FRP Holdings (FRPH) | Part 1 : Deeply Discounted Collection of Scarce Assets

40%+ Discount to NAV | Mining Royalties, DC Waterfront, and Industrial Land (Oh My!)

FRP Holdings, Inc. (NASDAQ: FRPH) is a Jacksonville, Florida-based real estate holding company that operates across four segments: Mining Royalty Lands, Multifamily, Industrial & Commercial, and Development. The company is the modern-day descendant of Florida Rock Industries, which was founded by the Baker family in 1929 and sold to Vulcan Materials for $4.2 billion in 2007. The real estate and mining royalty assets were retained and spun off into what is now FRP Holdings, with the Baker family remaining the largest shareholder and steward of the business.

FRPH trades at approximately $20.85 per share as of mid-March 2026, implying a market capitalization of roughly $398 million. The company’s own sum-of-the-parts analysis, published quarterly, values the enterprise at $693M–$783M, or $36.27–$40.96 per share. This represents a 43–49% discount to management’s NAV. We believe an independent, conservative NAV analysis supports a range of $33–$45 per share, with significant upside optionality embedded in the DC waterfront development pipeline, the Estero mixed-use project, and the irreplaceable Florida aggregate mining royalties.

The thesis rests on three pillars: (1) a deeply discounted collection of genuinely scarce assets - particularly the 500M+ ton aggregate reserve base and the DC waterfront land bank; (2) a management team with multi-generational alignment through substantial family ownership, now actively pivoting from a passive holding structure toward a growth-oriented, NOI-doubling strategy; and (3) a visible development pipeline that, upon stabilization, would more than justify a $1 billion enterprise value - the company’s own stated target.

II. Company Overview & History

The Baker Family Legacy

FRP Holdings traces its lineage to Florida Rock Industries, founded by Thompson Baker in 1929. The Baker family built Florida Rock into one of the largest construction materials companies in the southeastern United States. In 2007, Vulcan Materials acquired Florida Rock for $4.2 billion - a deal the Baker family accepted because, in their words, they had a fiduciary duty to minority shareholders, even though they did not want to sell.

The real estate and transportation assets had been spun off from Florida Rock in 1986 into what became Patriot Transportation Holding. In 2015, the transportation business was separated, and the remaining entity was renamed FRP Holdings. Thompson S. Baker II served as CEO until 2017, when he rejoined Vulcan Materials (he is now Vulcan’s president). John D. Baker II, the patriarch’s other descendant, served as Executive Chairman and CEO until the recent generational transition to his son, John D. Baker III, who became CEO. The Baker family collectively controls an estimated 15–20%+ of shares outstanding through direct holdings, living trusts, and family-related entities.

Corporate Structure

FRP Holdings operates through two subsidiaries: FRP Development Corp. and Florida Rock Properties, Inc. The business is organized into four reporting segments:

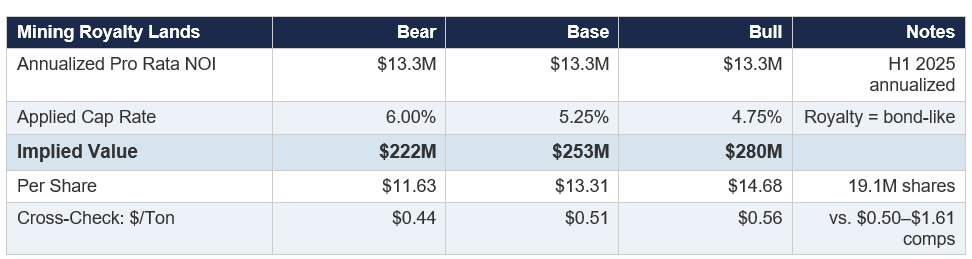

Mining Royalty Lands: The crown jewel. Approximately 16,648 acres across Florida, Georgia, and Virginia, sitting on 500M+ tons of aggregate reserves. These properties are leased to Vulcan Materials, Martin Marietta, Cemex, Argos, and The Concrete Company in exchange for royalty payments typically structured as a percentage of revenue (~10%) with minimum annual payments. Annualized pro rata NOI is approximately $13.3M.

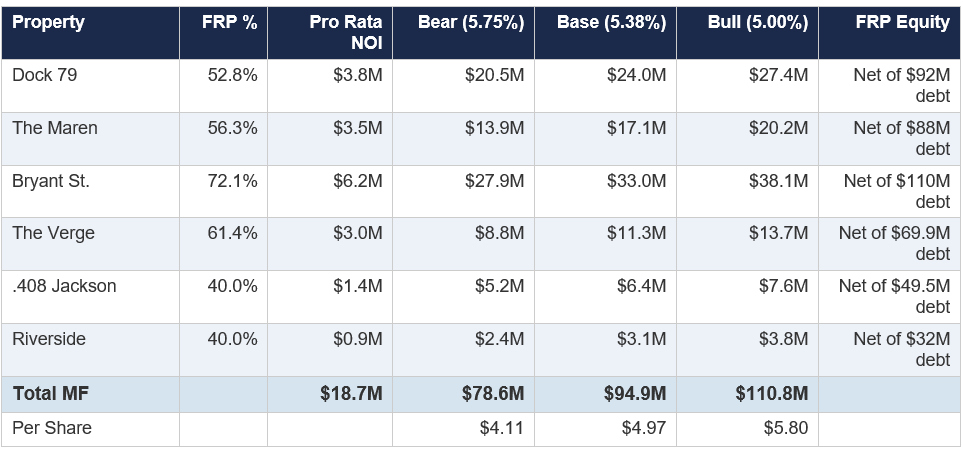

Multifamily: A portfolio of six apartment communities, primarily in the Washington, DC, Capitol Riverfront and Buzzard Point submarkets, as well as Greenville, SC. Properties include Dock 79, The Maren, Bryant Street, The Verge, .408 Jackson, and Riverside, held through consolidated and unconsolidated joint ventures with MRP Realty. Total annualized pro rata NOI is approximately $18.7M.

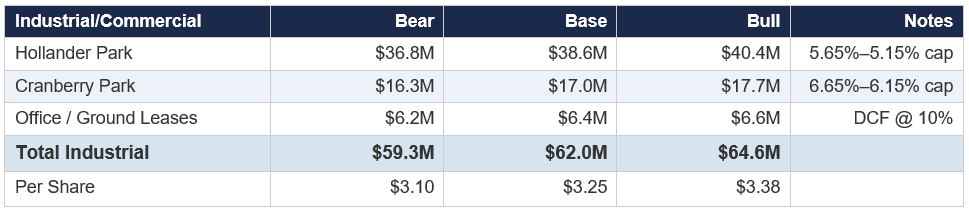

Industrial & Commercial: Ten warehouses across four locations in the Baltimore-Washington corridor, two ground leases, and one office building. Total annualized pro rata NOI is approximately $3.2M, though this segment is undergoing a dramatic expansion from 550,000 sq ft to 2.7M sq ft through the development pipeline.

Development: Owns land parcels in various stages of entitlement, permitting, and construction. Key projects include the Chelsea Road warehouse (completed April 2025), Lakeland and Davie FL industrial projects (now 100% owned post-Altman acquisition), Lake County FL industrial JV, and the Estero FL mixed-use master plan.

III. Asset-by-Asset Net Asset Value Analysis

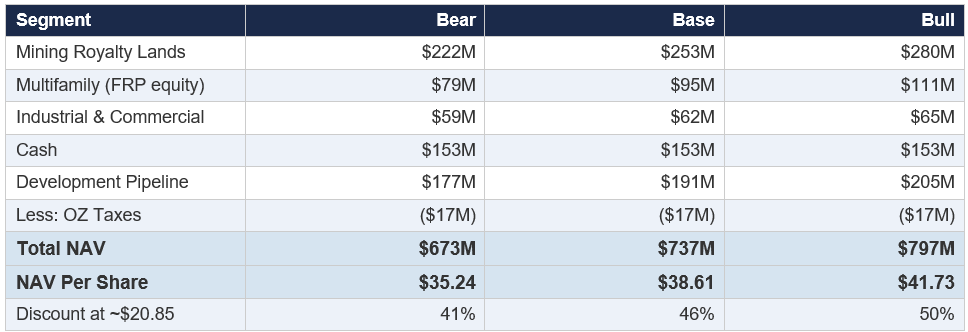

The following NAV analysis is constructed on an asset-by-asset basis, incorporating management’s own detailed quarterly valuation framework supplemented by independent cap rate ranges, comparable transactions, and our own scenario analysis. We present Bear, Base, and Bull cases for each segment.

A. Mining Royalty Lands

The mining royalty segment is the most underappreciated and irreplaceable asset within FRP Holdings. The company owns approximately 16,648 acres (plus 4,280 acres through a JV with Vulcan in Brooksville, FL) containing over 500 million tons of aggregate reserves. Nine quarries are actively mined; four are leased but not yet mined. Reserve life is estimated at 60+ years, with management privately indicating that reserves have not declined in recent years despite ongoing depletion - suggesting actual reserve life of 80–100 years as deeper deposits are discovered.

Royalty payments are structured as approximately 10% of tenant revenue per ton, with minimum annual rental floors. Tenants include Vulcan Materials, Martin Marietta, and Cemex - three of the four largest aggregate producers in North America. The FRP royalty model is the purest form of a landowner royalty: zero operating costs, zero capex, zero environmental liability (borne by the tenant/operator), and a contractual revenue stream that inflates with aggregate pricing.

Comparable Transactions

Martin Marietta acquired Bluegrass Materials in 2018 for $1.64 billion, which valued 2.2 billion tons of reserves at $0.75/ton. Martin Marietta acquired Texas Industries for $2.7 billion, valuing 1.68 billion tons at $1.61/ton. Vulcan entered volumetric production deals with Plum Creek Timber at values implying $0.50–$0.75/ton. Applying these benchmarks to FRP’s 500M+ ton reserve base yields a range of $250M–$800M on a reserve-value basis alone. However, these comps value integrated operations, not pure royalty streams, which arguably deserve a premium due to zero operational risk.

Even our Bear case values the mining royalties at the very low end of comparable transaction ranges on a per-ton basis, underscoring the conservatism of this approach. The revenue-generating capacity of these reserves will only grow over time as aggregate scarcity intensifies in Florida’s high-growth markets where new quarry permitting is extraordinarily difficult.

B. Multifamily Portfolio

The multifamily portfolio is concentrated in Washington, DC’s Capitol Riverfront and Buzzard Point submarkets - an area that has undergone a dramatic transformation over the past decade, anchored by Nationals Park and the broader Anacostia waterfront redevelopment. FRP holds its multifamily assets through JVs with MRP Realty, with ownership percentages ranging from 40% to 72.1%.

C. Industrial & Commercial

D. Cash & Net Working Capital

The $153M cash position represents a staggering 38% of the entire market capitalization. This provides substantial dry powder for development capital deployment, opportunistic acquisitions, and downside protection. Management has explicitly stated a target of deploying ~$71M in development equity annually.

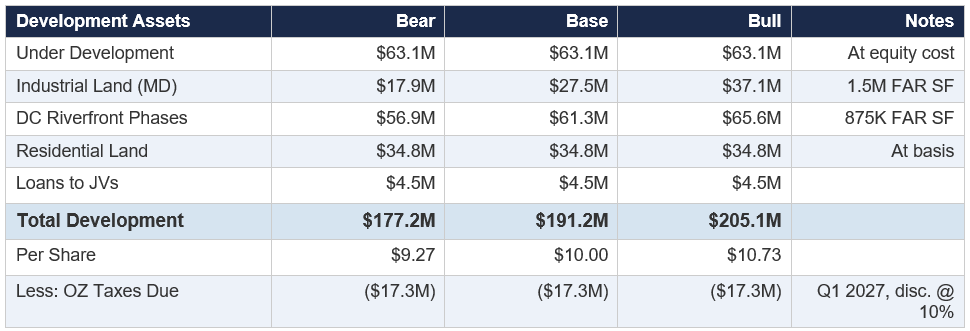

E. Development Pipeline & Land Bank

F. Consolidated NAV Summary

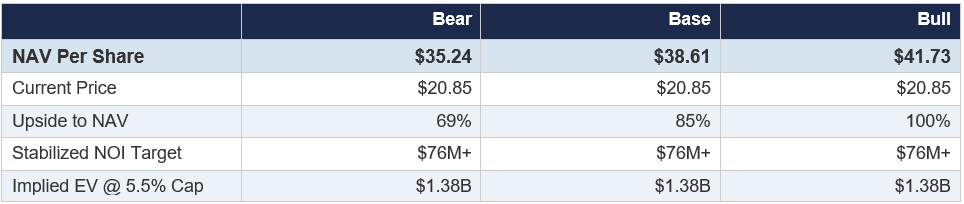

At ~$20.85, the market is pricing FRP Holdings at a 41–50% discount to our NAV range. Even our Bear case - which uses wide cap rates, values mining reserves at well below comparable transaction benchmarks, and assigns no premium to development optionality - implies 69% upside to the current share price.

IV. Management Quality & Incentive Alignment

The Baker Dynasty: Generational Stewardship

The Baker family has been in the aggregate, real estate, and construction materials business since 1929. Their track record is exceptional: building Florida Rock Industries into a multi-billion-dollar enterprise and executing a $4.2 billion sale to Vulcan Materials at a highly attractive price. The family subsequently built Bluegrass Materials and sold it to Martin Marietta in 2018 for $1.64 billion. These are not managers who dabble in real estate - they are deeply embedded operators with nearly a century of industry knowledge.

The company is now in the midst of a generational leadership transition. John D. Baker II serves as Executive Chairman, while his son, John D. Baker III (40 years old, Princeton/UT McCombs MBA), has stepped into the CEO role. This is a critical inflection point: the younger Baker appears to be driving a more growth-oriented, proactive strategy, including the Altman Logistics acquisition, the first-ever Investor Day (May 2025), a redesigned investor relations website, and an explicit commitment to double NOI within five years and push the SOTP valuation above $1 billion.

Insider Ownership & Alignment

The Baker family collectively holds an estimated 15–20%+ of shares outstanding through direct ownership, living trusts, and family entities. Recent insider activity has been materially supportive: John D. Baker II purchased $10 million of stock at $29.00/share and an additional $99K at $23.70/share in late 2025. Director John D. Baker II also purchased 7,175 shares for $171K and 854 shares for $20K in November 2025. In January 2026, John D. Baker III received 54,824 shares as an intergenerational family gift, bringing his total holdings to over 313,000 shares. This kind of meaningful insider buying - particularly the $10M purchase at $29, well above the current price - is a powerful alignment signal.

Compensation Structure

Executive compensation is modest by public-company standards. CEO Baker III’s 2024 compensation included option grants of $350K (vesting over 4 years with 10-year terms), a $10,350 401(k) match, and negligible other compensation. Director compensation consists primarily of equity awards (~78% equity, ~22% cash), reinforcing alignment. The absence of any dividend payout and the family’s willingness to forgo current income in favor of long-term compounding speaks volumes about their time horizon.

Strategic Pivot: From Sleepy Holdco to Active Developer

Historically, FRP Holdings was perceived as a sleepy, asset-rich holding company content to collect mining royalties and manage its DC apartment portfolio. Under the younger Baker’s leadership, the company is undergoing a strategic evolution. The Altman Logistics acquisition in October 2025 ($33.5M purchase price, $23.6M net cash) brought in a seasoned industrial development team, added ~1.3M sq ft of warehouse pipeline across Florida and New Jersey, and gave FRP 100% ownership of its Lakeland and Davie projects. Management has explicitly stated a target of delivering three new industrial assets every two years and expanding the industrial platform from 550,000 sq ft to 2.7M sq ft.

V. Why the Market May Be Missing This - And What Could Drive a Re-Rating

What the Market Is Missing

1. Mining Royalties Are Deeply Mispriced

The mining royalty stream generates $13.3M of annualized pro rata NOI with zero capex, zero operating expenses, and multi-decade reserve life. On a per-ton basis, our NAV assigns $0.44–$0.56/ton to FRP’s reserves versus $0.75–$1.61/ton in comparable M&A transactions. Critically, Florida’s aggregate reserves are depleting and new quarry permits are extraordinarily difficult to obtain due to environmental and land-use restrictions. This is a classic scarcity asset: the supply of permitted aggregate reserves in high-growth Florida markets is declining while demand from construction and infrastructure spending (IIJA, state DOT budgets) is rising. The market appears to price these royalties as if they were an ordinary real estate income stream rather than an irreplaceable, inflation-protected natural resource.

2. The DC Waterfront Land Bank Is Hidden in Plain Sight

FRP’s Capitol Riverfront footprint extends well beyond the stabilized apartment buildings. Phases III and IV of the Riverfront on the Anacostia development, plus the 664E site (currently leased to Vulcan Materials in Buzzard Point), represent 875,000 FAR square feet of entitled or entitleable land. In November 2022, FRP executed an agreement with Steuart Investment Company and MRP Realty for the development of up to 10 mixed-use projects comprising 3,000+ residential units and 150,000 sq ft of retail across Capitol Riverfront and Buzzard Point. At the Maren/Verge land comps of $65–$75/FAR SF, these future phases alone are worth $57M–$66M. The market assigns essentially no premium beyond the stated land comp value, ignoring the substantial development margin and NOI generation potential.

3. Cash Is 38% of Market Cap

The $153M cash position provides enormous optionality. Management has demonstrated discipline with the Altman acquisition ($23.6M net cash for a 15–20%+ IRR pipeline) and the Aberdeen Overlook lending venture (36% profit on drawn funds). This is not dead capital - it is being deployed at attractive returns into a proprietary development pipeline.

4. The Industrial Expansion Is Transformational But Unrecognized

The industrial platform is growing from 550K sq ft to 2.7M sq ft - a 5x expansion. The four key near-term industrial projects (Perryman/Cecil Co, Lakeland, Davie, Harford Co) represent 850,000 sq ft with a $146M project cost and projected stabilized NOI of $8.7M–$10.2M (FRP share: $7.9M–$9.2M). At a 5.5% cap rate, this NOI stream would be worth $144M–$167M, generated from $146M in project cost essentially creating value at cost. The Altman Logistics minority interests in 510K sq ft of NJ/FL projects are expected to deliver 2x MOIC upon sale.

Potential Re-Rating Catalysts

Near-Term (2026–2027): Chelsea Road warehouse lease-up and stabilization; Lakeland and Davie industrial project completions (summer 2026); Cecil County MD permits (early 2026); Aberdeen Overlook lot sale completion and profit realization ($11.2M expected); DC waterfront entitlement progress enabling vertical construction by 2027; delayed Q4 2025 earnings release and Altman integration update.

Medium-Term (2027–2029): Harford County industrial construction; Estero, FL mixed-use project stabilization (596 units, hotel, commercial - a potential $300M+ project); Woven Greenville SC lease-up (214 units); industrial NOI doubling as pipeline delivers; potential institutional discovery as company crosses critical NOI and market cap thresholds.

Structural / Event-Driven: Potential REIT conversion (would force dividend payout and access a much broader investor base - management has not discussed this publicly but the asset mix is REIT-eligible); increased sell-side coverage (currently only 3 analysts); Baker family take-private (less likely given growth ambitions, but the discount is wide enough that it would be highly accretive); strategic sale of mining royalties to a Vulcan/Martin Marietta at per-ton values far above implied market price.

VI. Are These Truly Scarce Assets?

Mining Royalties: Unequivocally Scarce

Florida aggregate reserves are a textbook scarcity asset. New quarry permits in Florida take years to obtain and face intense environmental and political opposition - the state’s Lake Belt mining region has been the subject of protracted litigation for decades. FRP’s 13 quarries across Florida, Georgia, and Virginia represent a portfolio that would be virtually impossible to replicate today. Aggregate is expensive to transport (a truck can only economically haul aggregate ~50 miles), making proximity to high-growth markets like Orlando, Tampa, Fort Myers, and Jacksonville irreplaceable. The 500M+ tons of reserves with 60–100 years of life represent a generational asset that literally cannot be rebuilt.

DC Waterfront Land: Scarce Within Submarket

The Capitol Riverfront/Buzzard Point area has been one of DC’s fastest-growing submarkets, driven by Nationals Park, The Yards, the new Frederick Douglass Memorial Bridge, and the Anacostia Riverwalk Trail. Available development sites are finite and shrinking. FRP’s 875,000 FAR SF of future development capacity represents a meaningful share of remaining buildable waterfront land in the submarket. This is scarce in the local market context, though not irreplaceable in the way that mining reserves are - there are other multifamily and mixed-use development opportunities in the greater DC area.

Industrial Land in I-95 Corridor: Moderately Scarce

The Cecil County and Harford County MD industrial land positions are well-located along the I-95 logistics corridor between Baltimore and Philadelphia. While not irreplaceable, the combination of entitlement progress, scale (900K+ SF distribution center potential), and proximity to major population centers makes these parcels attractive in a market where new industrial land with permits is increasingly constrained.

Estero / Florida Multifamily: Optionality, Not Scarcity

The Estero, FL mixed-use development (596 units, 60K sq ft commercial, 20K sq ft office, 190-key hotel on 46 acres) is a large, ambitious project but not a scarce asset per se. Its value is driven by execution, market timing, and the quality of the JV partnership rather than irreplaceability.

VII. Key Risks & Bear Case Considerations

Governance and Key-Man Risk. FRP is a family-controlled company with limited independent oversight. The Baker family’s interests are generally aligned with minority shareholders, but the concentrated control structure limits external accountability. The generational transition introduces execution risk - John Baker III is relatively young and untested as a public-company CEO, though early signals (Altman acquisition, Investor Day, strategy articulation) are encouraging.

No Dividend / Reinvestment Risk. FRP pays no dividend, and the stock has underperformed the S&P 500 and the broader real estate sector over the past year (-7.9% weekly drop recently, 52-week range $20.61–$29.47). Shareholders are entirely dependent on NAV accretion and eventual price convergence. If management’s development projects deliver below-target returns or encounter delays, the lack of current income magnifies the opportunity cost of holding.

DC Multifamily Headwinds. The Washington, DC multifamily market has experienced elevated vacancy rates and collection challenges in recent years. While FRP’s properties are stabilizing, the DC market faces supply risk from new deliveries and demand uncertainty tied to federal government workforce changes. NOI growth in this segment has been sluggish (2% YTD through H1 2025).

Industrial Execution Risk. The 5x expansion of the industrial platform is ambitious. Permitting delays (Cecil County has already been pushed back), construction cost inflation, and leasing risk in a softening industrial market could reduce returns. The Altman Logistics integration adds complexity and will temporarily inflate G&A.

Illiquidity. Average daily trading volume is roughly 56K–89K shares ($1.2M–$1.9M daily dollar volume). Institutional investors seeking large positions will face significant market impact. This illiquidity partially explains the persistent discount but also limits the shareholder base to patient, long-term holders.

Tariff and Construction Cost Risk. Management has flagged tariff exposure on industrial tenants and construction costs as risk factors. Elevated input costs could delay or compress returns on development projects.

VIII. Conclusion & Valuation Summary

FRP Holdings is a multi-generational, family-controlled real estate company trading at a 41–50% discount to a conservatively constructed net asset value. The market is systematically undervaluing three distinct sources of embedded worth:

First, the mining royalty portfolio - a zero-cost, inflation-protected, multi-decade revenue stream sitting on 500M+ tons of irreplaceable Florida aggregate reserves - is priced at a fraction of comparable transaction values. This is not a cyclical real estate asset; it is a natural resource royalty with the longevity and scarcity profile of a West Texas mineral interest.

Second, the DC waterfront land bank and the nascent industrial development pipeline represent hundreds of millions of dollars in future value creation that the market assigns essentially zero premium to. Management’s stated goal of doubling NOI within five years and pushing the SOTP above $1 billion is credible given the identified project pipeline and the capital available for deployment.

Third, the $153M cash position - larger than the entire implied value the market assigns to every asset outside of mining - provides both downside protection and offensive capital for a management team that has demonstrated discipline (Altman at 15–20%+ IRR, Aberdeen Overlook at 36% return on drawn funds).

Valuation Framework

The variant perception here is straightforward: the market is treating FRP Holdings as a sleepy, illiquid, income-deficient holding company. The reality is that it is a well-capitalized, family-aligned, asset-rich enterprise on the cusp of a multi-year transformation that should organically close the NAV discount as development projects stabilize, NOI doubles, and the asset quality becomes undeniable. The mining royalties alone, valued on a per-ton basis consistent with M&A precedent, would justify the entire current market capitalization - everything else (DC apartments, industrial, cash, development pipeline) is effectively free.

For patient capital willing to underwrite a 3–5 year holding period, FRP Holdings offers asymmetric risk/reward with genuine scarcity characteristics, deep family alignment, and visible catalysts for value recognition.

Hello Groundbreaker, have you looked into the debt on the DC properties ? I took a quick look, the terms seem favorable until 2033. That would be an important addition and clarification to your thesis IMO.

In general, I always love royalties, especially long term ones.

The setup you’re describing sounds good, but has a lot of variables and risks involved from my perspective. There are cleaner possibilities if you want to invest in a royalty company, and bets I would rather take if I want to bet on the CEO and management.