Pure Cycle (PCYO): The Market Is Paying You to Take the Water

The market values one of the West's largest private water rights portfolios at less than zero

In our recent Water Thesis (Water Rights: The Hidden Asset the Market Still Values at Zero), we flagged Pure Cycle Corporation (NASDAQ: PCYO) as one of the more compelling ways to own scarce western water rights at a substantial discount to their underlying value. That piece laid out the structural case: a company sitting on one of the largest private water portfolios on the Colorado Front Range that the market was effectively valuing at zero. The backdrop is a widening imbalance - Colorado River supply is shrinking just as data center demand emerges as a powerful new draw on western water.

This is the first in what will be a periodic series of updates to our active coverage names. We revisit these names as new disclosures, earnings, and news come out - and especially when the share price moves to a level we find compelling. With PCYO now trading below $10, this felt like the right moment to re-underwrite the thesis, which still points to a base-case NAV nearly 3x the current price.

Pure Cycle is, at its core, a bet that whoever owns the water wins. The company figured that out early. It started life in the 1980s building behind-the-house water-recycling units - until a young finance consultant named Mark Harding told them the gadget was beside the point: “the most valuable component is not what you’re making, it’s the resource itself.”

His advice was blunt - go long on water, buy all you can - and the logic was simply macroeconomics: fixed supply, relentless demand, a resource you literally cannot manufacture. So that’s what they did, acquiring the Lowry Range supply around 1988 when the market scoffed that they wouldn’t need it for 25 years. They were right about the timing and right about the water.

Three decades later, that early-and-cheap water portfolio is the engine: Pure Cycle monetizes it one tap at a time as the Denver metro builds out around it, capturing the land and the water value at its Sky Ranch development while selling surplus to oil & gas - and it still trades for less than the water alone is worth.

PURPOSE: WHY THE UPDATE

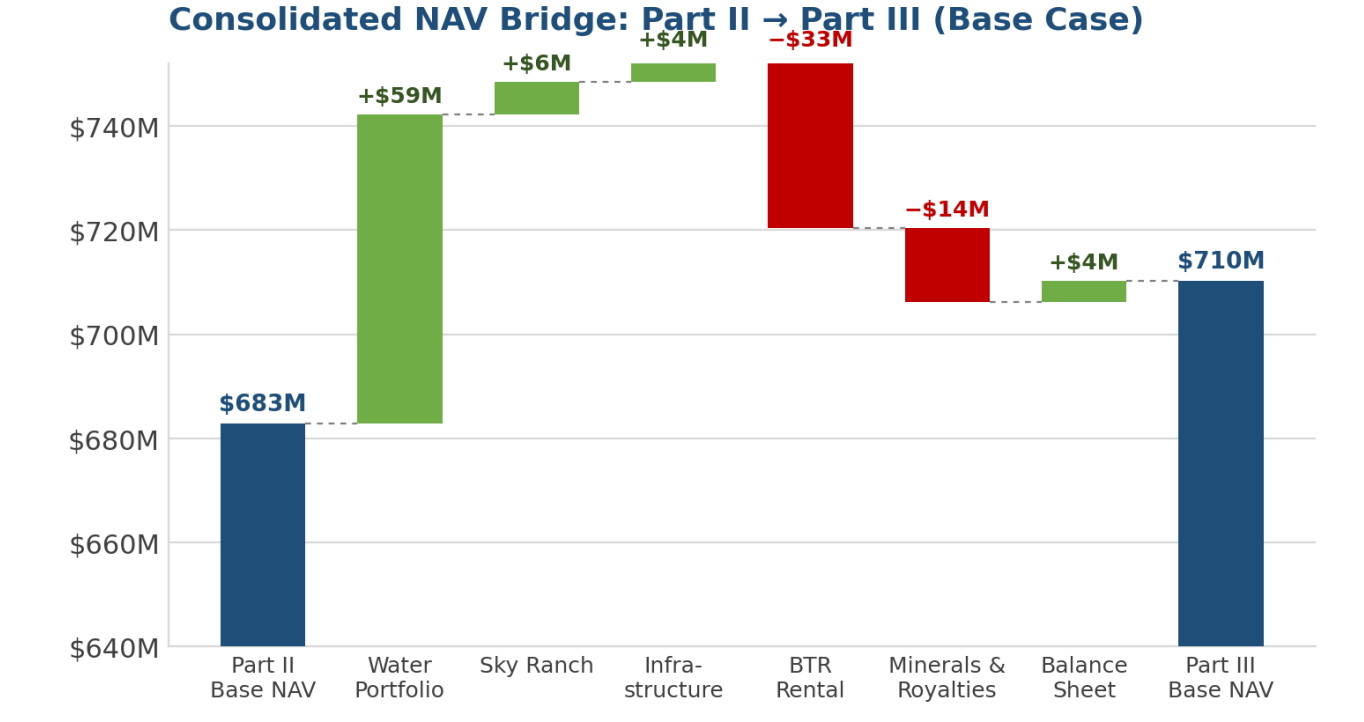

Part I and Part II of this thesis built the case for Pure Cycle Corporation as a structurally mispriced water and land franchise, and translated that case into a granular, asset-by-asset net asset value. Both have been published. This third installment is not a reiteration of the framework - it is a re-underwriting.. The purpose here is to mark the model to the newest disclosures, flag where the facts have moved in our favor and where they have moved against us, and arrive at a revised NAV that an honest analyst would defend today.

The headline: the intrinsic-value gap has not closed - if anything it has widened on an absolute basis - but the composition of that value has shifted. The water portfolio is roughly 10% larger than when we last wrote. The public-improvement receivable has grown by more than $11 million and now sits above $56 million. Land development is running six months ahead of schedule. Against those positives, the oil & gas royalty stream has reset sharply lower, the build-to-rent (BTR) segment has been deliberately scaled back, and the I-70 interchange has slipped a year. We incorporate all of it below.

ASSET 1: WATER RIGHTS PORTFOLIO

GAAP carrying value: ~$71.3M (Investment in water and wastewater systems, net - combined water rights + infrastructure line); up from ~$67.5M at FY2025 year-end.

1A. What Changed: A Bigger Portfolio

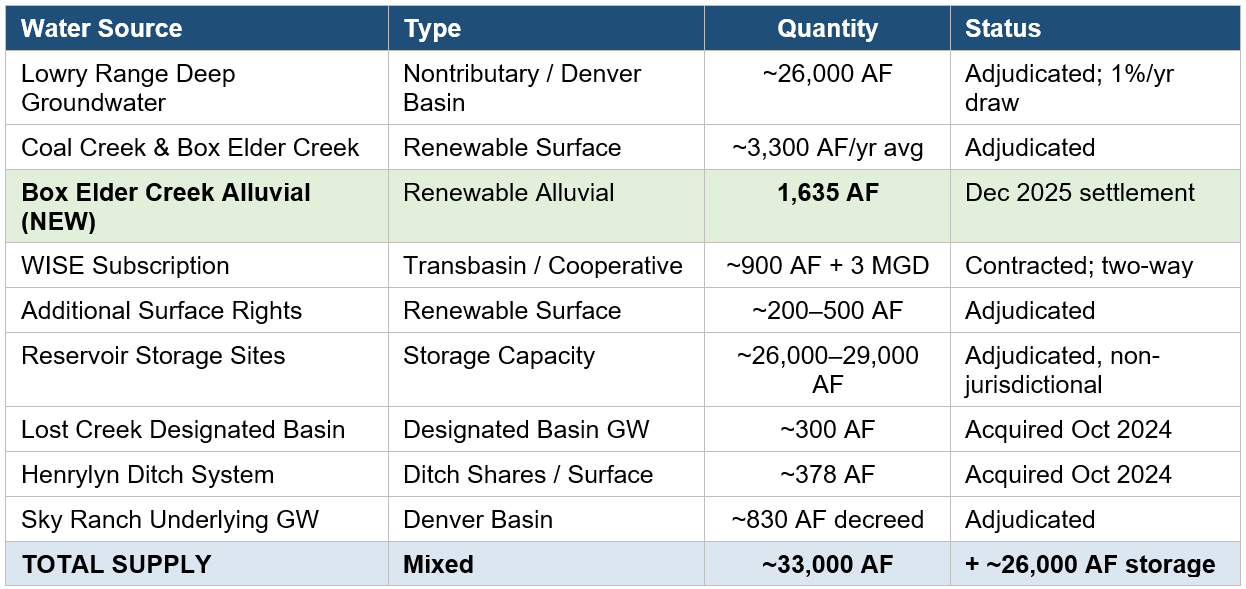

The most important water development since the prior thesis is concrete and adjudicated, not speculative. In a December 2025 Water Court settlement, Pure Cycle added 1,635 acre-feet of adjudicated water from the Box Elder Creek Alluvial aquifer to its portfolio. On the Q2 call, management confirmed the portfolio has grown roughly 10% and now stands at approximately 33,000 acre-feet (versus the ~29,500–30,000 AF we modeled previously), with the stated ability to serve more than 60,000 connections at full buildout. Management also reiterated its ~900 AF WISE (Water Infrastructure and Supply Efficiency) subscription and 3 MGD of associated pipeline capacity, which functions as a two-way spot market: Pure Cycle pulls extra water in winter (oil & gas demand) and sells surplus to other WISE participants in summer.

Why the alluvial add matters disproportionately: Box Elder Creek alluvial water is renewable, locally sourced surface-connected supply - the most valuable category on a per-AF basis - and it is intended to consolidate with the existing Box Elder Creek and Weld County supplies into an integrated system. This is not remote agricultural water bought for optionality; it is supply adjacent to the demand center with infrastructure proximity.

1B. Updated Inventory

Management states this portfolio is sufficient to serve approximately 60,000 single-family equivalents at full buildout. On the Q2 call, the CEO reframed the total monetization opportunity: at ~$40,000 of connection charge across 60,000 connections, the gross tap-fee opportunity is roughly $2.5–3.0 billion - a long-tailed figure, but one that frames the scale of the resource against a ~$243M market cap.

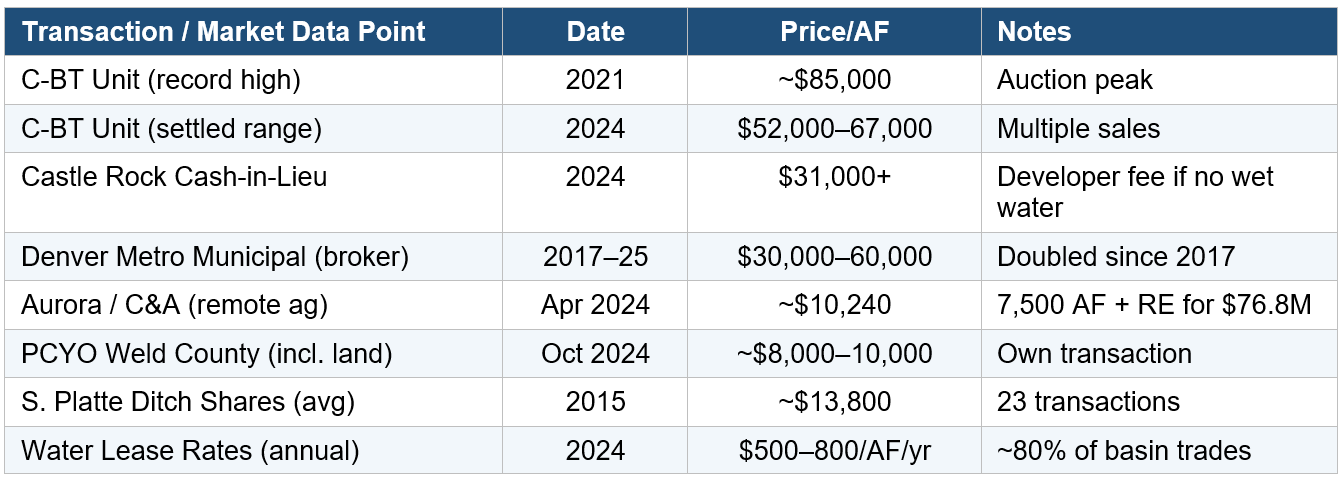

1C. Comparable Transaction Evidence (Refreshed)

The Colorado Front Range remains the best-documented wholesale water market in the western U.S. The comparable set has not materially loosened; if anything, scarcity pricing has held. Key reference points:

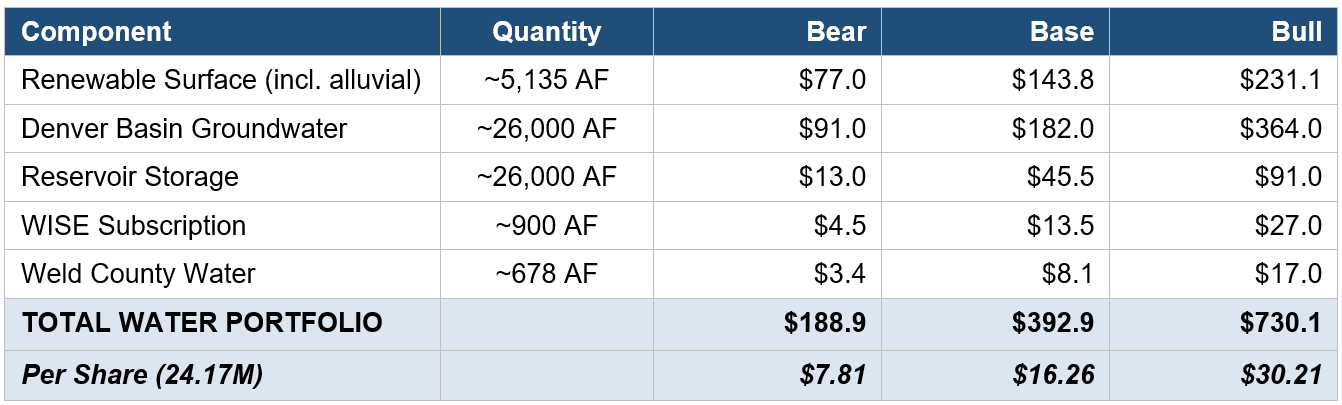

1D. Revised Water Portfolio NAV

We retain the prior per-AF valuation discipline but flow the larger portfolio through it. The renewable surface bucket now includes the 1,635 AF alluvial add and is sized at ~5,135 AF; groundwater is unchanged at ~26,000 AF; storage and Weld County water are unchanged. We also now carry the WISE subscription explicitly at a modest value reflecting its contracted, two-way nature.

Surface-water $/AF applied: Bear $15,000 / Base $28,000 / Bull $45,000. Groundwater: $3,500 / $7,000 / $14,000. Storage: $500 / $1,750 / $3,500. WISE: $5,000 / $15,000 / $30,000. The portfolio grew ~$29M (Base) versus the prior $333.6M, driven by the alluvial add and explicit WISE recognition. The implied-market-value insight is unchanged and starker: strip out all non-water assets at conservative values and the residual price the market assigns to ~33,000 AF of supply plus ~26,000 AF of storage remains a small fraction of Front Range clearing prices.

ASSET 2: SKY RANCH LAND DEVELOPMENT

Book value (land under development + held for development): ~$5.5M current + ~$5.0M held for development.

2A. What Changed: Density Up, Schedule Pulled Forward, More Builders

• Phase 2 lot count expanded materially. Management disclosed Phase 2 started at ~780 homes but, through product diversification (duplexes, townhomes, varied lot widths), has grown to a little over 1,030 lots. Higher density means more lots to sell, more taps, and - critically - higher assessed value, which expands the CAB’s bonding capacity to reimburse Pure Cycle.

• Builder roster nearly doubled. From 4 national builders at the start of Phase 2 to 7 today (Lennar, D.R. Horton, KB, Taylor Morrison, Challenger, Pulte, Oakwood). The three new entrants are anchored in Phase 2D, smoothing the transition into Phase 2E and reducing air-pocket risk between phases.

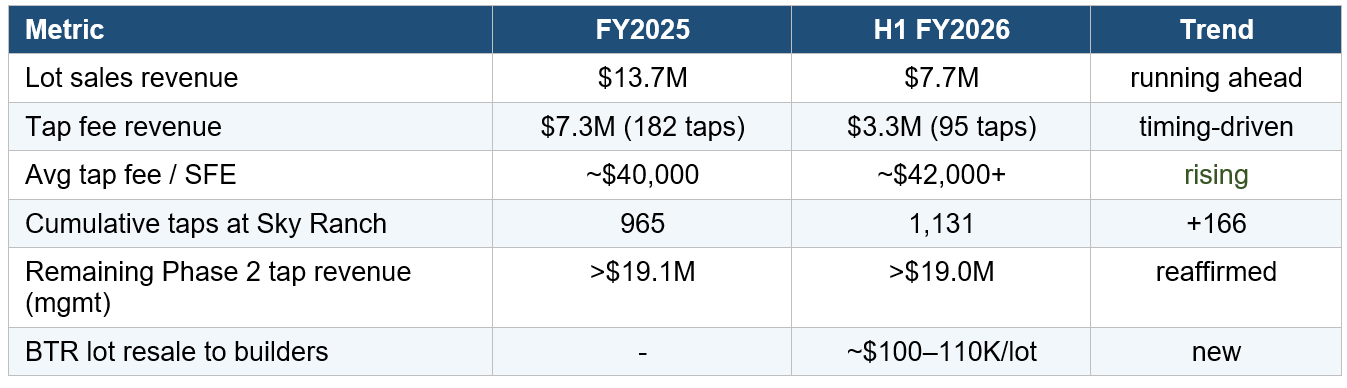

• Six months ahead of schedule. A mild winter let Pure Cycle complete Phase 2D to ~78% and Phase 2C to ~91%, delivering ~70% of Phase 2D lots by the end of Q2. This pulled revenue forward - H1 land-development revenue more than doubled to $8.6M - but management is explicit that the annual cadence will normalize.

• 1,131 taps sold cumulatively at Sky Ranch through Phase 2D (up from 1,016 in the prior thesis). Management reaffirms >$19.0M of remaining Phase 2 tap-fee revenue over the next three years.

• Phase 2E (159 lots) grading has mobilized; delivery targeted for summer 2027. Management quantified it on the call at ~$14M of lot revenue, ~$4.3M of tap fees, and ~$240K of recurring revenue.

• K-12 campus opening Fall 2026. The on-site charter high school (with National Heritage Academies) is ahead of schedule and is repeatedly cited as the top driver of buyer relocation demand - a non-trivial amenity tailwind for lot absorption.

2B. Updated Lot & Tap Economics

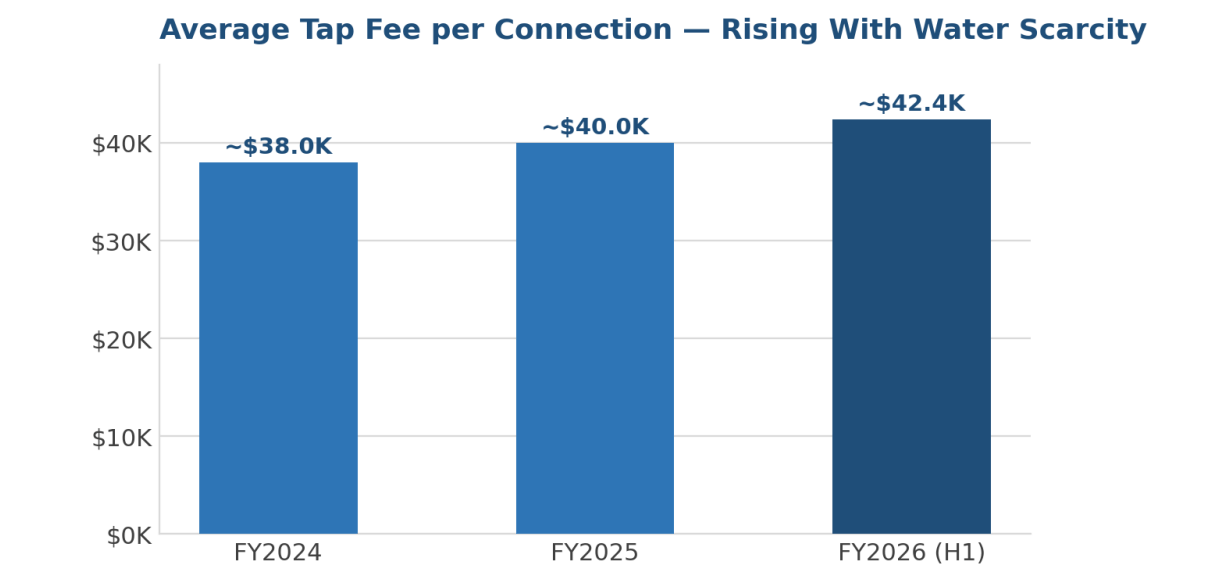

Tap-fee escalation intact: average tap fees continue to rise (~$38K in FY2024 → ~$40K FY2025 → ~$42K+ in FY2026), confirming the secular thesis that tap fees track Front Range water scarcity rather than housing cyclicality. This is the mechanism by which the water portfolio is monetized - slowly, contractually, and at escalating prices.

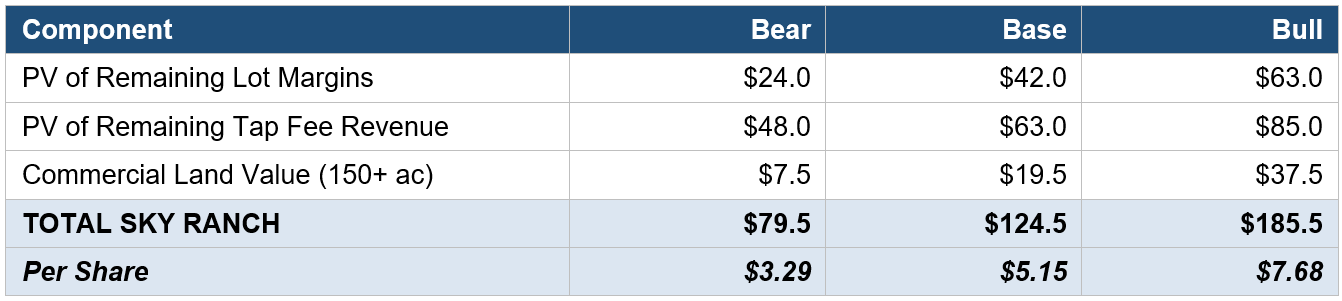

2C. Revised Sky Ranch NAV

We update remaining lot count for the higher Phase 2 density (~1,030 lots in Phase 2 vs ~780 originally) while holding future-phase assumptions broadly constant. Net lot margins and tap-fee present values are refreshed for the larger pipeline and the higher realized tap price.

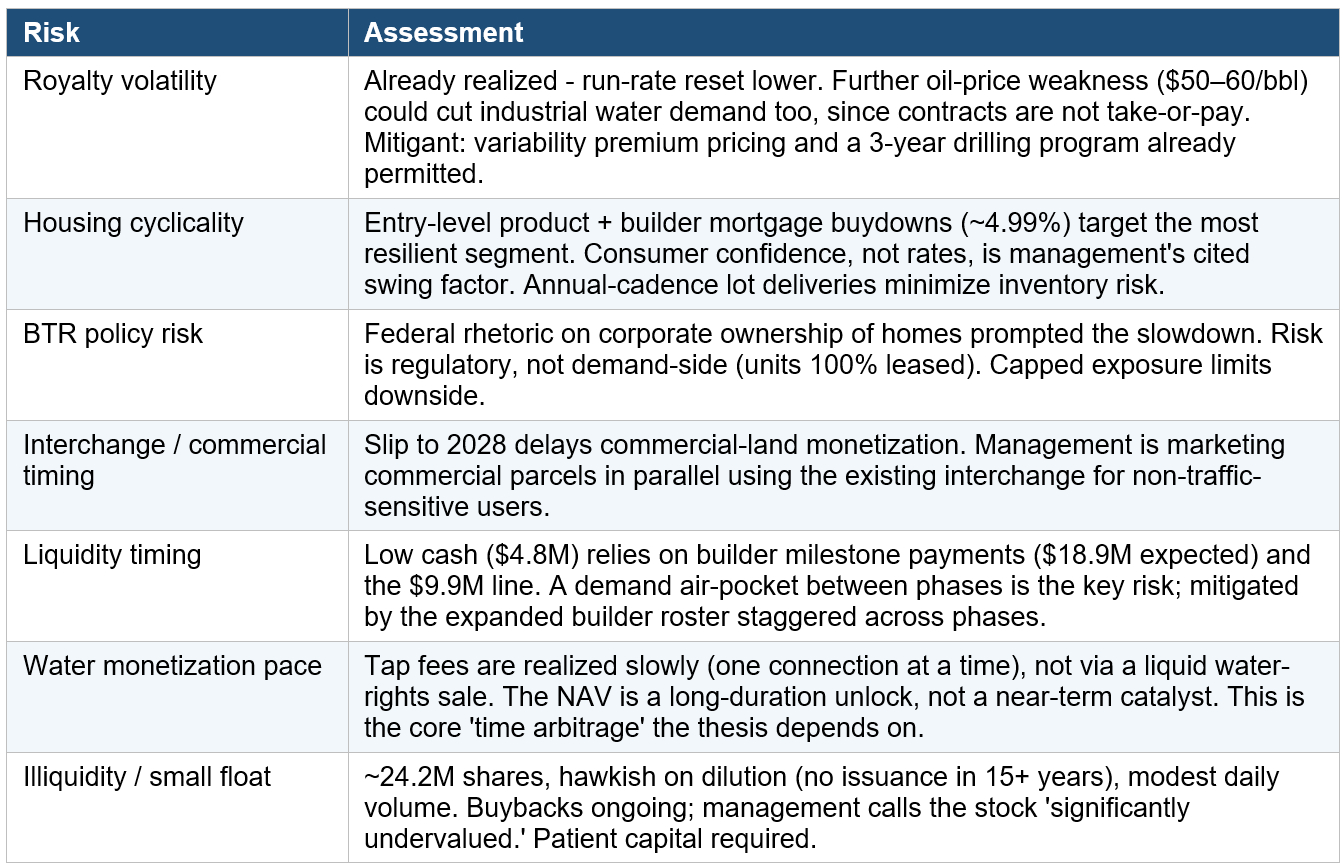

Commercial land - a watch item: management is now actively marketing the 150+ acres of I-70 frontage (retail and industrial brokers engaged) even ahead of the new interchange, targeting distribution centers, bottling/water-intensive users, and other commercial uses. The interchange completion has slipped to 2028 (from late 2027), and the data-center angle has cooled - Colorado has competing legislative bills on data-center tax incentives and faces gas-turbine power constraints, making it less attractive than peer states. We hold commercial land flat rather than marking it up; the marketing is encouraging but unproven, and the interchange slip is a real, if minor, headwind to the timing of value realization.

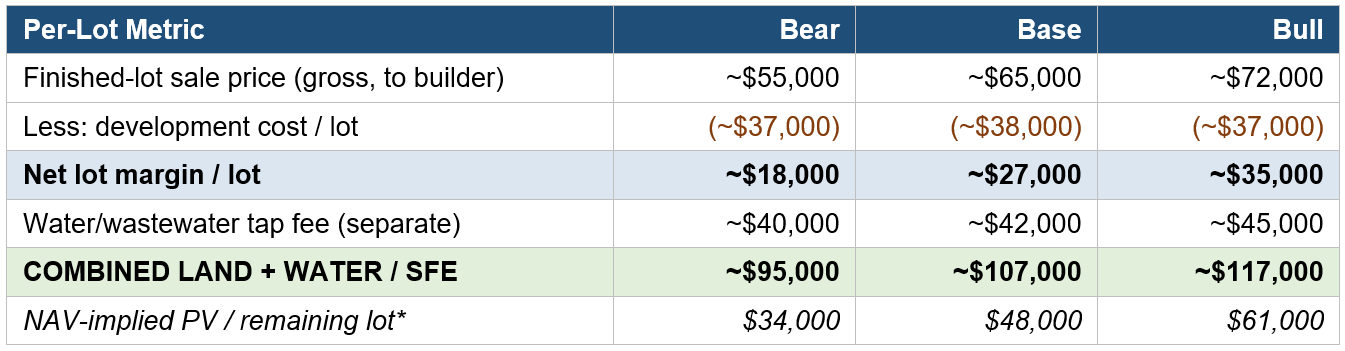

2D. Implied Finished-Lot Pricing Embedded in the NAV

Because the Sky Ranch NAV is built from a remaining-lot count and a per-lot margin, it is worth surfacing what the model implies on a per-lot basis - both to sanity-check the NAV against the market and to make the assumptions auditable. There are two distinct prices at Sky Ranch that must be kept separate: (1) the finished-lot sale price the homebuilder pays for the developed lot, and (2) the water/wastewater tap fee, billed separately when the building permit is pulled. Pure Cycle captures both. The combined figure is the true measure of land-and-water value monetized per home.

*PV-per-lot = (PV of remaining lot margins + PV of remaining tap-fee revenue) ÷ ~2,200 remaining residential lots (Base), i.e. the discounted value the NAV assigns to each unbuilt lot today. The combined-monetization row is undiscounted, gross-of-time realized value per home.

The validation that matters: the ~$107,000 combined land-plus-water figure (Base) is not a modeling artifact - it is corroborated directly by management. On the Q2 call, management stated it is reselling ~30 reserved BTR lots back to homebuilders at $100,000–110,000 per lot. That is the market clearing price for a Sky Ranch finished lot inclusive of its water entitlement, disclosed by the company itself, and it brackets our Base assumption almost exactly. The reported lot-sales line (~$60–70K/lot gross) understates total per-home value precisely because the tap fee is recognized in a different segment; combining them is what reveals the true ~$100K+ capture per door.

Why this de-risks the NAV: our Base NAV discounts each remaining lot to a present value of ~$48,000, against a combined realized monetization of ~$107,000 per lot delivered over time. In other words, the NAV is not capitalizing tomorrow’s prices - it is applying a substantial time-and-execution discount to a per-lot value the company is demonstrably achieving today. The Bull case ($117K combined) simply assumes continued tap-fee escalation and modest lot-price firming, both already in evidence.

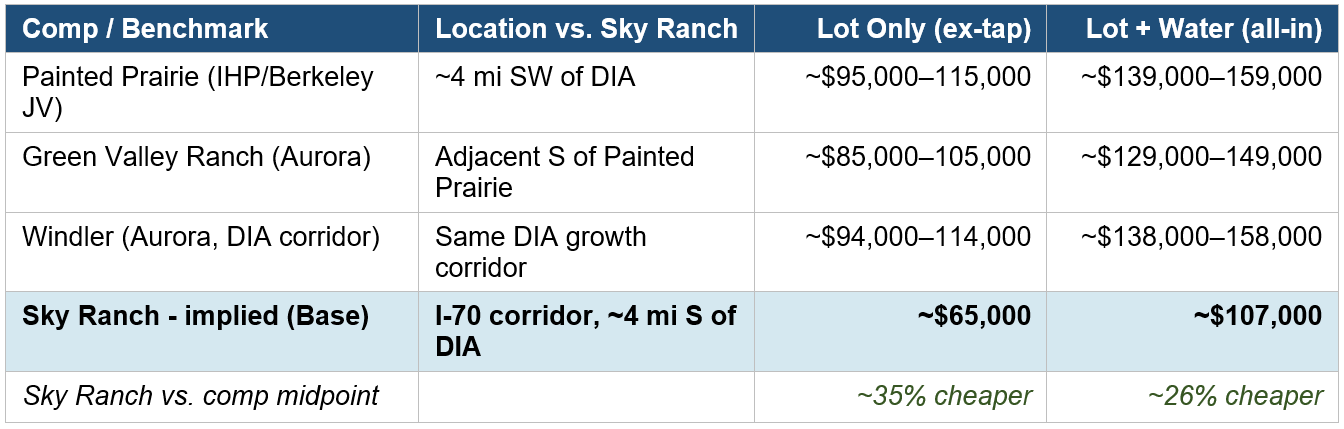

2E. Comparable Finished-Lot Transactions - East Denver / I-70 Corridor

To anchor the implied pricing against the open market, we assemble finished-lot comps from Sky Ranch’s direct submarket - the I-70 / Denver International Airport growth corridor (Aurora, Green Valley Ranch, Painted Prairie, Windler) - where the product (entry-level, alley-loaded, 34–45-foot lots) is closely comparable.

The apples-to-apples point, made explicit: in every one of these master plans - Sky Ranch included - the water/wastewater tap fee (or “system development charge”) is a SEPARATE charge the builder pays to a metro district or municipal water provider when the building permit is pulled. It is not embedded in the finished-lot price. A finished lot in Painted Prairie that trades at ~$100K still carries an Aurora Water connection fee on top of that ~$100K. To avoid the error of comparing Sky Ranch’s lot-plus-tap figure against a comp’s lot-only figure, the table below presents BOTH bases side by side, with each market’s actual, separately-billed tap/SDC verified from the current published fee schedule.

Verified Tap / System Development Charges (separate from lot price)

*Aurora figure is the city’s own published worked example: 3-bathroom single-family detached, 8,000 sq ft lot, 5/8” meter (water service connection $31,551 + Aurora sanitary sewer $6,411 + Metro Wastewater $6,070 + stormwater $424). The near-identical ~$42K–44K tap at both Sky Ranch and the comps is itself the proof that the two markets must be compared on a consistent basis.

Comp Set on Both Bases

Supplemental benchmarks (national, for context, lot-only basis): NAHB 2024 survey finished-lot share of 13.7–17.8% of sales price (≈ $73,000–94,000 on a $530K home); D.R. Horton FY25 lot costs at 26–27% of total cost and rising ~10% YoY; Lokal Homes / Builder Capital land-bank takedowns of attainable-price Denver infill lots; and a Castle Rock fee load exceeding $90,000 per new start - all consistent with the corridor figures above.

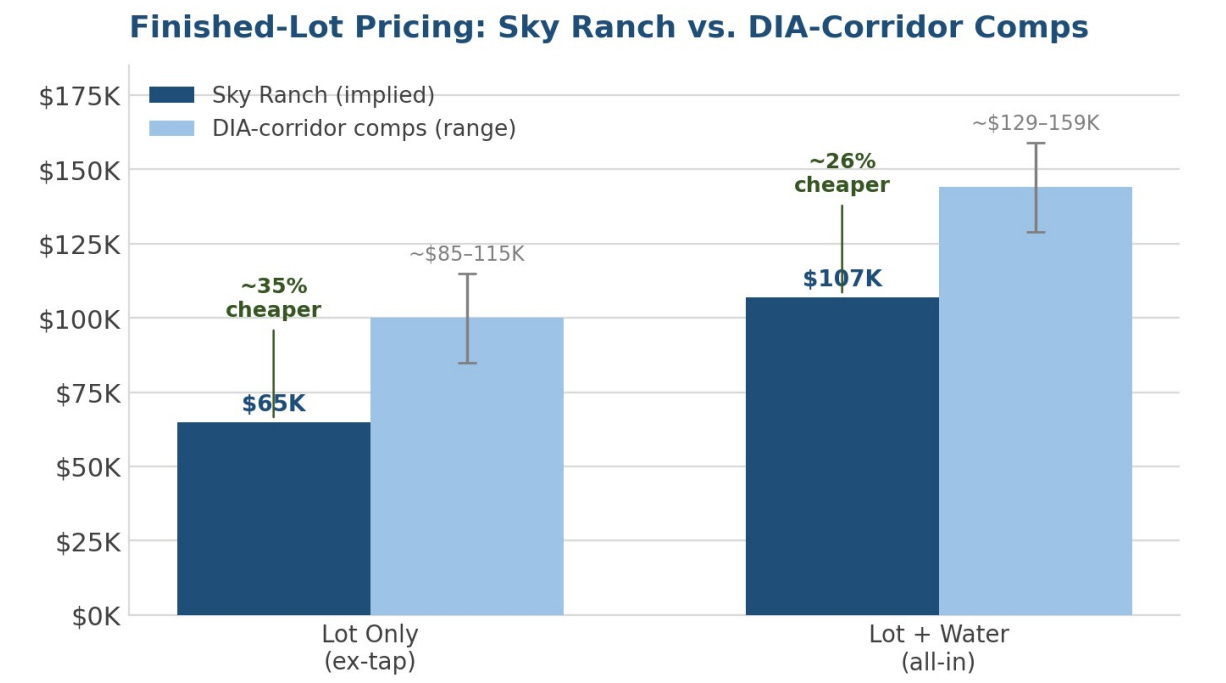

Reading the corrected comp set: on a like-for-like LOT-ONLY basis, Sky Ranch’s ~$65,000 finished lot is roughly 35% below the ~$85,000–115,000 cleared in the directly comparable DIA-corridor master plans. On a LOT-PLUS-WATER all-in basis, Sky Ranch’s ~$107,000 is roughly 26% below the comps’ ~$129,000–159,000 (their ~$100K lots plus their own ~$44K Aurora tap). The thesis point not only survives the apples-to-apples correction - it strengthens: Sky Ranch screens cheaper than its corridor peers on EITHER consistent basis. The earlier draft’s apparent in-line positioning was an artifact of comparing Sky Ranch’s bundled number against the comps’ unbundled number; corrected, the relative discount is clear.

Why Sky Ranch should screen somewhat cheaper - and why that is fine: it sits modestly further from the built-out core, its amenity base (the K-12 campus, commercial, trails) is still maturing, and its product skews to the most affordable end. We are not claiming Sky Ranch lots should command Painted Prairie prices today; we are observing that the NAV’s per-lot assumptions are struck at or below the relevant market, leaving the escalation embedded in the comps as unpriced upside rather than a required assumption.

A note on the soft market: Denver lot supply has loosened over the past year and Aurora/Arapahoe home pricing fell 5–8% in 2025, so the comp set is struck in a buyer-friendlier environment than 2024 - these are not peak-cycle figures. Sky Ranch’s annual-cadence delivery model and expanded seven-builder roster are designed precisely to absorb through this softness without discounting lots, and tap fees (a function of water scarcity, not housing demand) have continued to rise through the downturn. The implied pricing is thus underwritten to current, not peak, conditions.

ASSET 3: WATER & WASTEWATER INFRASTRUCTURE

GAAP carrying value: embedded in the $71.3M ‘Investment in water and wastewater systems, net’ line (up from $67.5M at FY2025 year-end), reflecting continued infrastructure investment during the quarter.

The infrastructure base - groundwater and alluvial wells, distribution pipeline, surface storage, two wastewater treatment facilities, and the state-of-the-art water reclamation facility (built for ~$10M in 2019–20, expandable to 5,000+ SFEs) - continues to be carried at historical cost less depreciation. Pure Cycle invested further in water and wastewater infrastructure during H1 FY2026, including capacity to capture stronger industrial (oil & gas) water demand. On the call, the CEO adopted the framing of a “HALO” asset - heavy asset, low obsolescence - and noted the company is using only ~4% of its developed water capacity while generating significant revenue from it.

Colorado municipal water systems typically transact at 1.5–3.0x rate base. We hold the prior methodology, scaled to the modestly higher book value:

ASSET 4: SINGLE-FAMILY RENTAL (BUILD-TO-RENT)

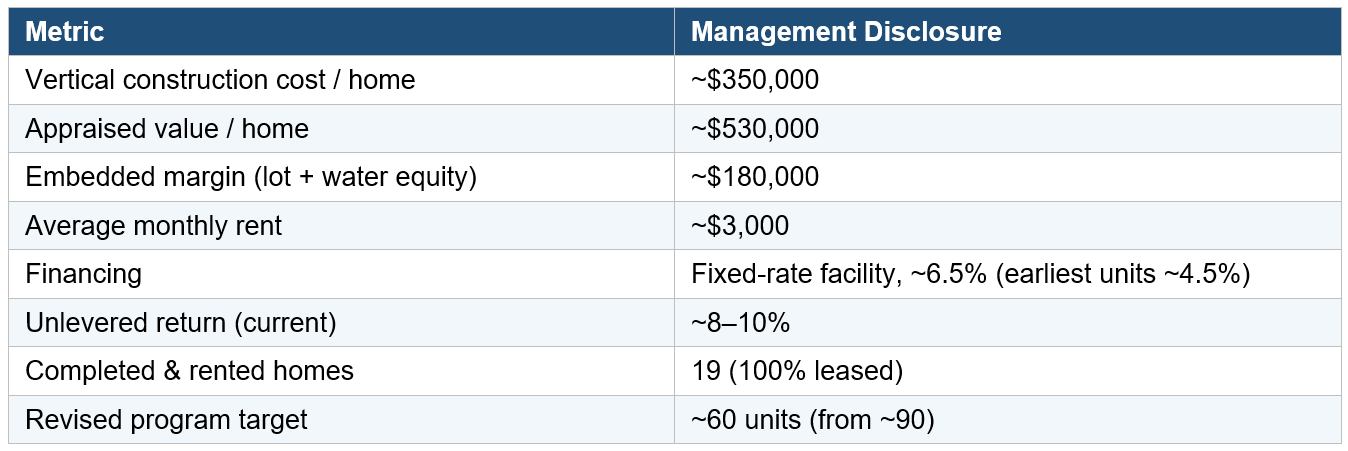

GAAP carrying value: $11.2M (Single-family rental units), up sharply from $5.2M at FY2025 year-end as 19 homes were completed and ~$5.0M of construction was self-financed during H1.

4A. What Changed: A Deliberate Slowdown

This is the segment with the most consequential strategic shift, and it cuts against a naive growth narrative. Management has deliberately scaled back the BTR program from a ~90-unit target to ~60 units. The stated reasons are twofold: (1) the current administration’s stance on corporate ownership of single-family homes introduces policy risk, and (2) management wants to establish clear, demonstrated return metrics on the existing units before committing more capital. Pure Cycle is reselling roughly 30 reserved lots in Phases 2C and 2D back to its homebuilder customers at ~$100,000–110,000 per lot - which actually flows value back into the higher-margin land-development segment.

Demand is not the constraint - discipline is. All 19 completed homes are rented, with management citing 95–100% occupancy and units leased prior to completion through August. The slowdown is a capital-allocation and policy-risk decision, not a demand problem. From an NAV standpoint, this is rational: it caps the segment’s size but redeploys capital into land development and removes the speculative ‘optionality beyond 200 homes’ bucket we previously carried.

4B. Updated Unit Economics (Management-Disclosed)

The Q2 call provided the most detailed BTR economics to date, which we now substitute for our prior estimates:

4C. Revised BTR NAV

We reset the model to the disclosed ~$180K embedded margin per home and the ~60-unit cap. We remove the prior ‘full buildout optionality (200+ homes)’ bucket entirely, since management has explicitly paused expansion. This is a more conservative - and more honest - treatment.

Net effect: BTR NAV falls from $54.7M (Base) to $22.1M (Base). This ~$33M reduction is the single largest downward revision in this refresh. We view it as appropriate de-risking - the capital is not lost, it is being redeployed into land development at attractive margins - but it is a genuine markdown that an honest NAV must reflect.

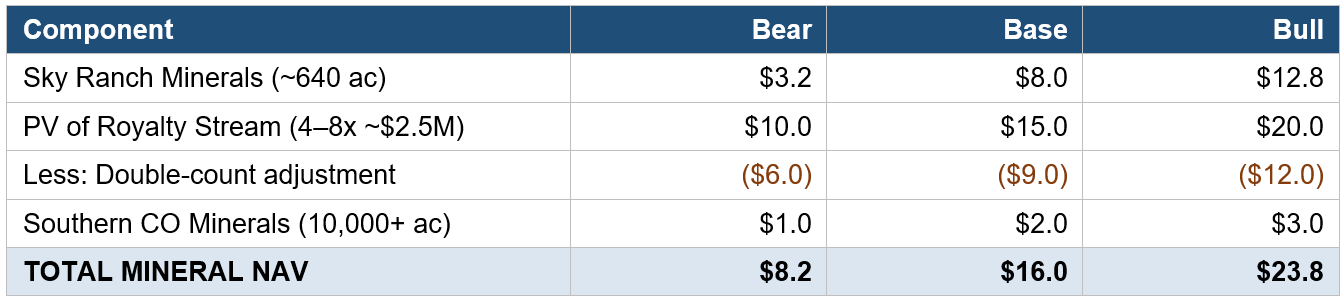

ASSET 5: MINERAL INTERESTS & ROYALTY INCOME

GAAP carrying value: ~$5.0M (Land and mineral rights held for development), up modestly with the Weld County mineral acres.

5A. What Changed: The Royalty Reset

The royalty stream has reset sharply lower, and this is the most important negative data point in the refresh. After a spectacular FY2025 driven by six new wells coming online, oil & gas royalty income, net fell to $0.5M in Q2 FY2026 and $1.26M for H1 FY2026, versus $1.9M and $4.7M in the comparable prior-year periods - a decline of roughly 70–73%. The prior thesis capitalized a $6.7M annual royalty figure; the current run-rate is closer to $2.5M.

Context matters - this is variability, not impairment. Royalty income is a function of production and oil prices, both of which are volatile. The decline reflects the natural decline curve on the 2024 wells and the absence of new completions in the period. Crucially, management framed the offsetting positive on the call: the company’s largest operator spent the prior year permitting ~200 wells in and around the service area and now has a dedicated rig that will take roughly three years to drill them. That drilling drives two things - new royalty wells over time (at zero capital cost to Pure Cycle) and, more immediately, a surge in industrial water sales (priced at ~3x residential rates). In other words, the royalty line is resetting while the industrial-water line inflects upward, both tied to the same drilling program.

5B. Revised Mineral NAV

We mark the capitalized royalty stream to the lower ~$2.5M run-rate, applying the same 4–8x multiple band, while holding per-acre values for the Sky Ranch and southern Colorado positions. We retain a double-count adjustment to avoid valuing the minerals on both a per-acre and cash-flow basis.

Mineral NAV falls from $30.2M (Base) to $16.0M (Base) - a ~$14M markdown reflecting the royalty reset. We note this is partially recaptured elsewhere: the same drilling program supports the higher industrial-water revenue now flowing through the water segment, where management expects to exceed guidance on industrial sales in FY2026. The value migrates across the income statement rather than disappearing.

ASSET 6: NET BALANCE SHEET & THE GROWING CAB RECEIVABLE

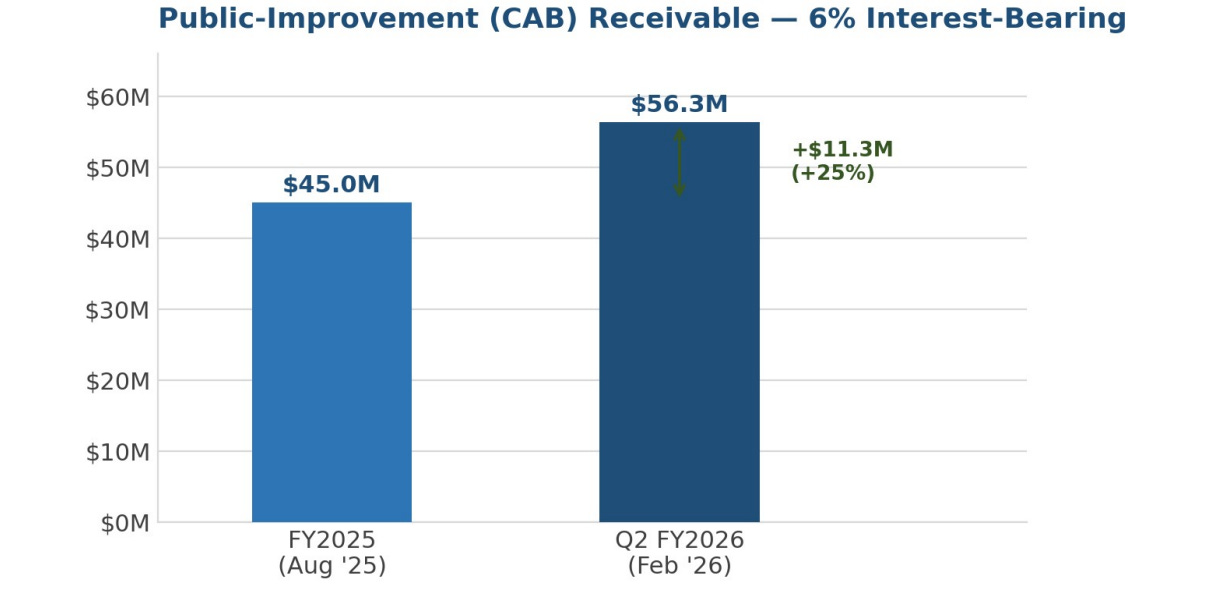

6A. The Public-Improvement Receivable - Now $56.3M

The most underappreciated asset on the balance sheet got materially larger. The related-party note receivable from the Sky Ranch Community Authority Board (CAB) - the public-improvement reimbursement obligation backed by property-tax assessments and bearing 6% interest - grew from ~$45M at FY2025 year-end to $56.3M at February 28, 2026, a ~$11M increase as the company advanced public improvements for Phases 2C, 2D, and 2E. At $56.3M, this single receivable represents ~$2.33 per share of contractual, interest-bearing, government-assessment-backed value.

A defined monetization path, on the record. On the Q2 call management laid out the reimbursement runway with unusual specificity. The 2022 Phase 2 bonds carry a 5-year call provision that begins to burn off in 2027. Because Phase 2 density rose from ~780 to ~1,030 lots, the assessed value (and thus bonding capacity) materially exceeds the original financing assumptions. Management estimates ~$10–12M of additional reimbursables from refinancing the existing Zone 1 bonds, plus potentially ~$20M of fresh financing as Phase 3 commences - a combined ~$30M monetization opportunity centered on 2027, coincident with the interchange financing. This is the mechanism that converts the receivable into cash.

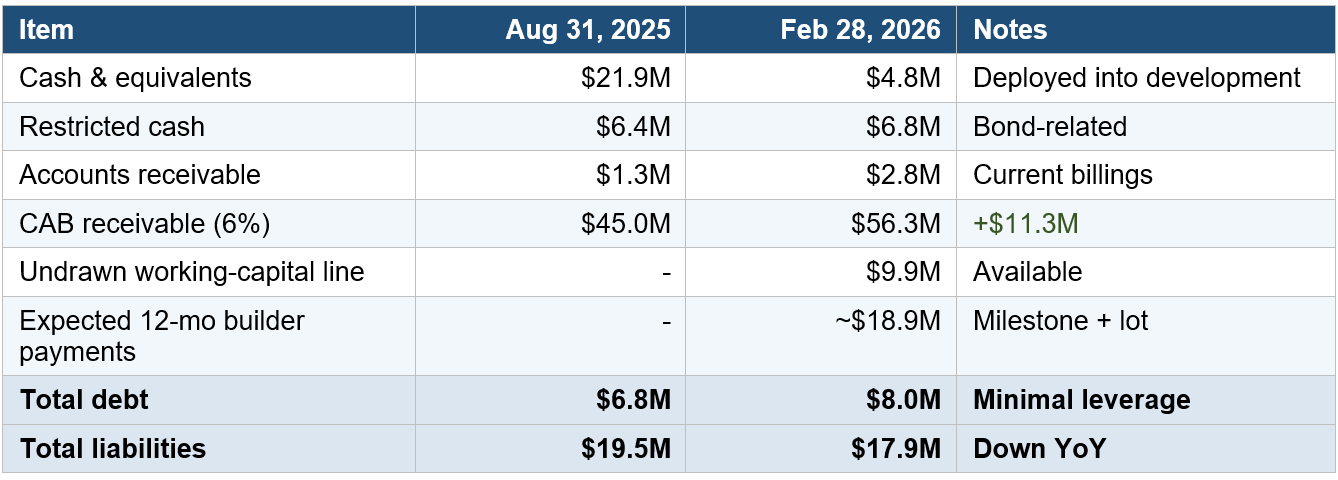

6B. Cash, Liquidity & Liabilities (Q2 FY2026)

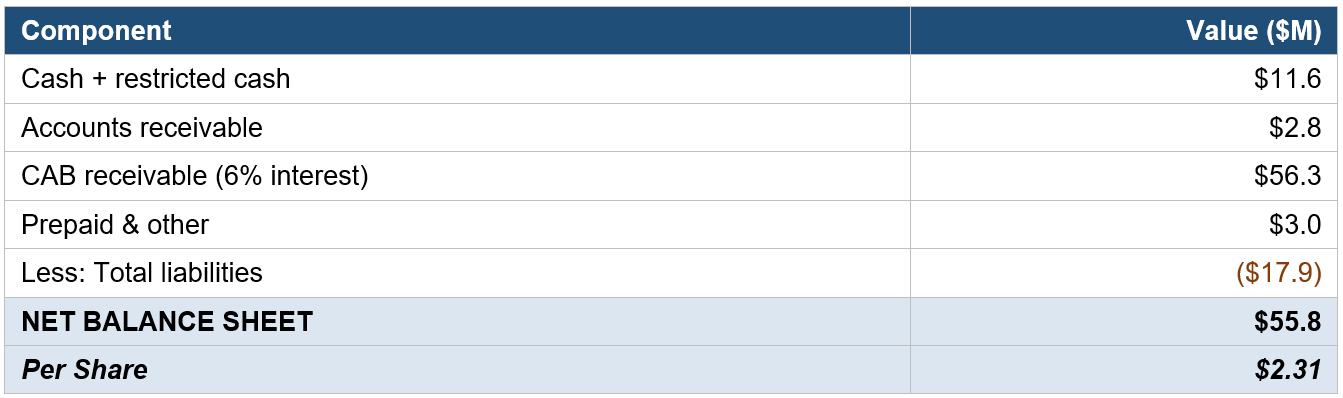

6C. Revised Net Balance Sheet Value

Net effect: the balance-sheet contribution rises from $51.7M to $55.8M, driven almost entirely by the growing CAB receivable, partially offset by lower cash. The cash deployment is not value destruction - it converted into land-under-development, rental units, and a larger interest-bearing receivable, all captured in other line items.

ASSET 7: RECURRING WATER, WASTEWATER & RENTAL REVENUE

Not a balance-sheet line, but a compounding annuity that grows with every connection. With 1,131 taps sold at Sky Ranch and rising rates, recurring water/wastewater service revenue continues to build. The newest wrinkle is the industrial (oil & gas) water inflection: H1 water deliveries rose to 418 AF (from 367 AF), with Q2 deliveries jumping to 272 AF (from 64 AF) almost entirely on oil & gas demand priced at ~3x residential rates. Management’s multi-year delivery contracts and dedicated-rig visibility support continued strength through FY2026–2027.

Management’s own FY2026 guidance frames the recurring base: ~$2.7M of recurring revenue and asset growth, with total revenue of $26–30M and EPS of $0.43–0.52. We do not capitalize this stream separately to avoid double-counting with the water rights and Sky Ranch values, but it is the connective tissue that makes the asset base a compounding utility rather than a static collection of land and water.

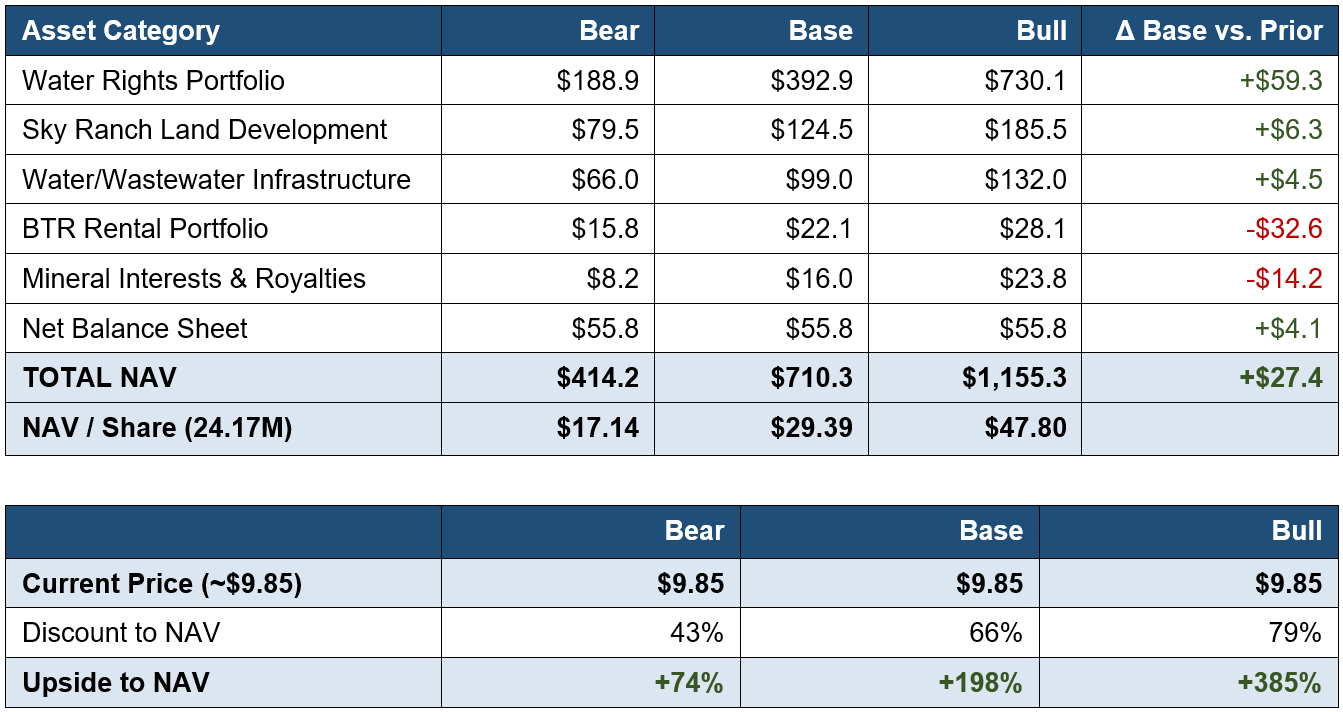

CONSOLIDATED NET ASSET VALUE - PART III (REVISED)

Rolling up every refreshed category produces the following revised consolidated NAV. The table also shows the change versus the prior (Part II) base case, so the direction of each revision is transparent.

The bottom line of the refresh: consolidated Base NAV rises modestly to ~$29.39/share (from ~$28.34) despite meaningful markdowns to BTR and minerals. The reason is instructive — the value lost on the royalty reset and BTR slowdown is more than recovered by the larger water portfolio and the $11M+ growth in the CAB receivable. The thesis is not fragile to any single line item; value migrates across the asset base as the business executes. With the stock at ~$9.85 - having drifted lower even as intrinsic value grew - the discount to Base NAV has widened to ~66%, and even the Bear case implies ~74% upside.

Sensitivity: If You Disagree on Water

The water portfolio remains the largest single driver. For skeptics, here is the NAV with water marked at GAAP book value only (no premium to the comparable-transaction evidence):

Even assigning zero premium to the water - treating ~33,000 AF of Front Range supply and ~26,000 AF of storage at depreciated book - the land pipeline, infrastructure, BTR, minerals, and the $56.3M CAB receivable still clear the current price. The water remains the margin of safety, not the thesis.

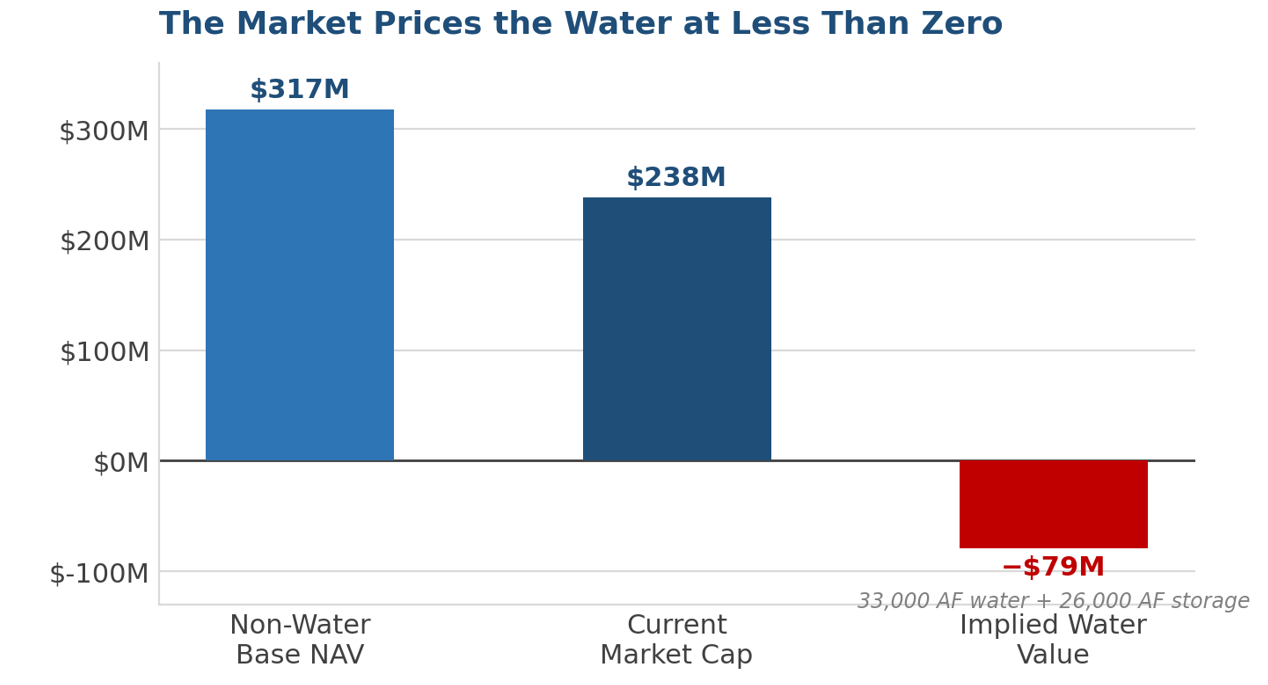

Implied Water Value in the Current Price

Subtracting non-water Base NAV from the current market cap: $124.5M (Sky Ranch) + $99.0M (Infrastructure) + $22.1M (BTR) + $16.0M (Minerals) + $55.8M (Balance Sheet) = $317.4M of non-water value. Against a ~$238M market cap, the market implies negative ~$79M for the water portfolio. The market is still assigning a negative value to the largest private water portfolio on the Colorado Front Range - now ~10% larger than a quarter ago, while the implied discount has actually deepened as the share price drifted lower. You could, in theory, buy the whole company, realize the non-water assets at conservative values, and be paid ~$79M to take ~33,000 AF of water and ~26,000 AF of storage.

WHAT MOVED, AND WHICH WAY

A disciplined refresh should make its revisions legible. Here is the honest scorecard of developments since Part II:

Tailwinds (value-positive)

• Water portfolio +~10% via the 1,635 AF Box Elder Creek Alluvial settlement (Dec 2025), plus explicit recognition of the ~900 AF WISE subscription. Total now ~33,000 AF.

• CAB receivable +$11.3M to $56.3M, with a defined ~$30M monetization path (refinancing + Phase 3 financing) centered on 2027.

• Sky Ranch density up from ~780 to ~1,030 Phase 2 lots; builder roster from 4 to 7; development ~6 months ahead of schedule; tap fees still escalating (~$42K+).

• Industrial water inflection - Q2 deliveries 272 AF vs 64 AF prior year on oil & gas demand at ~3x residential pricing; multi-year contracts and a dedicated rig drilling ~200 permitted wells over ~3 years.

• Equity grew to $148.7M and liabilities fell to $17.9M; 27th consecutive profitable quarter; H1 EPS $0.23 (+15% YoY).

Headwinds (value-negative or de-risking)

• Oil & gas royalty reset - H1 net royalty $1.26M vs $4.72M prior year; run-rate cut from ~$6.7M to ~$2.5M. Mineral NAV marked down ~$14M (Base).

• BTR deliberately scaled back from ~90 to ~60 units on corporate-ownership policy risk and a desire to prove returns first; BTR NAV marked down ~$33M (Base). Capital redeployed into land development.

• Interchange slipped to 2028 (from late 2027); now at ~30% design, 1601 permit targeted mid-2026. Delays the timing of commercial-land value realization.

• Data-center optionality cooled - Colorado policy dysfunction (competing incentive/disincentive bills) and gas-turbine power constraints make the state less competitive for hyperscale demand. We carry commercial land flat, not marked up.

• Cash drawn down to $4.8M from $21.9M - a timing/working-capital feature of the accelerated winter, not solvency stress, but worth monitoring against the $18.9M of expected builder payments and $9.9M undrawn line.

RISK REGISTER

CONCLUSION: THE GAP HELD

Two quarters of fresh disclosure have done what good disclosure should do - they have tested the thesis against reality. The test result is reassuring precisely because it was not uniformly flattering. The royalty stream reset hard. The rental program was reined in. The interchange slipped. And yet the consolidated Base NAV rose, to ~$29.39/share, because the water portfolio grew, the public receivable swelled past $56 million, and the land machine ran ahead of schedule. A thesis that can absorb a 70% royalty cut and a one-third reduction in its rental ambitions and still expand its intrinsic value is a thesis resting on a diversified, compounding asset base rather than a single fragile bet.

Across scenarios, the conclusion is intact:

Bear: ~$17.14/share (+74%). Water at deep discounts to every comparable; royalty at trough; BTR capped; interchange delayed. Requires actively pessimistic assumptions and still clears the price.

Base: ~$29.39/share (+198%). Midpoint values anchored to observable transactions and management’s own disclosed economics. No heroic assumptions — a 6–12 year, steady monetization.

Bull: ~$47.80/share (+385%). Market-clearing Front Range water, accelerated development, commercial land realized, royalty re-acceleration as the 200-well program drills out. Aggressive but inside observable conditions.

The market continues to price ~$9.85 for an asset base demonstrably worth $17–48+, and continues to assign a negative value to ~33,000 acre-feet of Front Range water rights plus ~26,000 acre-feet of water storage. As management put it on the call, this is a “heavy asset, low obsolescence” franchise still monetizing only a fraction of its full water portfolio. Time, water scarcity, and compounding remain on the investor’s side.

Very interesting thanks for the coverage. It seemed on the Q2 call that Colorado is not going to be as much as a boom area for datacentres. Did the conference call comments change your thinking at all with regard to the commercial opportunity for Pure Cycle when it comes to DCs? Secondly, it seems as though they are unlikely to monetise their water rights directly. I fear the most likely path for the thesis is gradual tap fees / water utility growth over a period of 5 decades. Whilst this presents a highly durable asset, it will take a long time to be repaid the investment at current market cap in terms of cash returned to shareholders.

Danke für Ihre ausführlichen Texte rund um das Thema Wasser/Wasserknappheit.Ein sehr komplexes Thema, welches in den nächsten Jahren sicher mehr Aufmerksamkeit verdient.

Erwägen Sie auch einen Bericht über Cadiz Inc. zu verfassen?

J.R.