Pure Cycle Corp (PCYO) | Part 2: NAV Deep Dive

60%+ NAV Discount | Evidenced-Based NAV Breakdown and Asset-by-Asset Analysis

Part I of this thesis established the qualitative case for Pure Cycle Corporation (PCYO) as a structurally mispriced water and land franchise. Part II translates that framework into a granular, evidence-backed net asset valuation. Every material component of PCYO’s asset base is dissected individually, with valuation ranges derived from observable comparable transactions, regulatory filings, management disclosures, and independent market data. The objective is not to arrive at a single “fair value” number but to construct a defensible range of intrinsic value that exposes the magnitude of the discount embedded in the current share price.

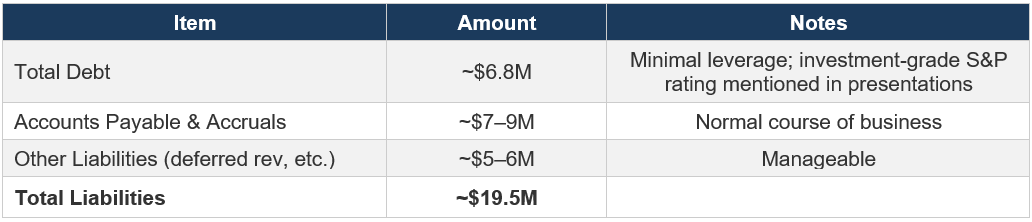

Key reference points: Share price ~$10.50 | Market cap ~$253M | Shares outstanding ~24.1M | Total GAAP equity $142.7M | Total assets $162.2M | FY2025 net income $13.1M | FY2025 EPS $0.54 | Total debt ~$6.8M.

ASSET 1: WATER RIGHTS PORTFOLIO

GAAP carrying value: ~$60–65M (included in “Investments in water and water systems, net”)

1A. Inventory of Water Assets

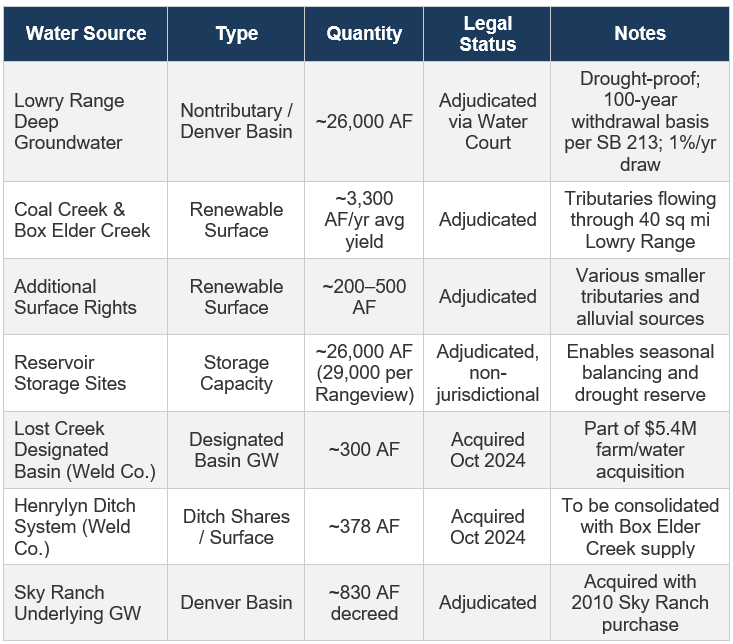

Pure Cycle’s water portfolio, assembled over 35+ years of adjudication and investment, is detailed in company filings and the Rangeview Metropolitan District’s disclosure documents. The portfolio comprises:

Total: approximately 29,500 acre-feet of groundwater and surface water supply, plus ~26,000–29,000 acre-feet of reservoir storage capacity. Management states this portfolio is sufficient to serve approximately 60,000 single-family equivalents at full buildout.

1B. Comparable Transaction Evidence

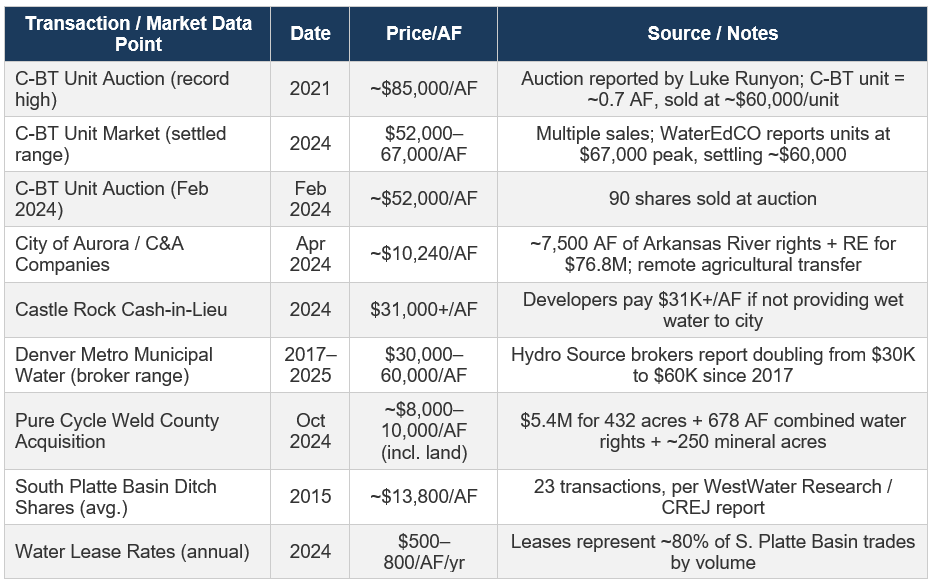

The Colorado Front Range is the most actively traded and best-documented wholesale water market in the western United States. The following transactions and market data points establish the range of values at which water rights comparable to PCYO’s have changed hands:

1C. Valuation Framework by Water Category

Renewable Surface Water (~3,500 AF)

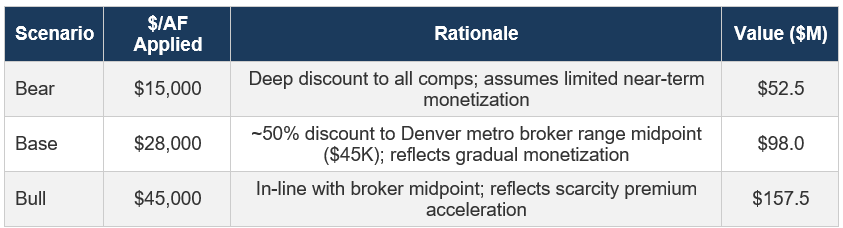

This is Pure Cycle’s most valuable water on a per-AF basis. Renewable surface water that is already adjudicated, proximate to the demand center, and integrated with existing infrastructure commands the highest premium. The closest comparable is the C-BT market, though PCYO’s surface water is sourced locally (Coal Creek, Box Elder Creek) rather than through transbasin diversion, making it immune to Colorado River Compact calls - a significant advantage. C-BT units have traded at $52,000–85,000/AF. Castle Rock requires $31,000+/AF cash-in-lieu for new development. Municipal brokers report $30,000–60,000/AF for Denver metro equivalents. We discount substantially because PCYO’s surface water will be monetized gradually through tap fees ($40,000–42,000 per SFE connection) rather than sold outright in a liquid market, and because the yield is weather-dependent (averaging ~3,300 AF/yr but variable).

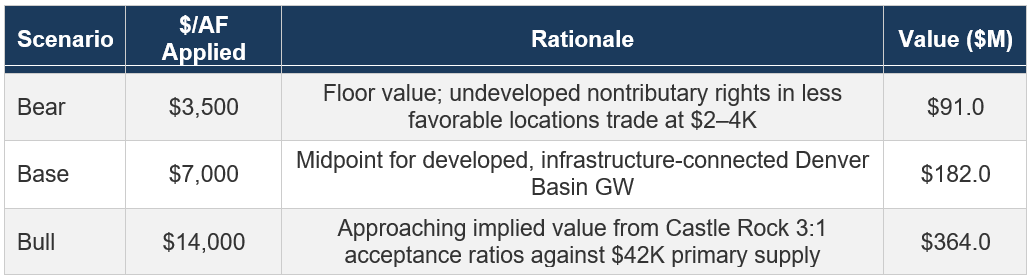

Denver Basin Nontributary Groundwater (~26,000 AF)

This is the largest component by volume but requires careful treatment. Under Colorado’s SB 213 framework, nontributary Denver Basin groundwater is legally withdrawable at a rate of 1% of the adjudicated volume per year over a statutory 100-year aquifer life. This means PCYO can legally withdraw ~260 AF/yr from this source. While “depletable,” this is a 100-year resource - far longer than most infrastructure investments. The groundwater is drought-proof (not dependent on snowpack or surface hydrology), already adjudicated through water court, and available on demand from existing wells.

Valuation anchors: Castle Rock and other south metro communities that rely heavily on Denver Basin groundwater accept dedications at a 3:1 ratio for nontributary rights outside town boundaries, implying the town values each AF of nontributary rights at roughly one-third the value of its primary supply. If primary supply is valued at $30,000–60,000/AF, the implied nontributary value is $10,000–20,000/AF. However, many Front Range communities will not accept Laramie-Fox Hills water at all, and value Arapahoe aquifer water more highly. For remote or undeveloped nontributary rights, secondary market transactions suggest $2,000–8,000/AF depending on location and infrastructure proximity. PCYO’s groundwater sits directly beneath its service area with wells and treatment infrastructure already in place, warranting a premium to undeveloped nontributary rights.

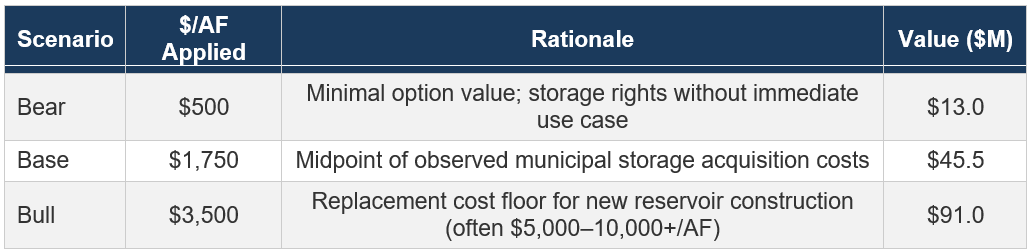

Reservoir Storage Rights (~26,000 AF capacity)

Adjudicated reservoir storage capacity is a distinct asset from the water itself. Storage enables seasonal balancing (capturing spring runoff for summer use), drought buffering, and aquifer storage and recovery (ASR). In a market where water supply is increasingly constrained, the ability to store water is becoming independently valuable. PCYO’s reservoir sites are non-jurisdictional (not subject to Army Corps or other federal wetlands permitting), reducing regulatory risk. Comparable reservoir storage values in Colorado are sparse, but municipal utilities have paid $1,000–5,000/AF for raw storage entitlements, and the capital cost of constructing new storage significantly exceeds this.

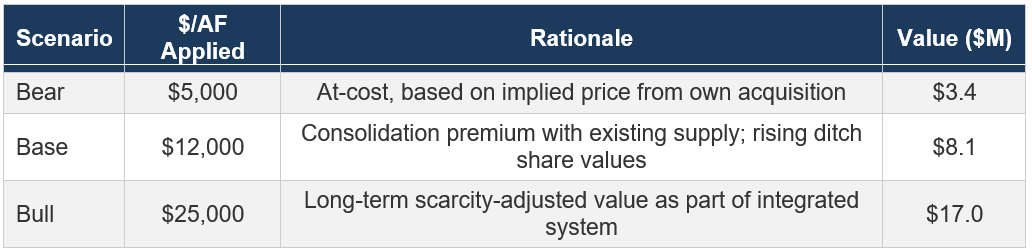

Weld County Water Acquisitions (~678 AF combined)

In October 2024, Pure Cycle acquired approximately 432 acres of land in Weld County plus 378 AF of Henrylyn ditch system water and 300 AF of Lost Creek designated basin water, along with ~250 net mineral acres, for $5.4 million. This is a directly observable transaction price from PCYO itself. Attributing roughly $1.5–2.0M to the land and mineral value, the implied water price is approximately $5,000–8,000/AF. Management has stated the intent to consolidate this water with the Lowry Range Box Elder Creek supply, suggesting strategic value beyond the standalone acquisition cost.

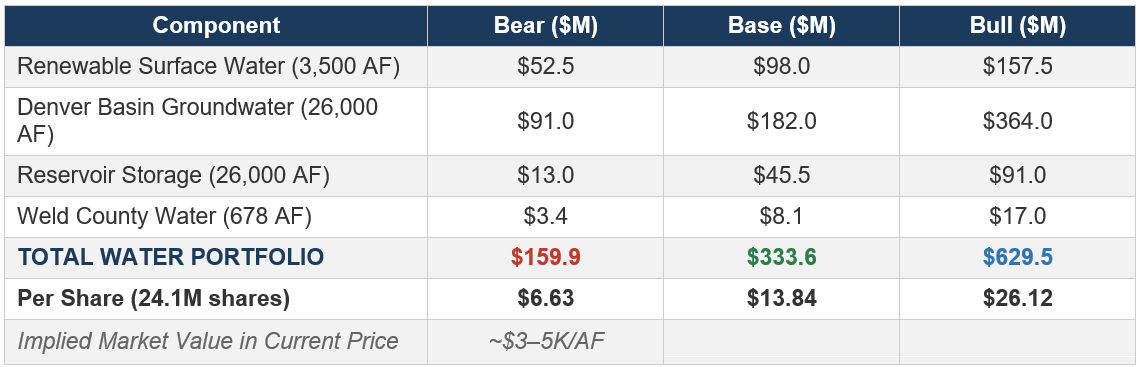

1D. Total Water Portfolio NAV

The critical insight: after stripping out all other assets at book value ($142.7M equity – $60M water systems book value = ~$83M non-water equity), the market’s implied value for the water portfolio is approximately $253M market cap – $83M = ~$170M, or roughly $5,500/AF across the entire portfolio. This is a fraction of what comparable water trades for on the Front Range. Even the bear case of $160M exceeds this implied market value, and the base case of $334M is nearly double.

ASSET 2: SKY RANCH LAND DEVELOPMENT

Book value of land under development + held for development: ~$10–12M

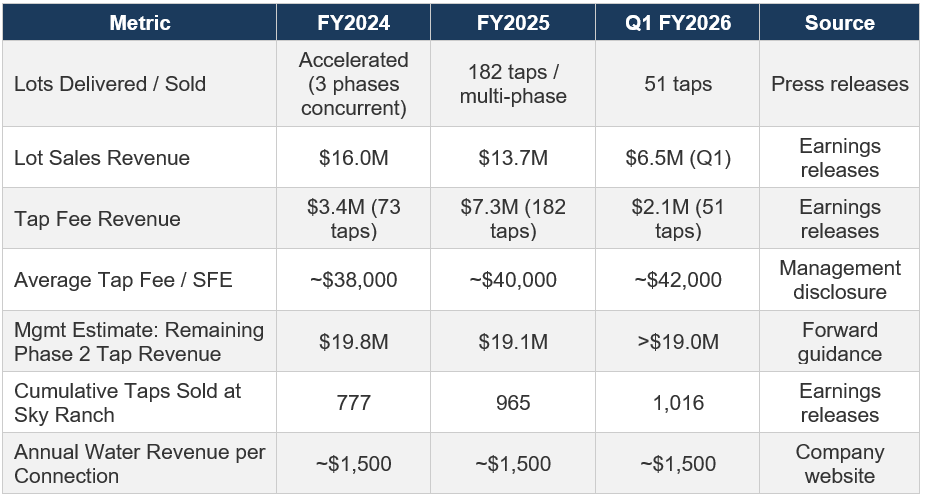

2A. Development Status & Lot Economics

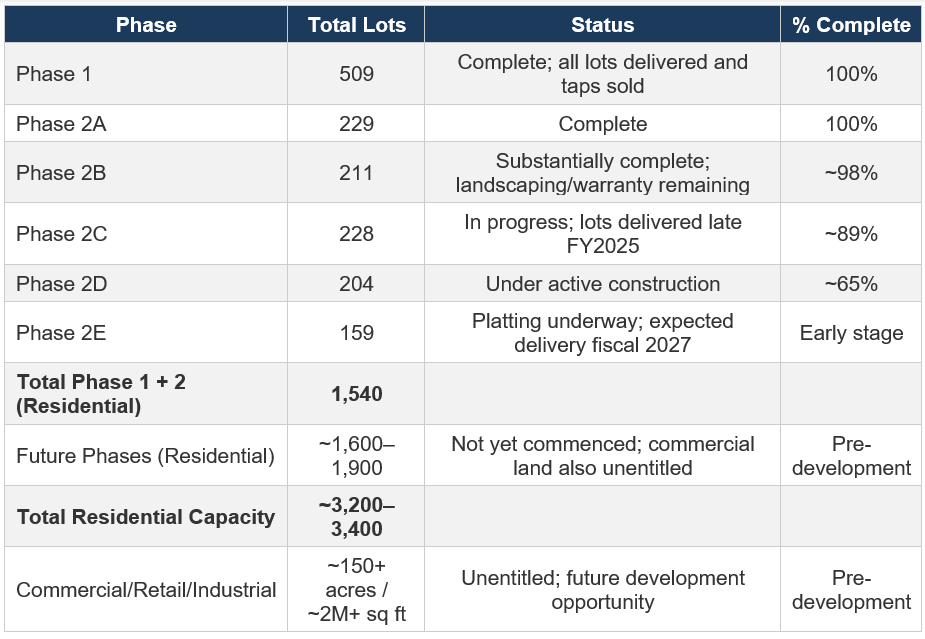

Sky Ranch is a 930-acre master planned community in Arapahoe County along the I-70 corridor, approximately 4 miles south of Denver International Airport. The property was acquired in 2010 out of bankruptcy for $7.0 million. As of November 30, 2025 (most recent quarter), the development status is:

2B. Evidenced Lot & Tap Fee Economics

Management disclosures provide remarkably detailed economics:

Key observation: Average tap fees have risen from ~$38,000 in FY2024 to ~$42,000 in Q1 FY2026 - a ~10% increase in just two years - reflecting the structural escalation of Front Range water costs. Management has confirmed the price per SFE is increasing even when the blended average is moderated by product mix (townhomes vs. detached). This is a secular tailwind: tap fees are a direct function of water scarcity, and water prices on the Front Range have compounded at 12–15% annually over the past decade.

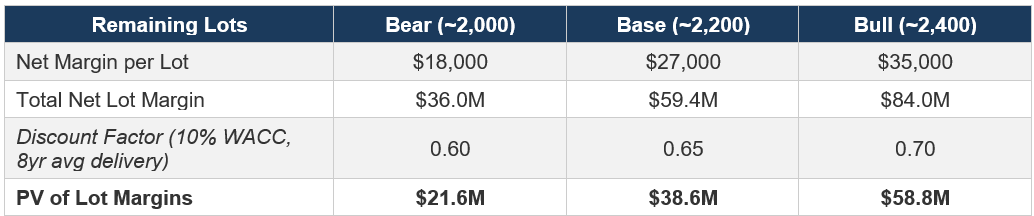

2C. Remaining Developable Value

As of November 30, 2025, approximately 1,016 taps have been sold. Total residential capacity is ~3,200–3,400 units. Remaining residential units: approximately 2,200–2,400. Of these, approximately 524 are in the current Phase 2 pipeline (2D: 204 lots + 2E: 159 lots = 363, plus remaining 2B/2C taps still to close). Beyond Phase 2, approximately 1,600–1,900 additional residential lots are planned in future phases, plus 150+ acres of commercial land.

To value the remaining development, we model three components separately: (1) net lot sale margins, (2) remaining tap fee revenue, and (3) commercial parcel value. Each is derived from observable data.

Lot Sale Margins

FY2025 lot sales revenue was $13.7M on approximately 200–230 lots delivered, implying an average lot sale price of ~$60,000–70,000. Cost of lot sales includes grading, roads, wet/dry utilities, and landscaping. Based on typical land development gross margins of 35–50% for finished lots in the Denver market, and PCYO’s reported segment profitability, net margins per lot are estimated at $20,000–35,000 after development costs.

Remaining Tap Fee Revenue

Management estimates >$19M in Phase 2 tap fee revenue remaining over the next 3 years. Beyond Phase 2, an additional 1,600–1,900 connections at rising tap prices represent substantial incremental revenue. We apply a growth rate to tap fees reflecting the observed ~5% annual escalation.

Commercial / Retail / Industrial Land (150+ acres)

Sky Ranch includes 150+ acres zoned for commercial, retail, and light industrial use, along the I-70 frontage. Management has discussed a new I-70 interchange under construction in 2026, which will dramatically improve accessibility and value of commercial parcels. Front Range commercial land along I-70 in the Denver metro trades at $100,000–300,000+/acre for fully entitled, utility-served parcels near interchanges. However, PCYO’s commercial land is earlier-stage. We apply a wide range.

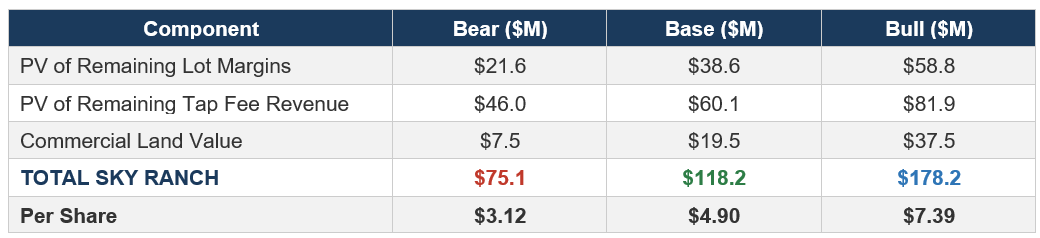

2D. Total Sky Ranch NAV

Anchor point: PCYO acquired the entire 930-acre Sky Ranch property for $7.0M in 2010. In the 15 years since, the company has extracted well over $50M in cumulative lot sale and tap fee revenue from less than half of the residential capacity, while the unimproved land has appreciated dramatically. The remaining development pipeline generates more value than the entire original acquisition cost many times over.

ASSET 3: WATER & WASTEWATER INFRASTRUCTURE

GAAP carrying value: ~$60–65M (Investments in water and water systems, net) + ~$3M construction in progress

Pure Cycle’s infrastructure portfolio includes 11 groundwater wells, 3 alluvial wells, 15+ miles of distribution pipeline, 150 AF of surface storage, two wastewater treatment facilities, a $10 million state-of-the-art water reclamation facility (completed February 2020 with capacity to serve 2,000 SFEs, expandable to 5,000+), and associated pumping, treatment, and SCADA control systems. This infrastructure is carried at historical cost less depreciation - a figure that bears no relationship to replacement cost in an inflationary environment where construction costs, permitting timelines, and environmental compliance requirements have escalated dramatically.

Municipal water systems in Colorado are typically valued at 1.5–3.0x rate base (book value) in acquisition transactions. The City of Thornton’s 2020 acquisition of water infrastructure from various small providers, and Parker Water & Sanitation’s ongoing infrastructure investments, provide contextual support for a replacement cost premium. The reclamation facility alone cost $10M to build in 2019–2020; replicating it today would likely cost $14–18M given construction cost inflation.

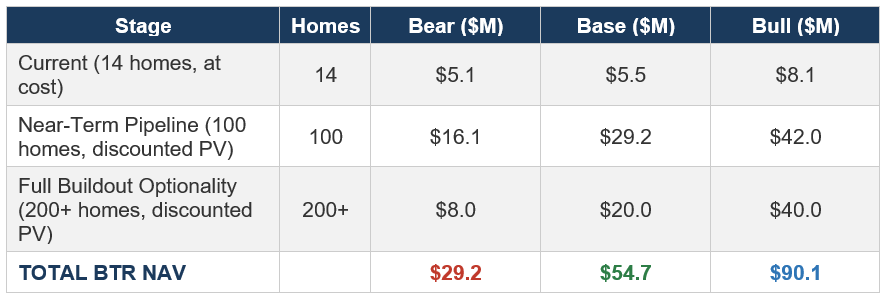

ASSET 4: SINGLE-FAMILY RENTAL (BUILD-TO-RENT) PORTFOLIO

GAAP carrying value: ~$5.1M (Single-family rental units on balance sheet)

4A. Current State

As of the latest filings, PCYO owns 14 completed and rented single-family homes at Sky Ranch. An additional 17 homes are under contract for construction in Phase 2B with expected delivery in fiscal 2026. Management has increased the Phase 2 target to 100 homes total, with the ability to add more than 200 homes as Sky Ranch builds out. The BTR segment generated its first full year of rental income in FY2024.

Demand signal: Management repeatedly references “overwhelming demand” for rental homes at Sky Ranch - a direct quote from multiple earnings releases. The company has progressively raised its rental unit targets (from the initial ~14 to 98 in Phase 2, to 100+ in Phase 2, to 200+ at buildout), suggesting demand exceeds the pace at which they can build.

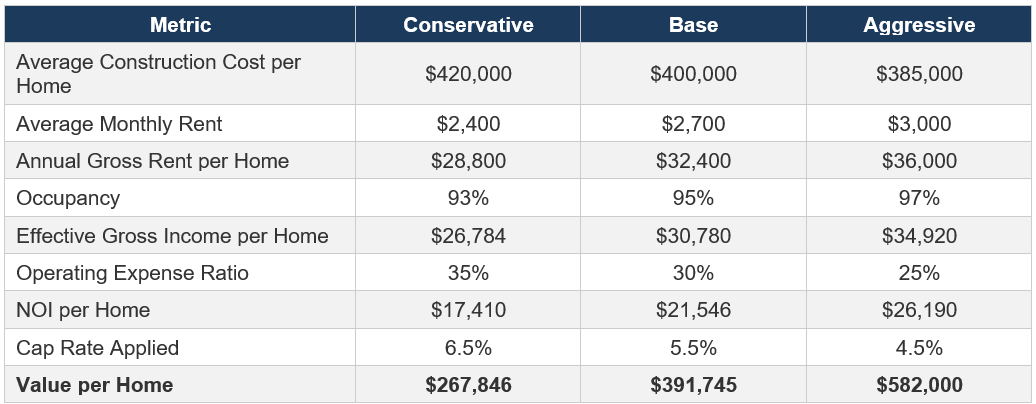

4B. Unit Economics

Denver-area entry-level single-family homes in the Sky Ranch price range ($380,000–450,000 construction cost) rent for approximately $2,200–3,000/month depending on size and finishes. Institutional BTR investors (Invitation Homes, American Homes 4 Rent, NexPoint Residential Trust) typically acquire stabilized SFR portfolios at cap rates of 4.5–6.5% in growth markets.

4C. Portfolio NAV at Scale

We model three milestones: current (14 homes), near-term (100 homes by ~FY2028), and full buildout (200+ homes). The NAV captures only homes actually built or firmly planned; future optionality beyond 200 homes is free.

ASSET 5: MINERAL INTERESTS & ROYALTY INCOME

GAAP carrying value: ~$3.7M (Land and mineral rights, net of amortization)

5A. Asset Description

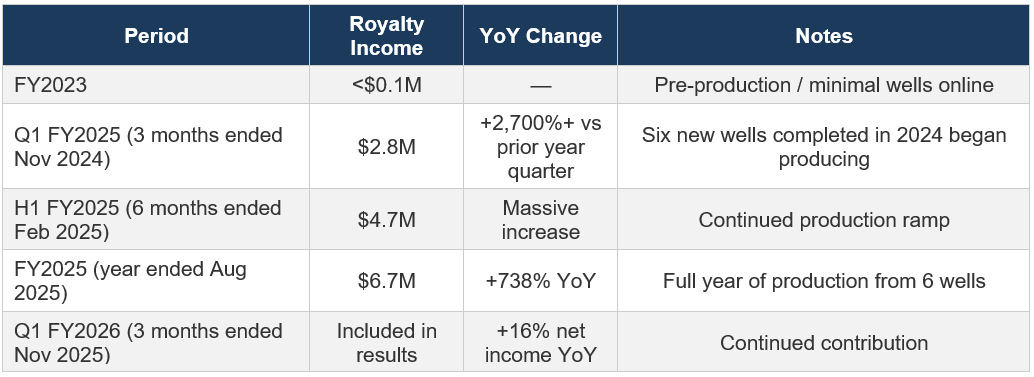

Pure Cycle owns over 10,000 net mineral acres, with the majority in southern Colorado. The most productive holding is approximately 640–700 acres in the Niobrara Formation of the Southern Wattenberg Field, directly underlying and adjacent to Sky Ranch. In 2011, the company executed an oil and gas lease with Anadarko (now Occidental) receiving a $1.27M bonus payment and a 20% gross royalty on production. Six horizontal wells have been completed and are producing as of the latest reports.

5B. Royalty Income Evidence

The royalty income trajectory is extraordinary:

$6.7 million in annual royalty income from just six wells on ~640 acres is a remarkably high yield. This is essentially free cash flow - PCYO bears zero drilling or completion costs as a royalty owner. The company has disclosed that it has entered into an agreement with its operator for an additional well pad, suggesting additional wells may be drilled. Each incremental well adds to the royalty stream at zero capital cost to PCYO.

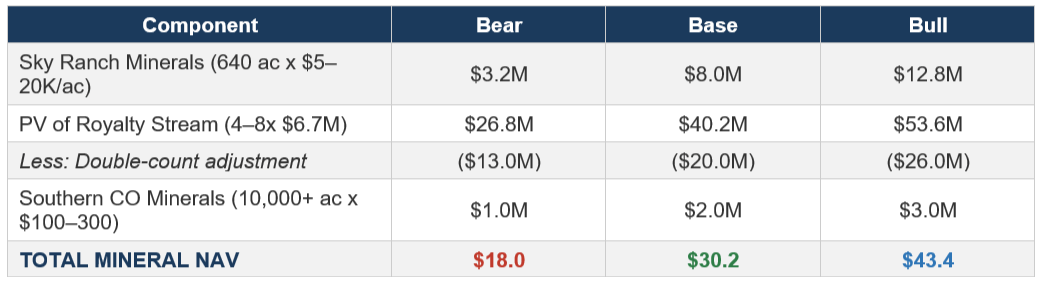

5C. Mineral Valuation

DJ Basin / Wattenberg mineral rights with producing wells typically trade at $5,000–20,000+ per net mineral acre for high-quality Niobrara positions. Non-operated mineral interests with proven production are commonly valued at 4–8x annual royalty income (PV-10 methodology, applying a discount for commodity price risk and decline curves). We also carry the 10,000+ acres in southern Colorado at nominal value ($100–300/acre) as these lack near-term production.

Note: The double-count adjustment prevents valuing the minerals both on a per-acre basis and a PV-of-cash-flow basis, since both approaches capture the same underlying asset.

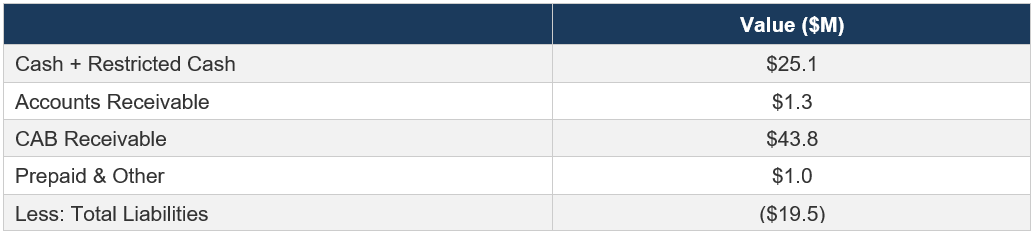

ASSET 6: NET BALANCE SHEET ITEMS

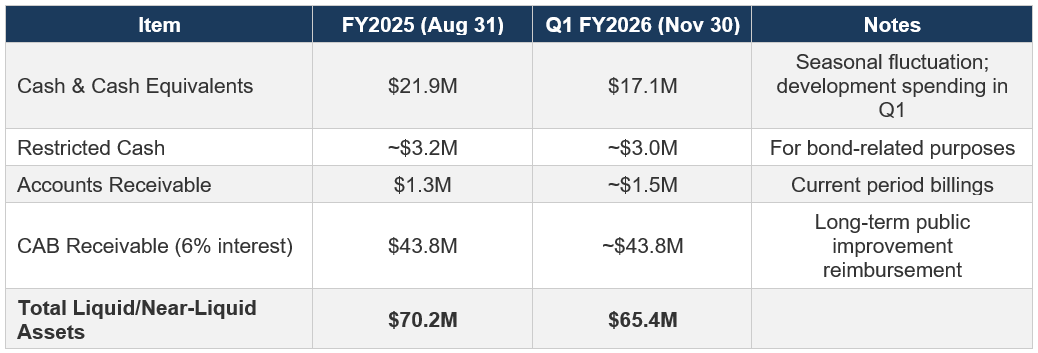

6A. CAB Receivable ($43.8M at 6% Interest)

This is one of the most underappreciated assets on the balance sheet. The Sky Ranch Community Authority Board (CAB) has approved public improvement reimbursements to Pure Cycle, represented as a receivable bearing 6% annual interest. The CAB is a quasi-governmental entity that levies property tax assessments on Sky Ranch homeowners to repay this obligation. As more homes are built and occupied, the tax base grows, accelerating repayment capacity. This is effectively a government-secured receivable - not a speculative developer IOU - with a contractual 6% coupon. At face value, $43.8M represents $1.82/share. The receivable is real, interest-bearing, and growing as development proceeds.

6B. Cash & Liquid Assets

6C. Liabilities

6C. Net Balance Sheet Value

ASSET 7: RECURRING WATER & WASTEWATER SERVICE REVENUE

This is not a traditional “asset” on the balance sheet, but it represents an annuity stream that grows with every home built and occupied at Sky Ranch and across the Lowry Range service area.

Current State: Approximately 1,016 connections sold at Sky Ranch as of November 30, 2025. Residential water deliveries grew to 347 AF in FY2025 (up from 306 AF in FY2024), representing ~1,000+ active residential connections generating ~$1,500/year each = ~$1.5M+ in annual recurring service revenue. This revenue compounds with every new home occupied - it never goes away. At 3,200–3,400 residential connections at Sky Ranch alone, annual recurring service revenue reaches $4.8–5.1M. At 60,000 SFEs across the full Lowry Range service area, the theoretical recurring revenue potential is $90M/year.

We do not capitalize this revenue stream separately to avoid double-counting with the water rights and Sky Ranch development values. However, it is important to recognize that the tap fee captures only the upfront monetization of a water right; the perpetual service revenue is an additional, compounding value layer that the market largely ignores.

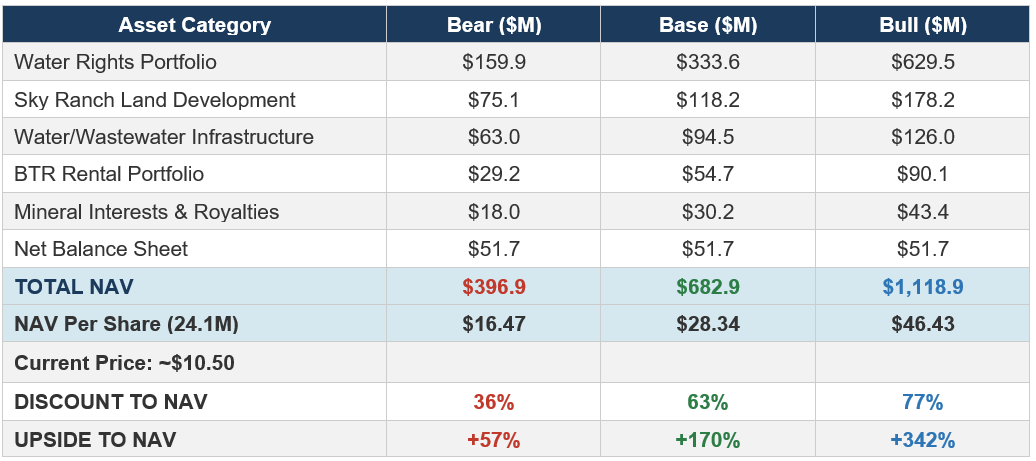

CONSOLIDATED NET ASSET VALUE - PART II REVISED

Incorporating the deeper analysis from each asset category, the revised consolidated NAV is:

Sensitivity: What If You Disagree on Water?

The water rights portfolio is by far the largest value driver. For investors skeptical of our valuation approach, here is the NAV sensitivity excluding all water rights above book value:

Even if you assign zero premium to water rights - treating them at GAAP book value with no recognition of the $30,000–67,000/AF market reality - the stock still trades at a discount to NAV. The land development pipeline, mineral royalties, BTR portfolio, and net balance sheet alone justify a price above the current market. The water rights are the margin of safety, not the thesis - they are the free optionality on a scarce, appreciating resource that the market assigns near-zero value to.

Implied Water Value in Current Stock Price

If we subtract the non-water NAV at base case values from the current market cap:

Non-water base NAV: $118.2 (Sky Ranch) + $94.5 (Infrastructure) + $54.7 (BTR) + $30.2 (Minerals) + $51.7 (Balance Sheet) = $349.3M

Market Cap: ~$253M. Implied water value: $253M – $349.3M = NEGATIVE $96.3M.

The market is not merely undervaluing the water - it is implicitly assigning a negative value to the largest private water portfolio on the Colorado Front Range. Put differently, you could buy the entire company, sell every non-water asset at reasonable values, and receive 29,500+ acre-feet of water rights and 26,000 AF of reservoir storage for free, plus pocket approximately $96 million in cash.

CONCLUSION: THE EVIDENCE IS OVERWHELMING

This Part II analysis has built a granular, evidence-backed NAV for Pure Cycle Corporation using observable comparable transactions (C-BT unit auctions at $52,000–67,000/AF, Aurora’s $10,240/AF Arkansas River acquisition, Castle Rock’s $31,000+/AF cash-in-lieu, PCYO’s own $5.4M Weld County water purchase), management’s own disclosed economics ($40,000–42,000 average tap fees, >$19M Phase 2 tap pipeline, $6.7M royalty income, $1,500/connection annual service revenue), and standard valuation methodologies (replacement cost for infrastructure, cap rate analysis for BTR, PV-10 for minerals).

The results are unambiguous across every scenario:

Bear case: NAV of ~$16.47/share (+57% upside). Applies the lowest reasonable values to every asset category. Would imply water rights worth less than Castle Rock’s cash-in-lieu fees. Requires actively pessimistic assumptions on housing, oil prices, water scarcity, and commercial land.

Base case: NAV of ~$28.34/share (+170% upside). Applies midpoint values supported by directly comparable transactions. Assumes gradual, steady monetization of the asset base over 8–12 years. No heroic assumptions required.

Bull case: NAV of ~$46.43/share (+342% upside). Applies market-clearing prices for Front Range water, assumes accelerated development pace, compressed BTR cap rates, and full mineral production upside. Aggressive but within the realm of observable market conditions.

The thesis does not depend on any single catalyst or heroic assumption. It rests on a simple observation: the market is pricing $10.50 for an asset base that is demonstrably worth $16–46+, with the gap widening every year as water scarcity deepens, development proceeds, and recurring revenue compounds. Time is on the investor’s side.