J.G. Boswell (BWEL) | Part 2: NAV Deep Dive

75% NAV Discount | Asset-by-Asset Breakdown

Asset 1: Surface Water Rights - The Core of the Thesis

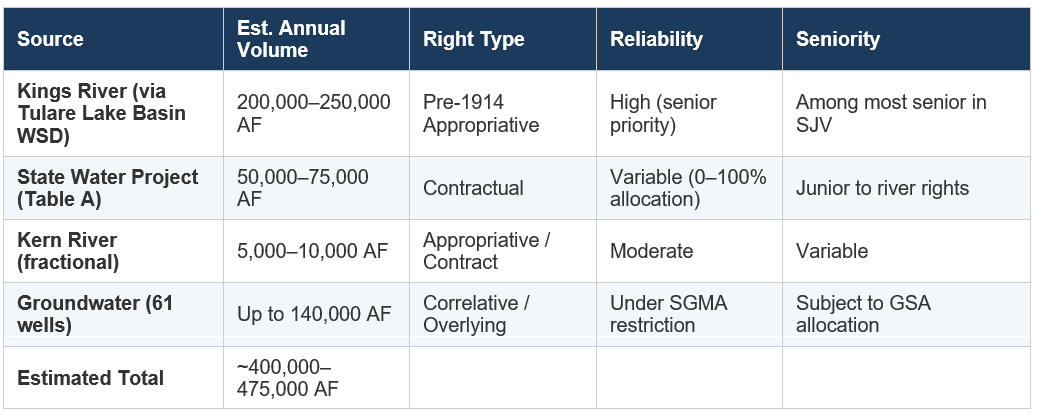

Inventory of Water Entitlements

Boswell’s water portfolio is the company’s most valuable and most difficult-to-value asset. The company holds water through multiple channels, each with distinct legal characteristics, reliability, and market value. Based on public records, legal filings, and investigative reporting, we estimate the following:

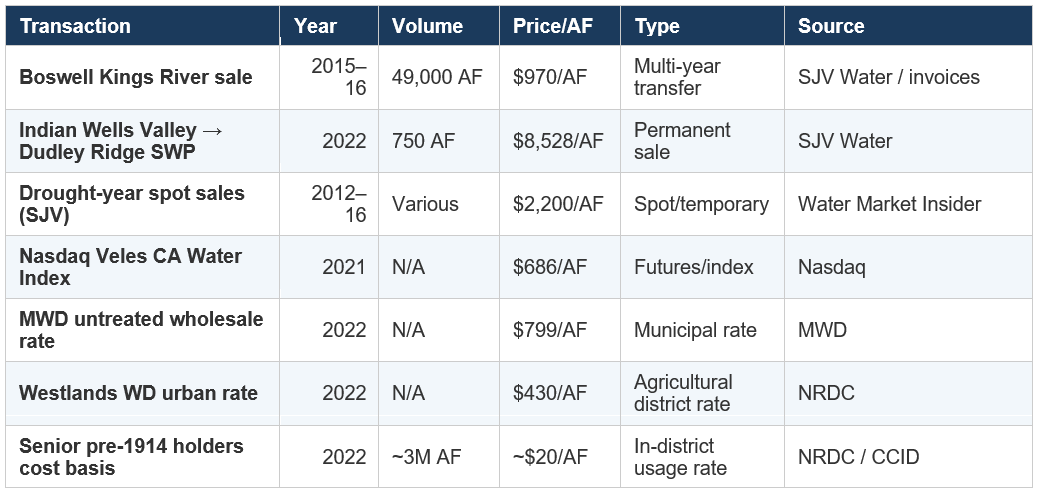

Comparable Transaction Analysis

California water transactions vary enormously based on right type, duration, and geography. The following table summarizes publicly documented transactions that serve as valuation anchors:

Valuation Methodology: Capitalizing an Annual Flow Right

Water rights are perpetual assets. Unlike a one-time commodity sale, a senior surface water right entitles the holder to divert a specified quantity every year, in perpetuity. The correct valuation methodology is therefore a capitalized income approach, analogous to valuing a perpetual bond or a mineral royalty.

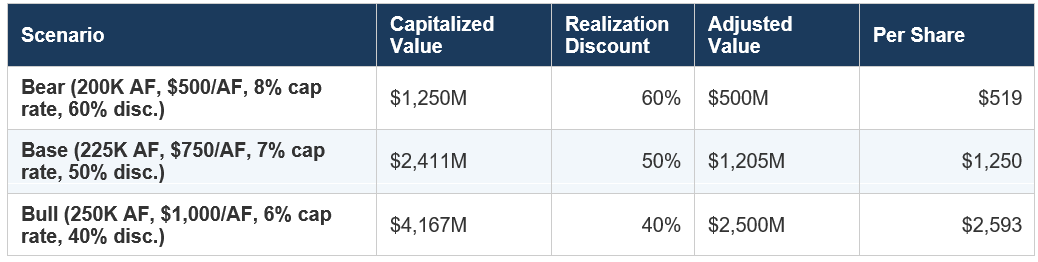

Key formula: Capitalized Value = (Annual Deliverable AF) × (Realized $/AF) ÷ (Discount Rate)

For Boswell’s Kings River rights, we assume 200,000 AF is the reliable annual yield. At the $970/AF the company achieved in its 2015–16 sales, and a 6% discount rate (appropriate for a perpetual, inflation-protected real asset), the capitalized value is:

200,000 AF × $970 / 0.06 = $3.23 billion

Even at a 10% discount rate: 200,000 AF × $970 / 0.10 = $1.94 billion

At a conservative $500/AF (below Boswell’s own realized price): 200,000 × $500 / 0.08 = $1.25 billion

This exercise demonstrates that even under aggressively conservative assumptions, the Kings River water rights alone are worth $1.25–$3.2 billion - roughly 2.5–6.5x the entire market capitalization of $490 million. The SWP contracts and Kern River rights add incremental value.

Realization Risk: Can Boswell Actually Sell This Water?

Legal constraints: California water rights are subject to the “no injury” rule: transfers cannot harm other legal users, including the environment. The Kings River Water Association has actively litigated to prevent water from leaving its “service area.” Boswell itself has sued to block rival Vidovich from transferring Kings River water to western Kings County, arguing those lands are outside the river’s service area. Any large-scale permanent transfer by Boswell would face identical legal challenges from neighboring users.

Regulatory constraints: The State Water Resources Control Board and the Department of Water Resources must approve inter-district transfers. Under SGMA, DWR is now scrutinizing whether water transfers are consistent with approved groundwater sustainability plans. In Kings County, where Boswell’s opponents have accused the company of selling surface water while backfilling with groundwater pumping, DWR director Karla Nemeth has publicly stated the department will reevaluate transfers because “this is a hot spot where the math doesn’t work.”

Physical constraints: Moving water from Kings County to urban buyers in Southern California requires physical conveyance infrastructure. The California Aqueduct runs through Kern County and can carry water south, but capacity is limited and contested. Boswell has already demonstrated the ability to move water to Kern County (137,000 AF over 12 years), but scaling this to full monetization would require expanded infrastructure or creative banking arrangements.

Political constraints: Water transfers out of agricultural communities are politically explosive. Small farmers in Kings County have publicly accused Boswell of “stealing” the region’s lifeblood. The Tachi Yokut Tribe, whose reservation is surrounded by Boswell land, is facing contaminated groundwater and may eventually assert tribal water rights claims.

Realization Discount

Given these constraints, we apply a 40–60% realization discount to the theoretical capitalized value. This accounts for the inability to sell 100% of the portfolio simultaneously, legal friction costs, political risk, and the long time horizon required to monetize fully. Even with a 50% discount applied to the conservative $1.25 billion floor, the water rights are worth approximately $625 million - still 28% more than the entire market cap.

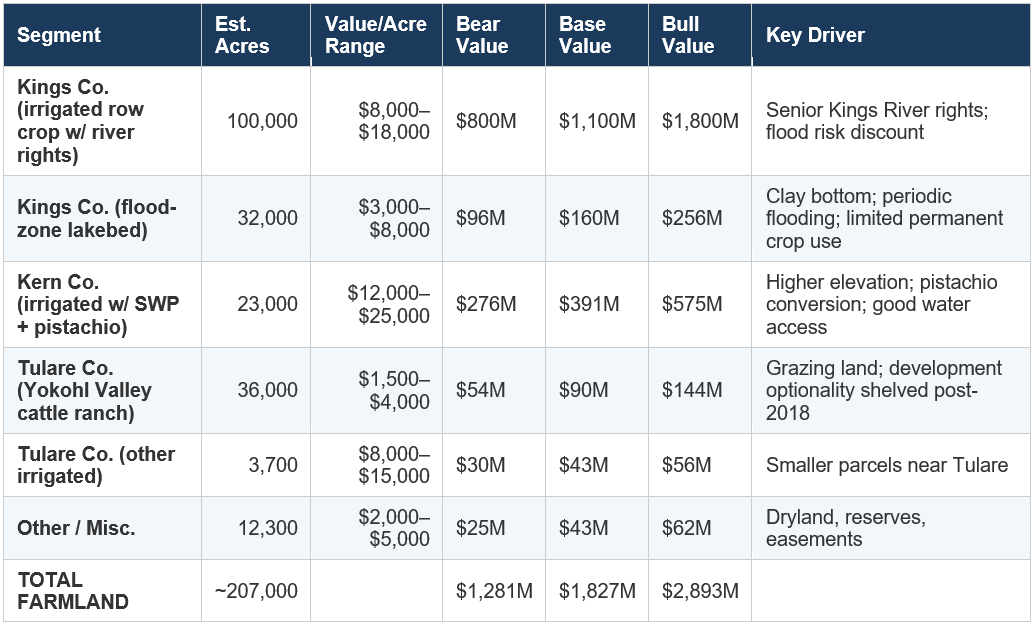

Asset 2: California Farmland - 207,000 Acres

Market Context: Central Valley Farmland Values

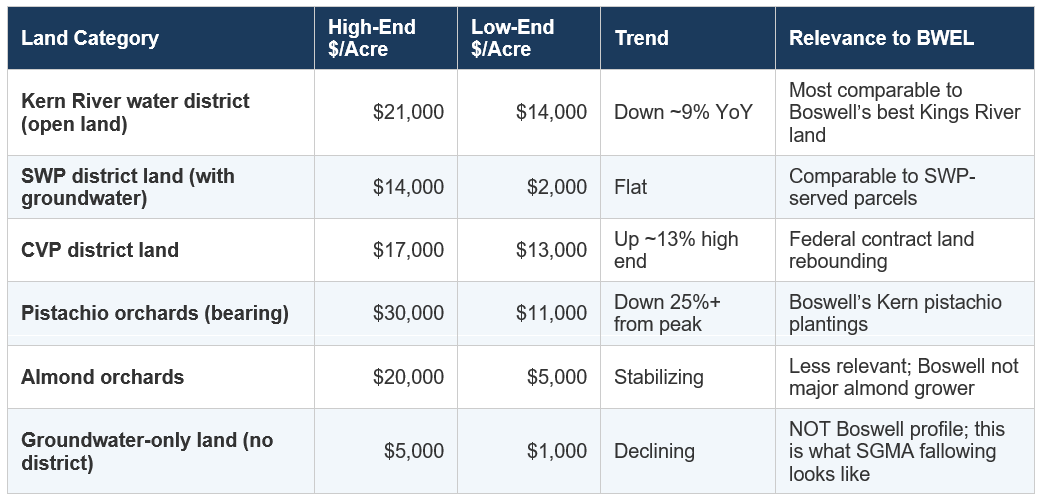

Farmland values in the Southern San Joaquin Valley have been under significant pressure since 2021, driven by declining nut prices, SGMA uncertainty, and rising input costs. The 2025 ASFMRA Trends report described “buyers sharpening their pencils” while sellers “become more realistic.” Alliance Ag Services data from January 2026 shows continued declines in Kern County, with some categories dropping to 2005 levels.

However - and this is critical for Boswell - the decline is not uniform. Farmland with reliable surface water has held value far better than groundwater-dependent land. As Alliance Ag broker Michael Ming stated: “Properties with adequate supplies will do a lot better. I see the footprint of ag in the valley shrinking just because of [water].” This bifurcation is the single most important dynamic in Central Valley real estate, and it overwhelmingly favors Boswell.

Comparable Sales Data (Kern County, Jan 2026)

Boswell Farmland Valuation by Segment

Critical Note:

These land values partially overlap with water rights values. Land with attached water rights sells for significantly more than dry land. To avoid double-counting, our final NAV uses a blended approach: we value land at its “water-included” price for the bear case, and separate land + water for the base/bull cases. See the Consolidated NAV section for reconciliation.

Realization Risks: Farmland

Williamson Act contracts: A significant portion of Boswell’s land is enrolled in the California Land Conservation Act (Williamson Act), which provides property tax reductions in exchange for agricultural-use restrictions. These contracts typically run 10–20 years and must be formally withdrawn before land can be converted to non-agricultural use, triggering cancellation penalties and back taxes.

SGMA fallowing risk: If the State Water Board takes over management of the Tulare Lake groundwater basin (the probation pathway), pumping caps could reduce the amount of land Boswell can profitably farm. However, Boswell’s surface water rights insulate it far more than groundwater-dependent neighbors. The irony is that SGMA’s fallowing mandate increases the value of Boswell’s water-secure land relative to surrounding parcels.

Flood risk on the lakebed: The 2023 Tulare Lake floods destroyed tens of thousands of acres of crops. The lakebed sits on an impervious clay layer with no outlets; floodwater must evaporate. The Army Corps of Engineers can order it used as a relief valve. This creates a permanent uninsurable risk for any permanent crops planted on the lakebed. Boswell’s response - planting pistachios on Kern County uplands rather than the lakebed - is strategically sound but limits the lakebed’s agricultural value.

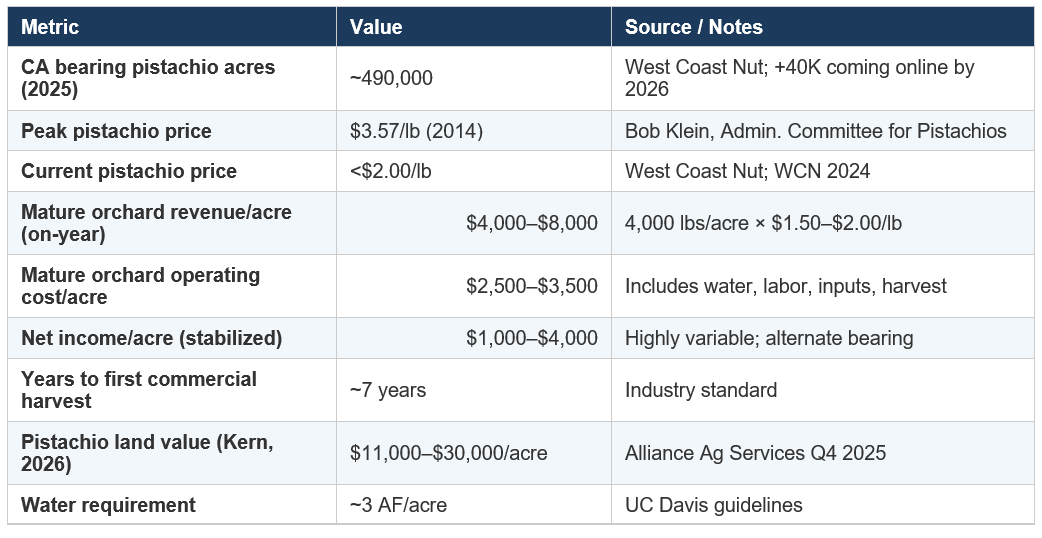

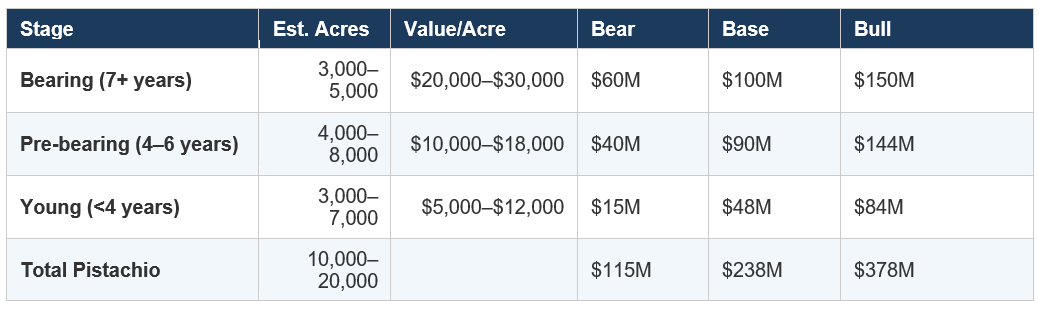

Asset 3: Pistachio Orchards - The Conversion Bet

Boswell’s pistachio plantings are among the least documented but most strategically significant assets. Pistachio grower Jim Valov publicly described a “massive JG Boswell pistachio farm outside the flooded Tulare Lake area” during the 2023 floods. The orchards appear to be concentrated in Kern County at elevations above the flood zone.

Pistachio Economics

Boswell Pistachio Valuation

We estimate Boswell has planted 10,000–20,000 acres of pistachios on Kern County land. Given the timing (likely 2018–2023 plantings, funded by Australian divestiture proceeds), these orchards range from young non-bearing to early-bearing stage. We value as follows:

Key risk: Pistachio prices are under severe pressure. California has added ~300,000 bearing acres in 15 years. Trade war risk (China tariffs on CA pistachios in 2018) remains elevated under current political conditions. However, Boswell’s structural advantage is water security: as SGMA forces groundwater-dependent pistachio growers to fallow, Boswell’s surface-water-irrigated orchards will be among the last standing. Alliance Ag’s Michael Ming estimates 250,000 acres in Kern County alone will come out of production by 2040. Many of those will be nut orchards on marginal water.

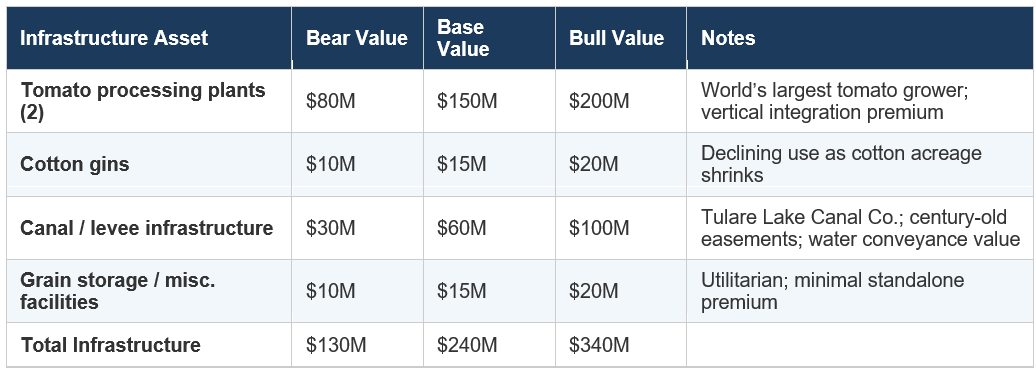

Asset 4: Tomato Processing Plants & Agricultural Infrastructure

Boswell operates two tomato processing plants and is described by The Land Report (January 2026) as “the largest producers of tomatoes in the world.” The company controls its supply chain from proprietary seed through finished paste products, marketed under the Boswell Tomatoes brand.

Replacement Cost Analysis

Modern tomato processing facilities are capital-intensive. A greenfield plant with capacity to process 1–2 million tons per season costs $150–$300 million to build. Boswell’s two plants, while older, have been continuously upgraded and represent decades of accumulated processing know-how. We estimate replacement cost net of depreciation at $100–$200 million.

Additionally, Boswell owns cotton gins (for its remaining Pima cotton operations), grain storage facilities, extensive canal and levee infrastructure, and the Tulare Lake Canal Company - a century-old canal system with legal easements across hundreds of square miles. The canal infrastructure, while not easily separated from the farming operation, has standalone value as water conveyance infrastructure in an increasingly water-constrained environment.

Realization pathway: The processing infrastructure is most valuable as part of the integrated operation. In a breakup scenario, the tomato plants would attract interest from major processors (Morning Star, Kraft Heinz, ConAgra). The canal infrastructure is more difficult to monetize independently but could be leased to water agencies or developers.

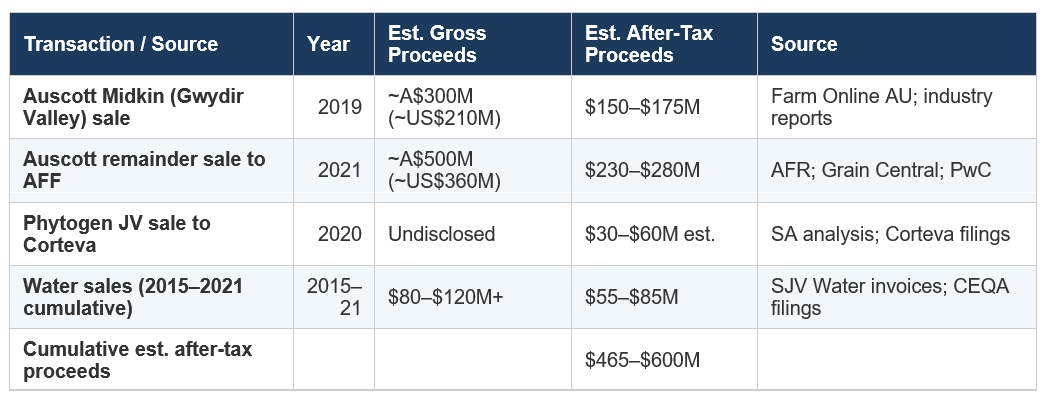

Asset 5: Cash, Investments, and Australian Divestiture Proceeds

Reconstructing the Balance Sheet

Boswell does not publish financials. However, we can reconstruct a partial balance sheet from public transaction data:

Against these inflows, Boswell has been investing in pistachio plantings ($10,000–$15,000/acre for development, suggesting $100–$300M in orchard capital expenditure), paying dividends ($15/share/year = ~$14.5M annually), and covering ongoing operating losses or thin margins on farming. The company also carried some debt historically, though the quantum is unknown.

We estimate the company’s net cash position (cash + liquid investments minus debt) at $100–$350 million as of early 2026. This is necessarily a wide range given the opacity of the balance sheet.

The Cash Question:

Where did the $465–$600M in asset sale proceeds go? Options: (1) pistachio development capex, (2) debt paydown, (3) retained cash, (4) land acquisitions, (5) shareholder distributions beyond the regular dividend. Without public financials, this is the single largest analytical uncertainty. Shareholders who attend the annual meeting (held in Pasadena) should ask this question directly.

Asset 6: Mineral, Oil, Gas, and Subsurface Rights

Boswell owns full or fractional subsurface oil, gas, and mineral interests in land it owns across California and Oregon. Kern County is one of the most prolific oil-producing regions in California (the Kern River, Midway-Sunset, and Cymric fields are among the largest in the state). While Boswell’s Kings County lakebed acreage is not in the most productive oil zones, its 23,000 Kern County acres likely carry some subsurface value.

We assign a nominal $20–$100 million for mineral rights. This is a placeholder; without production data or lease records, a more precise estimate is impossible. In a full liquidation scenario, the mineral rights could be separated and sold to a royalty company.

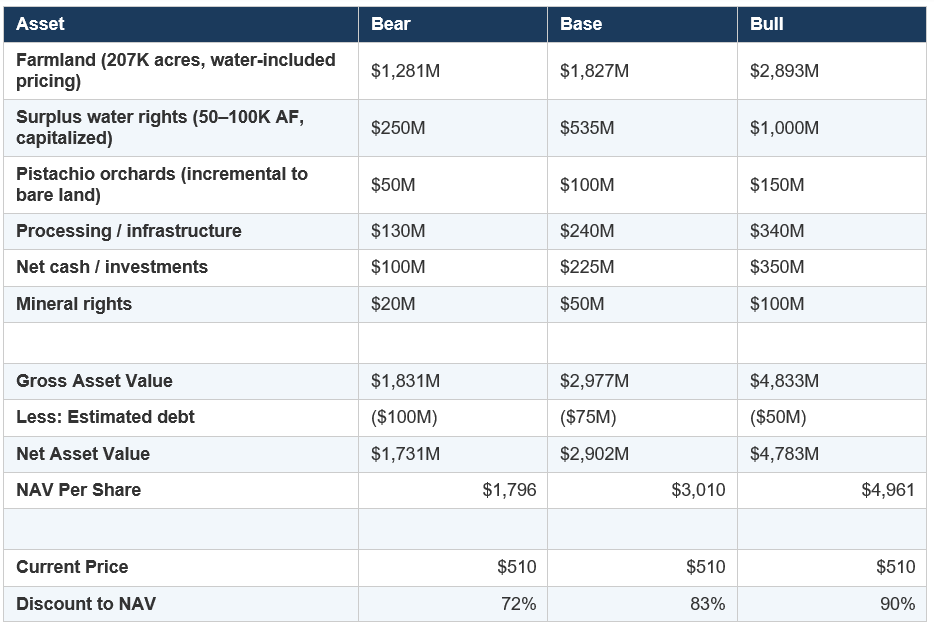

Consolidated NAV: Putting It All Together

Approach 1: Blended (Avoids Water/Land Double-Count)

Because land with attached water rights sells at a premium that already reflects the water’s value, a blended approach values the land portfolio at its “all-in” market price and adds only the incremental value of water that Boswell could sell without reducing its land value. We estimate 50,000–100,000 AF of “surplus” water (above what is needed to irrigate the farming operation) is available for annual sale.

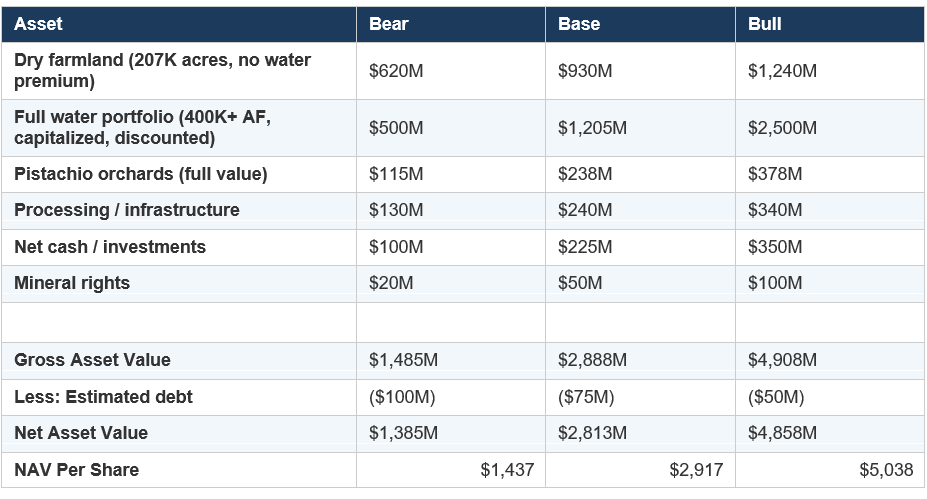

Approach 2: Separated (Water Valued Independently)

This approach values the land at dry-land prices (stripping out the water premium) and values the full water portfolio independently. This produces higher NAVs because it captures the option value of full water monetization.

Reconciliation:

Both approaches produce base-case NAVs in the $2,800–$3,000/share range, approximately 5–6x the current price. The bear case ($1,400–$1,800/share) implies the stock is trading at roughly 30–35 cents on the dollar even under pessimistic assumptions. The bull case ($4,800–$5,000/share) reflects full water monetization at prices already observed in California transactions.

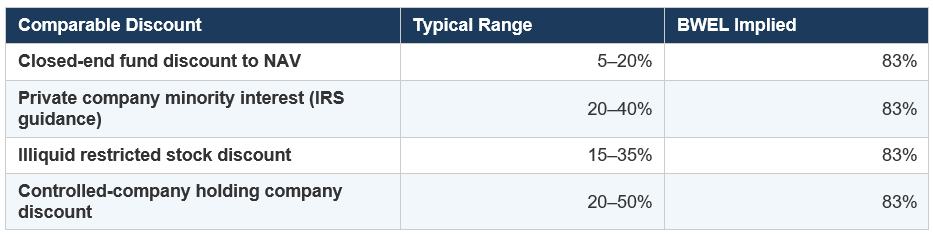

The Governance & Liquidity Discount: How Much to Haircut?

The elephant in the room is this: what good is a $3,000 NAV if the Boswell family never unlocks it? Private company minority interest discounts in academic literature and IRS guidance typically range from 20–40%, reflecting the inability to force liquidation, control capital allocation, or access financial information. For Boswell, the discount should arguably be even wider due to:

• No SEC filings - Minority shareholders operate with less information than the IRS provides on a tax return.

• ~500 share average daily volume - Exiting a 1,000-share position ($510K) could take weeks and move the stock.

• No governance rights - No independent directors, no proxy access, no say-on-pay.

• Indefinite holding period - Without a catalyst, the discount can persist for decades (and has).

What Discount Is Already Priced In?

At ~$510 per share against a base-case NAV of ~$3,000, the stock already trades at an 83% discount to NAV. This discount is more extreme than virtually any closed-end fund, SPAC trust, or minority interest in a family holding company. For context:

The market is applying a discount that assumes the assets will NEVER be monetized. Even a modest shift in this assumption - a single large water sale announced publicly, a significant dividend increase funded by Australian cash, or an SEC filing - could trigger a substantial re-rating. The stock doesn’t need to close the full gap to NAV for shareholders to earn exceptional returns.

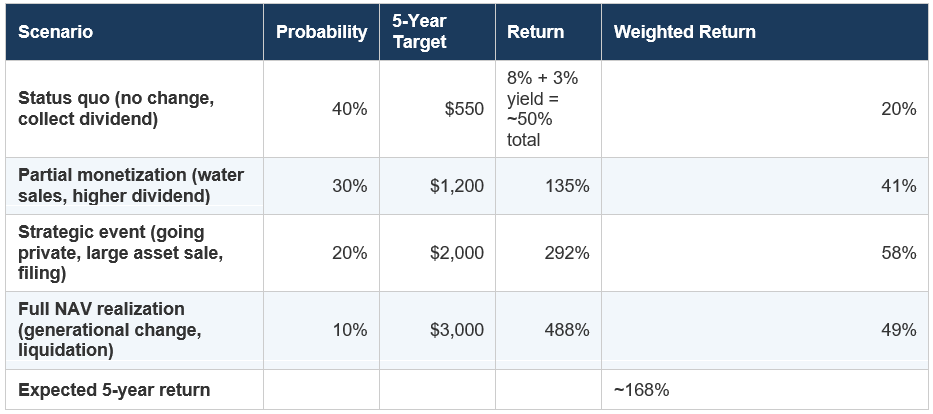

Probability-Weighted Return Framework

Even assigning a 40% probability to the status quo (dead money with a 3% dividend), the probability-weighted expected return is highly attractive because the upside scenarios are so asymmetric. This is the classic deep-value skew: limited downside (the land and water aren’t going to zero), enormous upside if management behavior changes even marginally.

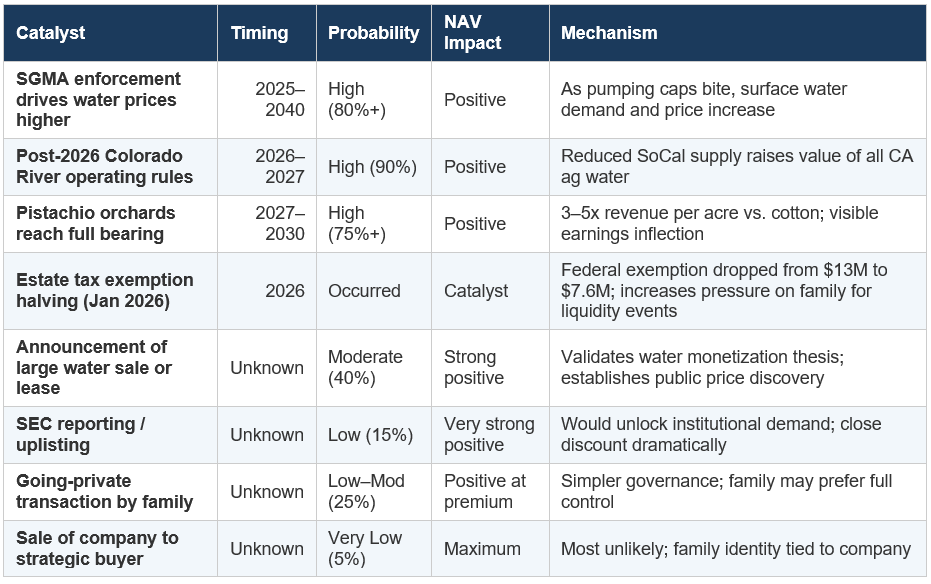

Potential Catalysts and Their Probabilities

The estate tax catalyst deserves special emphasis. As of January 1, 2026, the federal estate tax exemption was halved from over $13 million to $7.6 million per person. For the Boswell family, whose controlling interest may be valued at several hundred million dollars, this dramatically increases the tax burden upon generational transfer. Estate planning strategies (GRATs, family limited partnerships, charitable trusts) can mitigate but not eliminate this pressure. The most tax-efficient solution may involve either increasing the stock’s public float (creating a market for gradual family sales), structuring partial asset divestitures, or taking the company private at a premium.

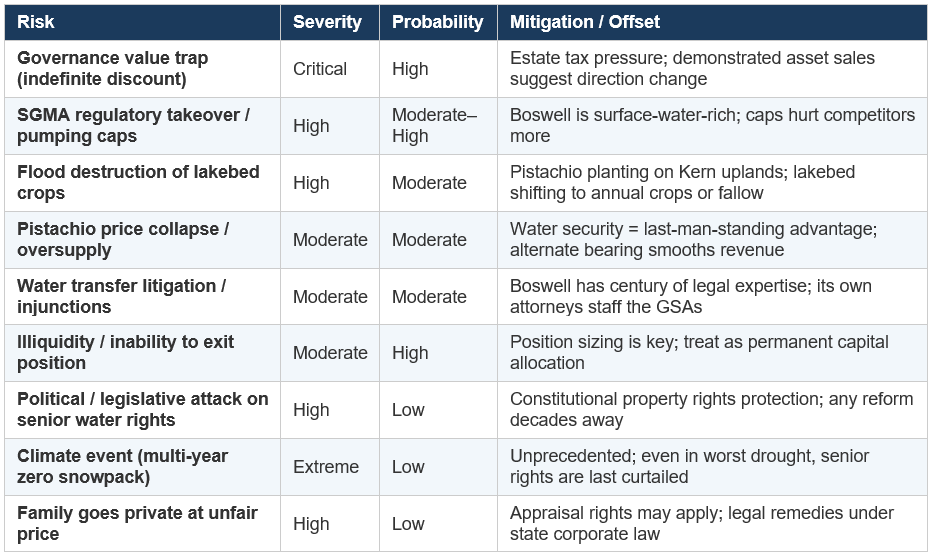

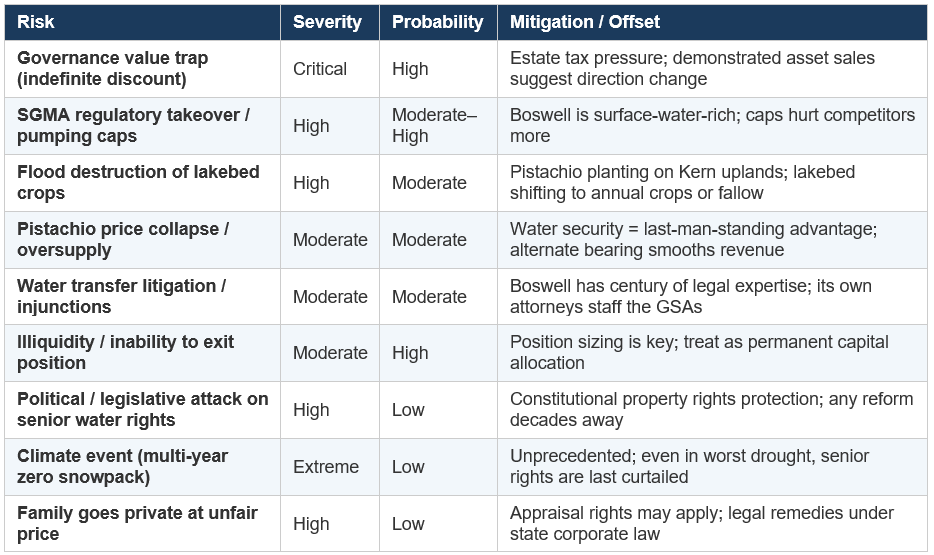

Comprehensive Risk Matrix

Conclusion: The Verdict on Realizability

The evidence is unambiguous: J.G. Boswell Company’s assets are worth multiples of its current share price under any reasonable methodology. The base-case NAV of approximately $3,000 per share - roughly 6x the current price - is supported by directly observable comparable transactions in farmland, water, and agricultural processing. The bear-case NAV of $1,400–$1,800 per share - still 3–3.5x the current price - uses deliberately conservative assumptions that underweight the most valuable asset (water rights) and assume wide realization discounts.

The question is not whether the assets are valuable. The question is whether minority shareholders will ever participate in that value. Here, the evidence is more ambiguous but trending positive. The 2019–2021 Australian divestiture, the pistachio conversion, the water sales, and the estate tax environment all suggest a family that is, slowly and on its own terms, transitioning from asset accumulation to asset monetization. This is not a company that is asleep. It is a company executing a multigenerational plan with extreme patience and zero interest in publicity.

For an investor with the right temperament - comfortable with illiquidity, comfortable with information asymmetry, comfortable holding for 5–15 years - BWEL offers a rare combination: a hard-asset floor, a secular tailwind (water scarcity), a demonstrated management pivot toward monetization, and a governance discount so extreme that even modest catalysts could generate outsized returns.

The margin of safety is the water. The upside is the inevitability of scarcity. The risk is the timeline.