J.G. Boswell Company (BWEL) | Part 1: OTC Stock with Billions in Water Rights

75%+ NAV Discount | Sleepy Family-Owned Company at Extreme Discount

J.G. Boswell Company is one of the most enigmatic and potentially undervalued securities in the American market. Trading on the OTC pink sheets with fewer than 1,000 shareholders, virtually no analyst coverage, and no SEC reporting requirements, Boswell operates in near-total secrecy while sitting atop what may be the single most valuable private collection of water rights and irrigable farmland in the Western United States.

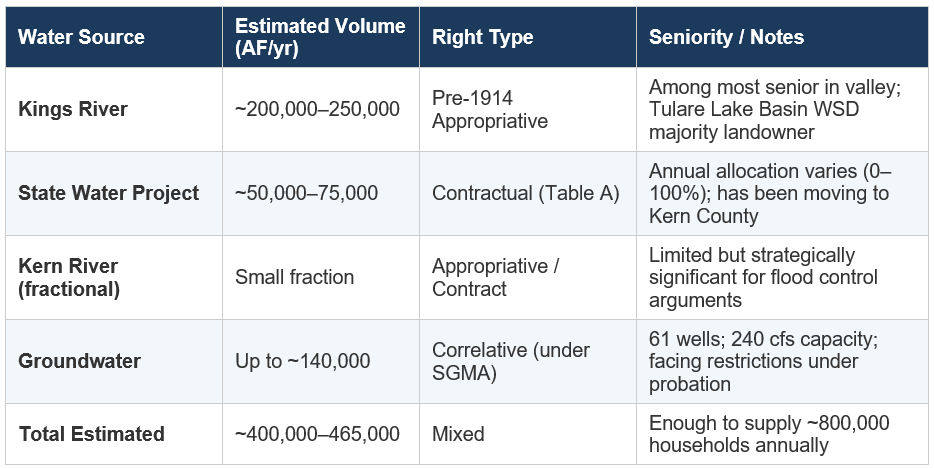

At a market capitalization of approximately $490 million, the company controls roughly 207,000 acres of land across Kings, Kern, and Tulare counties in California, including the vast majority of the former Tulare Lake bed - once the largest freshwater lake west of the Mississippi. Critically, Boswell holds an estimated 400,000 acre-feet of annual surface water rights through Kings River allocations, State Water Project contracts, and Kern River entitlements, supplemented by 61 wells capable of pumping up to 240 cubic feet per second. The water alone, at prevailing California transaction prices ($1,000–$10,000+ per acre-foot depending on right type and permanence), could be worth multiples of the entire market capitalization.

The thesis is simple: California’s structural water crisis is permanent and worsening. SGMA (the Sustainable Groundwater Management Act of 2014) will force up to 900,000 acres of San Joaquin Valley farmland out of production by 2040, while the Colorado River - which supplies Southern California’s 19 million residents - is in a 25-year megadrought with both Lake Mead and Lake Powell at dangerously low levels. In this environment, Boswell’s water portfolio is not merely valuable - it is irreplaceable. The company has already begun monetizing, having sold $47.5 million of Kings River water in 2015–2016 alone, exited its entire Australian operation (Auscott) for an estimated $800 million AUD combined, and shifted strategic focus to its core California assets. Management has publicly stated the pivot to “core agricultural businesses,” but the real game is water arbitrage on a multigenerational timescale.

Bear Case: $400–$500/share (~current). Base Case: $1,500–$2,500/share (3–5x). Bull Case: $3,500–$5,000+/share (7–10x). Water monetization, crop conversion, and catalytic management change could unlock extraordinary value over a 5–15 year horizon.

A Century of California Water: The Legal and Physical Architecture

The Doctrine of Prior Appropriation and Riparian Rights

Understanding Boswell’s moat requires understanding California’s peculiar water law, which blends two incompatible legal traditions. Riparian rights - inherited from English common law - grant landowners adjacent to a watercourse the right to reasonable use. Prior appropriation - the dominant doctrine of the arid West - grants rights to those who first diverted water and put it to “beneficial use,” regardless of land adjacency. The principle is encoded in the maxim: “first in time, first in right.”

California is a “dual doctrine” state that recognizes both systems. This creates a hierarchy: pre-1914 appropriative rights and riparian rights are the most senior, followed by post-1914 rights administered by the State Water Resources Control Board, followed by contractual rights to the State Water Project and Central Valley Project. In times of shortage, junior rights are curtailed first. Boswell’s Kings River rights are among the oldest and most senior in the San Joaquin Valley, dating to the company’s founding era in the 1920s and reinforced by subsequent dam construction, most critically the Pine Flat Dam built in 1954 on the Kings River.

The Colorado River Compact and the Law of the River

The Colorado River’s management is governed by what is known as the “Law of the River” - a labyrinth of more than 100 years of compacts, treaties, statutes, court decisions, and federal regulations. The foundational document is the Colorado River Compact of 1922, which divided the river between the Upper Basin (Colorado, Wyoming, Utah, New Mexico) and the Lower Basin (California, Arizona, Nevada), allocating 7.5 million acre-feet annually to each.

The compact was negotiated during an unusually wet period. Tree-ring studies have since revealed that the river’s long-term average natural flow is closer to 12–13 million acre-feet per year - not the 16.4 million the compact assumed. This structural over-allocation is the original sin of Western water management. California holds the most senior Lower Basin rights, with an allocation of 4.4 million acre-feet. The Imperial Irrigation District alone controls 3.1 million acre-feet - the single largest allocation on the river.

Key agreements governing the river are expiring at the end of 2026, and as of early 2026, the seven basin states remain at an impasse over post-2026 operating guidelines. Lake Mead and Lake Powell are each only about 31% full. Federal projections show that under dry scenarios, Lake Powell could drop below minimum power pool levels by late 2026, threatening hydropower generation at Glen Canyon Dam. The Bureau of Reclamation has stated it will impose its own plan if the states cannot reach consensus - a historically unprecedented step that underscores the severity of the crisis.

The State Water Project and Central Valley Project

California’s internal plumbing is equally critical. The State Water Project (SWP), the largest state-built water conveyance system in the country, moves Sacramento-San Joaquin Delta water south through the California Aqueduct to farms and cities in the San Joaquin Valley and Southern California. The Central Valley Project (CVP), a federal system, performs a similar function. Together they supply roughly 10–12 million acre-feet in wet years, but allocations have been dramatically curtailed during droughts - sometimes to zero for junior contractors. Boswell holds State Water Project contracts and has been a major recipient of SWP allocations, which it has increasingly moved to its highest-value lands in Kern County rather than using entirely in Kings County.

Climate Change and the Permanent Water Crisis

The Western water crisis is not cyclical - it is structural and worsening. The Colorado River basin has experienced its driest 25-year stretch in over 1,200 years. Scientists have identified this as an “aridification” rather than a drought, meaning the baseline climate is permanently shifting toward less available water.

Several reinforcing dynamics are at work. First, rising temperatures increase evapotranspiration, meaning that even when precipitation falls, more of it is absorbed into parched soils before reaching rivers and reservoirs. The Bureau of Reclamation estimates that the Colorado River has lost approximately 20% of its natural flow compared to the 20th century average, with continued declines expected. Second, the Sierra Nevada snowpack - California’s primary water storage mechanism - is shrinking and melting earlier. The snowpack functions as a natural reservoir, holding winter precipitation and releasing it gradually through spring and summer. Climate models project 25–40% reductions in average snowpack by 2050. Third, groundwater basins across the San Joaquin Valley have been critically overdrafted for decades. Land subsidence - the physical sinking of the earth’s surface caused by aquifer depletion - has exceeded 28 feet in parts of the valley. The city of Corcoran, surrounded by Boswell land, was threatened during the 2023 floods in part because its levee had sunk due to subsidence from excessive pumping.

The Colorado River negotiations illustrate the endgame. The river’s total supply has fallen to roughly 10–12 million acre-feet per year against roughly 15 million acre-feet of allocated demand. A report by the Colorado River Research Group aptly titled the situation “Dancing With Deadpool.” Arizona is already absorbing 18% cuts to its allocation. Nevada faces 7% cuts. California has avoided cuts thus far due to its senior rights, but even California’s agricultural users - particularly in the Imperial Valley - are facing pressure to conserve.

The implication for Boswell is profound: as total water supply in California contracts, the value of the water that remains - particularly senior surface rights held by entities like Boswell - increases geometrically. Water is a zero-sum game. Every acre-foot that disappears from the system makes every remaining acre-foot more valuable.

SGMA: The Catalyst That Changes Everything

The Sustainable Groundwater Management Act, signed by Governor Jerry Brown in 2014, is the most significant piece of water legislation in California history. For the first time, it requires sustainable management of the state’s groundwater basins, mandating that critically overdrafted basins reach sustainability by 2040. The implications are seismic.

The Public Policy Institute of California estimates that up to 750,000–900,000 acres of farmland in the San Joaquin Valley will need to be permanently fallowed to comply with SGMA - an area roughly the size of Rhode Island. Many of these acres are farmed by operations that are 100% dependent on groundwater and have no surface water entitlements. Under SGMA, these farmers face dramatic pumping restrictions: from approximately 3 acre-feet per acre historically, down to as little as 0.15 acre-feet in the most restricted zones.

In April 2024, the State Water Resources Control Board took the unprecedented step of placing Kings County groundwater managers on probation - the first step toward state takeover of the Tulare Lake groundwater basin. The basin serves vast tracts of dairy, ranching, and farming controlled by Boswell and rival developer John Vidovich. Multiple rounds of groundwater sustainability plans have been rejected for deficiencies in addressing dried-up wells, contaminated water, and subsidence.

For Boswell, SGMA is transformative. As a holder of approximately 400,000 acre-feet of senior surface water rights, the company is positioned to be a net seller into the emerging California water market. Many farmers who lose groundwater access will have no choice but to purchase surface water from those who have it. Groundwater trading platforms are already being developed, and several water districts have begun facilitating formal water markets. The Rosedale-Rio Bravo Water District in Kern County launched an open-source trading platform for groundwater in 2020, and similar systems are expanding across the valley.

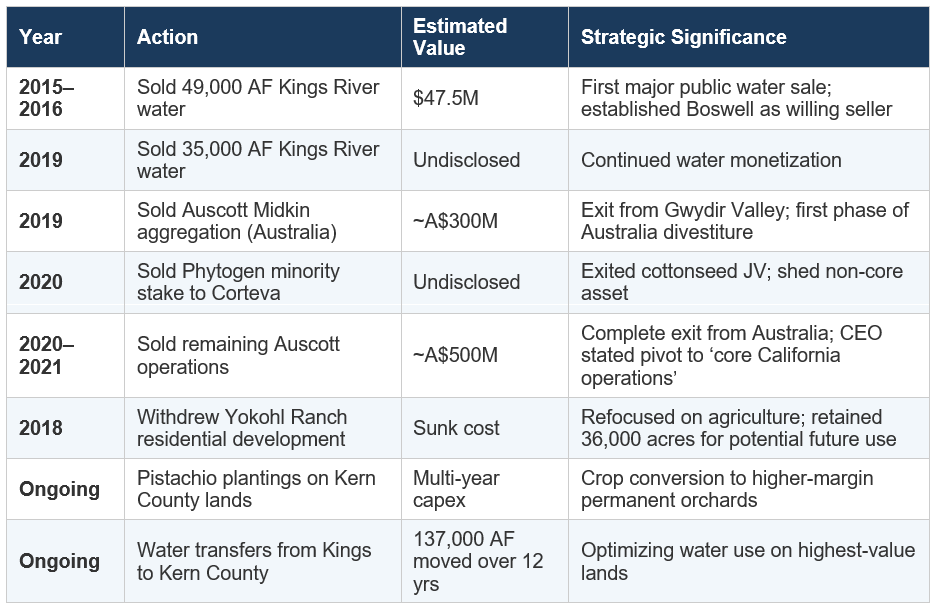

Boswell has already demonstrated willingness to sell water. According to records obtained by SJV Water, the company sold 49,000 acre-feet of Kings River water out of Kings County for $47.5 million in 2015–2016 (roughly $970 per acre-foot), and another 35,000 acre-feet in 2019 for an undisclosed sum. Over a 12-year period ending in 2021, Boswell moved 102,000 acre-feet of surface water out of Kings County. In FY2020, the company contracted to sell 100,000 acre-feet. These transactions, while large, represent a fraction of the company’s total entitlements.

Why Boswell Is Irreplaceable: The Asset Base

Land Holdings

The Boswell family, as ranked by The Land Report in January 2026, controls approximately 207,000 acres - placing them as the 81st largest private landowner in the United States. The core California footprint includes roughly 132,000 acres in Kings County, 23,000 acres in Kern County, and 3,700 acres in Tulare County, plus the 36,000-acre Yokohl Valley Ranch in Tulare County (formerly planned as a master residential community, now used for cattle grazing). The company owns the vast majority of the former Tulare Lake bed, which at its peak was the largest body of freshwater west of the Mississippi, fed by the Kings River, Kaweah River, Tule River, and Kern River.

The Lake bed’s value is multidimensional. The clay-bottomed lakebed sits atop an impervious layer that historically made it ideal for cotton (which tolerates saline soils). It also means the land functions as a massive natural flood basin - a critical function as climate change increases the volatility of Sierra Nevada runoff. During the 2023 floods, the Army Corps of Engineers ordered the lakebed to serve as a relief valve for the Kings River, flooding large portions of Boswell’s acreage. The company’s control of levees and drainage infrastructure gives it enormous influence over which lands flood and which are protected.

Water Rights Portfolio

Political and Institutional Control

Boswell’s water rights are reinforced by a web of institutional positions that would be virtually impossible to replicate. The company maintains seats on nearly every agricultural and water-related board and commission in Kings County. Boswell is the majority landowner in the Tulare Lake Basin Water Storage District and a major rights holder in the Kings River Water Association. The company’s vice president and general counsel, Jeof Wyrick, chairs the El Rico Groundwater Sustainability Agency. This institutional control is not incidental - it is the product of a century of deliberate strategic accumulation.

As the U.S. Supreme Court affirmed in 1973, representation on the local irrigation district board is determined by the value of landowners’ land. Since Boswell owns the majority of land in its districts, the company effectively controls flood management, water allocation, and infrastructure decisions. This legal framework has survived constitutional challenge and remains intact.

How Boswell Can Monetize: Six Pathways to Value Realization

1. Direct Water Sales and Transfers

The most straightforward monetization path is selling surplus water. At the $970/AF price Boswell achieved in 2015–2016, selling 100,000 acre-feet annually would generate roughly $97 million in revenue - against a total market capitalization of $490 million. As SGMA forces more farmland out of production and demand intensifies, water prices in the San Joaquin Valley are expected to rise substantially. Desert groundwater agencies have already paid $8,500 per acre-foot for permanent rights. If Boswell were to sell even a fraction of its water portfolio at mid-range prices ($2,000–$5,000/AF), the implied value would dwarf the current market cap.

2. Permanent Water Rights Sales to Municipal Users

Southern California’s Metropolitan Water District serves 19 million people and has already banked 1.5 million acre-feet of Colorado River water in Lake Mead for dry years. As the Colorado River negotiations tighten supply, MWD and other urban agencies will increasingly seek permanent supply from Central Valley agricultural holders. A large-scale, long-term water supply agreement between Boswell and a Southern California agency could be worth billions.

3. Crop Conversion to Higher-Value Permanent Crops

Boswell has historically been defined by cotton and processing tomatoes. But a quiet revolution is underway. The company has been planting pistachios on higher-elevation Kern County lands outside the Tulare Lake flood zone. Pistachio grower Jim Valov publicly commented on the “massive” Boswell pistachio operation during the 2023 floods, noting that these orchards were safely above the floodwaters.

The economics of pistachios versus cotton are compelling. Mature pistachio orchards generate $3,000–$6,000 per acre in revenue (versus $500–$1,500 for cotton). They require less water per dollar of revenue, and they produce a globally exported commodity with robust demand growth, particularly from China. California produces 98% of all U.S. pistachios. However, the transition is not without risk - pistachio trees take 7 years to bear, pistachio prices have recently declined from a peak of $3.57/lb in 2014 to below $2/lb amid a surge in new plantings, and permanent crops cannot be fallowed in dry years the way annual crops like cotton can.

4. Solar and Renewable Energy Leases

The flat, sun-drenched Tulare Lake bed is ideally suited for solar energy development. As SGMA forces marginal farmland out of production, converting fallowed acreage to solar leases becomes economically attractive. Solar lease rates in the San Joaquin Valley range from $800–$1,500 per acre per year. If Boswell were to lease 20,000 acres for solar (a modest fraction of its holdings), annual lease income could reach $16–30 million with zero water consumption.

5. Groundwater Banking and Recharge

Boswell’s lands can serve as massive groundwater recharge basins during flood years. The impervious clay of the lakebed is a disadvantage for natural recharge, but the company’s higher-elevation parcels and canal infrastructure could facilitate managed aquifer recharge (MAR). Under SGMA, water agencies pay significant premiums for recharge capacity. Boswell could earn revenue by accepting flood flows and banking water underground for later sale.

6. Flood Storage and Environmental Credits

The 2023 Tulare Lake flooding demonstrated that Boswell’s lakebed is, whether the company likes it or not, the valley’s ultimate flood relief valve. Under a 1964 agreement, only 5,170 acres of Boswell’s 22,000-acre lakebed can be used for flood storage. Renegotiating this arrangement - potentially in exchange for payments from the Army Corps of Engineers or downstream beneficiaries - could transform a liability into a revenue stream. Environmental water markets, including payments for habitat restoration and wetland banking, represent an additional frontier.

Behind the Curtain: What Boswell Is Really Doing

The Quiet Monetization Playbook

While Boswell operates with extreme opacity, a pattern of actions between 2019 and 2026 reveals a coherent strategic direction. The company is systematically monetizing non-core assets and repositioning around its irreplaceable California water and land portfolio.

The pattern is unmistakable: Boswell is consolidating around California, converting lower-value annual crops to higher-value permanent crops, and selectively selling water when prices are attractive. The Australian exit alone likely generated $500–$600 million USD in total proceeds across both transactions, substantially exceeding the company’s entire market capitalization at the time.

The Water Monopoly Question

“Monopoly” is a loaded term, but Boswell’s position in Kings County approaches something like it. The company is the majority landowner in the Tulare Lake Basin Water Storage District. It holds the largest single share of Kings River water rights. Its representatives sit on multiple groundwater sustainability agencies. It controls the canal and levee infrastructure that determines how water flows through the region. Rival developer John Vidovich has publicly accused Boswell of selling its surface water out of the county while pumping additional groundwater to continue farming its Kings County acreage - effectively exporting the region’s most valuable resource while drawing down the common pool.

The Boswell-Vidovich rivalry is the defining water conflict in the modern San Joaquin Valley. Vidovich, a Bay Area developer who has assembled his own vast land and water portfolio through Sandridge Partners, has challenged Boswell on multiple fronts: a pipeline dispute that led to physical equipment blockades, lawsuits over Kings River water transfers, accusations of groundwater export, and competing claims before the State Water Resources Control Board. The two entities are on opposite sides of virtually every water proceeding in Kings County.

Whether Boswell’s position constitutes a “monopoly” is debatable, but it is unquestionably a form of resource dominance that would be impossible to replicate at any price. The assets were accumulated over a century, reinforced by legal, political, and institutional control, and now sit at the nexus of California’s most pressing resource crisis.

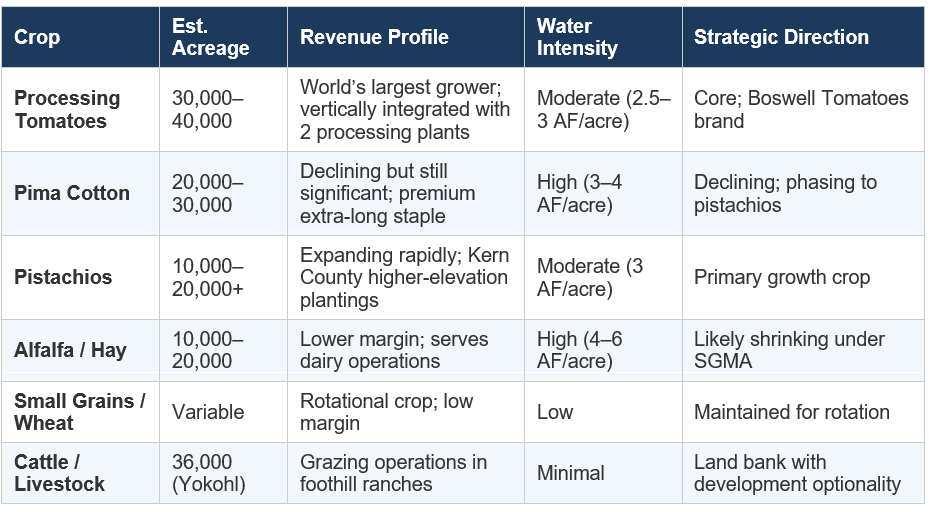

What They Grow Now: The Crop Portfolio in Transition

Boswell’s current agricultural operations span several product lines, though the company’s extreme secrecy makes precise acreage breakdowns difficult. Based on public sources, satellite imagery analysis, and agricultural reporting, the approximate crop mix is as follows:

The Pistachio Pivot

The shift from cotton to pistachios is arguably the most significant operational transformation in Boswell’s history. Cotton, the crop that built the Boswell empire, is increasingly uneconomic in California. The late J.G. Boswell II himself told The Wall Street Journal in 2000 that a farmer could make more money selling a water option than selling cotton. By January 2026, The Land Report described Boswell as “the largest producers of tomatoes in the world” - notably omitting cotton from the lead descriptor for the first time.

The pistachio shift makes strategic sense for several reasons. First, pistachios produce dramatically higher revenue per acre-foot of water consumed. Second, California’s Mediterranean climate gives it a near-monopoly on domestic production (98% of all U.S. pistachios). Third, global demand continues to grow, particularly in China, which has become the largest export market. Fourth, by planting on Kern County uplands outside the Tulare Lake flood zone, Boswell is insulating its highest-value crops from the flood risk that devastated the lakebed in 2023.

However, the transition carries risks. Pistachio trees are permanent crops that cannot be fallowed in dry years without killing them. Prices have dropped sharply from $3.57/lb in 2014 to below $2/lb as approximately 490,000 bearing acres are now in production statewide with another 40,000 coming online. The industry faces cyclical oversupply risk. Boswell’s competitive advantage lies in its water security: while overleveraged pistachio growers dependent on groundwater will be forced out under SGMA, Boswell can irrigate through any drought.

Management, Governance, and the Alignment Problem

J.G. Boswell Company is controlled by the fourth generation of the Boswell family. James W. Boswell serves as Chairman and CEO, with Cameron Boswell (his son) serving as Vice President of Administration. The family holds a controlling interest in the approximately 964,210 shares outstanding, with the stock trading at average daily volumes of a few hundred shares.

The governance structure is, to put it charitably, opaque. The company does not file with the SEC. It has fewer than 1,000 shareholders. It does not hold public earnings calls. It does not issue press releases. The only way to obtain an annual report is to be a shareholder. The family motto, as described in Mark Arax’s book The King of California, is: “As long as the whale never surfaces, it is never harpooned.”

Why Might Management Change?

Several forces could incentivize the Boswell family to unlock value, whether voluntarily or under pressure:

Generational Transition: J.G. Boswell II, the patriarch who built the modern empire, died in 2009 at age 86. His son, James W. Boswell, has run the company since. Cameron Boswell represents the fourth generation. Generational transitions in family-controlled companies often catalyze strategic change, estate planning pressures, liquidity events, or outright sales. The Boswell family’s 2019–2021 Australian exit - a $500–800M liquidation of a 58-year-old operation - suggests this process is already underway.

Estate Tax Pressure: With the stock at ~$510 per share, the family’s controlling interest is likely valued at several hundred million dollars for estate tax purposes. Given the illiquidity and complexity of the assets, there is strong incentive to either increase the public float, pursue a going-private transaction, or structure partial asset sales to generate cash for estate obligations.

SGMA Compliance Costs: The probationary status of the Tulare Lake groundwater basin creates real operational risk. If the state ultimately imposes pumping limits, Boswell faces the choice of reducing farming operations (and revenue) or investing heavily in surface water infrastructure and recharge. Selling water into the market may become more economically attractive than using it to grow cotton.

The Pistachio Capital Cycle: Planting pistachios requires significant upfront capital with 7-year payback periods. The Australian asset sales likely provided the cash to fund this conversion. If the conversion succeeds, Boswell’s per-acre profitability could increase 3–5x, potentially justifying a higher dividend or share buyback.

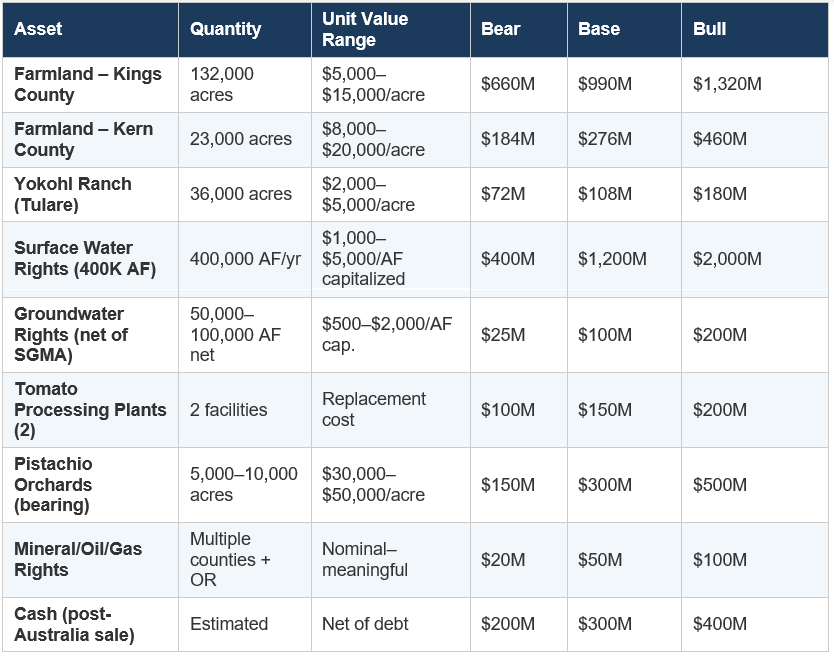

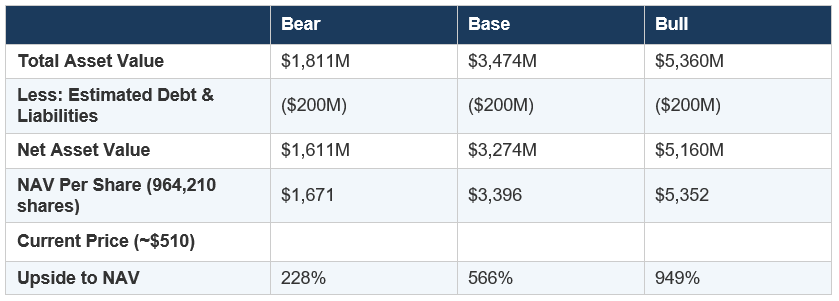

Valuation: A Sum-of-the-Parts Framework

Valuing Boswell requires a bottoms-up approach because the company reports no public financials. The following framework uses publicly available data, comparable transactions, and conservative assumptions.

The water rights are the single largest driver of the valuation gap. At the bear case ($1,000/AF capitalized value), the water alone is worth $400 million - roughly 80% of the entire market cap. At the base case ($3,000/AF), the water is worth $1.2 billion. At the bull case, which would reflect permanent transfers at prices already observed in California’s most water-stressed markets, the water could be worth $2 billion or more. Natural resources investor Rick Rule has publicly stated he believed BWEL shares were worth $3,500 each if the company stopped farming and simply sold water.

The 20-Year Dead Money Problem: Why the Stock Has Gone Nowhere

BWEL shares touched $1,200 in July 2014 and traded around $500–$575 as recently as mid-2025. As of early 2026, shares trade around $510. Over 20 years, the stock has essentially flat-lined. The reasons are structural, not fundamental:

No SEC Reporting: Without public financials, institutional investors cannot conduct due diligence to their fiduciary standards. No earnings, no balance sheet, no cash flow statement. This alone eliminates 95%+ of potential buyers.

Virtually No Liquidity: Average daily volume is roughly 500 shares, with many days seeing zero trades. The bid-ask spread is often $5–$10 wide. Institutions that manage hundreds of millions of dollars cannot build a meaningful position.

No Analyst Coverage: Zero sell-side analysts follow the stock. Seeking Alpha articles by individual investors are the only published analysis.

Family Control with No External Governance: Minority shareholders have no board representation, no say-on-pay vote, and no ability to pressure management for capital returns. The Boswell family runs the company as a private fiefdom that happens to have publicly traded shares.

No Catalyst Timeline: The water rights are valuable in theory, but without management willingness to monetize or distribute value, the assets can sit indefinitely at book cost (or below) on an invisible balance sheet.

Why This Time Could Be Different

Despite the dead money history, several structural factors are converging that did not exist previously:

SGMA is real and binding. Unlike previous voluntary conservation programs, SGMA has teeth: state probation, pumping fees, and potential state takeover of groundwater management. The 2040 compliance deadline creates a visible forcing function that did not exist before 2014.

The Colorado River compact is expiring. Post-2026 negotiations will almost certainly result in reduced deliveries to California’s agricultural users, further tightening the statewide supply-demand imbalance and increasing the value of every acre-foot Boswell holds.

Management has already begun selling. The 2019–2021 Australian exit, the Phytogen sale, and the water transfers represent a new posture from a family that historically hoarded assets. The stated pivot to “core California operations” is management’s way of saying: we’re concentrating the portfolio on what’s most valuable.

The pistachio conversion is a bet on permanent value. Planting 10,000+ acres of pistachios with a 7-year maturity represents a multigenerational commitment to generating higher returns from the same water. When these orchards mature (2025–2030), per-acre revenue could triple.

Climate change makes the thesis stronger every year. Every degree of warming, every dry winter, every foot of subsidence in the San Joaquin Valley makes Boswell’s senior surface water rights more valuable. Time is an asset for patient shareholders.

Risks

Governance / Value Trap: The single largest risk. Management has no obligation to unlock value, pay meaningful dividends, or provide transparency. The Boswell family could run the company as a tax-advantaged family office indefinitely. This is not a stock for investors who need a catalyst within 12–24 months.

Regulatory / Political Risk: California’s water politics are volatile. Future legislation could restrict agricultural-to-urban water transfers, impose additional environmental flow requirements, or change the priority structure of water rights. Boswell’s institutional control over local water boards could be challenged if the state takes over groundwater management under SGMA probation.

Flood Risk: The Tulare Lake bed floods. It flooded in 2023, it flooded in 1983, and it will flood again. When it does, tens of thousands of acres of crops are destroyed. Pistachio orchards in the flood zone would be a catastrophic loss. Boswell appears to be mitigating this by planting permanent crops on higher ground in Kern County, but the lakebed remains the core of the company’s footprint.

Pistachio Market Risk: The California pistachio industry has expanded from 100,000 bearing acres in 2001 to approximately 490,000 today, with another 40,000 coming into production. Prices have fallen below $2/lb from a $3.57 peak. A prolonged trade war or oversupply cycle could compress margins.

Liquidity: BWEL trades at average volumes of ~500 shares/day with wide bid-ask spreads. Building or exiting a position of any meaningful size could take months and could move the market.

Conclusion: The Permanent Long

J.G. Boswell Company is a generational asset disguised as a dead-money pink sheet. The company controls what is arguably the most valuable private portfolio of water rights and irrigable farmland in the Western United States, accumulated over a century by a family that understood the single most important truth about California: whoever controls the water, controls the future.

The structural forces converging on this asset - SGMA, the Colorado River crisis, climate aridification, Sierra Nevada snowpack decline, and the irreversibility of groundwater depletion - are not cyclical. They are permanent and accelerating. Every year that passes without a resolution to California’s water crisis makes Boswell’s portfolio more valuable. The company has already begun monetizing, having exited Australia for hundreds of millions, begun pistachio conversion, and sold water at nearly $1,000 per acre-foot.

At a market capitalization of ~$490 million, the stock is valued at roughly $2,400 per acre of farmland with the water rights, processing infrastructure, mineral rights, and estimated cash thrown in at zero. This is a remarkable mispricing for assets that, under any reasonable bottoms-up analysis, are worth $1.5–$5 billion.

The catch is real: this is a family-controlled, non-reporting, illiquid company run by people who prize secrecy above all else. There is no visible catalyst, no management presentation, no investor day. The whale does not surface. But for investors with a 5–15 year horizon and the temperament to hold an uncovered, illiquid, deeply asymmetric position, BWEL may represent one of the most compelling deep-value opportunities in the American market.

As the late J.G. Boswell II reportedly said: “Water rights are like democracy. Once you have them, you spend a lifetime protecting them.”