Pure Cycle Corp (PCYO) | Part 1 : Hidden Water Rights

60%+ NAV Discount | Water, Land & Infrastructure Compounder Hidden in Plain Sight on the Colorado Front Range

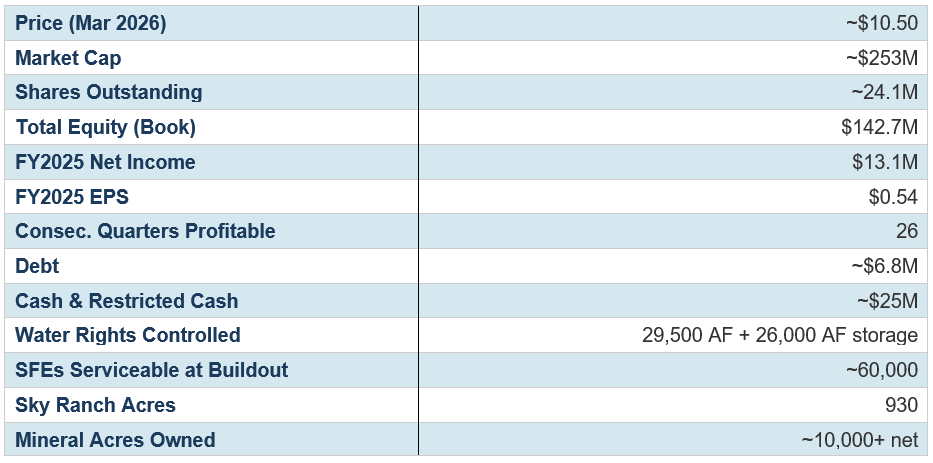

Pure Cycle Corporation (NASDAQ: PCYO) is among the most structurally mispriced water and land assets on public markets today. Trading at roughly $10.50 per share with a market capitalization of approximately $253 million, the company owns or controls 29,500 acre-feet of adjudicated groundwater and surface water rights, 26,000 acre-feet of reservoir storage capacity, a 930-acre master planned community under active development four miles from Denver International Airport, over 10,000 net mineral acres, a growing single-family rental portfolio, and the infrastructure (wells, treatment plants, pipelines, reclamation facilities) to monetize all of it. The market assigns an implied value to these water rights that is a fraction of comparable transaction pricing on the Colorado Front Range, where Colorado-Big Thompson units have traded at $52,000–67,000 per acre-foot in recent years and municipal water in the Denver metro area commands $30,000–60,000 per acre-foot.

This thesis argues that PCYO’s net asset value materially exceeds its current market capitalization under conservative assumptions, and that a series of organic catalysts - continued Sky Ranch lot delivery, expanding tap fee and recurring service revenues, build-to-rent scale, mineral royalty income, and an eventual reckoning with Front Range water scarcity - will steadily surface this value over the next three to seven years. The company operates with minimal debt ($6.8 million), has posted twenty-six consecutive quarters of positive net income, is led by a 35-year CEO who owns a meaningful equity stake, and is actively repurchasing shares at prices it publicly characterizes as “considerably undervalued.”

Base case NAV: ~$18–25 per share. Bull case NAV (reflecting market-clearing water rights values): ~$35–50+ per share. The stock trades at roughly $10.50.

COMPANY HISTORY: FROM SHELL TO STRATEGIC ASSET AGGREGATOR

")

Pure Cycle was incorporated in Delaware in 1976, originally focused on patented water purification and recycling technologies. For its first two decades, the company was essentially a pre-revenue development-stage entity, burning cash on technology development while slowly assembling water rights and infrastructure in the Denver Basin. The transformational event came in 1996, when Pure Cycle entered into a comprehensive settlement agreement with the State of Colorado Board of Land Commissioners and the Rangeview Metropolitan District. This agreement granted Pure Cycle the exclusive right to provide water and wastewater services to approximately 24,000 acres of primarily undeveloped state-owned land in southeastern Arapahoe County known as the Lowry Range.

This was an extraordinary concession. The Lowry Range sits in one of the fastest-growing corridors of the Denver metropolitan area, south of Denver International Airport, and its underlying Denver Basin aquifers contained tens of thousands of acre-feet of adjudicated groundwater. Pure Cycle invested nearly $70 million over the subsequent decades to adjudicate annual water supplies exceeding 30,000 acre-feet of drought-proof groundwater, approximately 3,300 acre-feet of renewable surface water from Coal Creek and Box Elder Creek tributaries, and non-jurisdictional reservoir storage sites providing at least 25,000 acre-feet of capacity. In 2006, the company purchased an additional 60,000 acre-feet per year of senior renewable water rights (Arkansas River surface water tied to ~17,500 acres of irrigated farmland in southeastern Colorado) to further bolster its portfolio.

In 2010, Pure Cycle made the acquisition that would redefine its business model. The company acquired the promissory note on the Sky Ranch property from Bank of America for $7.0 million in cash - purchasing a 931-acre property in Arapahoe County, adjacent to I-70, four miles south of Denver International Airport, out of a complex out-of-state bankruptcy. The property was zoned for up to 4,850 single-family equivalent units of residential, commercial, and retail development. At full buildout, the water and wastewater utilities at Sky Ranch were anticipated to generate in excess of $132 million in cumulative tap fee revenue and $6 million annually in recurring service fee revenue.

In 2015, in a pivotal capital recycling move, the company sold its ~14,600-acre Arkansas River farm and Fort Lyon Canal water portfolio for approximately $53 million to Arkansas River Farms, LLC (an affiliate of C&A Companies and Resource Land Holdings). This sale accomplished two objectives: it dramatically strengthened the balance sheet and freed management to focus entirely on monetizing the higher-value Denver metro water and land assets, particularly Sky Ranch.

Development at Sky Ranch broke ground in March 2018, with the initial 506-lot phase sold to three national homebuilders. Since then, Pure Cycle has delivered over 1,100 finished lots to homebuilder partners, built a state-of-the-art $10 million water reclamation facility, launched a build-to-rent single-family rental segment (2021), and expanded its mineral royalty income stream from oil and gas wells drilled on and around Sky Ranch in the Niobrara Formation of the Southern Wattenberg Field.

BUSINESS MODEL: THREE INTERLOCKING SEGMENTS

Water & Wastewater Resource Development

This is the core franchise. Pure Cycle owns or controls a portfolio of water rights comprising 29,500 acre-feet of groundwater and surface water and 26,000 acre-feet of adjudicated reservoir storage sites, sufficient to serve an estimated 60,000 single-family equivalents at full buildout. The water supply is sourced from deep Denver Basin aquifers (drought-proof groundwater), renewable surface tributaries (Coal Creek and Box Elder Creek) flowing through the 40-square-mile Lowry Range, and recently acquired Lost Creek and Henrylyn ditch water in Weld County. The company operates the full vertical stack: wells, treatment plants, storage, bulk transmission, retail distribution, wastewater collection, and a reclamation facility that treats 100% of Sky Ranch wastewater for reuse as irrigation and industrial supply.

Revenue is generated through two mechanisms. First, one-time tap fees paid by homebuilders when they pull building permits. These fees fund water rights dedication and infrastructure and have been rising due to Front Range water scarcity. For the nine months ended May 31, 2025, tap fee revenue surged to $5.3 million from $1.2 million in the prior year period. Second, recurring monthly metered usage fees from residential, commercial, and industrial customers, averaging approximately $1,500 annually per connection ($1,000 water, $500 sewer). Colorado requires developers to demonstrate 200 years of water supply before a building permit is granted; Pure Cycle’s enormous water portfolio makes it one of the few entities capable of self-certifying this requirement for its own developments, creating an unassailable regulatory moat.

Additional water revenue comes from bulk sales to oil and gas operators for drilling and completion operations. This revenue stream is lumpy - 639 acre-feet delivered in FY2025 versus a record 1,818 in FY2024 - but it monetizes excess capacity at high margins while the residential customer base scales.

Land Development

Launched in 2017, this segment develops the 930-acre Sky Ranch master planned community into finished lots sold to national homebuilder partners (including Richmond American, Meritage, and others). Sky Ranch is positioned as an entry-level, affordable community along the I-70 corridor - a strategic pricing niche that has proven remarkably resilient through rising interest rate environments because it targets first-time buyers underserved by the broader Denver market.

Pure Cycle’s model is distinctive: the company develops horizontal infrastructure (roads, utilities, grading, landscaping) and delivers “finished lots” to builders on an annual just-in-time cadence, minimizing excess capacity while maintaining a steady development pipeline. At full buildout, Sky Ranch is expected to accommodate approximately 3,200–3,400 residential units plus over 2 million square feet of commercial/retail/light industrial development translating to an additional ~1,800 SFEs.

As of the most recent filings, Phase 2A is complete, Phase 2B is substantially complete, Phase 2C lots were delivered in late FY2025, Phase 2D is under construction for delivery in early FY2026, and Phase 2E is being platted for delivery by end of calendar 2026. The company has sold over 1,100 lots in Phases 1, 2A, 2B, and 2C. Lot sales revenue was $16.0 million in FY2024, up 135% from FY2023.

Single-Family Rental (Build-to-Rent)

Launched in 2021, this newest segment retains select lots at Sky Ranch and contracts with national homebuilders to construct single-family homes for long-term lease. As of the latest reporting, the company owns 14 completed and rented homes, with an additional 17 homes forecasted for construction in Phase 2B and a total of over 200 lots reserved for the rental portfolio. This segment generates three revenue streams simultaneously: retained land value appreciation, recurring monthly rent, and water/wastewater service revenue from each connection. It represents an embedded REIT within the operating company.

Mineral Royalties (Hidden Fourth Segment)

Pure Cycle owns over 10,000 net mineral acres, with the most valuable concentration being approximately 700 acres in the oil-rich Niobrara Formation within the Southern Wattenberg Field at and around Sky Ranch. Six additional wells were completed in calendar 2024, with royalty income contributing meaningfully to FY2025 and Q1 FY2026 results. This is a capital-free revenue stream - operators bear all drilling and completion costs while Pure Cycle collects royalties on production from wells pooled with its mineral interests.

MANAGEMENT QUALITY, INCENTIVES & TRACK RECORD

Mark W. Harding - CEO/President (Since 2005; At Company Since 1990)

Harding is the indispensable principal. He joined Pure Cycle in 1990 from Price Waterhouse’s management consulting practice, holding a Bachelor’s in Computer Science and a Master’s in Business Administration from the University of Denver. He rose through the ranks as Corporate Secretary, CFO, and President (2001) before becoming CEO in 2005. During his 35-year tenure, Harding has been directly responsible for acquiring over $100 million in water and land interests, negotiating the foundational Lowry Range settlement, orchestrating the Sky Ranch acquisition at a distressed price, executing the $53 million Arkansas River sale, and transforming Pure Cycle from a pre-revenue development-stage entity into a consistently profitable, multi-segment operating company.

Harding owns approximately 2.2% of shares outstanding, aligning his economic interests with shareholders. His compensation structure (FY2023: $525,000 base salary, $750,000 performance-based bonus) ties rewards to development milestones and financial performance. He serves on multiple Denver-area water advisory boards and is regarded as a deep domain expert in Colorado water law and infrastructure.

Marc Spezialy - VP & CFO (Since 2023)

Spezialy brought fresh financial discipline to an already conservative balance sheet. His commentary in earnings releases emphasizes capital discipline, ROA and EPS growth, and prudent pacing of development to match builder absorption rates. Together, Harding and Spezialy have articulated a clear capital allocation framework: (1) invest in Sky Ranch phase development, (2) expand the single-family rental portfolio, (3) pursue strategic water and land acquisitions, and (4) return capital via share repurchases.

Share Repurchase Program

Pure Cycle has authorized an open-ended repurchase program for up to 200,000 shares. As of the most recent disclosure, the company has repurchased approximately 95,426 shares at an average price of $10.22, with 104,574 shares remaining under authorization. Management has stated publicly that it believes shares “remain considerably undervalued - maybe more than ever given our momentum.” This is not empty rhetoric; they are buying in the open market with shareholder capital at current prices.

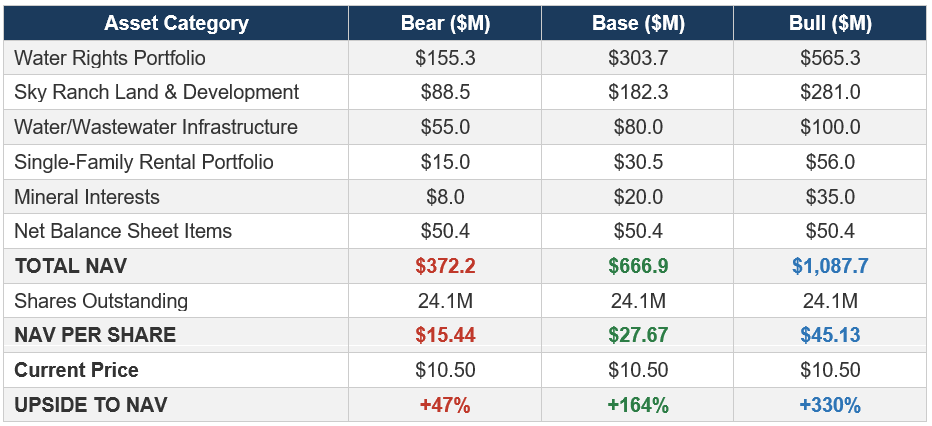

DETAILED NET ASSET VALUE ANALYSIS

The central thesis is that PCYO’s market capitalization dramatically understates the replacement cost and market value of its underlying assets. The following NAV is constructed on an asset-by-asset basis across bear, base, and bull scenarios.

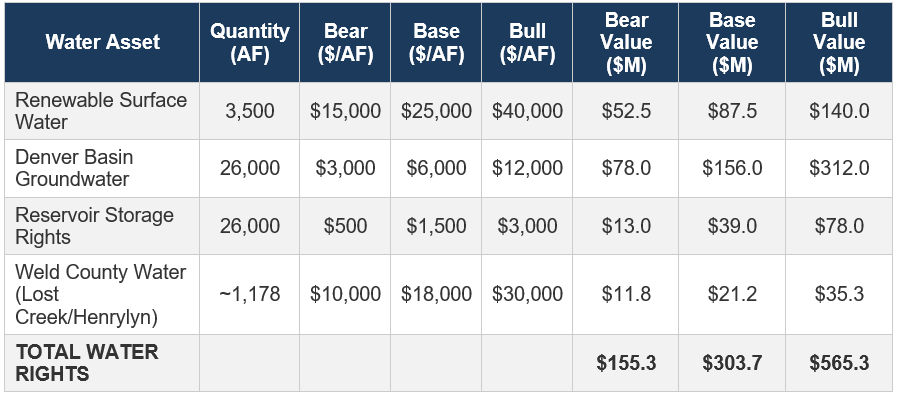

1. Water Rights Portfolio (29,500 AF + 26,000 AF Storage)

Valuation Basis: Colorado Front Range water rights represent one of the most actively traded and well-documented water markets in the western United States. Colorado-Big Thompson (C-BT) units - the benchmark for Front Range municipal water - spiked from ~$15,000/AF in 2013 to $67,000/AF in 2024 before settling around $60,000/AF. At auction in 2024, units sold for ~$52,000/AF. The City of Aurora paid approximately $10,240/AF for 7,500 AF of Arkansas River water rights. Municipal water brokers report that single-family home equivalent water in Denver metro growth areas has risen from $30,000/AF to $60,000/AF since 2017.

Pure Cycle’s water is not C-BT transbasin water (which carries Colorado River Compact risk); it is locally sourced Denver Basin groundwater and Lowry Range surface water - drought-proof, already adjudicated, and located proximate to end-use customers. This local sourcing and existing infrastructure arguably commands a premium to remote agricultural transfers that require court approval and infrastructure buildout. However, we apply conservative discounts given that the full 29,500 AF portfolio will be monetized over decades through tap fees rather than sold in a single transaction.

Of the 29,500 AF, approximately 26,000 AF is deep Denver Basin groundwater (depletable over 100+ year horizons but adjudicated and legally available) and ~3,500 AF is renewable surface water. The 26,000 AF of reservoir storage is a separate but complementary asset enabling seasonal balancing and drought resilience.

Key Assumptions: Renewable surface water is valued at a significant discount to C-BT market prices ($52,000–67,000/AF) because it requires existing infrastructure rather than transferable units. Denver Basin groundwater is valued far below surface water due to its depletable (though very long-lived) nature; the bear case uses replacement-cost-of-alternatives methodology, while the bull case approaches the marginal cost of new municipal water supply. Reservoir storage is valued as option value - the right to store water is distinct from the water itself. The recently acquired Weld County water (432 acres + 678 AF of ditch and designated basin water for $5.4M) provides a near-term comparable at approximately $8,000–10,000/AF inclusive of land.

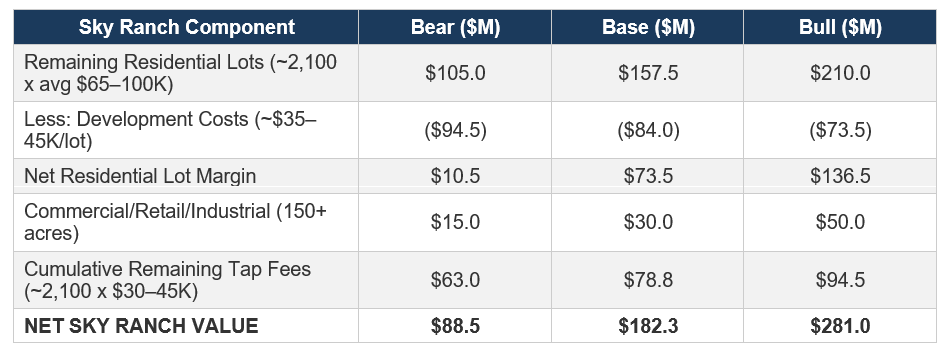

2. Sky Ranch Land & Development (930 Acres)

As of the latest reporting, roughly 1,100+ lots have been delivered across Phases 1, 2A, 2B, and 2C, with 2D and 2E under development. The remaining developable acreage accommodates approximately 2,000–2,300 additional residential units plus 150+ acres of commercial/retail/industrial zoned land. Lot sales have generated approximately $16M in annual revenue at current run rate, with gross margins in the 40–50% range.

These estimates capture remaining undeveloped value only. Cash already collected from Phase 1/2A/2B/2C lot sales and tap fees is reflected in the balance sheet (cash, receivables, infrastructure assets).

3. Water & Wastewater Infrastructure

The company carries $60–65 million of investments in water and water systems on its balance sheet (net of depreciation), including 11 groundwater wells, 15+ miles of distribution pipeline, three alluvial wells, 150 AF of surface storage, two wastewater reclamation facilities, and the recently completed $10M state-of-the-art Sky Ranch water reclamation facility. Replacement cost of this infrastructure significantly exceeds book value, but we use book as a conservative floor.

4. Single-Family Rental Portfolio

Currently 14 homes completed and rented, with 200+ lots reserved for the BTR program. At full buildout, this portfolio could comprise 200+ homes in the $350,000–450,000 construction cost range, generating $3,000–4,000/month in gross rent per unit. At institutional BTR cap rates of 5–7%, this portfolio at maturity could be worth $60–100+ million.

5. Mineral Interests (~10,000+ Net Acres)

The mineral portfolio includes over 10,000 net mineral acres, with the most productive ~700 acres in the Niobrara Formation. At a conservative $500–2,000/net mineral acre (typical for Wattenberg/DJ Basin non-operated royalty interests), plus the PV of existing and probable future royalty streams:

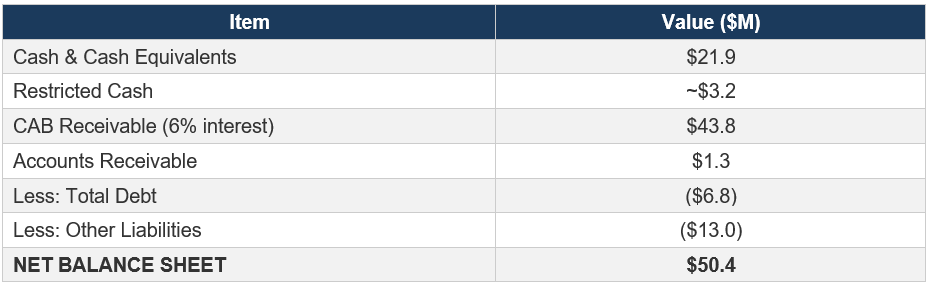

6. Balance Sheet Items

The $43.8 million CAB (Capital Assessment Bond) receivable is a particularly noteworthy asset - it represents approved public improvement reimbursements from the Sky Ranch metropolitan district, bearing 6% interest. This is essentially a government-backed receivable that will be repaid through property tax assessments as Sky Ranch builds out.

CONSOLIDATED NET ASSET VALUE SUMMARY

Even in the bear case, which applies deep discounts to every asset category, NAV per share exceeds the current stock price by nearly 50%. In the base case, NAV is roughly 2.6x the current market price. The bull case, which values water rights at levels still below the marginal cost of new municipal supply on the Front Range, implies more than 4x upside.

WHAT IS THE MARKET MISSING?

1. Water Rights Are Invisible on the Balance Sheet

Under GAAP, Pure Cycle’s water rights are carried at historical cost (the amount paid decades ago to adjudicate and develop them, net of amortization), which bears no resemblance to their current market value. The company invested ~$70 million over decades to adjudicate 30,000+ acre-feet of water rights that would cost hundreds of millions - potentially over a billion dollars - to replicate at today’s Front Range prices. The book value of “investments in water and water systems” is approximately $60–65 million; the market value of the water rights alone is multiples of this. Screeners and quantitative models that rely on GAAP book value see a $142.7 million equity company trading at 1.7x book. They do not see a company whose water rights alone may be worth $300–565+ million.

2. No Analyst Coverage, Micro-Cap Neglect

PCYO has virtually no sell-side analyst coverage. The company has a market cap of ~$253 million, average daily volume of only ~45,000–50,000 shares, and 39–44 employees. It falls below the radar of institutional investors who cannot build meaningful positions without moving the stock. The few quantitative screens that capture it misclassify it as a slow-growth regulated utility rather than what it actually is: a capital-light asset monetization vehicle sitting on a scarcity asset that is appreciating at double-digit annual rates.

3. The Tap Fee Flywheel Is Accelerating

Every lot sold at Sky Ranch generates revenue three ways simultaneously: lot sale proceeds, a one-time tap fee ($30,000–45,000+), and a permanent recurring water/wastewater connection ($1,500+/year). As development accelerates through multiple concurrent phases (2C, 2D, 2E now overlapping), the compound effect of one-time plus recurring revenues creates a flywheel that grows the earnings base faster than the lot count alone would suggest. With 60,000 SFEs of water capacity, Sky Ranch’s ~3,400 residential units consume less than 6% of the total water portfolio - the other 94% represents decades of future monetization runway through additional development, third-party wholesale, and water sales.

4. Water Scarcity Is Structural and Worsening

The Colorado Front Range is the most active, high-priced water market in the country. Population growth of roughly 80,000–100,000 people per year is colliding with a fixed and over-appropriated water supply. Colorado-Big Thompson water prices have risen from ~$15,000/AF in 2010 to $60,000–85,000/AF at peak auctions. The Colorado River Basin remains in a structural deficit, with combined Lake Mead and Lake Powell storage near historic lows. The post-2026 Colorado River operating guidelines are under active negotiation with no resolution, creating additional uncertainty for Colorado’s transbasin diversions. Pure Cycle’s locally sourced, drought-proof groundwater is immune to compact calls on the Colorado River - a critical distinction that few investors appreciate.

5. Data Centers as a Water Demand Shock

The explosive growth of hyperscale data centers - driven by AI infrastructure buildout - represents a new structural demand driver for water in areas with transmission infrastructure but limited water supply. A single large data center can consume 1–5 million gallons of water per day for cooling. The Denver metro area and eastern Colorado I-70 corridor are active data center markets. Pure Cycle’s combination of available water supply, existing transmission infrastructure, and large undeveloped acreage within the Rangeview service area positions it as a potential water supplier to data center developments - an optionality the market assigns zero value to today.

LONG-TERM UPSIDE CATALYSTS

Sky Ranch Buildout Completion (3–7 years): Delivery of remaining ~2,100+ residential lots plus commercial parcels could generate $150–250+ million in cumulative lot sale and tap fee revenue, with each phase de-risking the next and adding permanent recurring water customers.

BTR Portfolio Scale (5–10 years): Ramping from 14 to 200+ rental homes creates an embedded REIT generating $7–10+ million in annual rental income. At institutional cap rates, this portfolio alone could approach or exceed the current market cap.

Lowry Range Development (5–15+ years): Pure Cycle holds the exclusive water service agreement for 24,000 acres of the Lowry Range. As Denver continues to expand eastward, development of even a fraction of this acreage could generate hundreds of millions in incremental tap fee and service revenue over decades.

Water Rights Appreciation (Ongoing): If Front Range water prices continue their historical trajectory (C-BT units have compounded at ~12–15% annually from 2010–2024), Pure Cycle’s water portfolio appreciates in value every year without the company doing anything. This is the Michael Burry farmland-water thesis in its purest form: own the water, wait.

Third-Party Water Wholesale Expansion: The company can sell or lease excess water capacity to neighboring communities, developers, and industrial users who cannot source their own. The Weld County acquisition (October 2024: 432 acres + 678 AF for $5.4M) signals management is actively acquiring additional water rights to expand the service footprint.

Data Center / Industrial Optionality: The combination of water supply, I-70 corridor location, transmission infrastructure, and available land makes Pure Cycle a potential infrastructure partner for data center or industrial campuses in the eastern Denver metro. This is a free call option embedded in the equity.

Potential Acquisition Target: A larger water utility, infrastructure fund, or land developer seeking Front Range water assets would find Pure Cycle’s integrated portfolio extremely difficult and expensive to replicate. At current valuation, the company is arguably worth more in pieces than as a whole - the water rights alone justify the enterprise value before accounting for any operating earnings.

KEY RISKS

Housing Market Cyclicality

Sky Ranch lot sales are directly tied to national homebuilder demand, which is sensitive to mortgage rates, consumer confidence, and economic conditions. A severe recession or sustained mortgage rate elevation could slow lot absorption and delay development timelines. Mitigant: Sky Ranch targets the most resilient market segment (entry-level, $350–450K homes in a metro where median prices are much higher), and Pure Cycle’s just-in-time lot delivery model allows it to pace development to match demand rather than speculating on future absorption.

Groundwater Depletion Risk

Approximately 26,000 AF of Pure Cycle’s portfolio is deep Denver Basin groundwater, which is depletable over 100+ year horizons. Unlike renewable surface water, this supply is being slowly drawn down. Mitigant: The groundwater is legally adjudicated and available under Colorado water law; the company’s conjunctive use strategy pairs groundwater with renewable surface water, reclaimed water reuse, and storage to maximize sustainability; and the total portfolio far exceeds near-term customer demand.

Regulatory and Political Risk

Changes to Colorado water law, environmental regulations, or local development approvals could affect the company’s ability to develop and monetize its water and land assets. State-level actions on groundwater management (analogous to California’s SGMA) could alter the framework for Denver Basin aquifer usage. Mitigant: Pure Cycle’s water rights are already adjudicated through Colorado water courts, providing strong legal protection; the company has operated within this regulatory framework for 35+ years.

Concentration Risk

Essentially all current revenue generation is concentrated in a single master planned community (Sky Ranch) in a single county (Arapahoe) in a single metro area (Denver). Any localized economic, environmental, or regulatory disruption to this geography disproportionately impacts the company. Mitigant: The Lowry Range service area (24,000 acres) and Weld County water acquisitions diversify the geographic footprint; the water rights portfolio is serviceable across the broader southeastern Denver region.

Key Man Risk

Mark Harding has been the driving force behind every significant strategic decision since 1990. His departure without a credible succession plan could create uncertainty. Mitigant: The asset base is now self-sustaining - water rights, adjudicated decrees, infrastructure, and entitled land do not depend on any single individual. CFO Marc Spezialy (joined 2023) provides institutional depth.

Liquidity Risk

Average daily trading volume of ~45,000–50,000 shares means that institutional-size positions are difficult to accumulate or exit without material market impact. This is a feature for patient capital (the illiquidity discount contributes to the mispricing) but a genuine risk for investors who may need to liquidate quickly.

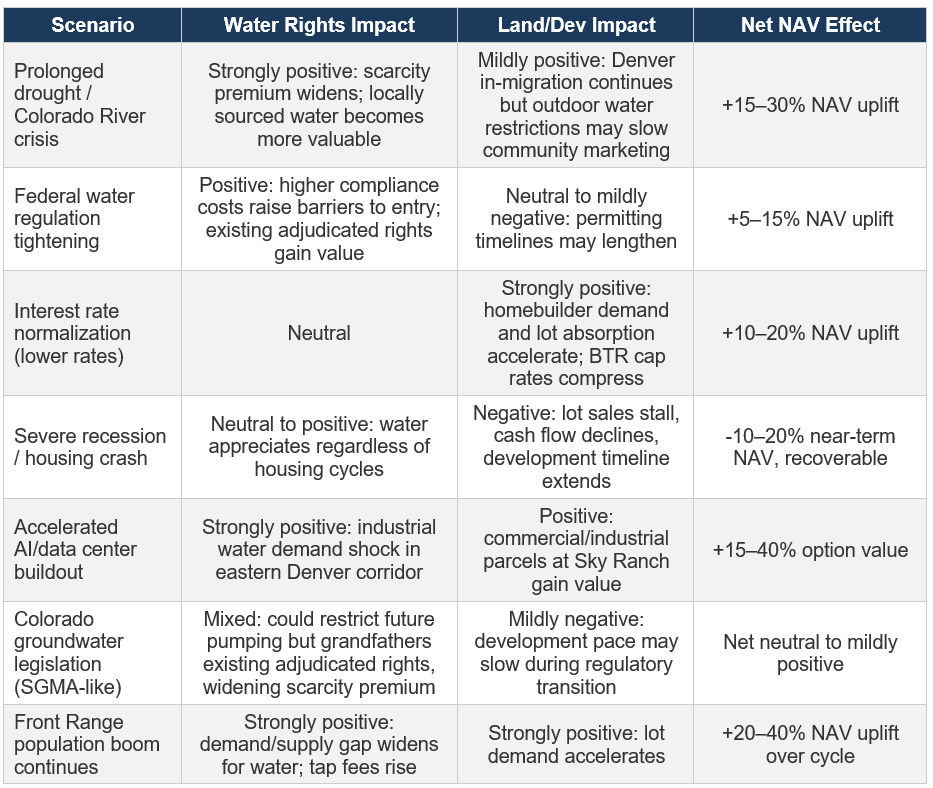

MACRO SCENARIO ANALYSIS: WATER, CLIMATE & ECONOMIC IMPACTS ON NAV

The critical takeaway is that most macro scenarios are neutral-to-positive for the water rights portfolio, which constitutes the largest component of NAV. Water is a consumable commodity with no substitute, inelastic demand, and a supply that is fixed by geology, hydrology, and legal decree. Economic downturns slow the pace of monetization but do not impair the underlying asset. Climate stress, population growth, and industrial demand shocks all tighten the supply-demand balance and increase the value of existing rights. The asymmetry is remarkable: the downside is tempo risk (slower monetization), while the upside includes permanent appreciation of a scarce resource.

CONCLUSION

Pure Cycle Corporation is a rare asset: a publicly traded, vertically integrated water and land franchise controlling one of the largest private water portfolios on Colorado’s Front Range, led by a 35-year owner-operator, generating consistent profits and free cash flow, carrying minimal debt, and trading at a dramatic discount to the replacement cost of its assets. The market classifies it as a boring micro-cap utility and ignores it accordingly.

But PCYO is not a utility. It is a water rights portfolio with embedded land development, rental, and mineral royalty monetization vehicles. Every lot delivered at Sky Ranch is a one-time revenue event that creates a permanent annuity (water service revenue) while consuming less than 6% of total water capacity. The other 94% - tens of thousands of acre-feet of adjudicated water in the most water-stressed, fastest-growing metro corridor in the western United States - sits waiting to be monetized across an arc of decades.

At $10.50 per share, you are paying roughly $253 million for an asset base that conservatively generates $13+ million in annual net income (growing), sits on $50+ million of net balance sheet value, and controls water rights whose replacement cost alone ranges from $155 to $565+ million depending on the methodology. The implied price per acre-foot of water in the current market cap - after subtracting all other assets at book value - is approximately $3,000–5,000/AF. Front Range water trades at $10,000–67,000/AF.

The dislocation is clear. The catalyst timeline is measured in quarters and years, not decades. And the asset is appreciating every day you wait.