Limoneira (LMNR): Priced Like a Lemon

The market sees a money-losing lemon grower. Hidden underneath is a California land-and-water portfolio worth multiples of the current price.

There are two ways to look at Limoneira. The first is the way a stock screener looks at it: a sub-$250 million agribusiness that lost $20.4 million in operating income in fiscal 2025, watched revenue fall from $191.5 million to $159.7 million, suspended its dividend, and let net debt climb. On that view, LMNR is a melting ice cube and you shouldn’t touch it.

The second is the way a private-market buyer looks at it: a company that has assembled, over 132 years, an irreplaceable portfolio of Ventura County dirt and senior California and Colorado River water, plus a half-interest in one of the few large residential developments that has actually cleared entitlement in Southern California this decade. On that view, the assets are worth two-and-a-half to four times the market capitalization, and management is in the middle of methodically turning them into cash.

Both views are correct. That is precisely the opportunity. The income statement and the balance sheet are telling opposite stories, and the market has chosen to believe the income statement. Our work says the balance sheet wins, the catalysts to prove it are already in motion, and the downside is protected by hard, salable assets that the company is selling, in public, at or above our marks.

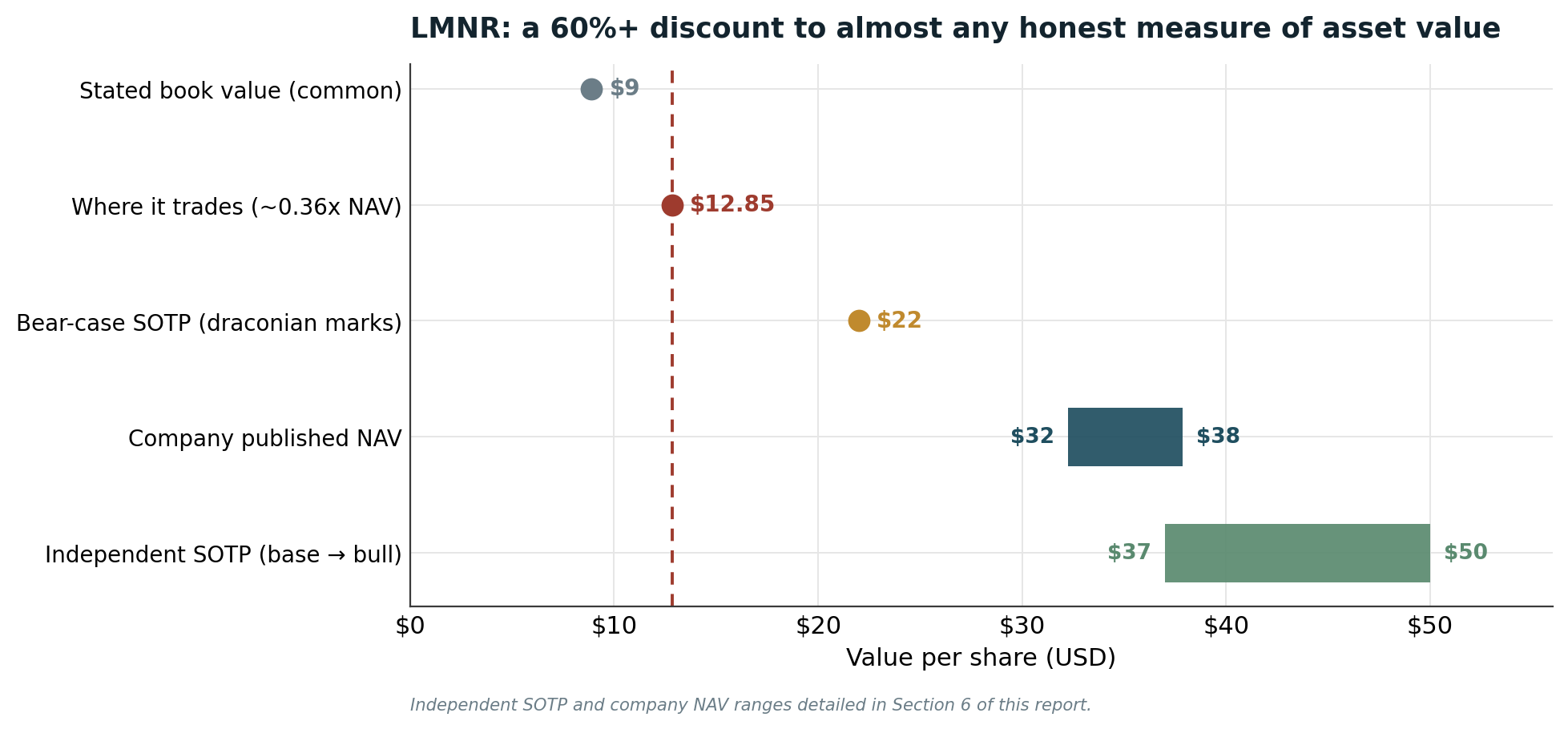

Limoneira owns roughly 7,000 acres of California farmland, ~21,000 acre-feet of senior and adjudicated water rights, a half-interest in a 2,050-home master-planned community now throwing off cash, and 550-plus acres of entitled and near-entitled development land. The company itself publishes a sum-of-the-parts net asset value of $556–656 million, or $32.23–$37.88 per share (as of October 2025). The stock trades at $12.85. You are being offered the assets at roughly 36 cents on the dollar of the company’s own appraisal - and, as we will show, that appraisal is itself sandbagged.

2. Invert the business: a water bank with citrus stitched to the front

The most useful mental model for Limoneira is to turn it upside down. Do not start with the lemons. Start with the land and the water, and treat the farming operation as a low-return overlay that happens to generate enough cash to carry the assets while you wait. Trees are a renewable, replaceable, commoditized crop. The dirt under them in coastal Ventura County, and the adjudicated water rights attached to it, are neither renewable nor replaceable. California has not adjudicated a major new coastal groundwater basin in living memory, and it is not zoning new farmland into existence. Limoneira is, functionally, a closed-end fund of scarce Southern California hard assets that trades at a 64% discount to net asset value and pays you to wait by farming.

The rest of this article does the dirty work: it values each asset against real, recent, third-party transactions, nets out the debt and preferred, and then explains, line by line, why the NAV gap exists and what closes it.

3. History: 1893 to the slow-motion liquidation

Limoneira (“the place of the lemon”) was founded in 1893 in Santa Paula, in the Santa Clara River Valley of Ventura County. For more than a century it operated as a sprawling private agricultural partnership, accumulating land, water rights, and shareholders. By 2010 it had more than 500 holders of record and was forced onto the NASDAQ to comply with SEC registration rules - it did not IPO to raise growth capital so much as to satisfy a regulator. That accidental, reluctant public listing is the original sin of the stock: LMNR has spent fifteen years as a public company without ever being managed like one, and total shareholder returns since 2010 have been poor.

The modern story begins in late 2023, when Peter Nolan - for seventeen years a managing partner at the buyout firm Leonard Green & Partners, now running his family office, Nolan Capital - bought roughly 1.1 million shares at $14.12 to $15.20, took a 6.1% stake, joined the board, and pushed CEO Harold Edwards to explore a sale. The company ran a formal strategic-alternatives process through 2024 and into 2025. It concluded in March 2025 with no transaction.

The resulting self-liquidation is slow-motion and tax-efficient - and it happens to be exactly what a disciplined control buyer would do with these assets if it had bought the whole at a discount:

• 2022: sold the Oxnard Lemon property and packinghouse for $19.1 million.

• 2023: sold roughly $100 million of Tulare County acreage to pay down debt.

• Aug 2025: bought up minority units of the Limco Del Mar partnership, lifting ownership from 28.8% to 54.5%, to control the entitlement of 221 acres of Ventura farmland for housing.

• Nov 2025: sold the Chilean ranches (Pan de Azúcar and San Pablo, ~500 acres lemons + 100 acres oranges) for ~$15 million, retaining a 47% interest in the Chilean packing/marketing business.

• Authorized: a $30 million share-repurchase program (March 2025); near-term sale pipeline of ~$40 million of land (Windfall Farms, Argentina) and $50–$70 million of water rights through fiscal 2027.

This is the behavioral tell. A management team that genuinely believed the operating business was the value would be reinvesting in lemons. Instead they are merging the citrus sales operation into Sunkist, shrinking the footprint, and converting hard assets to cash and buybacks. They are, in everything but name, liquidating into their own discount.

And the one director with both the most capital at risk and the clearest read on private-market value keeps buying. Nolan’s original 2023 stake went in at $14.12–$15.20. On January 2 and 5, 2026 - after the failed sale, after the FY2025 loss, and weeks before the dividend pause - he bought another 20,000 shares at a weighted ~$12.78, lifting his direct holding ~6.3%. He is adding below his own cost basis. A former buyout principal does not write personal checks into a melting ice cube; he writes them when he has seen the data room and concluded the discount is the opportunity.

4. Why the stock is at the lows: four optical disasters, zero asset impairment

To buy LMNR you have to understand precisely why it is cheap, because the reasons are the thesis. There are four, and all four are accounting or optics, not economics.

4.1 The alternate-bearing “trough illusion”

Avocado trees bear heavily one year and lightly the next - a biological certainty called alternate bearing. Fiscal 2025 was a deep “off” year. Fourth-quarter avocado revenue collapsed to $0.3 million from $8.9 million a year earlier; volumes fell to 396,000 pounds from 4.6 million. The avocado segment swung from $7.1 million of quarterly operating income to a loss. A screen running trailing numbers sees a business in free fall. The agronomy guarantees the snap-back - and it arrives just as 700–800 acres of non-bearing trees reach production.

4.2 The Sunkist revenue “cliff” that isn’t

In 2025 Limoneira merged its citrus sales and marketing function into Sunkist. The mechanical consequence is that roughly $27–$28 million of low-margin brokered-fruit revenue - third-party lemons that Limoneira merely passed through - now flows through Sunkist instead of across Limoneira’s income statement. First-quarter fiscal 2026 revenue accordingly “fell” from $34.3 million to $18.2 million. Headlines read “revenue down 47%.” In reality the company shed near-zero-margin pass-through volume and is keeping the margin-rich packing and grown-fruit business, with an expected ~$10 million of annual SG&A savings. This is margin-accretive surgery being scored as a demand collapse.

4.3 The dividend pause read as distress

In March 2026 the board paused the common dividend. Income and yield-oriented holders - a meaningful part of a small agribusiness’s shareholder base - sold mechanically. But the stated use of the freed cash is to fund avocado conversion (high-return replanting) and the Limco Del Mar housing entitlement, alongside the buyback. Pausing a ~2% dividend to fund 20%-plus internal projects is textbook capital allocation, not insolvency. The selling it triggered is price-insensitive and temporary; the value it funds is permanent.

4.4 Historical-cost accounting that hides the entire thesis

This is the deepest reason and the most durable edge. Property, plant and equipment sits on the balance sheet at $172.6 million net - but that figure carries Ventura County land acquired across more than a century at its original cost, in some cases pennies on today’s dollar. Land is not marked to market under GAAP. The 50% Harvest joint venture is carried inside a $72.2 million “equity in investments” line at equity-method cost, even though it is projected to distribute $155 million of cash over the next five years. The water rights are carried at essentially nothing. The result: stated book value is about $8.90 per share, the company screens as a serial money-loser, and the $30-plus of real, salable asset value per share is completely invisible to any model that starts from reported earnings or reported book. The accounting is the moat around the mispricing.

5. Sum-of-the-parts: the asset-by-asset build

We now value each asset against the most relevant arm’s-length evidence we can find, deliberately favoring transaction comps over models. Where the company has published a mark, we state it, then stress it in both directions.

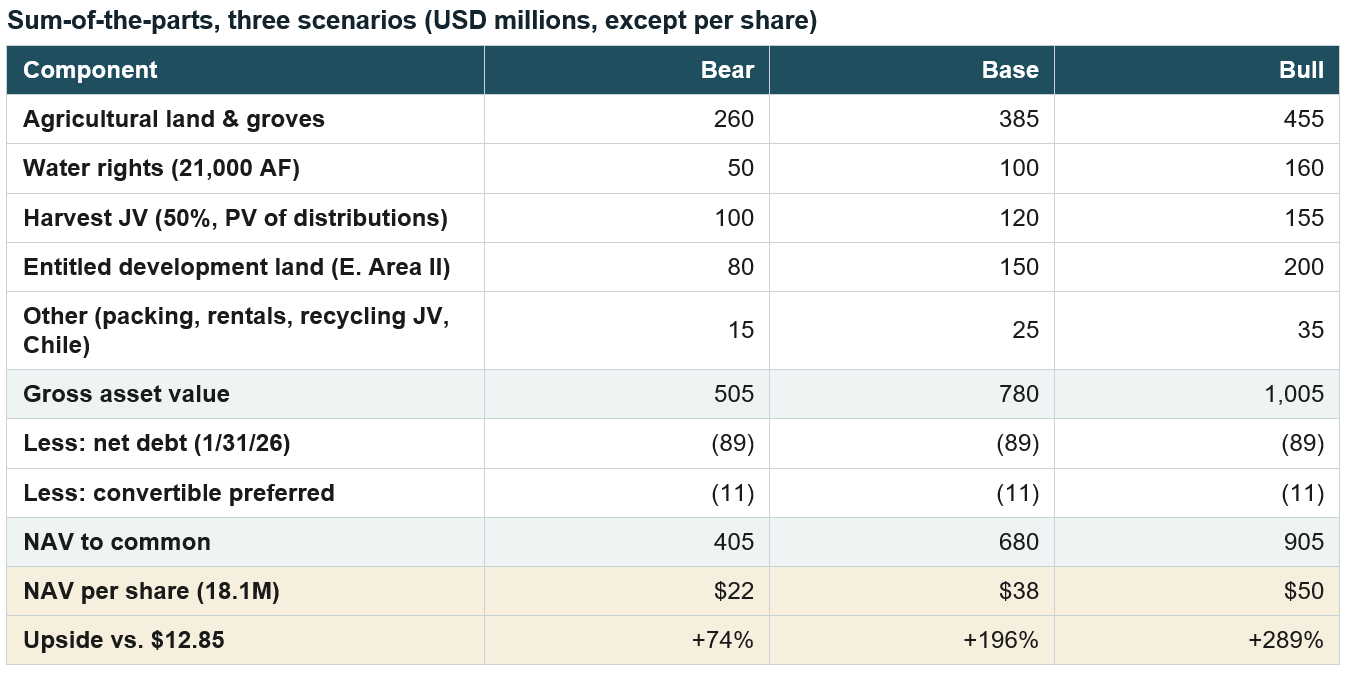

5.1 Agricultural land and groves - ~7,000 acres - base mark $385M

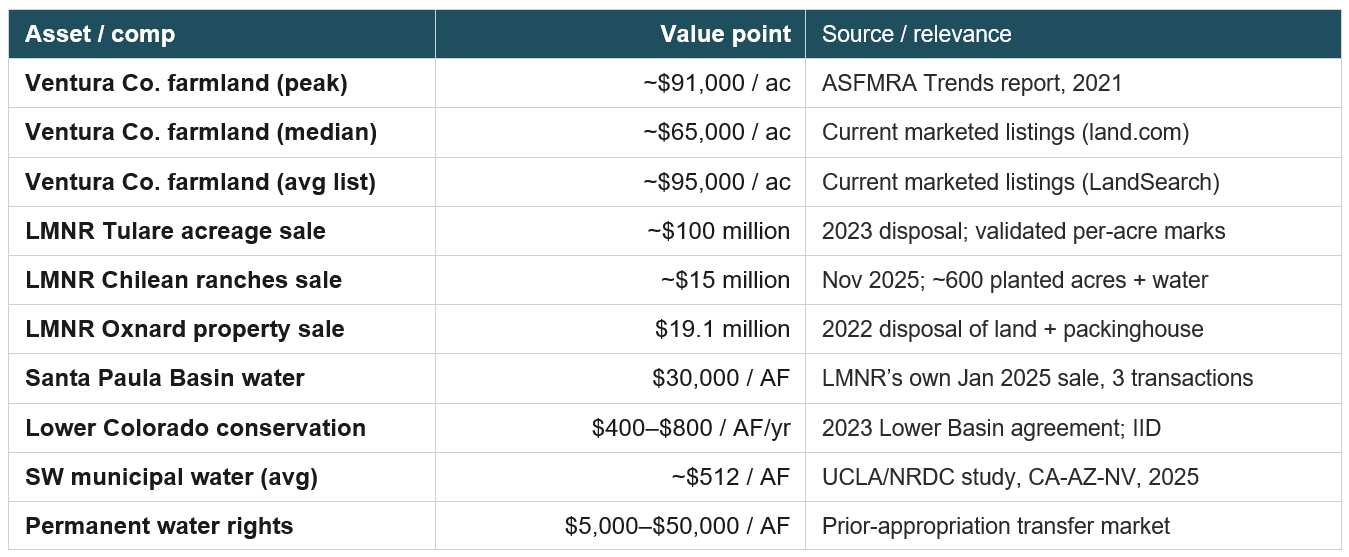

Limoneira owns approximately 7,000 acres of agricultural land, of which roughly 1,839 acres are planted to lemons, ~1,600 to avocados, ~1,062 to oranges, and ~403 to specialty citrus and other crops, concentrated in Ventura, Santa Barbara, and Tulare counties. The company carries these in its NAV at roughly $385 million, or about $55,000 per acre blended. That mark is not aggressive - it is conservative.

The comparable evidence on Ventura County citrus and avocado land:

• The American Society of Farm Managers & Rural Appraisers (ASFMRA) Trends report documented Ventura land values reaching ~$91,000 per acre by 2021.

• Current marketed farmland in Ventura County shows a median of ~$65,000 per acre (land.com) and an average listing price around $95,000 per acre (LandSearch).

• Premium coastal orchard parcels, where homesite value underpins the dirt, trade higher still.

Crucially, Limoneira’s own disposals validate the marks: it sold Tulare acreage for ~$100 million in 2023 and Chilean ranches for ~$15 million in 2025, both consistent with or above per-acre carrying values. Base case we accept $385 million (~$55k/acre); our bear case haircuts to $260 million (~$37K/acre, below distressed comps); our bull case marks to the county median across the better acres for ~$455 million.

5.2 Water rights - ~21,000 acre-feet - base mark $100M, and the most mispriced asset of all

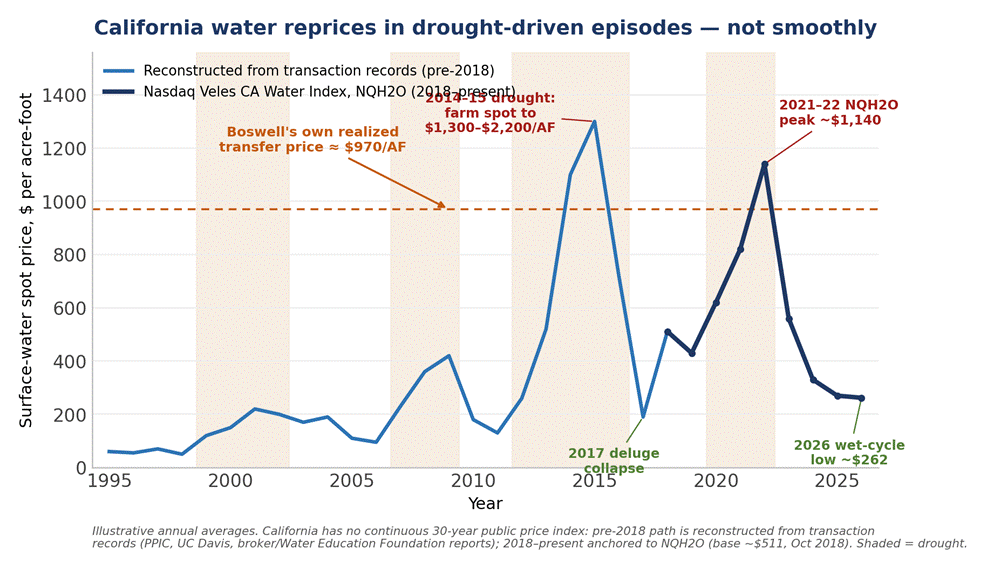

This is where the analysis gets interesting, and where Limoneira’s assets plug directly into the structural scarcity story playing out across the American Southwest. The company holds two distinct, premium water positions:

• Santa Paula Basin (adjudicated): 9,430 acre-feet of adjudicated rights, of which ~1,500 acre-feet are “conserved” and monetizable today without compromising farming. In January 2025 Limoneira sold pumping rights in this basin in three separate transactions at $30,000 per acre-foot - a price benchmarked to fees developers pay adjacent municipalities. That is a hard, recent, third-party mark.

• Colorado River Class 3 pumping rights: 12,000 acre-feet, of which ~7,280 acre-feet are conserved and monetizable. This is the Arizona-adjacent, Lower-Colorado position - the same water that data-center, power-plant, and municipal buyers across Arizona and the desert Southwest are now competing for.

The company values the combined conserved water at roughly $100 million and guides to $50–$70 million of monetization through fiscal 2027. Consider the asymmetry. The Santa Paula conserved volume alone, at the realized $30,000/acre-foot, is worth ~$45 million. The Colorado River conserved volume sits on top of a market where the 2023 Lower Basin agreement reset conservation payments to $400–$800 per acre-foot per year, where municipal buyers in California, Arizona, and Nevada pay an average of $512 and as much as $2,500-plus per acre-foot, and where permanent prior-appropriation rights trade at $5,000–$50,000 per acre-foot. The structural point made by every water economist studying the basin is the same: as compute, power, and population bid against alfalfa, every acre-foot must now justify its use - and the holder of senior, conserved, transferable rights is the seller into a rising market.

Limoneira gives you both halves of the water trade: a coastal-California, municipality-driven basin already printing $30,000/acre-foot, and a Lower-Colorado position that is a free call option on Southwest data-center and urban water demand. Even if every tree on the property were bulldozed tomorrow, the water underneath has a deep, growing bid. Base case $100 million; bear case $50 million (Santa Paula only); bull case $160 million as the Colorado position re-rates.

One corroborating fact deserves its own line. The director who has overseen Limoneira’s water assets since 2012, and who sits on its Risk Committee, is Scott Slater - the former president and CEO of Cadiz (NASDAQ: CDZI), author of California Water Law and Policy (the state’s leading treatise), and the lead negotiator of the largest conservation-based water transfer in U.S. history. There is arguably no person in the country better positioned to know what these specific rights are worth and how to monetize them.

Slater, too, has been an open-market buyer of the stock alongside Nolan (he bought 5,000 shares on January 8, 2026 at $12.85). When the single most qualified water-rights attorney in California is on the board and buying stock, valuing the water at essentially nothing is an error.

The CEO discussed water rights in their most recent earnings call (which had only two analyst questions):

“There are seven states now that are negotiating into who gets what in terms of a new water accord that’s put on the Colorado River. There continues to be quite a bit of turmoil between the states, and there’s been an inability to come up with an agreement for each of the seven states that is satisfactory.

With that being said, the amount of cuts that need to come off the river put Limoneira’s water rights into a position of being very, very valuable. How they monetize at this point is still a little bit unclear, although we do believe that there’ll be long-term fallowing programs that will be positioned for our advantage. We do expect to announce programs in the near term that we’ll be able to take advantage of that will bring value and allow that water from the Colorado River to be monetized in the near term.”

We discuss this dynamic in detail in our Water Rights Thesis and BWEL Thesis

5.3 Harvest at Limoneira - 50% JV - the $155M cash machine inside “equity investments”

In 2015 Limoneira contributed its East Area I land to a 50/50 joint venture (Limoneira Lewis Community Builders) with The Lewis Group, selling Lewis half for $20 million, to develop “Harvest at Limoneira,” a master-planned community in Santa Paula. The Santa Paula City Council has since increased the entitlement from 1,500 to 2,050 homes, plus 300 multifamily rentals in a separate Lewis venture. Through Phase 2 the JV has sold 1,261 homesites (Lennar alone bought 867), and Phase 2’s five new neighborhoods opened for sale in February 2026.

Limoneira expects $155 million of cash distributions from this JV over fiscal 2026–2030 (part of ~$180 million total across the Harvest, LLCB II, and East Area II programs over seven years). Against a ~$233 million market capitalization, a single joint venture is projected to return two-thirds of the entire market cap in cash within five years - yet it is carried at equity-method cost inside the $72.2 million “equity in investments” line, and the cash is back-end-weighted to 2027–2030, beyond the horizon of most investors looking at this name.

This back-loaded cash flow is exactly how master-planned communities are supposed to pay out: the capital-hungry work (land, grading, infrastructure, entitlement) is front-loaded, so the lots that sell in the later phases convert almost entirely to cash. The long-dated nature of the project has run past the average investor’s patience - right as the cash machine is turning on.

5.4 Entitled development land - East Area II and retained parcels - base mark $150M

Separate from the Harvest JV, Limoneira retains roughly 550 acres of currently entitled development land (East Area II and retained parcels east of Santa Paula) plus ~220 acres of near-term land-use-conversion land. The company values this collectively at ~$176 million; it sits on the balance sheet in “real estate development” at just $10.6 million. We haircut modestly to $150 million in the base case for entitlement and timing risk. The scarcity argument is clear: Ventura County’s SOAR growth-control ordinances make entitled residential land one of the rarest commodities in coastal Southern California, and Limoneira is one of a tiny number of entities positioned to convert agricultural land to housing at scale. The entitlement is the alpha.

5.5 Limco Del Mar - 221 acres - the 20-year option now in the money

Limoneira has wanted to build homes on the 221-acre Limco Del Mar ranch for two decades. In August 2025 it spent $5.6 million to lift its stake from 28.8% to 54.5% (booking a $2.9 million gain in the process) and began the entitlement process; management calls a three-to-five-year approval timeline “realistic and ambitious.” We carry Del Mar inside “other” as pre-entitlement optionality. If it entitles, it is worth a multiple of farmland value; if it does not, it remains productive citrus and avocado ground. Heads we win, tails we own Ventura dirt.

5.6 The operating agribusiness - a normalized-EBITDA cross-check

We deliberately value the land on an asset basis rather than capitalizing farm earnings, to avoid double-counting - the land mark already embeds productive capacity. But it is worth proving that the operating business does not subtract value. In the on-cycle fiscal 2024, adjusted EBITDA was $26.7 million. Fiscal 2025’s negative $6.5 million reflected the avocado off-year, ~$7 million of one-time Sunkist-transition and tree-removal costs, and farm-management contract loss. Normalize for the cycle, layer in the ~$10 million Sunkist saving, the avocado ramp (management projects 34 million pounds and a $30 million EBITDA uplift by 2030), and the $4–$5 million organic-recycling JV beginning in 2027, and a mid-cycle EBITDA of $25–$35 million is readily defensible.

That cross-check reframes the whole valuation: at $12.85, the ~$322 million enterprise value is roughly 11x a normalized $28–$30 million of EBITDA - a fair, unremarkable multiple for the farming and packing business on its own. You are paying a reasonable price for the operating company and being handed the $100 million water portfolio, the $155 million of JV cash, and 770 acres of entitled and near-entitled development land for nothing.

6. The NAV bridge and scenario table

Read the bear column twice. It marks the land below distressed comps, gives the Colorado River water essentially zero value, discounts the JV cash heavily, and still produces $22 of NAV - a 74% premium to the current price.

The bull case of $50 is not a stretch projection either: it simply marks the better acres to the Ventura County median, lets the Colorado River water re-rate toward the Southwest scarcity bid, and credits the JV at the gross PV of its contracted distributions - every input a documented comp, none of it heroic.

7. Comparable transactions: the marks are not theoretical

Every input above is anchored to an arm’s-length transaction, not a discounted-cash-flow guess. The table consolidates the evidence.

Two observations.

First, Limoneira’s own disposals (Tulare, Chile, Oxnard) print at or above the per-acre values we use, so the land marks are not aspirational - they are realized.

Second, the closest public-market analog is Alico (read our recent ALCO post), the Florida citrus company that is explicitly winding down groves and re-rating on land monetization; the parallel - a legacy citrus operator whose intrinsic value migrates from the crop to the dirt and water - is exact.

LMNR has not yet been re-rated for it. While we see plenty of value at ALCO’s current price, it has partially re-rated with the stock up ~60% over the last 18 months.

8. The debt: the bear’s best argument, addressed honestly

We will not wave this away, because it is the one part of the bear case with teeth. Net debt has gone the wrong way: from $40.0 million of long-term debt at fiscal year-end 2024, to $72.5 million at fiscal year-end 2025, to $89.9 million (and $88.6 million net) by January 31, 2026. Operating cash flow was negative $6.0 million in fiscal 2025. A money-losing company with rising leverage and a paused dividend is a legitimate thing to be cautious about, and the borrowings sit under an AgWest Farm Credit master loan agreement with debt-service-coverage, leverage, and debt-to-capitalization covenants that must be watched.

Three facts contain the risk:

1. The first quarter is the structural cash trough, amplified this year by the Sunkist transition that pushes revenue recognition into the back half. Management guides explicitly to a third- and fourth-quarter-weighted year.

2. The deleveraging inflection is imminent. The Harvest JV held $27.6 million of cash at the JV level as of January 2026 and is projected to distribute $155 million through 2030; ~$40 million of land and $50–$70 million of water are in the near-term monetization pipeline. Even crediting only the firmly-guided pieces, identified inflows of ~$245–$265 million dwarf the $89 million of net debt.

3. The debt is small against the assets. Net debt is ~13% of even the bear-case gross asset value and ~11% of base case. This is a lightly levered asset base experiencing a temporary operating-cash trough, not an over-levered one facing a solvency wall.

The rising-debt narrative is what is keeping the stock cheap right now, and it is the single data point a bear will cite. It is also the data point most likely to reverse hardest, because the offsetting cash flows are already under contract. If monetizations slip materially, the thesis is delayed, not broken - you still own the assets.

Two structural points deserve more weight than the headline leverage number, one comforting and one cautionary.

The comfort: the lender is AgWest Farm Credit, a Farm Credit System cooperative - a collateral lender, not a cash-flow lender. This is mortgage-style debt secured by farmland, underwritten against durable land value rather than against trailing EBITDA. Farm Credit System lenders are structurally patient through agricultural cycles precisely because their borrowers’ earnings are cyclical and their collateral is not; they are the antithesis of a covenant-light leveraged-loan syndicate that force-sells at the trough. With net debt at roughly 11–13% of gross asset value, the loan-to-value here is low-teens.

The caution: the covenant most exposed is the debt-service-coverage / fixed-charge test, not the leverage or debt-to-capitalization tests. Debt-to-capitalization is comfortable (debt is roughly a third of book capital) and asset coverage is strong, but a coverage covenant measured against EBITDA is the one that bites when EBITDA is negative. The realistic near-term risk is therefore not default but the need for a covenant waiver or amendment if the operating trough runs longer than guided or the monetizations slip past their dates. That is a manageable, relationship-driven outcome with a Farm Credit lender holding ample collateral - but it is a real cost and a real dependency, and the dividend, already paused, is no longer available as a lever if cash gets tight. The next levers would be accelerated asset sales (value-destructive if forced) or equity (dilutive at this price).

This is not a CCC/distressed credit - the asset coverage and the patient secured lender remove genuine near-term default risk - but it is not investment grade either, because the business cannot currently service its debt from operations and is reliant on asset sales to delever. “Asset-rich, cash-flow-poor, adequately secured” is the right one-line credit summary, and it is exactly the profile that produces a deeply discounted equity - the debt is money-good, the equity is where the cyclical risk and the asymmetric upside both sit.

9. The self-liquidating catalyst ladder

Unlike most NAV-discount stories, LMNR does not require a single binary event. It has a ladder of scheduled, largely contracted catalysts, any one of which forces a partial re-rate:

• FY2026–2030: $155 million of Harvest JV distributions, weighted to 2027–2030 ($35M / $41M / $32M / $42M).

• Through FY2027: $50–$70 million of water-rights monetization at benchmarked prices.

• By end FY2026 (Windfall): ~$40 million targeted from the Windfall Farms (Paso Robles) and Argentina disposals - though only Windfall carries firm end-of-fiscal-2026 timing in management’s guidance; Argentina is “advancing” without a hard date and may be the laggard.

• FY2027+: avocado ramp toward 34M lbs and ~$30M of incremental EBITDA; organic-recycling JV adds $4–$5M.

• 3–5 years: Limco Del Mar entitlement - a step-change in intrinsic value if approved.

• Ongoing: $30 million buyback authorization, retiring shares at ~0.36x NAV - the highest-return capital deployment available to management.

Add the contracted inflows and you get roughly a quarter-billion dollars of identified cash arriving over five years against a $233 million market cap. The company is, mechanically, going to return more than its entire market value in cash and asset sales while still owning the residual land, water, and operating business. The re-rate does not require a buyer; it requires the calendar to advance.

10. Risks and what would make us wrong

1. Execution and management quality. Post-IPO total returns have been poor; this team has a long history of value not translating to the stock. A board with Nolan and a buyback mitigate but do not eliminate this.

2. Realization timeline / value-trap risk. The assets are real but the cash is back-weighted. With no dividend today, you are paid only in eventual NAV convergence. If catalysts slip several years, the IRR compresses even if the thesis is “right.”

3. Leverage. If monetizations stall while operating losses persist, the AgWest covenants tighten and the company could be forced to sell assets on a worse timetable. Watch debt-service coverage each quarter.

4. Entitlement risk. Limco Del Mar and East Area II depend on Ventura County / Santa Paula approvals under restrictive growth-control regimes. Entitlement can be slow, conditioned, or denied.

5. Water monetization is capacity-limited. Only the “conserved” portion is salable without impairing farming; the headline 21,000 acre-feet overstates what can be sold near-term. Our base case already uses the conserved subset.

The disconfirming evidence we are watching: a quarter where land or water deals are pulled rather than delayed; a covenant breach or forced refinancing on worse terms; or a Harvest JV distribution materially below the published schedule. Absent those, the seasonal noise is just noise.

12. Conclusion

Limoneira is one of the cleanest expression we have found of a single, durable inefficiency: hard-asset value buried under historical-cost accounting and a cyclically depressed income statement, owned by a company that has finally started selling the assets to prove the point. The company itself says the parts are worth $32–$38 a share (as of October 2025). Our independent build, crediting the JV cash the company appears to exclude, lands at ~$38 base and $50 bull. A deliberately punitive bear case still clears $22. The stock is $12.85.

You are buying Ventura County dirt and senior Southwestern water at roughly a third of conservative appraised value, with a ~$250 million stream of asset-sale and JV cash scheduled to arrive over five years, a $30 million buyback retiring stock at 0.36x NAV, and the two most relevant insiders - a former buyout principal and the dean of California water law - buying the stock on the open market. The reported earnings are ugly and will stay ugly through the transition. The ugliness creates the opportunity.

Very thorough write up. Thank you

You think it is just the re-rating that is interesting? Or does the business have longer term potential to grow, beyond 2030?