J.G. Boswell (BWEL): A Generational Water Asset, Priced Like a Farm

The original King of California - senior water rights and an 82% discount to NAV, just as the West's water crunch comes to a head

California’s largest private farm sits on a multi-billion-dollar water fortune - and the market is pricing the water at zero. J.G. Boswell owns ~207,000 acres in the bed of the former Tulare Lake, controls some of the most senior water rights in the most water-stressed farm region in the country, and trades on the pink sheets - no SEC filings, almost no liquidity, a ~$516 million market value against assets conservatively worth several billion.

The origin. In the early 1920s the boll weevil beetle destroyed cotton across the American South. A Georgia cotton man, Colonel J.G. Boswell, went west, founded the company in 1925, and began assembling land in the bed of Tulare Lake - once the largest freshwater lake west of the Mississippi. The definitive history of Boswell, Arax and Wartzman’s book titled The King of California, reads less like a corporate profile than the chronicle of a private kingdom.

What it is today. Family-controlled and headquartered in Pasadena, Boswell farms ~207,000 acres. The crop mix has moved from Pima cotton to processing tomatoes (it is described as the world’s largest tomato grower) and, more recently, to pistachios on higher Kern County ground. But the crops are almost beside the point. The real value is water: senior, pre-1914 Kings River rights. Pre-1914 rights are uniquely valuable because California water is allocated by strict seniority - the oldest rights are filled first and curtailed last. In a drought, juniors get cut to zero while Boswell’s keep flowing, leaving it with water to sell exactly when prices spike.

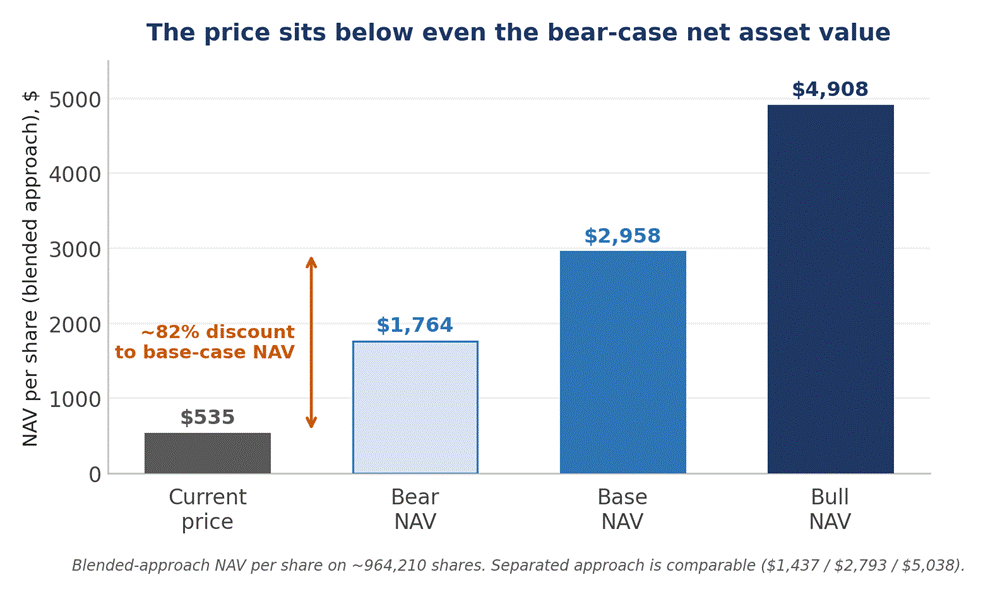

Why it’s compelling. The proposition is simple: a portfolio of hard, scarce, inflation-protected real assets - farmland, senior water rights, and cash - conservatively worth ~$2.9 billion, owned through a stock priced near $516 million. That is an ~82% discount to net asset value. The market treats Boswell solely as an illiquid farm - and, as the next sections argue, prices the senior water rights at essentially zero.

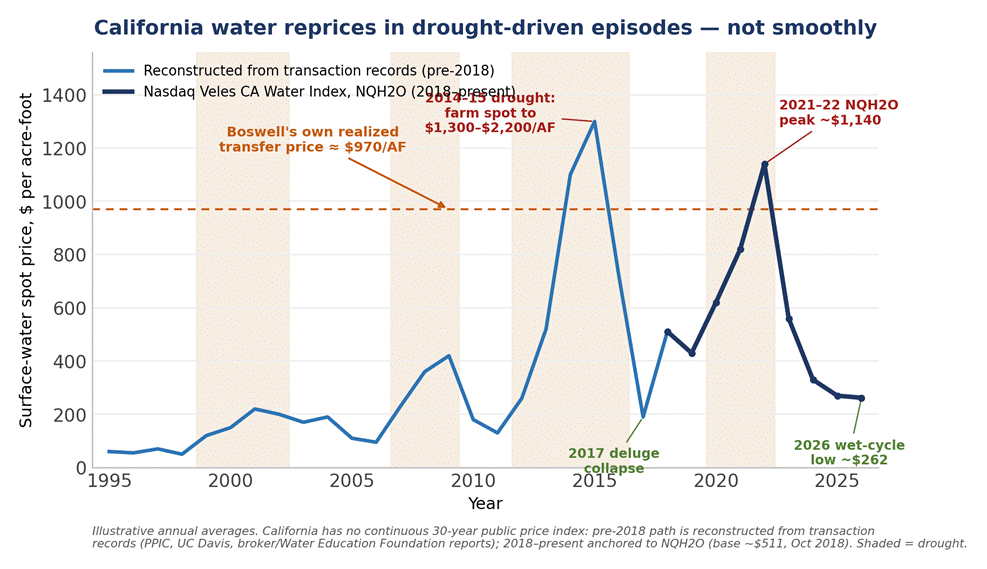

The timing is not accidental. The century-old Colorado River compact expires in October 2026 with reservoirs near record lows and no replacement deal, which would force cuts to Southern California and make every in-state senior water right more valuable. That is the kind of stress event that re-rates this asset class: California water values have historically jumped 5–10x during periods of water scarcity.

Note: This deep-dive fits directly with our Water Rights Thesis, which explains why senior water rights are the AI-power buildout’s inevitable second derivative and an asset class the market still values at zero. If you want the macro case for water, start there.

The NAV at a Glance

The full asset-by-asset build is below; here is where it lands. A base-case NAV near $2,950/share - roughly 5× the current price. Later in this article, we break down the NAV asset-by-asset.

What Changed in 2026

The five things that moved

1. Groundwater rules now have teeth. SGMA, California’s 2014 groundwater law, forces over-pumped basins back into balance and lets the state intervene if locals don’t comply. For Boswell, SGMA squeezes its neighbors’ groundwater-dependent land while leaving its senior surface rights untouched - so its water becomes relatively more valuable without the company lifting a finger.

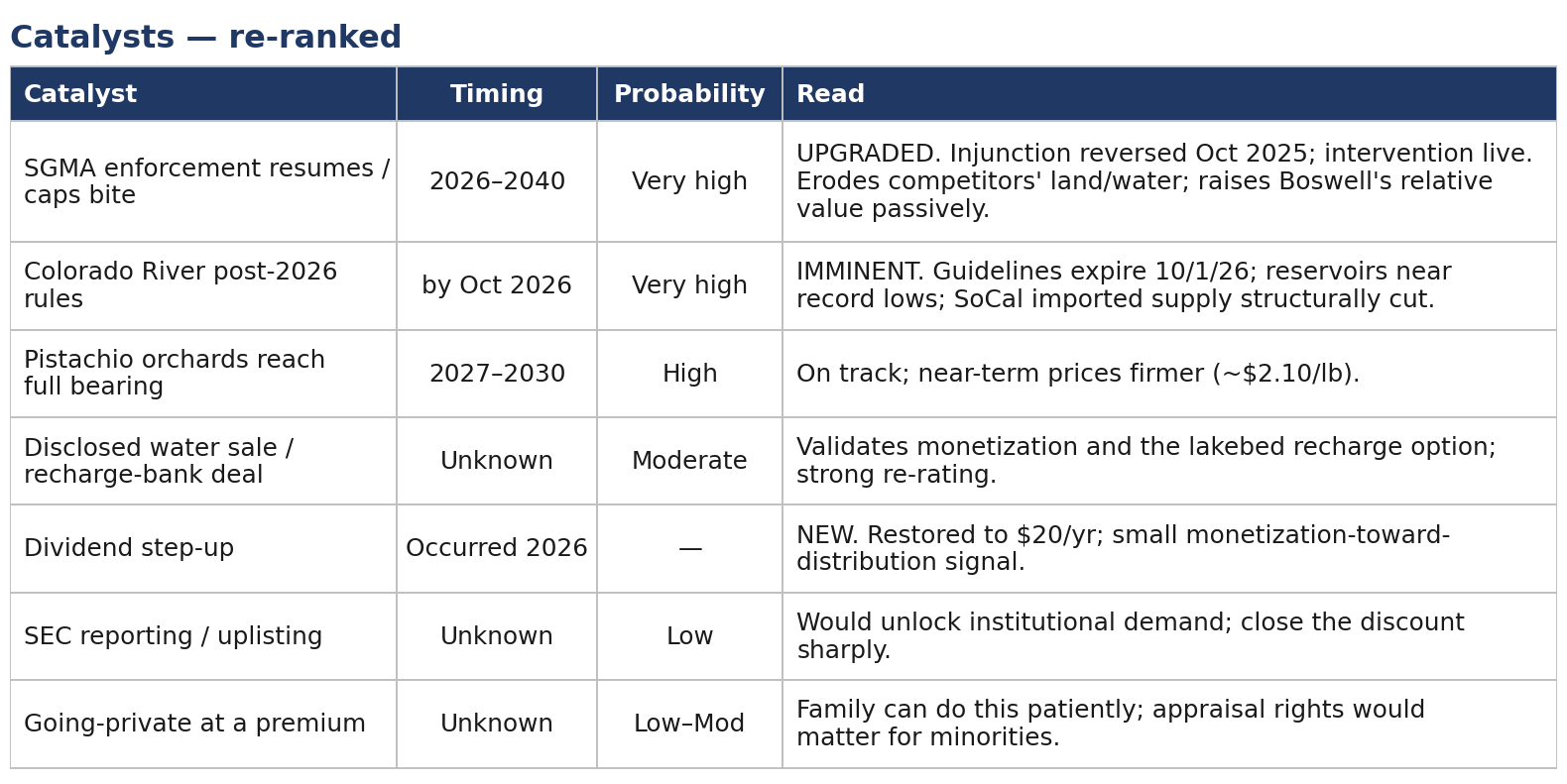

2. The Colorado River reset is imminent, not theoretical. The 2007 Colorado River Guidelines expire October 1, 2026. As of mid-2026 Lake Mead sat ~30% full and Lake Powell ~23–26%, April–July inflow to Lake Powell is ~13% of normal (lowest on record), and no seven-state agreement exists. The structural cut to Southern California’s largest imported supply is likely determined in the next 6-12 months.

3. The dividend was restored. After a 2025 cut to $3.75/quarter ($15/yr), Boswell returned the payout to $5.00/quarter ($20/yr) for 2026 - a small but real cash-return.

4. Farmland likely bottomed in 2025. Alliance Ag / SJV Water data (Jan 2026) show farmland declines flattening and “more properties in escrow than in years.” Water-secure land is decoupling upward.

5. Pistachio pricing firmed. Even with a record California crop in 2025, prices held up and pistachio growers are profitable again - partly because Iran, the world’s #2 producer, has been impacted by export disruptions. Less supply abroad means more pricing power for California growers like Boswell.

What the Market Is Missing - and Why Now

1. The market is paying for a farm and getting the water for free

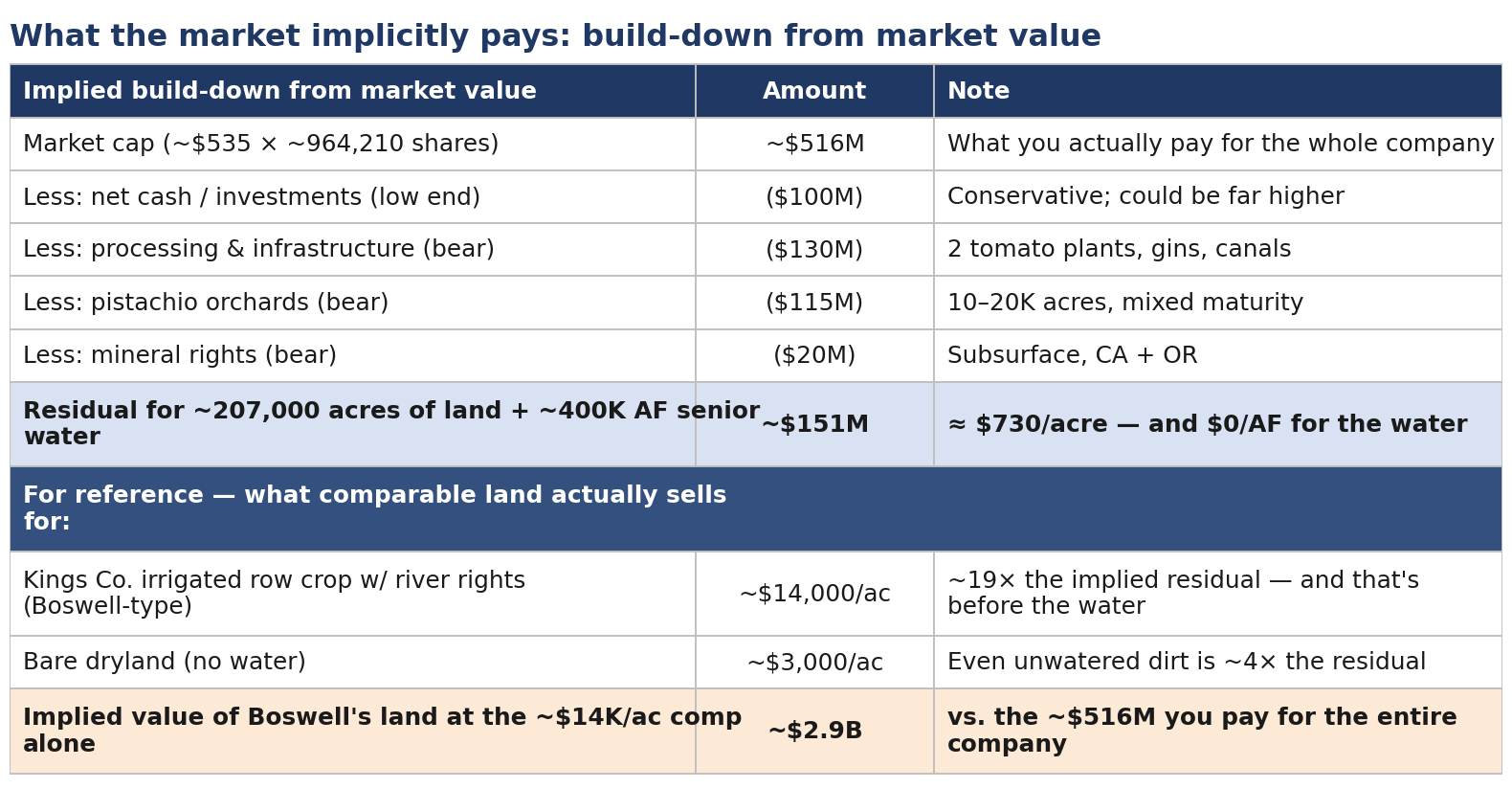

Work backward from the share price and the mispricing becomes concrete. At a ~$516M market cap, here is what the market is implicitly willing to pay for the operating-and-land assets after backing out the pieces that are hardest to argue with:

The residual works out to roughly $730 per acre for the land - below even a pessimistic dryland estimate of ~$3,000/acre - which means the market is not only refusing to pay for the senior water rights, it is paying less than bare dirt for irrigated ground and pricing the water entitlement at zero (or negative). The senior, pre-1914 Kings River rights - the asset that is genuinely scarce and last curtailed in any drought - carry no recognized value in the quote. The market sees a farm a family won’t sell and stops there.

Why the market does this is understandable: Boswell doesn’t file, the stock trades a few hundred shares a day, and the water has never been carved out and sold to a city. So the rights sit inside an operating farm, valued (if at all) as a farming input rather than as the scarce, separately-monetizable asset they are. The bet is simply that this is wrong - and that the catalysts below will force the recognition.

2. The real catalyst is regulatory, and it became enforceable in late 2025

The single most important development is legal, and it is dated. SGMA - California’s 2014 groundwater law - has a “state backstop” that lets the State Water Board take over basins with inadequate plans. Boswell’s land sits in the Tulare Lake Subbasin, placed on probation in April 2024. The Kings County Farm Bureau won an injunction that froze enforcement - and that injunction was the thing keeping the backstop theoretical. In October 2025 the appellate court reversed it and affirmed the Board’s broad authority. Enforcement has resumed; reporting and fees are due May 1, 2026.

Why this matters more than a water sale: it does not require Boswell to do anything. As SGMA allocations bind across the Valley over the next 5–15 years, groundwater-dependent acreage - the bulk of competing farmland - must fallow, and its value erodes toward dryland prices. Boswell’s senior, pre-1914 Kings River surface rights are the last curtailed in any drought and are not SGMA groundwater at all. The result is a passive relative-value transfer: Boswell’s water-secure land and senior rights compound in relative value while neighbors are administratively shrunk. You are not betting on a management decision. You are betting on scarcity arithmetic that the state has just been cleared to enforce.

3. The market lumps “Boswell’s water” into one number; it is two very different assets

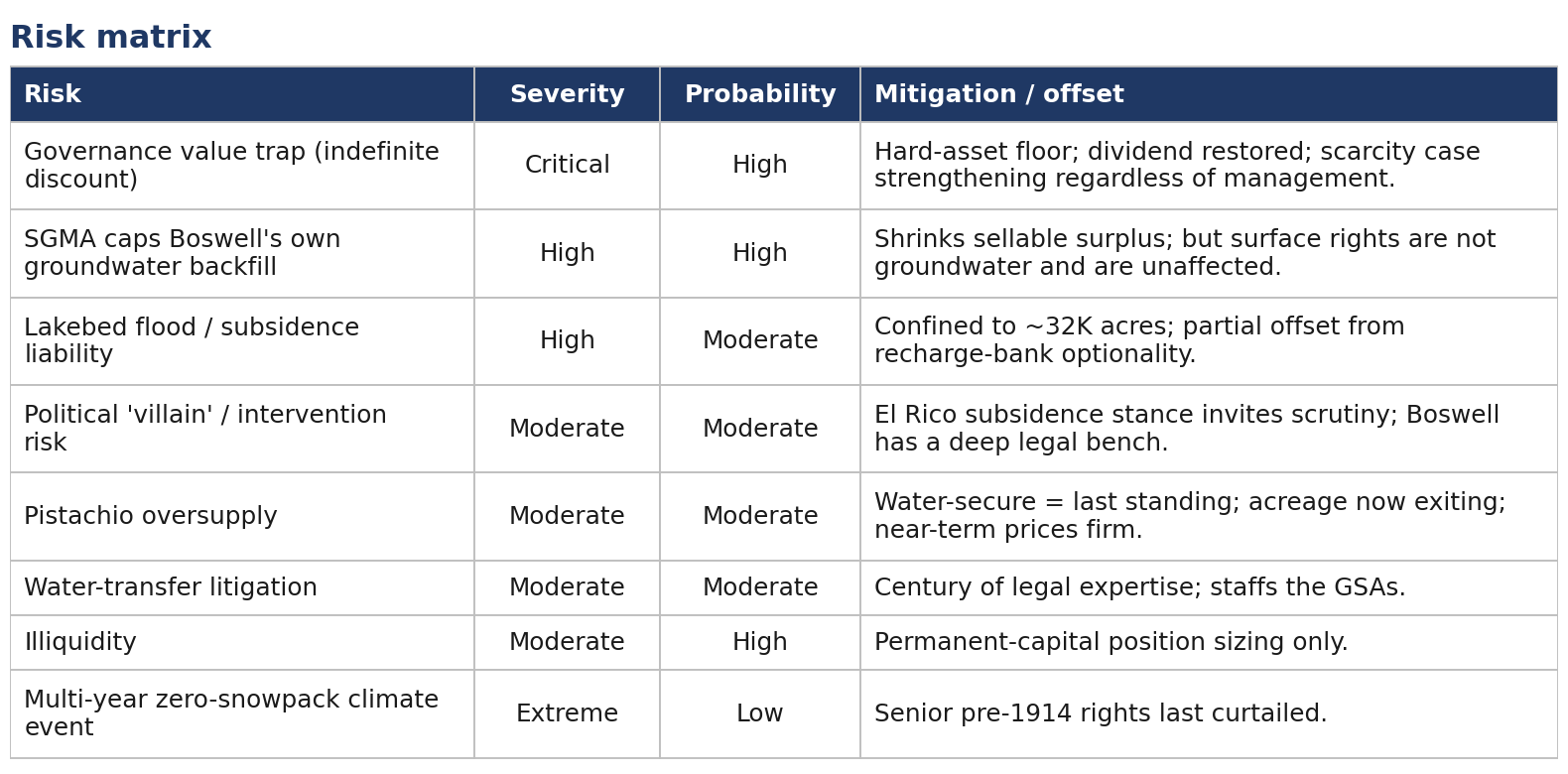

Most coverage totals surface rights and groundwater into a single ~400–475K AF figure. Separate them and the picture sharpens. The senior surface portfolio (pre-1914 Kings River, plus SWP and a Kern fraction) is the moat: durable, defensible, monetizable, last-curtailed. The groundwater (61 wells, up to ~140K AF) is the contested asset that SGMA is about to cap. Boswell controls the El Rico GSA and has pushed a plan permitting roughly six more feet of subsidence - i.e., it intends to keep pumping hard. That is exactly the “backfill” behavior (sell/lease surface water, replace with groundwater) that the resumed state intervention is designed to stop. So discount the groundwater more, and lean on the senior surface rights as the thing that is genuinely scarce and genuinely Boswell’s.

4. The Tulare lakebed is a recharge call option

Boswell’s near-total control of the old Tulare lakebed gives it a regional recharge-bank optionality - capturing wet-year flood flows, banking them, and selling credits or stored water to capped neighbors - that is essentially unmodeled in the public discount.

5. Why now

Two clocks are striking in the same 12-month window. The legal precondition for SGMA enforcement cleared in late 2025, so the mechanism that erodes everyone else’s water-dependent land is finally switched on - and the Colorado River operating rules expire October 1, 2026 with reservoirs near record lows, structurally tightening Southern California’s imported supply. Both make Boswell’s senior water scarcer. That divergence - a market price that ignores the water, against fundamentals that make it scarcer - is the opportunity.

The Michael Burry trade, in public form. Burry - yes, the Big Short one - has invested privately in water-rich farmland, arguing that water rights directly are too political. That’s exactly what Boswell is - with a public ticker. The market hasn’t noticed this, so you get the Burry strategy with an 80%+ discount.

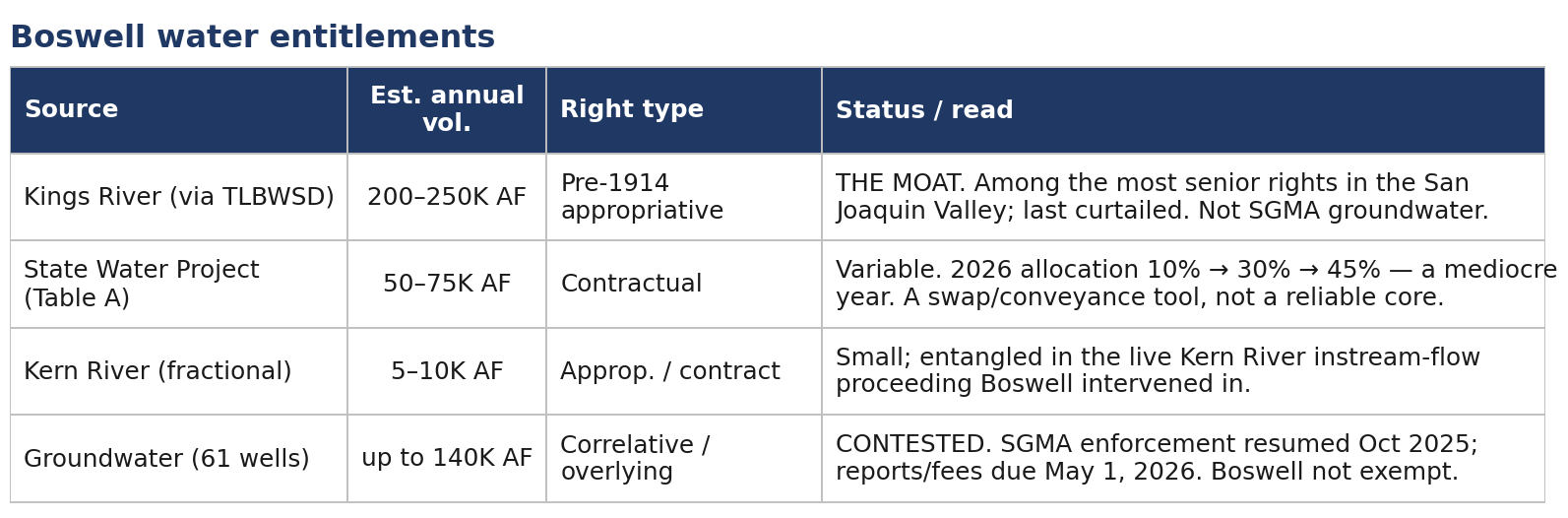

Asset 1: Water Rights

Inventory of water entitlements

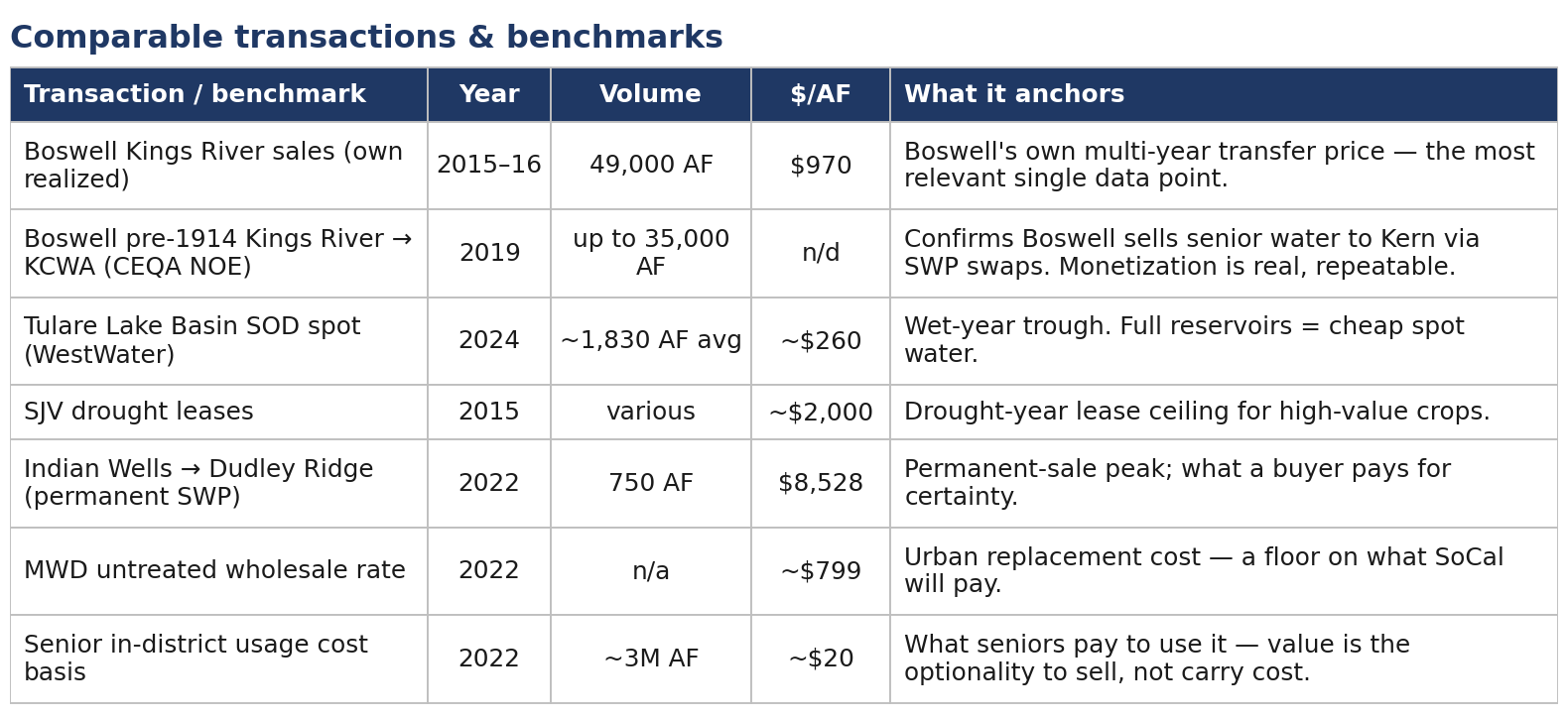

Comparable transactions - refreshed, and read for what they actually prove

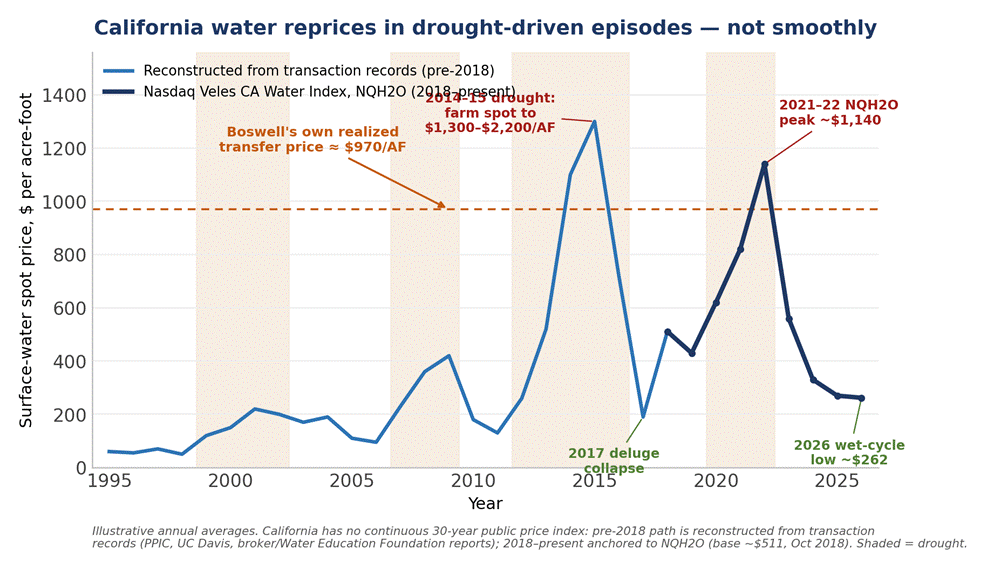

California water pricing is bimodal: cheap in wet years, explosive in drought. The point of the comps is not a single “price of water” but the spread between an in-district trough and a permanent-sale peak - and where senior rights sit within it.

Valuation: capitalized flow, with the SGMA caveat

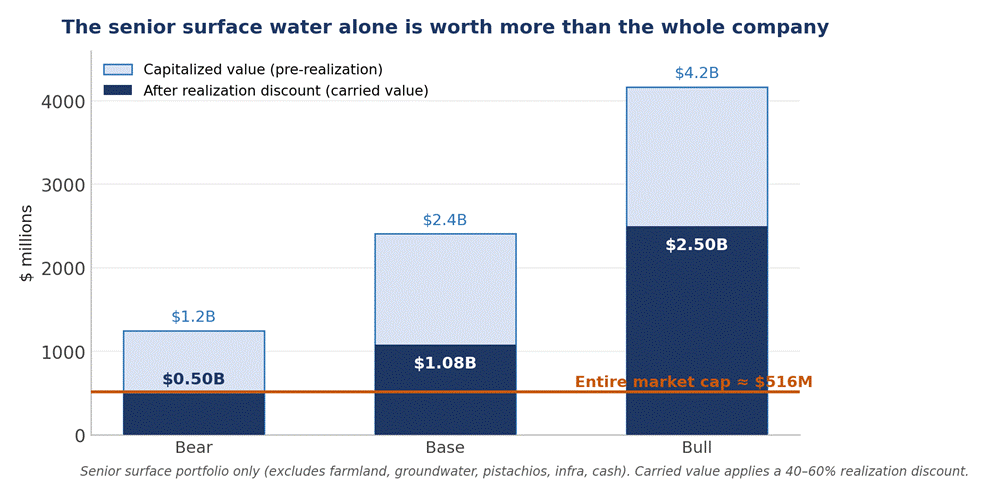

Senior surface water is a perpetual annual entitlement, correctly valued as a capitalized flow: Capitalized Value = Annual Deliverable AF × Realized $/AF ÷ Cap Rate. On 200,000 AF at $970/AF and a 6% rate, the gross math is ~$3.2B; at 10% it is ~$1.9B; at a conservative $500/AF and 8% it is ~$1.25B - still 2.4–6.5× the entire market cap.

The double-count discipline

You cannot simultaneously (a) farm 200K AF, (b) sell a 50–100K AF “surplus,” and (c) carry full capitalized value on all of it. Water used to grow the crop is already inside the farmland value.

So this article values water in two ways: (1) Blended - land at water-included prices plus only a capitalized surplus; (2) Separated - land at dryland prices plus the full senior portfolio.

Realization - the constraints are the same, but two have sharpened

• Regulatory - sharpened: SGMA enforcement is no longer theoretical. The state backstop is affirmed and resuming. This raises the value of surface water (neighbors get capped) but constrains Boswell’s groundwater.

• Physical / conveyance: Boswell has already moved ~137K AF to Kern over 12 years and executed SWP swaps to deliver Kings River water south - a proven path into a tightening SoCal market as the Colorado River is cut.

• Political - sharpened: Boswell is the public face of subsidence in a basin sinking the town of Corcoran. That “villain” profile is a headline and intervention risk.

Surface water rights - scenario value

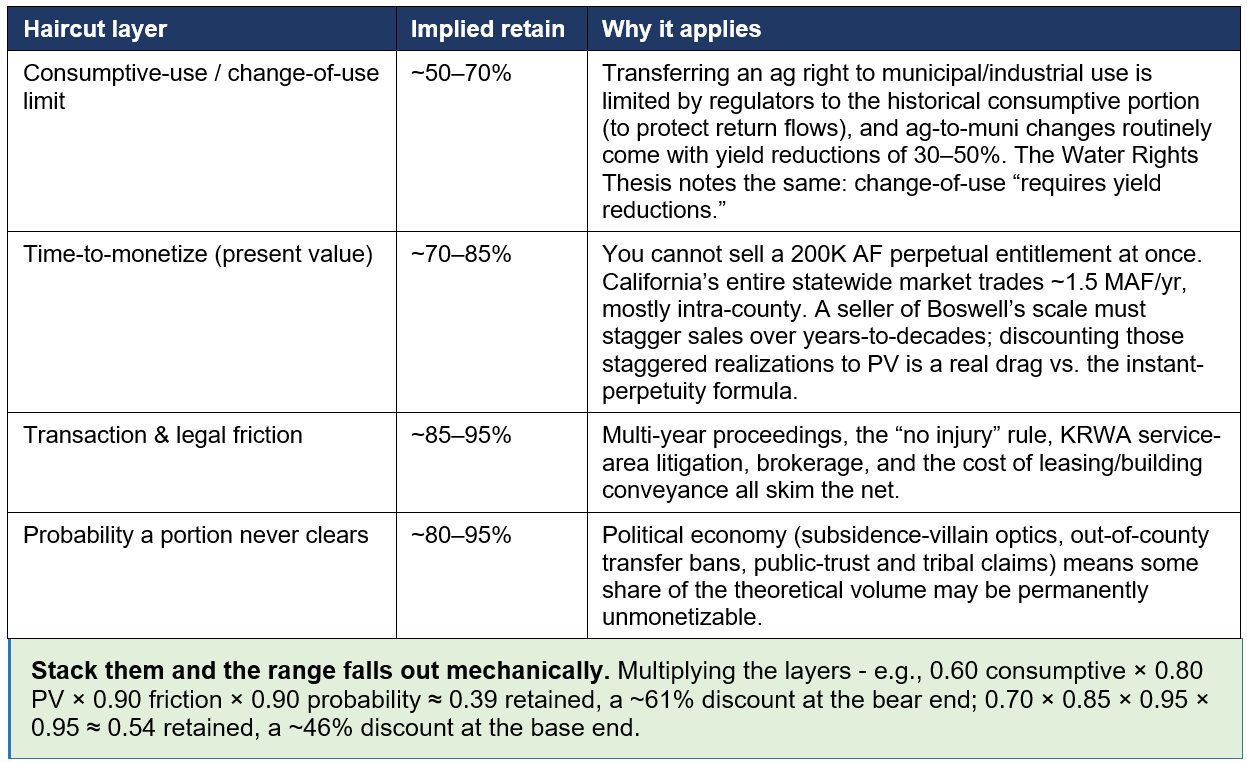

Where the 40–60% realization discount comes from

A skeptic should push on this number, because the discount does most of the work between a $1.9–3.2B theoretical figure and the $0.5–2.5B we actually carry. It is not a plug. It is the product of four independent, stacked haircuts - each documented, and each pushing the same direction:

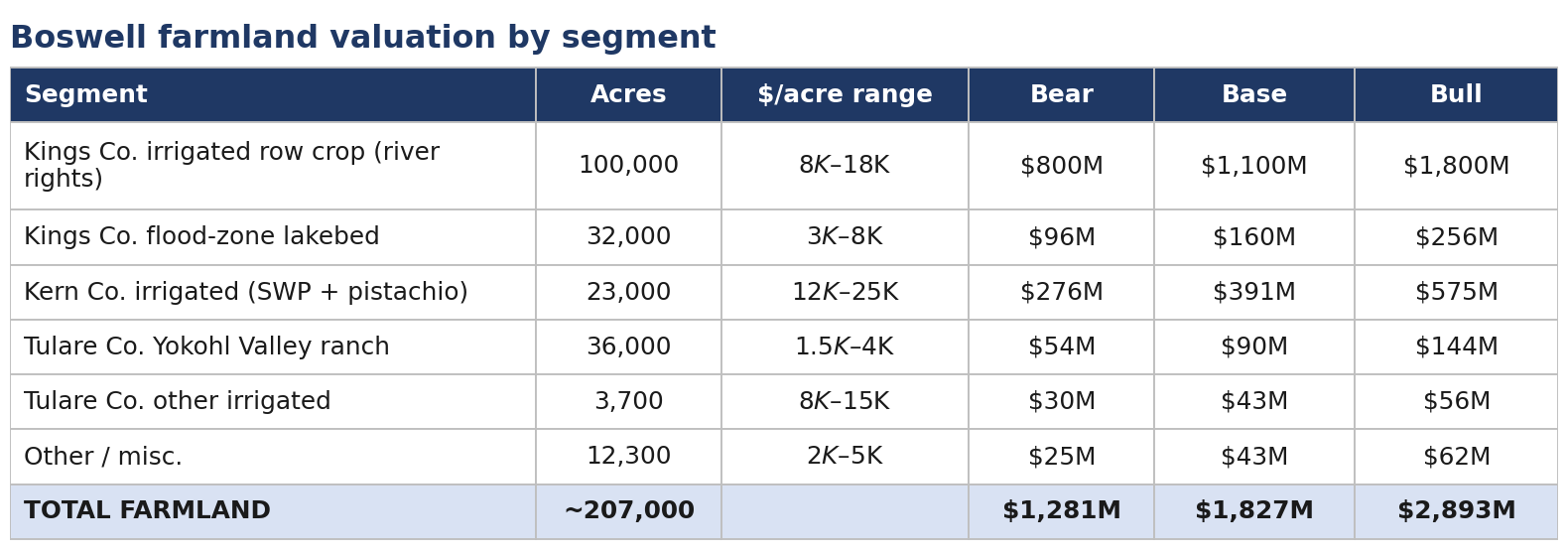

Asset 2: California Farmland - ~207,000 Acres

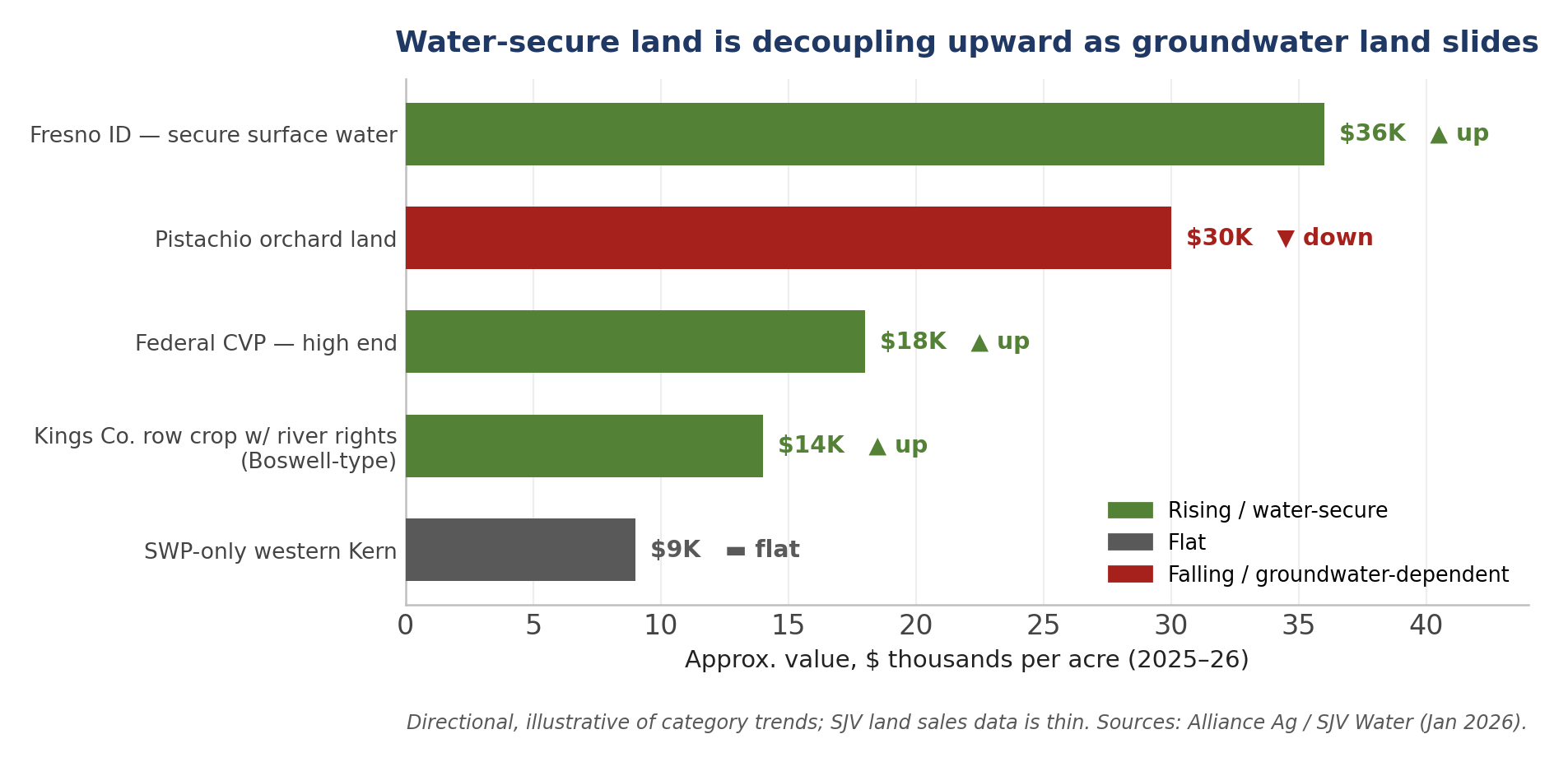

Statewide farmland values appear to have bottomed in water-secure districts while groundwater-only land kept sliding - exactly the bifurcation that defines the Boswell profile.

Market context, refreshed (Alliance Ag / SJV Water, Jan 2026)

• Declines flattened in 2025 and may have bottomed in several water-category districts; brokers report more land in escrow than in the prior couple of years.

• Federal CVP-served land rebounded at the high end, ~$16K → ~$18K/acre (thin sales data, but directionally telling).

• Fresno Irrigation District cropland printed as high as $36K/acre - a rare upward outlier driven entirely by secure, low-cost surface water. This is the closest live analogue to Boswell’s best Kings River-served ground.

• SWP-only western Kern land remains pinned at ~$2K–$13K/acre. Pistachio orchard land fell to ~$30K from ~$40K at end-2024.

Boswell farmland valuation by segment

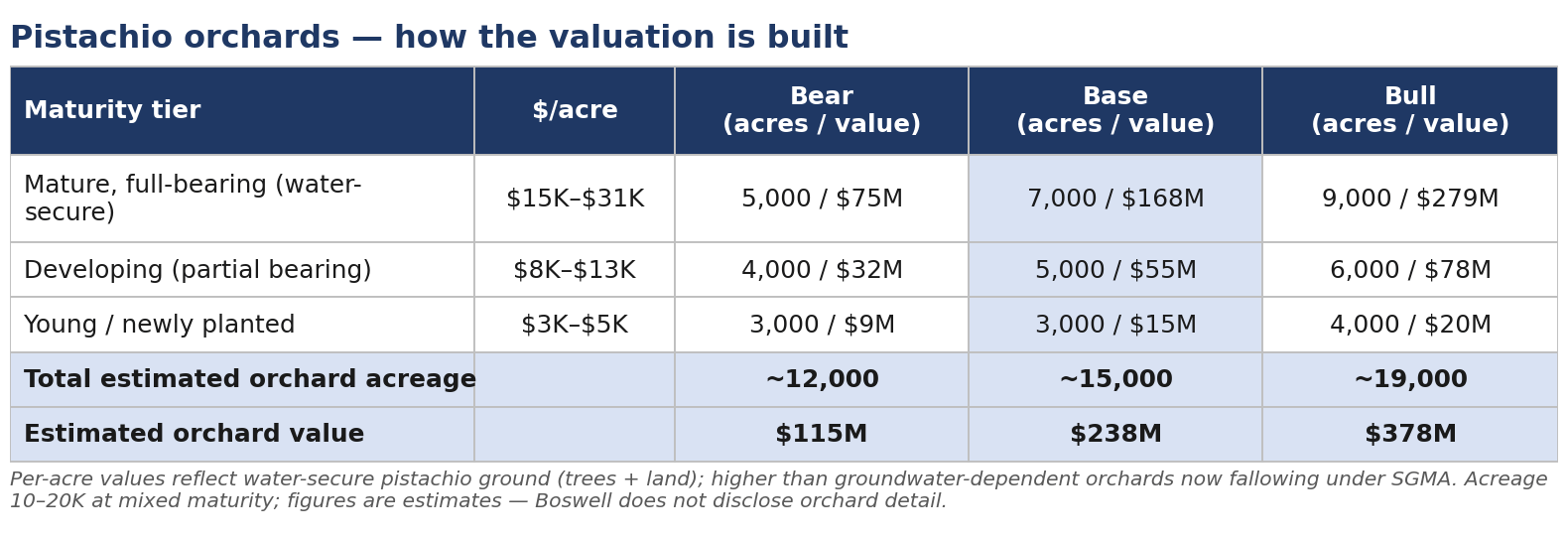

Asset 3: Pistachio Orchards - the Conversion Bet, Firmer Than Feared

Near-term economics improved and the structural “last man standing” logic strengthened - as SGMA caps groundwater, marginal-water orchards fallow while Boswell’s surface-irrigated trees keep producing. The standing risk is the supply glut from a decade of plantings, partly offset by acreage now starting to exit.

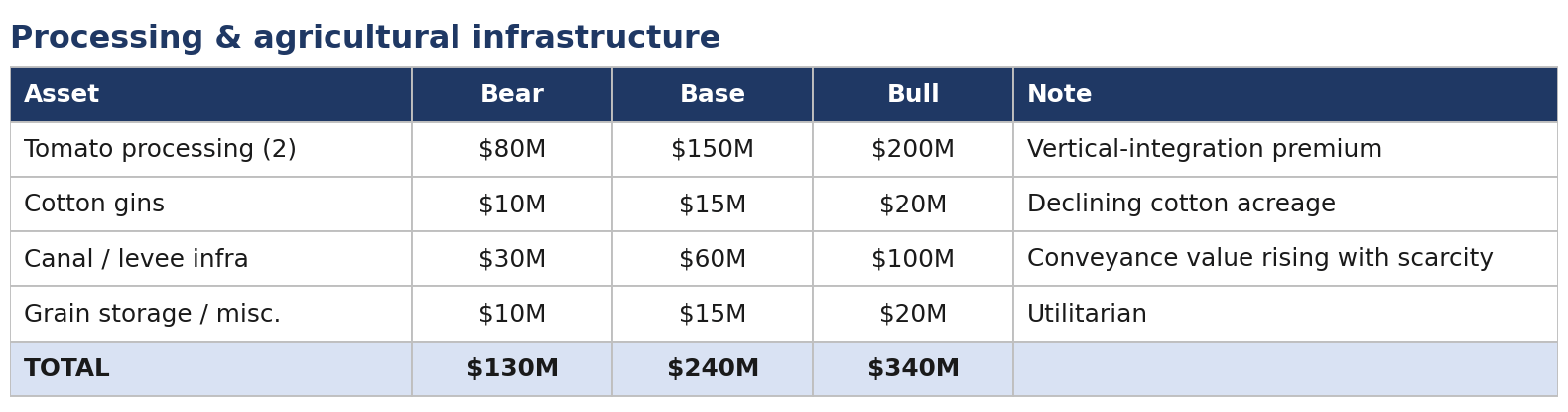

Asset 4: Processing & Agricultural Infrastructure

Two tomato processing plants (Boswell is described as the world’s largest tomato grower), cotton gins, grain storage, and the century-old Tulare Lake Canal Company conveyance network. Valued as replacement-cost-net-of-depreciation.

Asset 5: Cash, Investments & the Australian Proceeds

Still the largest analytical blind spot - Boswell does not file.

The dividend tells us a little: The 2025 cut from $5.00 to $3.75/quarter, then the 2026 restoration to $5.00 ($20/yr, ~$19.3M), is a small but genuine signal: the company tightened cash in 2025 (orchard capex, thin farm margins, or water-year economics) and is comfortable distributing again in 2026. It is consistent with a slow pivot from accumulation toward distribution.

Asset 6: Mineral, Oil & Gas Rights

Full/fractional subsurface interests across California and Oregon, with the ~23K Kern acres carrying the most likely value. Nominal $20–100M; separable to a royalty buyer in a liquidation. No new data this period.

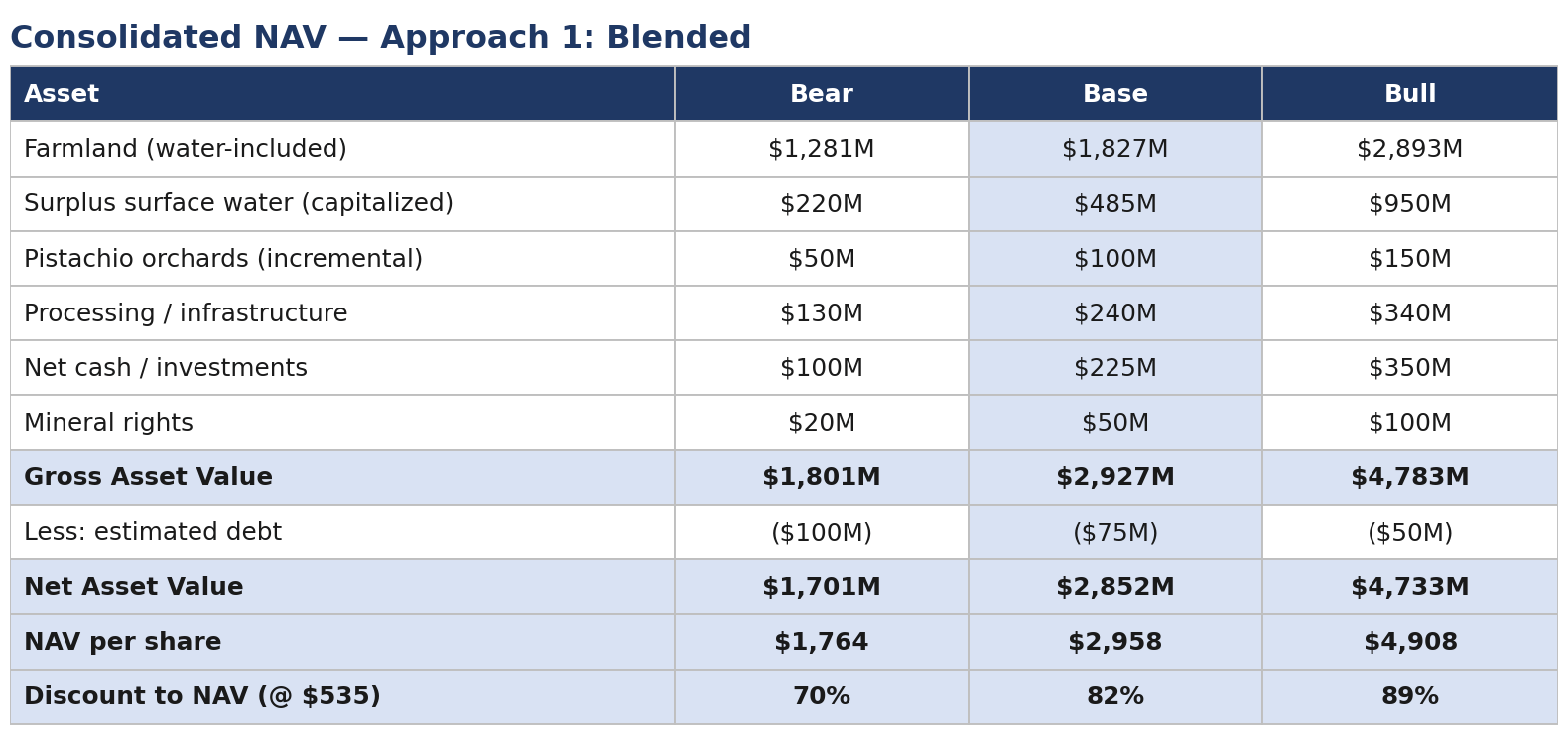

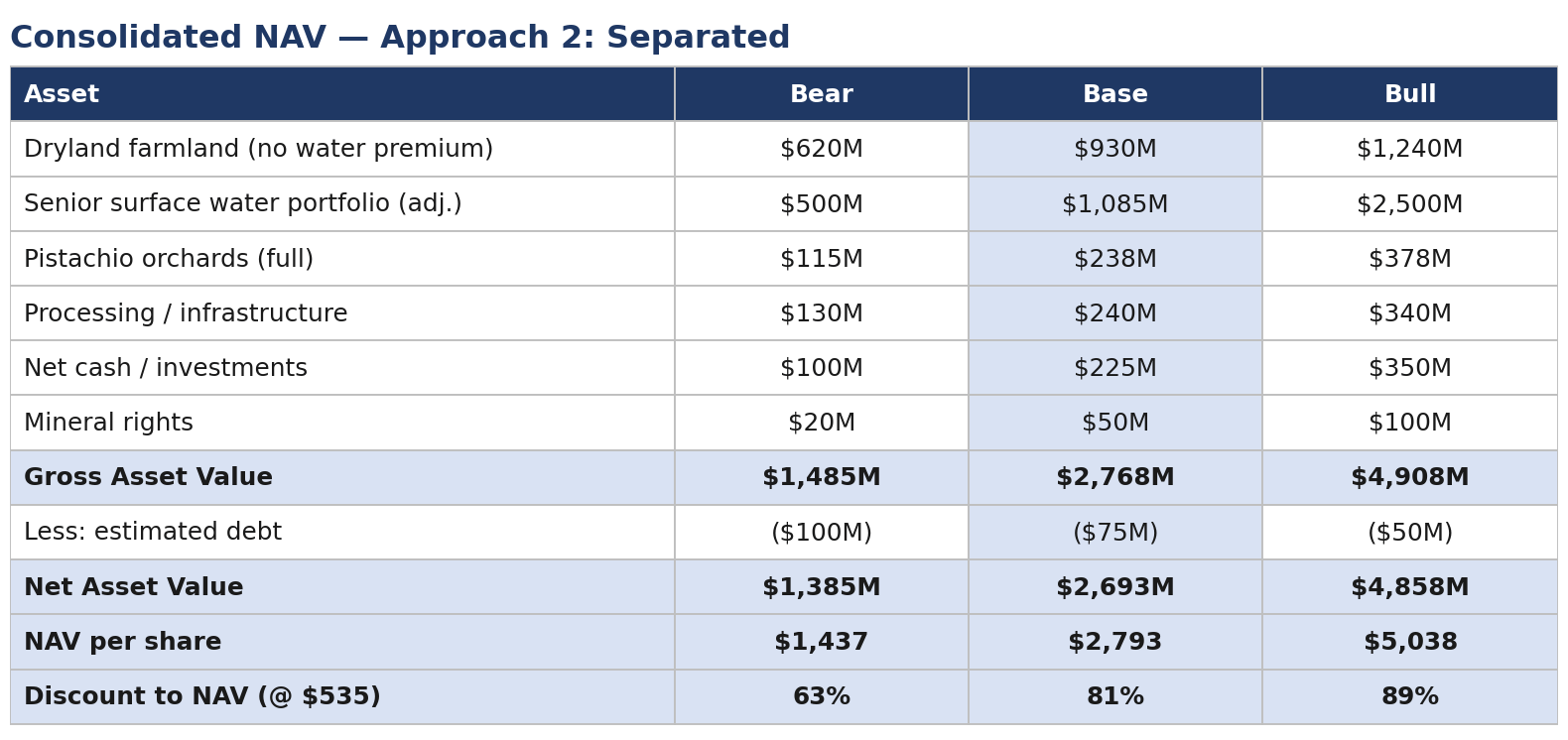

Consolidated NAV - Updated

Approach 1: Blended (avoids water/land double-count)

Approach 2: Separated (water valued independently)

Reconciliation

Both approaches still land in a ~$2,800–$2,960 base-case NAV - roughly 5.3× the $535 price, an ~82% discount. The bear case (~$1,400–$1,760) implies the stock trades at 30–37 cents on the dollar even on pessimistic assumptions.

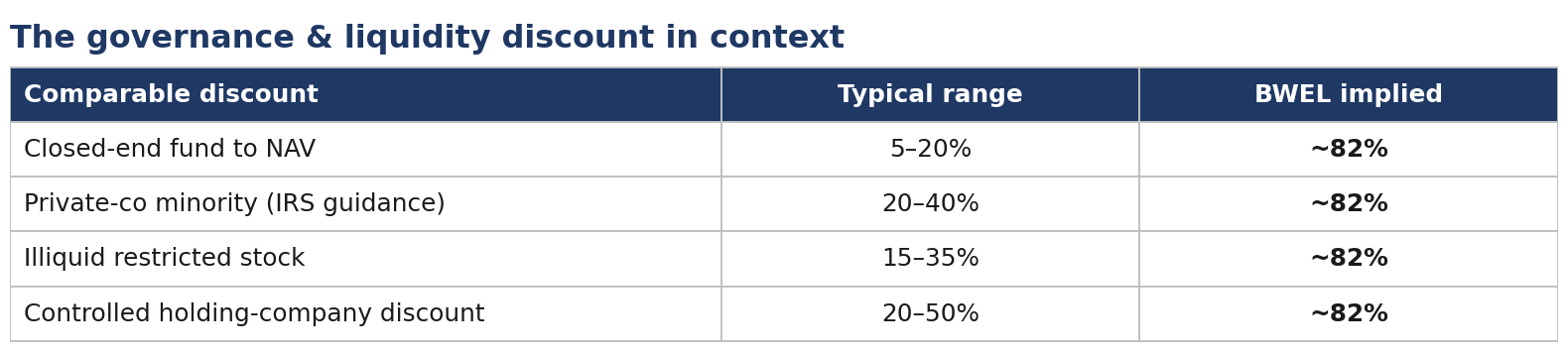

The Governance & Liquidity Discount

The structural objection is unchanged: a $2,900 NAV is academic if the family never unlocks it. No SEC filings, ~hundreds of shares of daily volume, no governance rights, indefinite holding period. At ~$535 against a ~$2,900 base NAV, the market already applies an ~82% discount - wider than virtually any closed-end fund, restricted-stock, or family-holding-company comparable, all of which cluster at 5–50%.

The right way to read the ~82% discount: it is the market saying bluntly: “they will never monetize”. The market pricing the senior water as if it stays locked inside the farm forever. Any evidence of monetization re-rates a discount that currently assumes “never.”

The TPL precedent: An archaic, opaque structure is not disqualifying

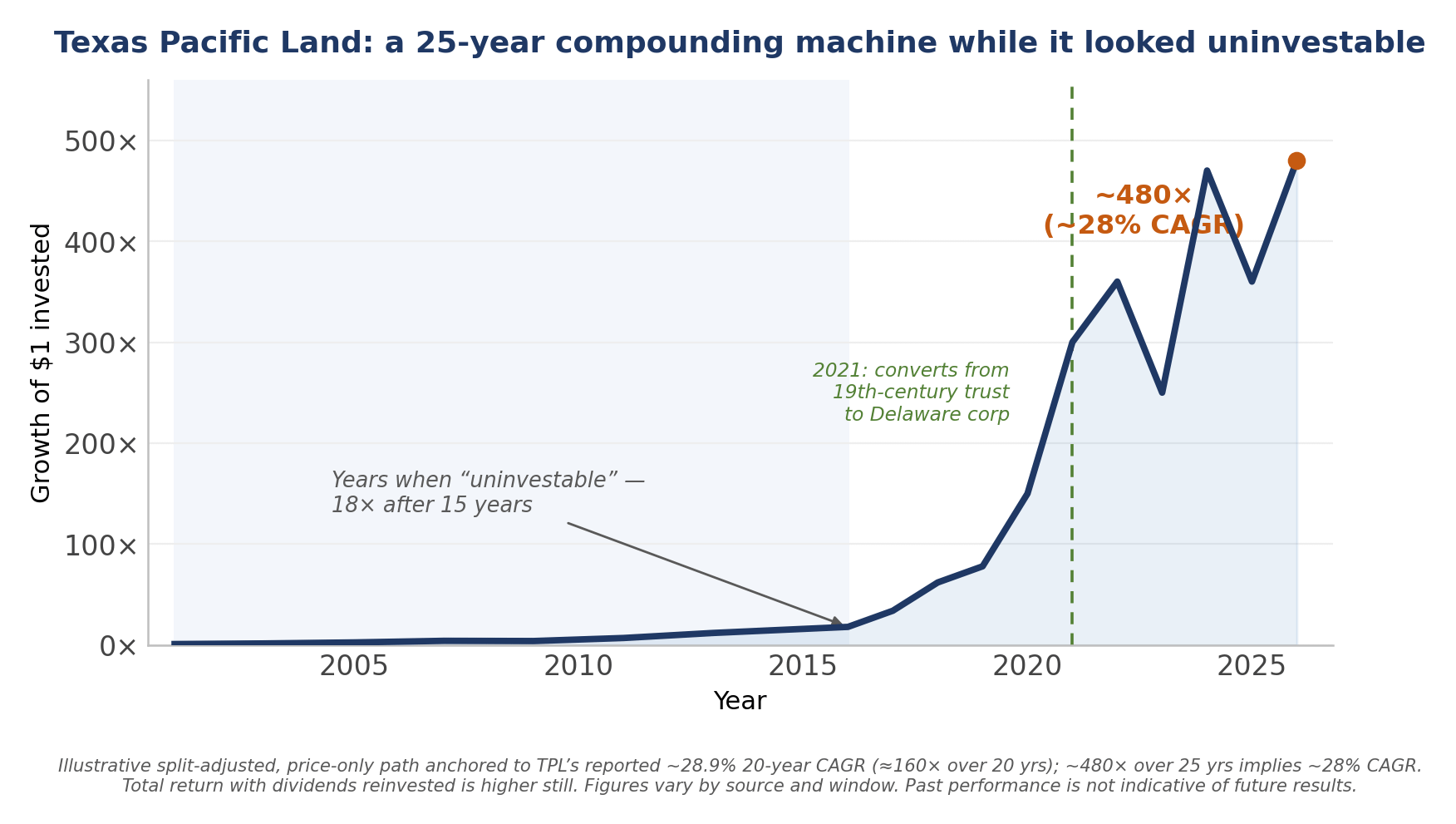

Boswell’s opacity feels like a permanent value trap, but the closest precedent argues the opposite. Texas Pacific Land spent more than a century as a 19th-century business trust - an archaic, minimally-governed structure, run by a tiny handful of trustees, that most institutions couldn’t or wouldn’t touch - sitting on vast, under-monetized Permian land and water rights. It only converted to a conventional Delaware corporation in January 2021.

Over that long stretch as an unloved oddity, TPL was one of the best-performing U.S. equities in existence: it returned 480x over a 25-year period (~28.5% CAGR), driven by the same engine proposed here - scarce real assets, especially water, slowly re-rating as they got monetized and recognized

The most patient public exponent of that idea was the late Murray Stahl (1953–2026, RIP), co-founder of Horizon Kinetics - TPL’s largest shareholder. Horizon held TPL for decades on an ultra-low-turnover basis, content to do essentially nothing and let the asset compound. Writing to clients in late 2019, after years of owning it, Stahl captured the discipline plainly:

“There have been periods measuring in years during the time we’ve held Texas Pacific Land Trust when nothing had changed.” - Murray Stahl, Horizon Kinetics Q4 2019 commentary

That is the temperament Boswell asks of an owner: the willingness to hold a scarce, mispriced asset through long stretches of nothing, because the eventual re-rating dwarfs the wait.

The lesson is that TPL compounded at a high rate for decades precisely while it looked uninvestable. Boswell offers a similar asset base (scarce land + senior water) at a similar starting point of neglect.

Catalysts

Risk Matrix

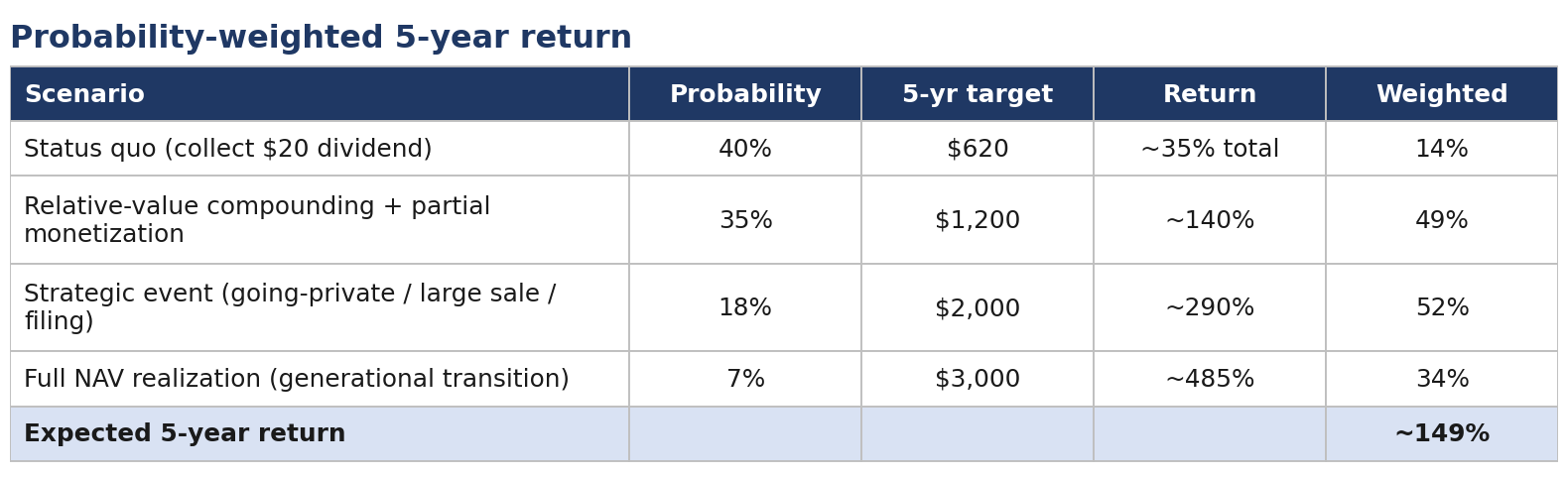

Probability-Weighted Return

The weighting leans toward regulation-driven outcomes rather than a forced family sale. “Relative-value compounding” carries the most weight because SGMA drives it without any management action. The asymmetry is intact: the downside is a hard-asset floor the market already prices below.

Even with 40% weight on dead-money status quo, the expected 5-year return is ~150% because the upside scenarios are so asymmetric and the downside is bounded by hard assets. The market already pays nothing for the water, so the downside is limited. The base case is natural compounding of value. For Boswell, SGMA squeezes its neighbors’ groundwater-dependent land while leaving its senior surface rights untouched - so its water rights inevitably become more valuable.

Conclusion

The asset case is stronger than it was 6 months ago: farmland appears to have bottomed with water-secure land decoupling upward, pistachios firmed, the dividend was restored, and the value floor is intact. What stands out is the simplicity of the mispricing.

Back out cash, processing, pistachios, and minerals from the ~$516M market value and the residual price of Boswell’s ~207,000 acres is a few hundred dollars an acre - below bare dryland - with the senior water rights valued at zero. The market is paying for a dry farm and getting one of the most senior water portfolios in the most water-stressed farm region in America for free.

Two forces now make that water demonstrably scarcer: SGMA will mechanically increase the value of senior water rights for the next 5–15 years, while the Colorado River reset landing by October 2026 cuts Southern California’s imported supply. Neither requires Boswell to lift a finger.

The margin of safety is that the market assigns no value to the water. The upside is scarcity with an enforcement mechanism. The risk is, as ever, the timeline - but with senior water rights, time is on your side.

This reminds me somewhat of TRC. Similar market cap....$529 million. In TRC the inherent "value" has seemingly been trapped forever by litigation and a never ending approval process for development. I have the opinion it too is worth multiples if ever unlocked.

Thanks