Tejon Ranch (TRC) | Part 1: 270,000 Acres at the Gateway to Los Angeles

50% + NAV Discount | Water, power, entitled homes, and an AI-era energy corridor as a free call option

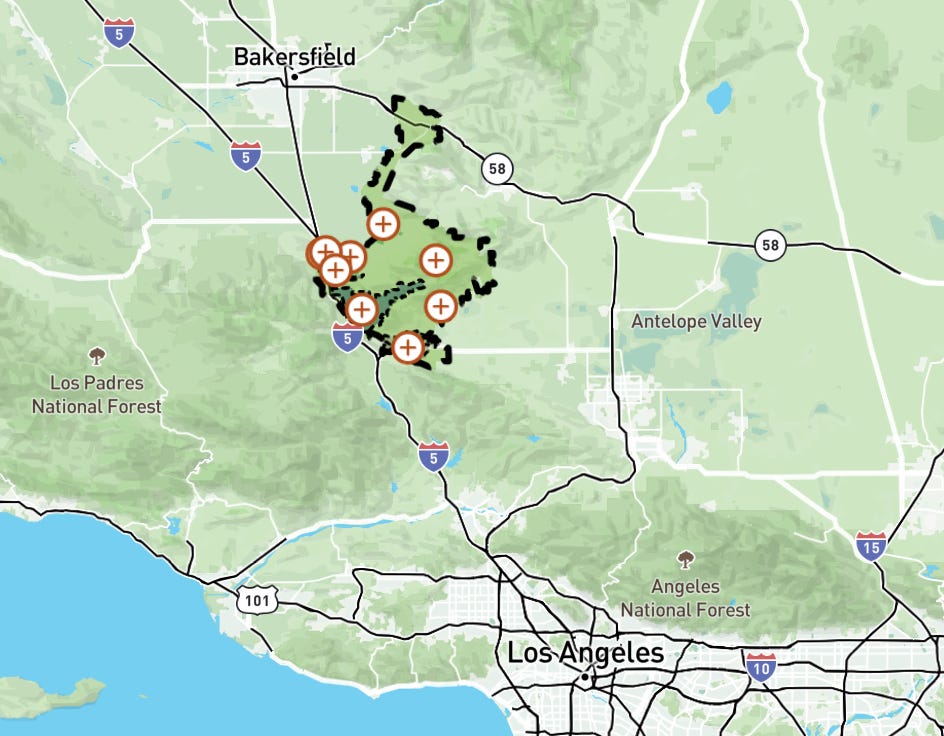

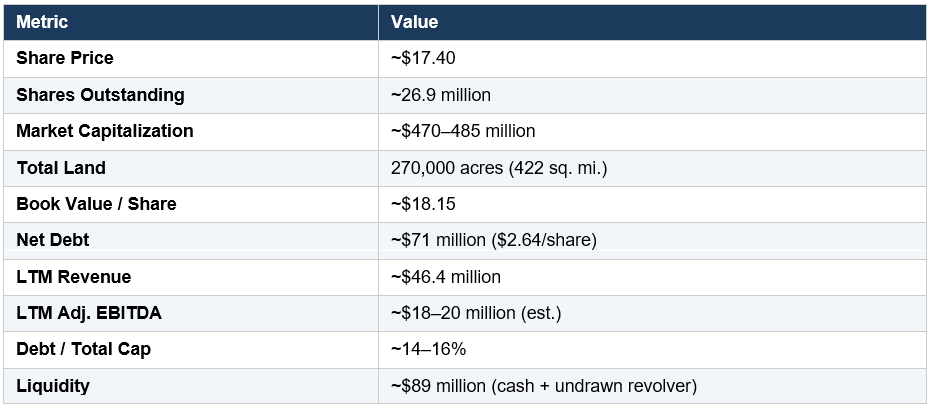

Tejon Ranch Co. (NYSE: TRC) is one of the most unique publicly traded real estate companies in the United States. At approximately $17–18 per share and a market capitalization of roughly $470–485 million, the stock trades at a deep discount to the normalized net asset value of its underlying land, infrastructure, water rights, and entitled development pipeline. The company owns 270,000 contiguous acres (422 square miles) - an area nearly as large as the City of Los Angeles - positioned directly at the geographic chokepoint between Northern and Southern California on Interstate 5.

This is not merely a landholding company. Tejon Ranch sits at the intersection of California’s most critical infrastructure corridors: highways (I-5, SR-58, SR-138), rail (Union Pacific, potential High Speed Rail), the California Aqueduct (30 miles transecting the property), power transmission lines (PG&E, SCE), and fiber optic networks (AT&T, CVIN). Every resource moving between the two halves of California’s $4 trillion economy passes through Tejon’s land.

The investment thesis rests on a central insight: the market values Tejon Ranch at roughly its book value—approximately $18 per share—while carrying the land at historical cost basis from acquisitions dating to the 1930s and 1940s. The TRCC industrial platform alone, using market-comparable cap rates and land values, generates an illustrative NAV of $14–20+ per share. This means the market is assigning zero or negative value to 35,000+ entitled and partially entitled residential units, 240,000 acres of conservation and ranch land, 142,000+ acre-feet of water rights, mineral royalties, the Pastoria power plant ground lease, and numerous other revenue-generating assets.

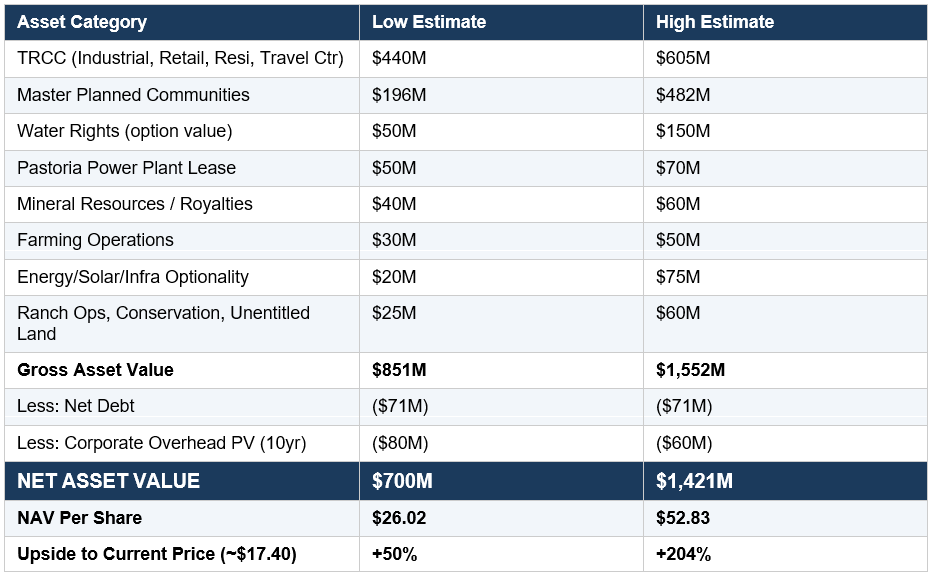

II. NET ASSET VALUE: ASSET-BY-ASSET ANALYSIS

The following analysis derives a normalized NAV by estimating market values for each of Tejon Ranch’s major asset categories. Carrying values on the balance sheet dramatically understate economic reality because the land was acquired for essentially zero basis in 1936 and the company uses historical cost accounting.

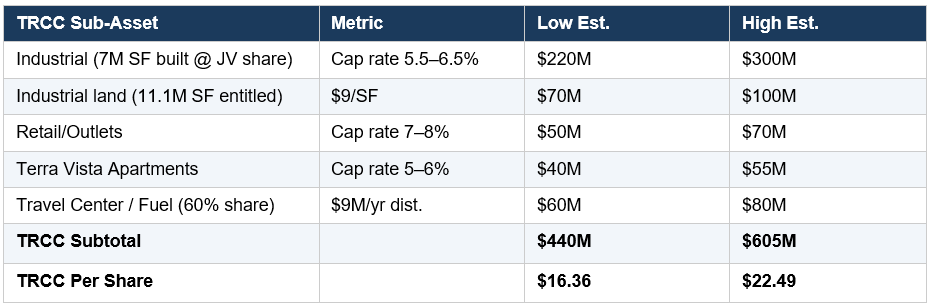

A. Tejon Ranch Commerce Center (TRCC)

TRCC is the crown jewel and the only asset currently generating meaningful, visible cash flow. It is a 20-million-square-foot-entitled, mixed-use commercial/industrial/retail/residential campus straddling I-5, roughly equidistant between Los Angeles and Bakersfield.

Built and Operational Assets

• Industrial: ~7 million sq. ft. built, 100% leased. Tenants include IKEA, Caterpillar, Nestlé, Famous Footwear, Dollar General. An additional 11.1 million sq. ft. of entitled industrial capacity remains. Industrial land has appreciated from $0.57/sq. ft. in 2000 to ~$9.00/sq. ft. today - a 1,500%+ increase.

• Retail/Outlets: ~674,000 sq. ft. of commercial retail (Outlets at Tejon), 95% occupied. Tenants include Nike, Polo Ralph Lauren, Tommy Hilfiger. Approximately 282,000 sq. ft. of additional entitled retail remains.

• Residential (Terra Vista): 228 apartments delivered in Phase 1 (spring 2025), with entitlements for up to 495 total units. Over 55% leased as of Q3 2025. Provides critical workforce housing for the ~5,000 industrial employees at TRCC.

• Travel Center/Fuel: TA/Petro joint venture (60/40 TRC ownership). One of the busiest travel centers in California, serving ~100,000 vehicles/day on I-5. Has paid $45 million in cash distributions over a recent five-year period.

TRCC NAV Estimation

The company’s own investor presentation showed TRCC generating an illustrative NAV per share of $14.65–$20.11, representing a 96x–132x return on the original $0.15/share basis cost of the land. Using conservative market-comparable assumptions:

At the low end, TRCC alone accounts for nearly all of the current market capitalization. This means the market is pricing the remaining 260,000+ acres, all residential entitlements, water rights, mineral royalties, and other assets at effectively zero.

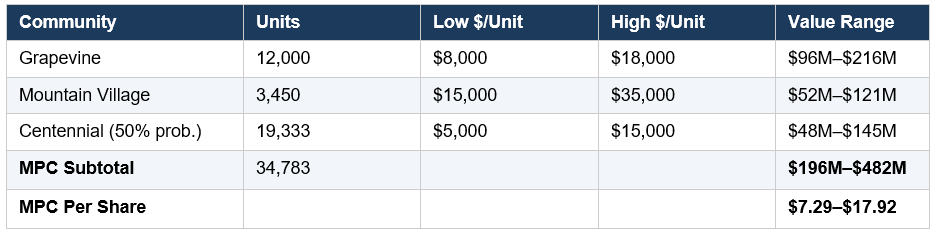

B. Master Planned Communities (35,000+ Homes Entitled)

Tejon Ranch has three master planned communities at various stages of entitlement and development, collectively representing over 35,000 residential units and more than 15 million sq. ft. of commercial space.

1. Grapevine at Tejon Ranch (Kern County)

• 12,000 residential units + 5.1 million sq. ft. of commercial space

• 8,010 acres, with 4,200 developable and 3,800 designated open space

• Kern County Board of Supervisors approved 5-0 in 2016; reaffirmed 5-0 in 2019

• Adjacent to TRCC, designed to house workers at the Commerce Center

• Expected 20-year buildout; nearest-term residential MPC after Terra Vista

2. Mountain Village (Kern County)

• ~3,450 luxury residential units plus resort/hotel components

• High-country location on the western portion of the ranch near Lebec

• Entitled by Kern County; currently in tract map preparation stage

• Targets upscale/resort buyers seeking nature-oriented lifestyle near LA

3. Centennial at Tejon Ranch (Los Angeles County)

• 19,333 residential units (including 3,480+ affordable) + 10.1 million sq. ft. commercial

• ~12,000 acres in northwest LA County

• Approved by LA County Board of Supervisors in 2019, but subject to litigation

• June 2025 Court of Appeals decision rescinded approvals on narrow EIR grounds (prevailed on 20 of 23 claims)

• Re-entitlement process underway; management targets late 2026 for new Board action

• Designed as net-zero GHG community; addresses California’s acute housing shortage

MPC Valuation

Valuing entitled but undeveloped residential land in California requires adjusting for regulatory risk and time to monetization. Comparable entitled residential land in Southern California ranges from $30,000 to $105,000+ per acre. Applying conservative per-unit and per-acre values:

Note: Centennial is probability-weighted at 50% given the re-entitlement risk. Grapevine and Mountain Village carry higher probability given their Kern County approvals and less contested litigation history. These figures use deeply conservative per-unit values - comparable California MPC lots frequently trade at $30,000–$100,000+ per fully improved lot.

C. Mineral Resources, Water, Energy & Ranch Operations

Water Rights & Infrastructure

Tejon Ranch’s water portfolio is among its most strategically valuable and underappreciated assets. The California Aqueduct runs 30 miles through the property, providing both a source and delivery mechanism. Key water metrics:

• ~142,000–148,000 acre-feet of water held for future use and purchased water contracts

• State Water Project (SWP) entitlements under long-term contracts

• On-ranch and off-ranch water banking capabilities

• Average annual net cash flow from water: ~$2.4 million (temporary right-of-use leases)

• Water sufficient for full buildout of all real estate developments

• Strategic optionality: water is monetizable via temporary leases without selling underlying rights

In water-scarce California, these rights function as a perpetual call option. Water rights in the southern San Joaquin Valley and greater LA basin have been transacting at $2,000–$10,000+ per acre-foot for permanent transfers. Even at a conservative $1,500/AF, 142,000 AF represents $213 million in embedded value - though the company would never sell its permanent rights, this illustrates the floor value of the optionality.

Pastoria Energy Center (Ground Lease)

• 750 MW natural gas-fired combined-cycle power plant, owned/operated by Calpine

• Located on land leased from Tejon Ranch

• Generates $4+ million in annual ground lease revenue

• CPI-escalating rent; long-term lease structure

• At a 6–8% cap rate: ~$50–70 million in value

Mineral Resources

• Oil and gas royalties from multiple leases across the ranch

• Rock and aggregate royalties

• Cement royalties from National Cement (producing 23 million cubic yards)

• Combined mineral and commercial ground lease revenues: ~$7 million/year average

• Minimal capital requirements; pure royalty income

Other Infrastructure & Revenue

• 390 miles of major utility infrastructure easements (electricity, oil, gas, telecom)

• Fiber optic routes (AT&T, CVIN)

• Microwave, radio, and cellular transmitter site leases

• Solar development potential (Calpine has developed plans for industrial-scale solar adjacent to Pastoria)

• Pumped hydro energy storage feasibility (Premium Energy proposed a 1,000 MW facility connected to the California Aqueduct on/near Tejon Ranch)

Farming Operations

• Active farming of almonds, pistachios, wine grapes, olives, and hay

• 12-year adjusted farming EBITDA: $61.3 million (21% margin)

• Cyclical but consistently cash-generative; crops are irrigated via highly efficient drip systems

• Q3 2025 farming revenue up 34% YoY driven by almond crop recovery

• Farming is a holding-period monetizer that produces income while land awaits higher-value uses

Ranch Operations & Conservation

• Grazing leases, game management, filming revenues

• 240,000 acres permanently conserved under 2008 Conservation and Land Use Agreement with five major environmental groups (Audubon, Sierra Club, NRDC, Endangered Habitats League, Planning and Conservation League)

• Only 10% of the ranch (27,000 acres) designated for development; 90% conserved

• Conservation agreement provides regulatory and social license that competitors cannot replicate

D. Consolidated Net Asset Value Summary

Even applying a 30–40% “liquidity / time-to-monetization” discount to the midpoint NAV of ~$39/share yields an adjusted target of $23–27 - still 35–55%+ upside from current levels.

III. MANAGEMENT & GOVERNANCE

New CEO: Matthew Walker

Matthew Walker was appointed President and CEO in early 2025, representing a significant inflection point. Within his first eight months, he has executed several initiatives that signal a break from the company’s historically opaque and passive management style:

• Cost discipline: 20% workforce reduction saving ~$2 million annually. This is the first meaningful headcount restructuring in the company’s modern history.

• Transparency revolution: Hosted Tejon’s first-ever quarterly earnings call in Q3 2025 and an Investor Engagement Event at the NYSE in November 2025.

• Strategic framework: Articulated four strategic pillars - Income, Growth, Governance, and Culture - with specific hurdle rates (12% unlevered IRR primary, 18% levered IRR secondary).

• Capital allocation reset: Signaled preference for joint venture (JV) financing on capital-intensive projects rather than balance sheet funding, preserving equity value.

• Shareholder engagement: Proactively published CEO letters and opened dialogue with activist investors.

Board Composition

The board has undergone significant refreshment: 40% of directors were added within six months of Walker’s arrival. 90% of directors are independent. TowerView LLC, the largest shareholder, has board representation (Daniel Tisch). The board removed classified director terms in response to shareholder feedback. A 2025 proxy contest with Bulldog Investors resulted in activist nominee Andrew Dakos joining the board, adding a value-oriented investor perspective.

The governance improvements are material. For years, Tejon Ranch operated more like a private fiefdom than a public company - no earnings calls, limited investor communication, and questionable capital allocation. The current regime represents the most shareholder-friendly governance in the company’s modern history.

IV. WHAT THE MARKET IS MISSING

1. The Historical Cost Accounting Illusion

Tejon Ranch carries its land on the balance sheet at historical cost - much of it from its original 1936 acquisition at effectively $0 per acre. Book value of ~$18/share tells investors almost nothing about the economic value of entitled California real estate, water rights, mineral royalties, and infrastructure easements. Traditional earnings-based or book-value-based screening misclassifies TRC as a mediocre small-cap with minimal earnings. In reality, it is a deeply undervalued real asset portfolio hidden inside a public equity wrapper.

2. Earnings Power Is Deliberately Suppressed

The company generates only ~$46 million in annual revenue and minimal net income because it is in the pre-monetization phase of its most valuable assets. Entitlement costs, litigation defense, and infrastructure investment suppress current earnings. This is analogous to a biotech company spending on R&D before a drug launch - current financials do not reflect terminal asset values. The $110 million in cumulative TRCC cash flows since 2000 demonstrates what happens when entitled land is actually developed.

3. Scarcity Value Is Real and Increasing

There is no other 270,000-acre contiguous land holding available for purchase anywhere near Los Angeles. California’s regulatory environment (CEQA, the Endangered Species Act, local opposition) makes it virtually impossible to assemble and entitle a comparable development pipeline today. The company’s own management has described this as likely “the last regional development at this scale in California.” The 2008 Conservation Agreement with five major environmental groups provides regulatory and social license that would take decades to replicate. This is a true barriers-to-entry moat.

4. The Hard Rock Casino Catalyst

Hard Rock Casino Tejon, a $600 million facility owned by the Tejon Indian Tribe and managed by Hard Rock International, opened on November 13, 2025 - directly adjacent to Tejon Ranch’s properties. Phase 1 includes a 150,000 sq. ft. gaming floor with 2,500+ slot machines and 50+ table games, 7 restaurants, and already paid $10 million in jackpots in its first 10 days. Phase 2 (expected late 2027) adds a 400-room hotel, pool/spa, and 2,800-seat Hard Rock Live concert venue.

While Tejon Ranch Co. does not own the casino, the spillover effects are enormous: additional traffic on I-5, increased visibility for the Outlets at Tejon, new demand for workforce housing at Terra Vista, enhanced appeal for Grapevine residential development, and general economic development that raises land values across the entire southern Kern County footprint.

5. No Analyst Coverage, No Institutional Attention

TRC has virtually no sell-side coverage. Average daily trading volume is ~86,000 shares. The market cap of ~$475 million puts it below the threshold for most institutional mandates. This creates a persistent informational inefficiency - exactly the type of situation where patient, research-intensive investors can extract outsized returns.

V. SCARCE ASSETS OR SIMPLY LAND?

This is the critical question for any Tejon Ranch analysis. The answer is definitively that these are scarce, irreplaceable assets - not merely dirt.

Why These Assets Are Truly Scarce

• Geographic monopoly: Tejon Ranch controls the only viable east-west and north-south corridor between the Central Valley and Los Angeles. Every highway, rail line, aqueduct, power line, and fiber optic cable connecting these two massive economic regions passes through the ranch. This cannot be replicated.

• Regulatory moat: California’s entitlement process is the most difficult in the nation. It took Tejon Ranch 20+ years to secure its current entitlements. No competitor can assemble, entitle, and develop a comparable pipeline - the regulatory barriers are simply too high. The company’s Conservation Agreement with major environmental groups gives it unique social license.

• Water rights: In California, water is often more valuable than the land itself. Tejon’s 142,000+ acre-feet of banked and contracted water, sourced from the California Aqueduct running directly through the property, represents an irreplaceable asset in an increasingly water-scarce state.

• Infrastructure density: 390 miles of utility infrastructure already traverse the ranch. This existing easement and infrastructure base dramatically lowers the cost and time to develop new projects - whether industrial, residential, or energy-related.

• Four ecosystem convergence: The ranch sits at the confluence of the Central Valley, Sierra Nevada foothills, Mojave Desert/high desert, and coastal mountains. This unique topography and geography create intrinsic value across farming, energy, minerals, residential, and conservation uses.

Comparable land simply does not exist. The closest analog might be historical comparisons to Irvine Ranch or other large California ranches that were developed over decades into multi-billion-dollar real estate portfolios. But those opportunities are gone - Tejon represents the last one of its kind.

VI. THE AI / DATA CENTER / ENERGY ANGLE

This is where the long-term optionality of Tejon Ranch becomes most compelling - and most speculative.

The Power & Connectivity Foundation

Tejon Ranch’s infrastructure profile reads like a data center developer’s wish list:

• 750 MW of existing power generation (Pastoria Energy Center) on the property

• Major PG&E and SCE transmission lines crossing the ranch

• 30 miles of California Aqueduct providing cooling water access

• Fiber optic backbone (AT&T, CVIN) already traversing the property

• Enormous flat, developable land adjacent to existing power infrastructure

• Location between the two largest data center markets in the western U.S. (LA and the Bay Area)

Why AI Infrastructure Could Be Transformative

The U.S. is experiencing an unprecedented surge in data center demand driven by AI workloads. Lawrence Berkeley National Laboratory projects data center electricity demand will grow from 176 TWh in 2023 to 325–580 TWh by 2028. Hyperscale developers (Google, Microsoft, Amazon, Meta) are urgently seeking sites with three attributes: available power, water for cooling, and land. Tejon Ranch has all three in abundance.

Consider the economics: data center ground leases can command $50,000–$150,000+ per acre annually for powered, connected sites. Even a modest 200-acre data center campus on Tejon Ranch could generate $10–30 million in annual ground lease revenue - transformative for a company currently generating ~$46 million in total revenue.

The company has not announced any data center deals, and this remains entirely speculative. But the physical assets are in place, and the convergence of power, water, fiber, and available land at scale is exceptionally rare in California. If even one hyperscale developer targets this corridor, the land value implications would be enormous.

Solar & Energy Storage

Beyond data centers, the ranch is positioned for California’s clean energy buildout. Calpine has already developed plans for industrial-scale solar adjacent to Pastoria. Premium Energy Holdings has proposed a $2–3 billion pumped hydro energy storage facility connected to the California Aqueduct on or near Tejon Ranch, capable of storing and releasing 3,500 GWh per year. While neither is confirmed, they illustrate the energy optionality embedded in the property.

As California pushes toward its 2030 and 2045 renewable energy targets, Tejon Ranch’s combination of abundant solar irradiance, existing grid interconnection, and proximity to major load centers makes it a natural site for utility-scale solar, battery storage, and potentially green hydrogen production.

VII. WATER & POWER: THE HIDDEN MOAT

Water Situation

Tejon Ranch’s water position is one of its most defensible competitive advantages:

• California Aqueduct: 30 miles of the State Water Project’s main canal run directly through the property, providing both sourcing and delivery infrastructure. The Edmonston Pumping Plant, the world’s highest single-lift pumping plant, pushes water over the Tehachapi Mountains nearby.

• Banked water: 142,000–148,000 acre-feet of water held in banks on and off company land, plus long-term SWP entitlement contracts. This is sufficient for full buildout of all planned developments.

• Monetization: While awaiting development, water is monetized through temporary right-of-use leases (averaging $2.4 million/year net) and agricultural use. Critically, these are temporary leases - the permanent rights are never sold.

• SWP allocation variability: Annual State Water Project allocations fluctuate significantly with California’s wet/dry cycles. In drought years, Tejon’s banked water becomes even more valuable. In wet years, the company recharges its banks.

In California real estate, the saying is that “water flows uphill toward money.” Tejon has both the water and the money-generating real estate potential - a combination that is extraordinarily difficult to replicate.

Power Connectivity

The ranch’s power infrastructure position is equally formidable:

• PG&E and SCE high-voltage transmission lines cross the property

• Pastoria’s 750 MW facility is interconnected to the state grid

• Potential for behind-the-meter or co-located power generation for future tenants

• Solar development potential across thousands of flat, sun-drenched acres

• Proximity to the Tehachapi wind corridor, one of California’s major wind power regions

VIII. WHAT DOES THE COMPANY LOOK LIKE IN THE FUTURE?

Near-Term (2026–2028)

• TRCC flywheel accelerates: Terra Vista leases up, additional industrial spec buildings developed via JV partnerships, remaining 11 million SF of entitled industrial density begins to draw interest from major logistics operators

• Hard Rock Casino spillover drives increased traffic, retail revenue, and land appreciation

• Centennial re-entitlement progresses through LA County (target: late 2026 Board action)

• Grapevine tract mapping and infrastructure planning advances

• Potential energy/solar/data center lease announcements create positive catalysts

• Quarterly earnings calls and investor engagement continue to improve transparency

• Adj. EBITDA potentially reaches $25–30M as Terra Vista and TRCC industrial growth contribute

Medium-Term (2028–2033)

• Grapevine construction begins: first residential lots sold to homebuilders

• TRCC industrial build-out approaches 15+ million SF, approaching full entitlement

• Centennial (if re-entitled) begins infrastructure and first phases of development

• Mountain Village resort/residential development initiated

• Water asset value appreciated significantly as California drought cycles intensify

• Potential REIT conversion or partial asset spin-off to crystalize value

• Revenue potentially reaches $100–200M+ as lot sales, industrial rents, and residential revenue layer on

Long-Term (2033–2045)

• Grapevine and Centennial approach mid-buildout with thousands of occupied homes

• The “Tejon corridor” becomes a recognized regional economic hub between LA and Bakersfield

• Energy infrastructure (solar, storage, potentially data centers) generates material cash flow

• Total enterprise value potentially exceeds $2–4 billion as the development pipeline matures

• The company transitions from a pre-monetization land holding into a diversified real estate operating company with substantial, recurring cash flows

IX. IS THIS FAIRLY VALUED GIVEN TIME TO MONETIZATION?

The most legitimate bear case against Tejon Ranch is the time-value discount. Many of these assets will not generate meaningful cash for 5–15 years. A rational investor should discount long-dated cash flows accordingly.

However, several factors suggest the market’s implied discount is too severe:

• TRCC alone justifies the current price. At a conservative $440–600M+ valuation for TRCC, the market is paying nothing for everything else. The question is not whether the MPCs and other assets have value - it’s how much free optionality the market is giving away.

• Inflation is your friend. Land, water, and entitled real estate are among the best inflation hedges. Unlike financial assets that can be devalued by monetary policy, physical assets in supply-constrained California appreciate with inflation. A 3–4% annual land value appreciation rate over 10 years compounds the NAV substantially.

• Catalysts can accelerate the timeline. A data center lease, a major homebuilder JV, a solar PPA, or Centennial re-entitlement could each independently cause a significant re-rating.

• The discount rate should reflect asset quality. These are not speculative mining claims in the desert. They are entitled (or near-entitled), infrastructure-adjacent, water-secure California real estate assets. The appropriate discount rate is a real estate discount rate (7–10%), not an equity risk premium (12–15%+).

Applying a 10% discount rate over a 10-year monetization horizon to a midpoint terminal NAV of ~$40/share yields a present value of ~$15.40 - close to the current price. But this assumes zero interim cash flow (which is wrong: TRCC, farming, minerals, and water generate $15–20M+ annually now) and zero probability of accelerated monetization (data centers, new CEO initiatives, etc.). A more realistic discounted NAV, incorporating interim cash flows and a reasonable probability of positive catalysts, yields $22–30+ per share.

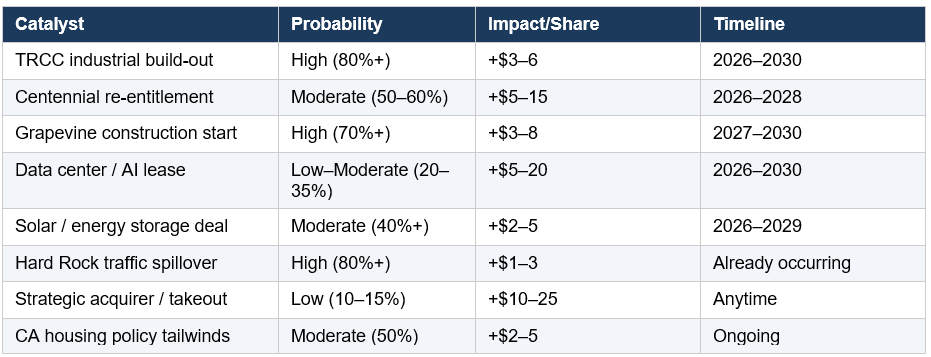

X. SOURCES OF ASYMMETRIC UPSIDE

The TRC investment opportunity is fundamentally asymmetric: the downside is cushioned by tangible, cash-flowing real assets, while the upside is driven by multiple independent catalysts, each of which could significantly re-rate the stock.

Catalyst Map

The asymmetry is structural: at ~$17/share, an investor is getting TRCC at cost with a free perpetual option on 35,000 homes, 142,000 AF of water, energy development potential on 270,000 acres, and the possibility that AI-driven infrastructure demand transforms the value of the ranch’s power-connected corridor.

XI. KEY RISKS

• Execution risk: New CEO is only ~12 months into the role. Strategic vision is promising but unproven in execution. History of management missteps and value destruction through poor capital allocation.

• Centennial litigation: Re-entitlement could take longer than expected or result in a materially reduced project scope.

• Time horizon: Full value realization may require 10–20 years. Patient capital only.

• California regulatory risk: New environmental regulations, water allocation changes, or wildfire-related policy shifts could increase costs or reduce development potential.

• Water allocation variability: SWP allocations can drop dramatically in drought years, affecting farming and water lease income.

• Cyclical agriculture: Pistachio and almond crops are weather-dependent (the 2024 pistachio crop failed due to insufficient chill hours).

• No dividend: The company does not pay a dividend and reinvests internally. Shareholders bear opportunity cost.

• Interest rate sensitivity: Higher rates increase the discount rate on long-duration land assets and reduce residential housing demand.

• Concentrated geography: All assets are on one contiguous property in one state, creating single-point-of-failure risk (earthquake, wildfire, regulatory change).

XII. CONCLUSION

Tejon Ranch Co. is a deeply misunderstood, structurally mispriced asset. The market sees a small-cap company with ~$46 million in revenue, minimal earnings, and a long list of development projects that may take years to materialize. What it fails to price is the scarcity, irreplaceability, and embedded optionality of 270,000 acres at California’s most critical infrastructure chokepoint.

The normalized NAV analysis yields a range of $26–53 per share against a current price of ~$17.40. Even after applying aggressive time-value discounts, the stock appears meaningfully undervalued. The downside is protected by tangible, income-producing real assets (TRCC industrial at 100% occupancy, farming, mineral royalties, water). The upside is driven by multiple independent catalysts - any one of which (Centennial, data centers, Grapevine, energy) could re-rate the stock by 30–50%+ on its own.

The new management team under Matthew Walker represents the most significant governance inflection point in the company’s history. For the first time, Tejon has a CEO focused on transparency, capital discipline, and shareholder value creation - paired with a refreshed, independent board.

For investors with a 3–5 year horizon and tolerance for illiquidity and complexity, Tejon Ranch offers one of the most compelling risk/reward profiles in U.S. small-cap equities: a real asset portfolio trading near book value that owns what may be the most strategically located undeveloped land in California - with water, power, entitled homes, and an AI-era energy corridor as a free call option.