Seaport Entertainment Group (SEG) | Part 1: Hated Spin-Off with Hidden Value

60%+ NAV Discount | An Ugly Duckling Spin-Off with Golden Assets

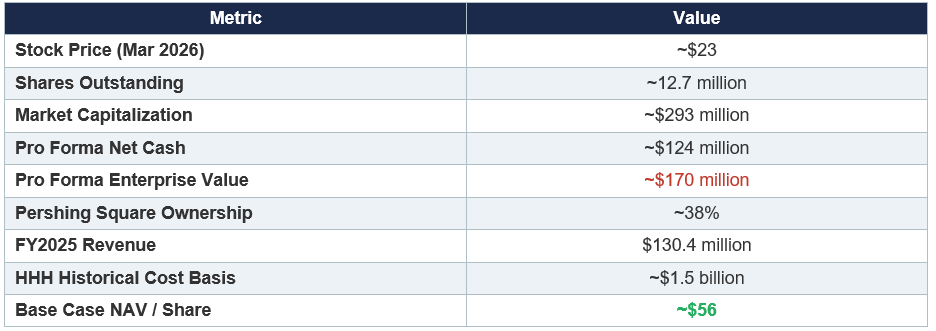

Seaport Entertainment Group (NYSE: SEG) is a collection of irreplaceable entertainment and real estate assets spun off from Howard Hughes Holdings in August 2024 and currently trading at a fraction of both historical cost basis and our estimated private market value. At a stock price of approximately $23 and a pro forma enterprise value of roughly $170 million, the market is implicitly assigning near-zero value to several high-quality assets, including an 80% interest in the air rights above the Fashion Show Mall on the Las Vegas Strip, a 25% ownership stake in Jean-Georges Restaurants, and the upside from over 220,000 square feet of recently executed leases and programming at the Seaport in Lower Manhattan.

Howard Hughes Holdings invested approximately $1.5 billion into these assets over the past decade. Pershing Square Capital Management, Bill Ackman’s fund, owns approximately 38% of SEG and backstopped the post-spin rights offering at $31.50 per share. Management is largely compensated in equity and has relocated to New York to operate the business full-time. The company has no meaningful debt maturities until 2038, carries roughly $124 million in pro forma net cash, and has authorized a $50 million buyback program. The setup is textbook deep-value: a misunderstood spinoff, orphaned by institutional holders, with a pathway to significant NAV realization through operational stabilization, lease-up, and selective asset monetization.

Key Metrics at a Glance

Company Overview and History

Genesis: The Howard Hughes Spinoff

Seaport Entertainment Group was created through a tax-free pro rata distribution from Howard Hughes Holdings (HHH) completed on August 1, 2024. For every nine shares of HHH common stock held, stockholders received one share of SEG. The separation was designed to unlock value by allowing HHH to operate as a pure-play real estate company focused on master planned communities, while SEG would independently pursue its entertainment and experiential real estate strategy.

The assets transferred to SEG represent the culmination of over a decade of investment by HHH totaling approximately $1.5 billion. This capital was deployed across the acquisition, renovation, and development of the South Street Seaport district in Lower Manhattan; the construction of the Las Vegas Ballpark; a 25% equity investment in Jean-Georges Restaurants; and the acquisition of an 80% interest in the air rights above the Fashion Show Mall on the Las Vegas Strip.

Business Segments

Landlord Operations: This segment holds and operates the physical real estate assets at the Seaport, including restaurant, retail, office, entertainment properties, and residential units. Rental revenue increased 21% year-over-year in FY2025, driven by private event activity, new lease executions, and termination income.

Hospitality: Encompasses the company’s food and beverage operations, including wholly owned restaurants, the Lawn Club joint venture, and the former Tin Building culinary experience (now being repositioned). In FY2025, management internalized F&B operations previously managed by third parties, improving cost control and flow-through.

Entertainment: Includes the Las Vegas Aviators Triple-A baseball team, Las Vegas Ballpark, the Rooftop at Pier 17 concert series, the Fashion Show Mall air rights, and various sponsorship agreements. Full-year entertainment segment adjusted EBITDA grew 124% in FY2025.

Asset Portfolio Summary

SEG’s portfolio can be categorized into five primary asset clusters, each with distinct risk/reward characteristics and valuation frameworks. At today’s enterprise value of approximately $170 million, one needs only a handful of these assets to justify the current price, leaving the remainder effectively valued at zero by the market.

Net Asset Value: Asset-by-Asset Analysis

The following analysis values each of SEG’s major assets independently using a combination of cap rate analysis, replacement cost, comparable transaction data, and discounted cash flow where appropriate. We then aggregate to a total gross asset value, subtract liabilities, and arrive at a per-share NAV. The critical insight is that the market is pricing the entire company at a level that can be justified by only one or two of its constituent assets, implying the rest are being carried at zero.

Asset 1: The Seaport District, Lower Manhattan

Physical Footprint and Composition

The Seaport encompasses over 478,000 square feet of entertainment, restaurant, retail, and office space in a historic waterfront neighborhood in Lower Manhattan, situated on the banks of the East River within walking distance of the Brooklyn Bridge. Key sub-assets include Pier 17, a 300,000+ square foot mixed-use structure housing the Rooftop concert venue, Meow Wolf’s forthcoming 75,000 square foot immersive experience, Flanker Kitchen + Sports Bar, event space, and various restaurants; the Tin Building, a landmark 53,000 square foot structure being repositioned as the U.S. flagship of Balloon Museum; and the Cobblestones district, home to a collection of restaurants, bars, and retail tenants spanning the pedestrian-only historic streets.

Leasing Momentum and Stabilized EBITDA Trajectory

Since becoming a standalone public company in August 2024, management has leased or programmed over 220,000 square feet, bringing occupancy to approximately 90% at year-end 2025. The remaining vacancy is approximately 53,000 square feet (pro forma for the Malibu Farm closure), predominantly comprising restaurant-oriented space and complementary daily-needs tenants. Management projects the 220,000+ square feet leased since the spin will generate over $30 million in stabilized annual EBITDA once tenants are operational.

The Tin Building repositioning represents the single most impactful economic event. By replacing a cash-burning culinary operation with a lease to Lux Entertainment (Balloon Museum), the company expects a pro forma annual EBITDA improvement of more than $22 million. This alone transforms the Tin Building from a drag on earnings to a positive cash-flowing asset with contractual rent escalations and percentage rent participation.

Cap Rate Valuation

To value the Seaport district, we employ a stabilized NOI / cap rate framework. Stabilized Seaport EBITDA will comprise contributions from landlord rental income (including Meow Wolf, Balloon Museum, Flanker, Gitano, and other tenants), hospitality segment operating earnings (internalized F&B, Lawn Club, Sadie’s), and entertainment segment earnings (concert series, events, sponsorships). We estimate total stabilized Seaport EBITDA in the range of $45 to $55 million, reflecting the $30 million from new leases, the $22 million Tin Building swing, and baseline contribution from existing operations, partially offset by remaining capex-related timing and vacancy.

Lower Manhattan waterfront entertainment real estate is genuinely scarce. There is no comparable mixed-use entertainment district with this combination of waterfront frontage, Brooklyn Bridge adjacency, a rooftop concert venue named best outdoor venue in America by Rolling Stone, and anchor tenants like Meow Wolf. Cap rates for prime Manhattan experiential retail and entertainment assets have historically traded between 4.5% and 6.5%. Our base case of 6.0% is conservative given the quality and irreplaceability of the location.

Asset 2: Las Vegas Ballpark and the Aviators

The Las Vegas Ballpark is a 10,000-capacity facility located in the Summerlin master planned community, completed in 2019 at a cost of approximately $150 million. It serves as home to the Las Vegas Aviators, the Triple-A affiliate of the Oakland Athletics. The facility also secured $80 million in naming rights revenue over a 20-year period, providing a significant embedded cash flow stream.

The Aviators won the 2025 Pacific Coast League Championship, the franchise’s first PCL title since 1988. Group and season ticket sales for 2026 are pacing ahead of prior year. Management has internalized day-to-day operations of the Enchant holiday activation, which occupied the ballpark during the winter off-season, positioning the company for improved execution and margin in 2026.

Minor league baseball franchise values have appreciated meaningfully in recent years, driven by MLB’s restructuring of the minor league system and the increasing value of live entertainment. Comparable Triple-A team transactions have ranged from $40 million to over $100 million, depending on market and facility quality. The Aviators benefit from operating in one of the fastest-growing metro areas in the United States, with a brand-new facility and strong community support.

CEO Partridge noted on the FY2025 earnings call that live sports is a business with tremendous value appreciation over time, and that management would expect a high premium for the team and ballpark given the quality of the facility and operation. We concur. The remaining pro forma debt on the ballpark loan is approximately $39 million, maturing in 2038.

Asset 3: Fashion Show Mall Air Rights (80% Interest)

This is perhaps the single most underappreciated asset in SEG’s portfolio and the key source of asymmetric upside. SEG owns an 80% interest in the air rights above the Fashion Show Mall, a 1.9 million square foot retail center on 34 acres of the Las Vegas Strip, directly across from the Wynn and Encore resorts. The remaining 20% is owned by Brookfield Properties, which owns the mall itself. These air rights were originally acquired by Howard Hughes in 2004.

The company’s own IR materials describe the potential to develop a casino and hotel on the Las Vegas Strip using these air rights. Given that the Las Vegas Strip spans only 4.2 miles and is virtually fully built out, the scarcity value of any developable parcel, let alone one with existing infrastructure, utility access, and a prime central Strip location, is extraordinary. For context, the Cosmopolitan of Las Vegas, situated on 8.7 acres of the Strip, sold for $5.65 billion in 2021. Resorts World Las Vegas, the most recent ground-up Strip casino development, cost approximately $4.3 billion to build.

We are not modeling a fully developed casino in our base case, as SEG does not currently have the capital, gaming license, or development plans to execute independently. However, the option value of these air rights is substantial. The asset could be monetized through a joint venture with a major gaming operator, a ground lease, an outright sale to a developer, or as contributed equity in a future development partnership. Even in a highly conservative bear case, the 80% interest in air rights above a prime Strip location is worth $100 million or more.

The range of outcomes for this asset is extremely wide, which is precisely why the market assigns it minimal value in the current stock price. For a patient, long-duration investor, this optionality is being acquired at an effectively zero cost basis within the current enterprise value.

Asset 4: Jean-Georges Restaurants (25% Stake)

SEG holds a 25% ownership interest in Jean-Georges Restaurants, the global restaurant group founded by celebrated chef Jean-Georges Vongerichten. The stake was acquired by Howard Hughes for $45 million. Jean-Georges operates a portfolio of restaurants spanning New York, Paris, Shanghai, Tokyo, Dubai, and other international markets, with licensing and management agreements that generate recurring fee income. The brand carries significant cachet and generates steady licensing revenue with minimal capital requirements.

Following the corporate restructuring completed in 2025, SEG converted the Tin Building joint venture and various management agreements into new license agreements with Jean-Georges, simplifying the relationship while preserving the ongoing partnership at the Seaport. The 25% stake continues to provide SEG with equity participation in the broader Jean-Georges enterprise. We value this stake at $50 to $70 million in our base case, representing a modest premium to acquisition cost reflecting organic growth and brand appreciation.

Asset 5: 85 South Street Residential (21 Units)

SEG owns a 21-unit apartment building at 85 South Street in the Seaport district. The building is nearly 100% occupied and cash flowing, with a mix of market-rate and rent-stabilized units. Management has initiated a marketing process for the potential sale of this asset. Lower Manhattan residential values have appreciated significantly, and a waterfront-adjacent multifamily building in this neighborhood would likely attract strong buyer interest. We estimate a disposition value in the range of $20 to $30 million.

What Gets You to the Current Enterprise Value?

At an enterprise value of approximately $170 million, the market is essentially paying only for a partially stabilized Seaport district at a very high implied cap rate (roughly 10%+ on even conservative near-term NOI estimates) and assigning zero to the Las Vegas Ballpark, zero to Jean-Georges, zero to the Fashion Show Mall air rights, and zero to the residential building. Said differently, if the Seaport alone stabilizes at $30 to $50 million in EBITDA, the rest of the portfolio is free. This is the fundamental mispricing.

Management and Governance

Leadership Team

Matt Partridge, CEO: Partridge joined SEG in 2024 as CFO before being elevated to President and CEO in Q3 2025. This is his fifth public company role, and he brings direct experience in capital allocation, real estate operations, and public company governance. Importantly, Partridge relocated his family to New York City to run the business and is compensated primarily in equity. His communication on earnings calls is refreshingly direct, operationally focused, and devoid of promotional excess.

Lenah Elaiwat, CFO: Appointed CFO effective December 2025 after serving as Interim CFO and Chief Accounting Officer. Elaiwat brings nearly 20 years of financial leadership in real estate and financial services. Her focus on cost discipline was evident in the 32% reduction in G&A expenses achieved in FY2025.

Anton Nikodemus (Former CEO): Nikodemus, who led SEG through its initial spinoff, is a gaming and hospitality industry veteran who previously oversaw the Cosmopolitan, Aria, Bellagio, and Park MGM for MGM Resorts International. His background was instrumental in the original strategic vision, particularly the Fashion Show Mall casino opportunity. Partridge’s elevation suggests a pivot toward operational execution and financial discipline in the current phase.

Incentive Alignment

Alignment of interest is strong. Management is largely compensated in equity, creating direct incentive to close the NAV gap. Pershing Square Capital Management, led by Bill Ackman, owns approximately 38% of SEG and backstopped the post-spin rights offering at $31.50 per share, well above the current trading price. Ackman served as Chairman of Howard Hughes Holdings for 13 years, including when the SEG spinoff was conceived and announced. Pershing’s cost basis and sustained involvement signal deep conviction in the long-term value of these assets.

The Board has authorized a $50 million stock repurchase program, providing a mechanism to return capital and support the stock price, though management has indicated they will be opportunistic rather than formulaic in execution. A $150 million shelf registration provides additional flexibility for strategic capital deployment. Both tools are appropriate given the company’s excess liquidity and the significant discount to NAV.

Operational Execution Track Record

In its first full year as a standalone entity, management delivered a 24% improvement in net loss, a 49% improvement in non-GAAP adjusted net loss, a 32% reduction in G&A expense, the execution of over 220,000 square feet of leases and programming, the internalization of food and beverage operations, the completion of the $143 million sale of 250 Water Street (generating $76 million in net proceeds), and the strategic repositioning of the Tin Building from a negative-EBITDA culinary experiment to a positive cash-flowing lease with Balloon Museum. These are not incremental improvements. They represent a fundamental restructuring of the company’s operating model executed within 18 months of the spinoff.

Scarcity vs. Land: Are These Truly Irreplaceable?

A critical question for any real asset thesis is whether the assets in question are genuinely scarce and irreplaceable, or whether they simply represent land that could be replicated elsewhere. In SEG’s case, several of the key assets possess characteristics that make them uniquely difficult, if not impossible, to replicate.

The Seaport: Location and Character Cannot Be Manufactured

The Seaport occupies a historic waterfront neighborhood at the southeastern tip of Manhattan, directly beneath the Brooklyn Bridge, with panoramic views of the East River and the Brooklyn skyline. This location benefits from centuries of accumulated cultural significance, landmark preservation, and urban context that no new development can duplicate. The district combines historic architecture, pedestrian-only cobblestone streets, and waterfront access in a way that creates an authentic sense of place, something that planned entertainment districts (like Hudson Yards, for example) struggle to achieve despite far greater capital investment.

The Rooftop at Pier 17 was named Best Outdoor Music Venue in the United States by the Rolling Stone Audio Awards in 2026. When Meow Wolf’s 75,000 square foot immersive experience opens as the company’s first East Coast location, the Seaport will offer a combination of live concerts, immersive art, fine dining, waterfront recreation, and cultural programming that exists nowhere else in New York City. These are not simply tenants occupying generic commercial space. They are destination anchors whose presence generates cross-traffic, extends dwell time, and creates a compounding network effect for the entire district.

Fashion Show Mall Air Rights: You Cannot Create New Strip Frontage

The Las Vegas Strip, at approximately 4.2 miles in length, is one of the most constrained development corridors in global entertainment. Virtually every developable parcel has been built on, and new entrants have been forced into increasingly creative (and expensive) solutions, whether demolishing existing properties like the Tropicana to build the new A’s stadium, or constructing vertically above existing structures. There are no greenfield Strip sites remaining. An 80% interest in air rights above a 34-acre parcel at the center of the Strip, directly across from Wynn/Encore, represents one of the last meaningful development options on the most economically productive stretch of entertainment real estate on Earth. This is not land. This is a development option on irreplaceable infrastructure.

Las Vegas Ballpark: Purpose-Built, Market-Anchored

While a stadium itself is a depreciating physical asset, the Ballpark’s value derives from its position within the Summerlin master planned community, the ongoing growth of the Las Vegas metro area, the Aviators’ affiliation with the Athletics (who are building a new MLB stadium nearby), and the facility’s capacity for non-baseball entertainment programming like Enchant and Savannah Bananas events. The combination of a modern, purpose-built venue with a growing local market and diversified event calendar creates an asset with appreciating franchise value layered on top of the physical structure.

Re-Rating Catalysts and Asymmetric Upside

What the Market Is Missing

1. Orphaned Spinoff Dynamics: SEG was distributed to Howard Hughes Holdings shareholders, many of whom are large-cap REIT investors with no mandate to hold a micro-cap entertainment and hospitality company. The forced selling and index exclusion that accompanied the spinoff created an artificial supply/demand imbalance that depressed the stock below intrinsic value. The subsequent uplisting to the NYSE in June 2025 and inclusion in the Russell 2000 and Russell Microcap indices were initial steps toward correcting this, but the float remains limited (Pershing Square holds 38%, and insiders hold additional shares), which constrains institutional participation.

2. Earnings Trajectory Inflection: The company is in the early innings of a transition from a money-losing, pre-stabilized asset collection to a cash-generating, leased-up entertainment platform. The inflection is already visible: FY2025 non-GAAP adjusted net loss improved 49% year-over-year, and the combined effect of the Tin Building repositioning (+$22M EBITDA), new leases ($30M+ stabilized EBITDA), and continuing G&A reductions will drive materially improved reported financial results in 2026 and 2027. As reported losses shrink and EBITDA turns positive, the stock should attract fundamental investors who have avoided it due to current negative earnings.

3. Fashion Show Mall Monetization: Any announcement of a joint venture, ground lease, or development partnership for the Fashion Show Mall air rights would represent a step-function value creation event. Given that management has hired a former MGM Resorts executive and has explicitly described the asset as a potential casino/hotel site on their IR website, the question is when, not whether, some form of monetization is pursued. Even a modest announcement of a feasibility study or partnership discussion could serve as a powerful catalyst for re-rating.

4. Buyback Execution: With $50 million authorized for repurchases against a market cap of roughly $293 million, management has the capacity to retire approximately 17% of the outstanding float if they choose to execute aggressively. In a stock with limited float and significant insider ownership, even modest buyback activity could meaningfully support the stock price while creating accretive value for remaining shareholders.

5. Meow Wolf and Balloon Museum Opening: The openings of Meow Wolf (first East Coast location) and Balloon Museum (U.S. flagship) at the Seaport in 2026 will generate significant media attention and foot traffic. Meow Wolf’s existing locations attract millions of visitors annually. The resulting increase in visitation, cross-selling to restaurants and bars, and overall neighborhood vibrancy should directly translate to improved financial performance across all Seaport segments.

6. 2026 Macro Tailwinds: The 2026 FIFA World Cup in New York City and the America 250 celebrations provide unique macro tailwinds for the Seaport, which is positioning itself as a key event and gathering destination for these nationally significant occasions. Manhattan tourism volumes, corporate event spending, and general foot traffic in Lower Manhattan should benefit from these extraordinary one-time catalysts.

Sources of Asymmetric Upside

The asymmetry in this investment stems from the combination of downside protection (net cash balance sheet, irreplaceable real assets carried below cost, $50M buyback authorization) and multiple upside pathways (operational stabilization, Fashion Show Mall monetization, potential accretive acquisitions, live sports value appreciation, and strategic alternatives for the broader company). The downside from current levels is limited by the asset base and cash position, while the upside is amplified by the wide range of potential outcomes for the Fashion Show Mall air rights and the nonlinear impact of operational stabilization on a currently loss-making company.

Put simply, the market is pricing SEG as though none of the management’s operational improvements will stick, none of the newly signed leases will perform, and none of the undeveloped assets will ever be monetized. That is the bet you are taking on the short side. On the long side, you are paying $170 million of enterprise value for assets that cost $1.5 billion to assemble, and you are getting a management team and a strategic investor that are aligned, competent, and actively executing.

What Does This Company Look Like in the Future?

2027-2028: Stabilized Operations

By late 2027, the Seaport should be effectively fully leased and stabilized. Meow Wolf, Balloon Museum, Flanker, Sadie’s, the expanded event space, and the concert series will all be operational and contributing. We estimate stabilized Seaport EBITDA in the range of $45 to $60 million, with the Las Vegas operations contributing an additional $10 to $15 million. Total company EBITDA, after corporate overhead of roughly $25 to $28 million annually, could reach $30 to $47 million. At even a modest 12x to 15x EV/EBITDA multiple, the implied enterprise value would be $360 to $705 million, representing 110% to 315% upside from the current level.

2028-2030: Fashion Show Mall Monetization

The most transformative potential event for SEG is the monetization of the Fashion Show Mall air rights. Whether through a JV, ground lease, or outright sale, the realization of value from this asset could be a multiple of the entire current enterprise value. If SEG enters into a development partnership with a major gaming operator, the company’s 80% interest in the air rights could serve as a contributed equity interest in a multi-billion-dollar casino development, potentially yielding hundreds of millions of dollars in value creation.

Long-Term Platform Vision

On the FY2025 earnings call, CEO Partridge articulated a vision for SEG as a scalable real estate-centric hospitality and entertainment platform, potentially expanding through acquisitions of companies with scalable intellectual property and brand recognition. The $150 million shelf registration and strong balance sheet position the company to pursue accretive opportunities. If management executes on this vision, SEG could evolve from a single-district operator into a multi-property entertainment platform, a transformation that would command a materially higher valuation multiple.

Key Risks

Execution Risk: The transition from pre-stabilized to stabilized operations requires successful tenant buildout, construction completion, and ramp-up of new concepts. Delays, cost overruns, or tenant underperformance could extend the timeline to profitability. The remaining $70 to $90 million in capex to reach stabilization represents a meaningful commitment relative to the company’s cash position.

Concentration Risk: The company’s revenue is heavily concentrated in two geographic nodes: Lower Manhattan and Las Vegas. Macroeconomic weakness, a decline in tourism, or adverse local market conditions in either city could disproportionately impact results.

Fashion Show Mall Uncertainty: There is no guarantee that the air rights will ever be developed or monetized. Regulatory hurdles (FAA, Clark County, gaming license requirements), capital intensity, and the need for third-party partnerships introduce significant uncertainty around both timing and magnitude of value realization.

Limited Float and Liquidity: With approximately 12.7 million shares outstanding and 38% held by Pershing Square, the public float is thin. This creates volatility risk and may deter institutional investors who require minimum liquidity thresholds.

Continued Net Losses: While improving, the company remains in a net loss position. Extended periods of negative earnings could pressure the stock price and limit management’s flexibility, particularly if the macro environment deteriorates.

G&A Burden: Public company costs for a micro-cap entity are proportionally heavy. While G&A has been reduced meaningfully, the annual run rate of approximately $27 million represents a significant fixed cost that must be covered by operating earnings.

Conclusion

Seaport Entertainment Group represents one of the more compelling deep-value opportunities in today’s market. The combination of irreplaceable physical assets, a credible operational improvement trajectory, strong insider alignment, a clean balance sheet, and an embedded call option on one of the most valuable undeveloped parcels on the Las Vegas Strip creates a risk/reward profile that is difficult to find in public equities.

The market is treating SEG as a broken spinoff burning cash, when in reality it is a rapidly improving entertainment platform that is 18 months into a multi-year transformation. Howard Hughes spent $1.5 billion assembling these assets. Pershing Square bought in at $31.50 per share. Management is compensated in stock and executing against a clear playbook. The Seaport is 90% leased. The Tin Building repositioning is worth $22 million in annual EBITDA. And the Fashion Show Mall air rights remain a zero-cost call option on one of the most constrained real estate markets in the world.