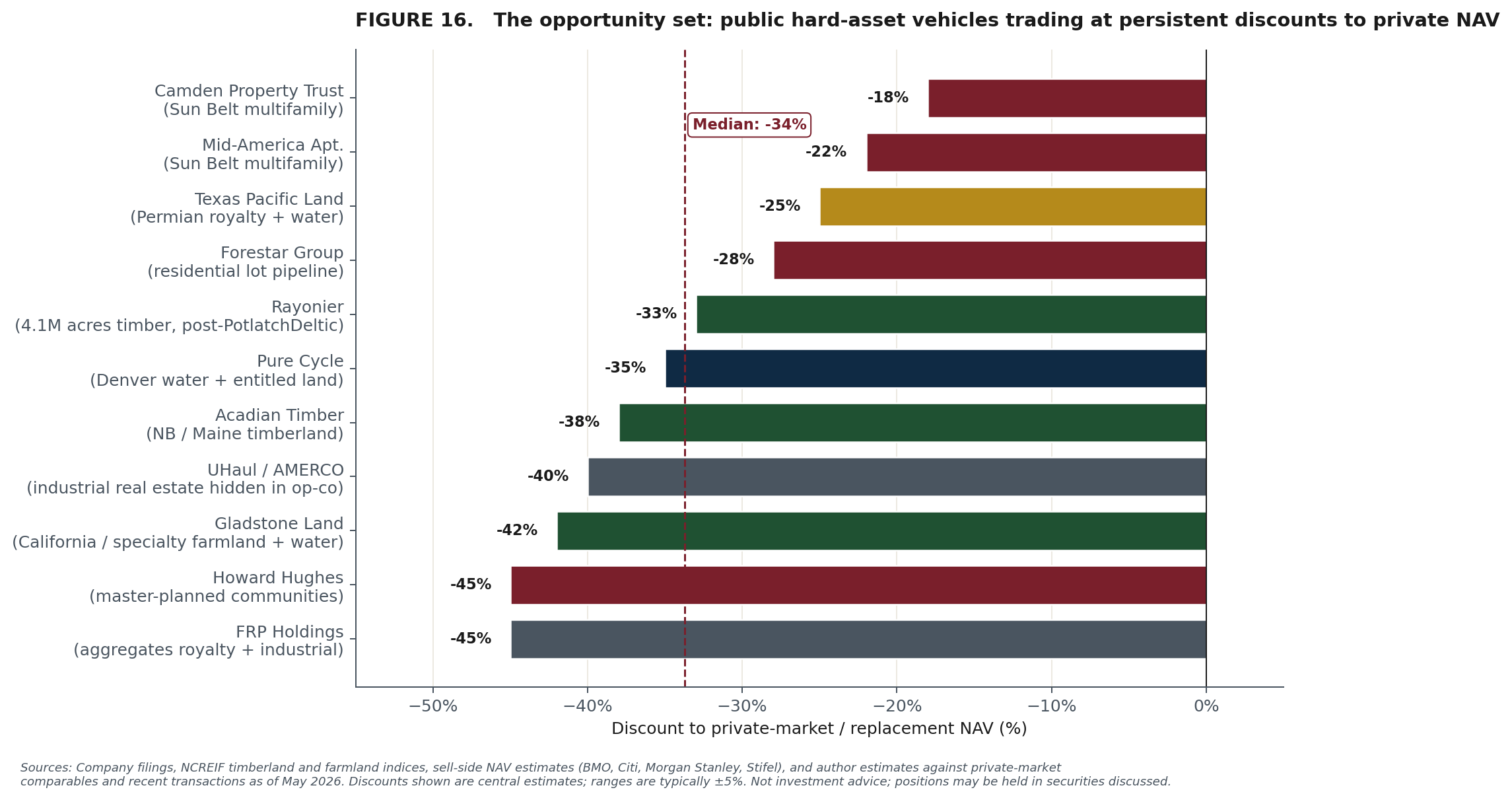

The opportunity for early movers remains asymmetric. With capital rotating back toward hard assets, a rate regime of higher-for-longer, and inflation that refuses to behave, the structural tailwinds for hard-asset revaluation are the most powerful in modern market history - and the listed vehicles that express them still trade at meaningful discounts to private value. The risk/reward is not subtle.

The Golden Age of SaaS is in the rearview mirror. What replaces it is not a golden age of AI - though AI will be transformational - but a golden age of the physical world: the assets that cannot be replicated, cannot be downloaded, cannot be generated by a language model, and cannot be substituted by any technology yet conceived.

The inversion is here. The atoms are winning.

Good piece, and water is the right second derivative to pull on. Where I’d push back: the market has recognized water. What it still can’t/doesn’t do is book it. The rights that clear at auction re-rate. The water two steps upstream of the data center doesn’t, because it isn’t legible yet. That gap is the trade.

This is exactly the market structure shift I’m watching.

The last cycle rewarded asset-light businesses because software could scale faster than physical constraints. The next cycle may reward the opposite: control over power, compute, commodities, infrastructure, logistics, and real-world capacity.

When scarcity moves from code to atoms, capital allocation changes. Margins, moats, and valuation multiples have to be rebuilt around physical bottlenecks, not just digital distribution.

That is the framework I care about: how macro scarcity transmits into sectors, balance sheets, and portfolio construction.