Canterbury Park (CPHC) | Regional Racetrack & Casino

50% NAV Discount | Real Estate Developer Disguised as a Micro-Cap Racetrack

Canterbury Park Holding Corporation (NASDAQ: CPHC) is a micro-cap company trading at $15.50 per share with a market capitalization of approximately $80 million. On the surface, it appears to be a modestly profitable horse racetrack and unbanked card casino in Shakopee, Minnesota. In reality, CPHC is a real estate development company in the early-to-middle innings of monetizing approximately 140 acres of prime, entitled suburban land in one of the fastest-growing counties in the state of Minnesota - disguised as a gaming operation that most institutional investors cannot or will not own.

The thesis is straightforward: the market values CPHC based on its declining operating EBITDA of approximately $9.4 million while assigning negligible or zero value to its balance sheet assets, which include $17 million in cash, $20 million in TIF receivables, equity interests in multiple real estate joint ventures, $5 million in member loans, and approximately 50 acres of undeveloped land carried at cost on the books. Management itself has stated that cash, TIF receivables, and JV contributions alone are worth over $10.50 per share - roughly 68% of the current stock price - before attributing any value to 50 acres of unbooked land or the operating business itself.

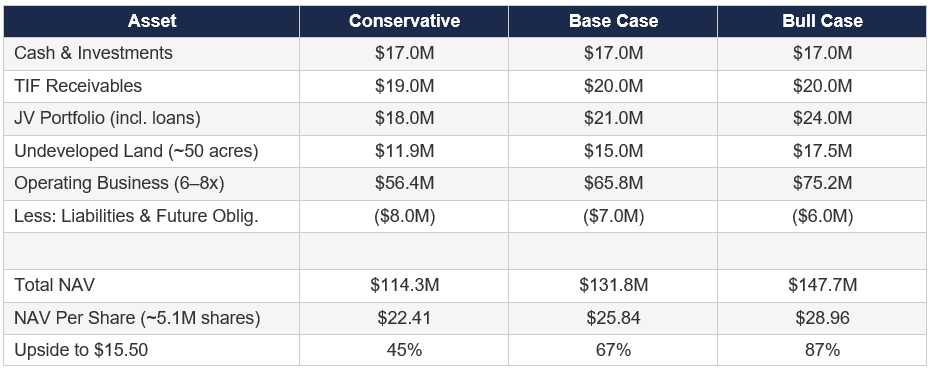

We estimate the company’s net asset value at $25 to $30+ per share, implying 60–100%+ upside from the current price. The asymmetric upside is driven by multiple near-term catalysts: the June 2026 opening of a 19,000-seat Live Nation amphitheater adjacent to the property, accelerating TIF reimbursements, rising JV occupancy approaching cash-flow breakeven, and approximately 25 acres of newly road-accessible prime land adjacent to the amphitheater that management plans to develop into hospitality, entertainment, and commercial uses.

Core Thesis: What the Market is Missing

The market sees a declining racino with ~$9M EBITDA. What exists beneath the surface is a debt-free balance sheet with $10.50+/share in liquid and semi-liquid assets, ~50 acres of entitled development land at cost, JVs reaching stabilization, and a Live Nation amphitheater catalyst opening in 3 months. The stock trades as if the real estate does not exist.

Company Overview

Canterbury Park Holding Corporation, headquartered in Shakopee, Minnesota, owns and operates Canterbury Park Racetrack and Casino, the only thoroughbred and quarter horse racing facility in the state. The company was founded in 1994 when a group of investors led by Randall Sampson acquired the formerly bankrupt Canterbury Downs facility. The company has been publicly traded on NASDAQ under the ticker CPHC since its inception. It operates through four reportable segments: Horse Racing, Casino, Food and Beverage, and Real Estate Development.

Operating Business

The Horse Racing segment offers live thoroughbred and quarter horse racing from May through September and year-round simulcast wagering. The Casino segment operates 24/7 unbanked card games including poker and table games. Critically, Canterbury operates an unbanked card casino, meaning the house does not participate in the games; revenue is derived from collection fees charged to players. This is an important distinction: Minnesota law prohibits Canterbury from offering slot machines or banked table games, which limits the casino’s earnings power relative to a full-service gaming operation. The Food and Beverage segment operates concessions, restaurants, bars, a buffet, and catering services across the property.

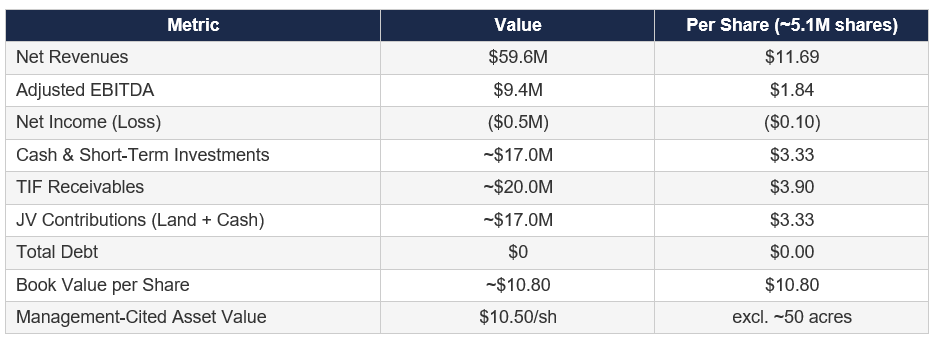

For full-year 2025, the company reported net revenues of $59.6 million (down 3.2% year-over-year) and Adjusted EBITDA of $9.4 million (down 12.9%). The company reported a net loss of $529,000, primarily driven by equity-method losses from its real estate joint ventures. The operating decline stems from two factors: the 2023 expiration of purse subsidies from the Shakopee Mdewakanton Sioux Community (SMSC) that had supported racing purses, and increased regional gaming competition.

Canterbury Commons Development

In 2018, Canterbury received regulatory approval to redevelop approximately 140 acres of underutilized land surrounding the racetrack into a mixed-use community known as Canterbury Commons. The vision is to create a “live, work, play, and stay” destination anchored by the existing racetrack and casino. Since then, the company has executed a disciplined capital-light development strategy, contributing land as equity into joint ventures with experienced developers rather than taking on construction risk and debt directly. The development to date includes nearly 1,000 residential units across multiple projects, four restaurants, a brewery, two entertainment venues, 57,000 square feet of commercial office space, and a 19,000-seat amphitheater under construction. Approximately 50 acres remain for future development.

Key Financial Summary (FY2025)

Net Asset Value: Asset-by-Asset Build-Up

The critical analytical framework for CPHC is not an earnings multiple but a bottoms-up net asset value approach. The company’s assets fall into six distinct categories, each requiring separate valuation treatment. The market’s failure to properly value these assets - many of which are carried at historical cost or generate equity-method accounting losses that obscure economic value - is the core of the mispricing.

Asset 1: Cash and Short-Term Investments

As of December 31, 2025, the company held approximately $17 million in cash and short-term investments, equating to $3.33 per share. The company carries zero debt. This is a clean, liquid asset that requires no discount.

Asset 2: Tax Increment Financing (TIF) Receivables

When the City of Shakopee approved the Canterbury Commons development in 2018, Canterbury agreed to front the cost of required infrastructure improvements (roads, utilities, grading) in exchange for reimbursement via future property tax revenues generated by the new developments. As of year-end 2025, the company had approximately $20 million in TIF receivables on its balance sheet ($3.90 per share). The company began receiving initial repayments of approximately $580,000 in Q4 2025. Canterbury expects to complete remaining developer improvements by July 2027 and to be reimbursed by no later than July 2027.

We value TIF receivables at book value. The receivables are government-backed obligations linked to verified tax revenues. Canterbury has never applied a loss allowance against this asset, and the commencement of repayments in Q4 2025 validates collectibility. A modest discount for time value would be appropriate but is immaterial given the 1–2 year remaining collection horizon.

Asset 3: Real Estate Joint Ventures (Equity Investments)

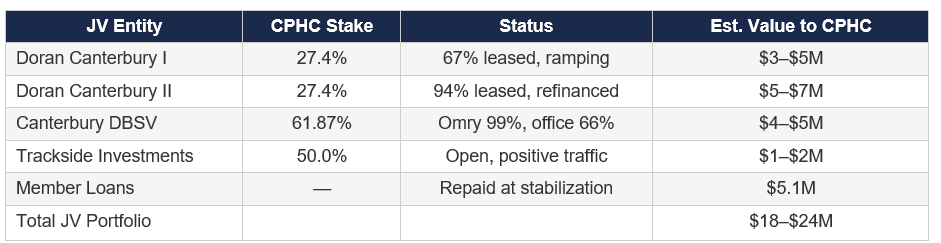

Canterbury’s joint venture portfolio is the most complex and most misunderstood element of the balance sheet. The company holds equity interests in four distinct JV vehicles, all structured as development partnerships where Canterbury contributed land as its primary equity contribution while partners handled construction, financing, and management:

Doran Canterbury I, LLC (27.4% ownership): Phase I of the Triple Crown Residences, a luxury multifamily project. This property experienced construction delays after a fire sprinkler system failed inspection in late 2023, requiring extensive remediation. A certificate of occupancy was granted in early 2025 and the property reached 67% leased by year-end 2025. The project is still ramping, but the trajectory is positive.

Doran Canterbury II, LLC (27.4% ownership): Phase II of the Triple Crown Residences. This property opened in 2024 and has leased rapidly, reaching 94% occupancy by year-end 2025. The strong leasing allowed the property to refinance in January 2026, a significant milestone that validates the underlying asset value and positions the JV for potential distributions.

Canterbury DBSV Development, LLC (61.87% ownership): The Greystone-partnered development encompassing the southwest portion of Canterbury Commons. This includes The Omry (147-unit senior market-rate apartments at 99% occupancy), a 28,000 sq. ft. commercial office building (66% leased), and additional commercial space. The Omry’s near-complete lease-up is a strong signal of demand depth in this submarket.

Trackside Investments, LLC (50% ownership): This venture developed the Boardwalk Kitchen & Bar, a 6,000 sq. ft. upscale restaurant and bar with an 18,000 sq. ft. patio featuring trackside views. It opened in summer 2025 and reported positive initial patronage.

On a GAAP basis, these equity investments are carried at approximately $5.8 million on the balance sheet, reflecting cumulative equity-method losses driven primarily by Canterbury’s share of depreciation, amortization, and interest expense from the Doran ventures. These accounting losses dramatically understate the economic value of the underlying real assets. The Doran Phase II property, for example, is a 94%-leased luxury apartment complex that just refinanced - its enterprise value far exceeds Canterbury’s book carrying value.

We also note Canterbury has made approximately $5.1 million in member loans to these JV vehicles. These will be repaid as the developments reach positive operating cash flow. Additionally, Canterbury has future capital contribution obligations of approximately $6.85 million related to Doran Canterbury I. In aggregate, Canterbury has contributed approximately $17 million in land and cash to its JV portfolio ($3.33 per share).

Valuation: We estimate the fair market value of Canterbury’s aggregate JV interests at $15–$20 million ($2.94–$3.92 per share), reflecting the gap between depressed GAAP book values driven by non-cash depreciation charges and the economic reality of stabilizing multifamily and commercial assets in a high-growth submarket. Phase II’s refinancing alone validates significant embedded value. As Phase I finishes leasing and the portfolio reaches stabilization, GAAP equity-method income should turn positive, providing an earnings catalyst.

Asset 4: Undeveloped Land (~50 Acres)

Canterbury retains approximately 50 acres of entitled, development-ready land that is carried on the balance sheet at historical cost of roughly $2.4 million. This book value bears no relationship to market reality. The most relevant comparable transaction is the May 2023 sale of 37 acres to Swervo Development for the amphitheater project at $237,000 per acre ($8.8 million total). The Greystone JV valued Canterbury’s 13-acre land contribution at $261,000 per acre.

However, the remaining 50 acres are arguably more valuable today than those prior transactions would suggest. Of particular note is the approximately 25 acres of prime land adjacent to the soon-to-open Live Nation amphitheater, which Canterbury has specifically identified for higher-value entertainment, hospitality, and commercial uses. The company has engaged Hunden Partners to conduct a market analysis study identifying highest and best use for these parcels. The opening of a 19,000-seat concert venue operated by Live Nation will fundamentally transform the traffic patterns and commercial viability of adjacent parcels.

We value the 50 acres in a range of $237,000–$350,000 per acre, yielding a range of $11.9–$17.5 million ($2.33–$3.43 per share). The lower bound reflects prior transaction comparables; the upper bound reflects a premium for the amphitheater-adjacent parcels, improved infrastructure, and the flywheel effect of an increasingly developed master-planned community.

Asset 5: Operating Business (Racetrack + Casino + F&B)

The core operating business generated $9.4 million in Adjusted EBITDA in 2025 on $59.6 million of revenue. While this represents a decline from $10.8 million in 2024 and $13.4 million in 2021, the business remains a durable cash generator with competitive protections: Canterbury is the only thoroughbred and quarter horse racing facility in Minnesota, and gaming licenses are effectively irreplicable assets.

We apply a 6–8x EV/EBITDA multiple to the operating business. This is a discount to comparable regional gaming operations, reflecting the unbanked casino structure (no slots, no banked table games), the regulatory ceiling on gaming expansion in Minnesota, and the seasonal nature of live racing. At 6–8x on $9.4 million in EBITDA, the operating business is worth $56–$75 million. The property includes the physical racetrack, grandstand, casino floor, stabling facilities (300+ new stalls), and associated infrastructure on several hundred acres.

Asset 6: Property, Plant & Equipment (Net of Above)

The company’s PP&E is captured within the operating business valuation above. There is no incremental value to add separately, as the racetrack, casino building, barns, and supporting infrastructure are essential to the EBITDA stream and are not separable from the business.

NAV Summary

Implied Value of Operating Business at Current Price

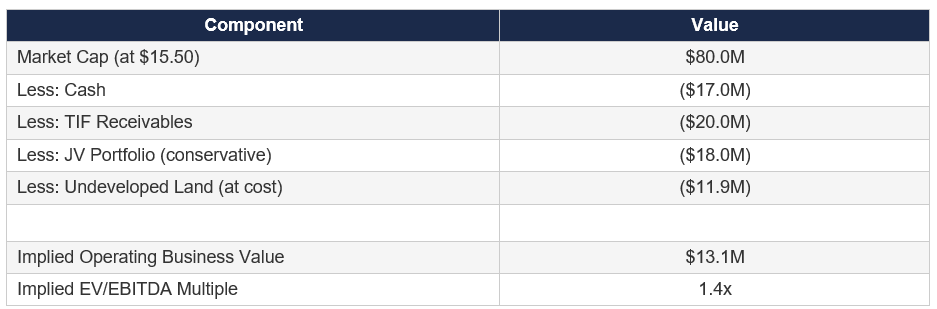

At $15.50 per share ($80M market cap), if we subtract the value of cash ($17M), TIF receivables ($20M), JV interests ($18–21M), and undeveloped land ($12–15M), the market is implying the racetrack, casino, and food & beverage operations - which generate $9.4M in annual EBITDA - are worth approximately $7–13M, or less than 1.5x EBITDA. This is an irrationally low valuation for a cash-generating monopoly gaming asset with an irreplaceable license.

Key Assets Deep-Dive

The Live Nation Amphitheater (Opening June 2026)

Perhaps the most transformative near-term catalyst is the 19,000-seat amphitheater being constructed by Swervo Development Corporation on 37 acres purchased from Canterbury in May 2023 for $8.8 million. The venue will be operated by Live Nation Entertainment, the world’s largest live entertainment company. It is the Twin Cities’ first large-scale outdoor concert venue and is scheduled to open for a full season in June 2026 - just three months from the date of this report.

While Canterbury does not own the amphitheater or retain a direct revenue share, the spillover effects are substantial. A 19,000-capacity venue hosting 40–60+ shows per season will drive hundreds of thousands of incremental visitors to the Canterbury Commons campus annually. This foot traffic directly benefits Canterbury’s casino, food and beverage, and entertainment operations. More importantly, it dramatically enhances the development value of the 25 acres of prime, newly road-accessible land adjacent to the amphitheater. Live Nation-anchored entertainment districts have proven to be powerful catalysts for hotel, restaurant, retail, and mixed-use development nationwide.

The TIF Receivable as a Cash Catalyst

The $20 million TIF receivable is not merely a balance sheet line item; it is a near-term cash inflow catalyst. The company received its first $580,000 payment in Q4 2025, validating the collection mechanism. As existing developments continue to pay property taxes, the pace of TIF reimbursements will accelerate. Full collection by 2027 would provide Canterbury with significant free cash flow that can be returned to shareholders, reinvested in development, or used to repurchase shares.

50 Acres of Entitled Suburban Land

Canterbury’s remaining 50 acres are not merely land - they are entitled, zoned, infrastructure-improved parcels within an active master-planned community in one of the fastest-growing suburbs in the Twin Cities metro area. Shakopee’s population has grown over 14% since the 2020 census and the Metropolitan Council projects 43% growth through 2050. Scott County has been one of the fastest-growing counties in Minnesota for two decades, with a median household income of over $107,000.

These are not commodity agricultural parcels. They are institutional-quality development sites with completed roads, utilities, and entitlements, surrounded by an increasingly dense and successful mixed-use community. The flywheel effect of nearly 1,000 residential units, multiple restaurants, office space, and a Live Nation amphitheater creates a demand ecosystem that did not exist when Canterbury sold its first parcels. Each subsequent development phase increases the value of the remaining land.

Scarcity Analysis: Unique Assets or Just Land?

A critical question for any land-heavy investment thesis is whether the assets represent true scarcity or simply another suburban development plot. Canterbury’s asset base contains multiple layers of genuine scarcity:

The Gaming License: Canterbury holds the only thoroughbred and quarter horse racing license in Minnesota. State law and tribal lobbying have effectively foreclosed the possibility of expanded gaming or new racing licenses. This is a one-of-one asset in a state of 5.7 million people. The license cannot be replicated through capital investment alone; it exists because of regulatory and political conditions that are unlikely to change.

The Master-Planned Entitlements: The Canterbury Commons development plan was approved through a complex, multi-year regulatory process involving the City of Shakopee, Scott County, and various state agencies. The TIF agreement, zoning variances, and infrastructure commitments represent years of political capital and regulatory groundwork that a competitor could not easily replicate, even on equivalent acreage.

The Live Nation Anchor: The 19,000-seat amphitheater operated by Live Nation is a franchise asset for the greater Canterbury Commons campus. Live Nation does not build amphitheaters in every suburb; the selection of this site reflects the strategic value of the location, transportation infrastructure, and development density. This anchor tenant validates the entire development thesis and is non-replicable in the immediate trade area.

Location and Demographics: Shakopee sits at the intersection of US Highway 169 and Highway 101, with direct access to the Twin Cities metro area. The site is adjacent to other major entertainment destinations including Mystic Lake Casino and Valleyfair Amusement Park. The combination of entertainment density, transportation access, and rapid population growth creates a fundamentally different value proposition than undeveloped suburban land on the metropolitan fringe.

In short, these are not simply land parcels. They are entitled, anchored, infrastructure-improved development sites within a master-planned community bearing an irreplaceable gaming license, in one of the fastest-growing suburbs in the Upper Midwest. The scarcity is real and multi-layered.

Management and Incentive Alignment

Founder-Led, Insider-Heavy Ownership

Canterbury Park is led by co-founder, Chairman, President, and CEO Randall D. Sampson, a CPA who has served in this role since the company’s formation in 1994. Sampson is the largest individual shareholder with approximately 984,500 shares representing roughly 19–20% of the company. Total insider ownership is approximately 37%, and when combined with institutional holders like Black Diamond Capital Management (17%), GAMCO/Gabelli (12–15%), the top four shareholders control approximately 59% of shares outstanding.

This ownership structure has important implications. First, management’s economic interests are overwhelmingly aligned with shareholders - Sampson’s stake alone represents approximately $15 million at current prices and likely constitutes the vast majority of his personal net worth. Second, the concentrated ownership base means any strategic action (sale, spin-off, going-private) requires buy-in from a very small number of decision-makers, potentially accelerating value realization. Third, the presence of value-oriented institutional investors like Gabelli and Black Diamond provides a natural constituency for shareholder-friendly capital allocation.

Capital Allocation Track Record

Management has pursued a conservative, self-funding development strategy that prioritizes balance sheet strength. The company carries zero debt and has funded all TIF infrastructure improvements and JV equity contributions from operating cash flow and land sale proceeds. Canterbury pays a modest quarterly dividend of $0.07 per share ($0.28 annualized) representing a 1.8% yield, signaling commitment to returning capital while preserving flexibility.

The capital-light JV structure is a key positive. Rather than taking on construction debt and development risk, Canterbury contributes land as equity and lets experienced operating partners (Doran, Greystone, Trackside) handle construction and asset management. This preserves balance sheet optionality while allowing Canterbury to participate in development upside through its equity interests.

Management Criticism and Risks

Legitimate criticisms of management include the slow pace of value realization and limited shareholder communication. The company has no analyst coverage, conducts no earnings calls, and provides only bare-minimum SEC disclosure. The pace of land monetization has been methodical but arguably too conservative - 50 acres remain undeveloped seven years after the initial Commons approval. The Doran Phase I sprinkler issue, while not directly management’s fault, delayed leasing by 12–18 months and depressed reported results.

The counter-argument is that Sampson has been patient and disciplined in partner selection, achieving strong lease-up rates (94–99% on stabilized projects) and preserving a fortress balance sheet through a period of industry headwinds. The question is whether this patience is creating value or forestalling it.

Why This Could Experience a Fundamental Re-Rating

Multiple catalysts exist to close the gap between the current stock price and underlying NAV over the next 12–24 months:

1. Amphitheater Opening (June 2026): The opening of the Live Nation amphitheater will generate significant local and regional media coverage, driving awareness of Canterbury Commons as a destination. More importantly, it will generate foot traffic that directly benefits Canterbury’s gaming and F&B operations and catalyzes development interest in adjacent parcels. This is the single most visible near-term catalyst.

2. TIF Cash Inflows (2025–2027): Accelerating TIF repayments convert a balance sheet asset into free cash flow that can be deployed for share repurchases, special dividends, or reinvestment. The initial $580,000 Q4 2025 payment was a proof of concept; as the tax base matures and new assessments are added, quarterly payments should increase materially.

3. JV Equity-Method Income Inflection: As the Doran Phase I and Phase II properties stabilize and the DBSV portfolio approaches breakeven, Canterbury’s reported equity-method losses will swing to income. This will mechanically improve reported EPS, potentially attracting screens and quantitative investors who have been repelled by the net loss.

4. New JV Announcements for Remaining Acreage: Management has stated it will explore entertainment and hospitality development for the 25 amphitheater-adjacent acres throughout 2026, in partnership with Hunden Partners. New JV announcements, particularly for hotel or entertainment uses, would crystallize the value of the remaining land and demonstrate the ongoing monetization trajectory.

5. Capital Return Acceleration: With capex declining to historical levels of $2–3 million annually now that barn relocation and TIF infrastructure are complete, free cash flow should increase notably starting in 2026. Management has multiple options: increase the dividend, initiate a meaningful buyback, or pursue a special distribution.

6. Strategic Alternatives: The concentrated ownership structure makes strategic transactions feasible. Potential paths include a real estate spin-off or REIT conversion of the JV portfolio, a sale-leaseback of the racetrack property, a going-private transaction led by Sampson and private equity, or an outright sale of the gaming license to a regional operator. Any of these would likely occur at a significant premium to the current price.

Asymmetric Upside and Downside Protection

The risk/reward in CPHC is fundamentally asymmetric. The downside is cushioned by a debt-free balance sheet with tangible asset backing: $17 million in cash, $20 million in TIF receivables, real estate JV interests, and 50 acres of land provide a floor well above the current price even in a liquidation scenario. The company’s book value alone is $10.80 per share, and this significantly understates the fair value of assets carried at cost.

The upside, however, is leveraged to multiple re-rating catalysts that could materialize over the next 12–36 months. If the amphitheater opening drives casino traffic growth, if JV income turns positive, if new development deals are announced, or if management pursues strategic alternatives, the stock could re-rate toward our base-case NAV of $26 per share (67% upside) or higher. In a scenario where the remaining 50 acres are developed into high-value uses at premiums to prior transactions, NAV could exceed $30 per share (93% upside).

The key asymmetry: you are buying a dollar of assets for roughly sixty cents, with multiple ways to win and limited downside given the fortress balance sheet. Even if the operating business continues to decline modestly, the land and development portfolio provide a value floor that the market is ignoring.

Implied Value of the Racetrack and Casino

One of the most revealing exercises is backing into the market’s implied valuation of the operating gaming business after stripping out balance sheet assets.

At the current stock price, the market is implying the racetrack, casino, and F&B operations - the only horse racing and card casino operation in Minnesota, generating $9.4 million in annual EBITDA - are worth approximately $13 million, or barely over 1x EBITDA. For reference, comparable regional gaming operations typically trade at 6–10x EBITDA. Even highly distressed casino assets rarely trade below 3–4x. This implied valuation is irrational unless one believes the operating business will cease to exist, which is implausible for a company with no debt and a monopoly gaming license.

Time to Monetization and Fair Value Assessment

The primary bear case is time. Canterbury Commons is a multi-decade development project, and investors are paying carrying costs (in the form of depressed earnings and equity-method losses) while waiting for value to be realized. This is a legitimate concern and the reason the stock trades at a discount.

However, we believe the market is over-discounting the time value for several reasons. First, the TIF receivables are being repaid now, not in some distant future. Second, the JV portfolio is approaching stabilization - Phase II is refinanced, The Omry is 99% leased, and Phase I is accelerating toward target occupancy. Third, the amphitheater opens in three months, not three years. Fourth, capex is declining to maintenance levels, freeing up significant operating cash flow starting in 2026.

At $15.50 per share, an investor is effectively getting the time optionality for free. The tangible liquid and semi-liquid assets (cash + TIF + JV interests) already account for approximately $10.50 per share per management’s own calculation. The remaining $5.00 per share is buying the entire operating business, 50 acres of development land, and a portfolio of re-rating catalysts. This is an exceptionally favorable price for time.

What Does the Company Look Like in 3–5 Years?

By 2028–2030, Canterbury Park could look fundamentally different from the company that exists today:

The operating business should stabilize or modestly improve, driven by amphitheater-related foot traffic, expanded VIP casino programs, and the maturation of Canterbury Commons as a regional destination. EBITDA of $10–12 million is achievable.

The JV portfolio should be generating positive equity-method income, contributing $1–2 million annually to consolidated net income. The Doran properties, once fully stabilized, may begin distributing cash to equity holders.

TIF receivables should be fully collected, having contributed $20 million in cumulative cash. This capital will have been redeployed into development, buybacks, or dividends.

A significant portion of the remaining 50 acres should be under development or sold, with new JVs or land sales crystallizing value. The amphitheater-adjacent parcels in particular should command premium pricing given the proven entertainment traffic patterns.

In this scenario, Canterbury could be generating $12–15 million in consolidated EBITDA (inclusive of JV distributions), with a clean balance sheet, a reduced land inventory, and a proven track record of value monetization. At a 7–8x multiple, the equity would be worth $85–$120 million, or $16–23 per share, plus the remaining land optionality and any capital that has already been returned to shareholders. On a total-return basis, the opportunity is compelling.

Key Risks

Gaming Competition: The Shakopee Mdewakanton Sioux Community’s Mystic Lake Casino is a formidable competitor located nearby. Potential expansion of tribal gaming, sports betting, or other forms of legalized gambling in Minnesota could further pressure Canterbury’s casino revenues.

Regulatory Risk: Minnesota legislators have prohibited historical horse racing machines and restricted the racing commission’s ability to expand gaming types. Canterbury is structurally limited to an unbanked card casino, which caps earnings power.

Development Execution: Real estate development is inherently risky. Delays, cost overruns, permitting issues, and market downturns can all impair returns. The Phase I sprinkler issue demonstrated that execution risk is real, not hypothetical.

Liquidity and Micro-Cap Risk: CPHC trades roughly 1,800 shares per day with zero analyst coverage. The stock is illiquid, volatile, and unsuitable for investors who require daily liquidity. Institutional investors face meaningful position-sizing constraints.

Key-Man Risk: Randy Sampson is 67 years old and has been CEO for 30+ years. Succession planning is opaque. A transition to new leadership could change strategic direction, though the concentrated ownership base provides continuity.

Going-Private Risk: With 20% ownership and depressed share prices, Sampson could partner with private equity to take the company private at a modest premium, depriving public shareholders of full value realization. The existing shelf offering authorization adds another vector of potential dilution.

Conclusion

Canterbury Park Holding Corporation is a classic micro-cap NAV story: a misunderstood company with significant hidden asset value trading at a steep discount to intrinsic worth, with multiple identifiable catalysts for re-rating. The market sees a declining casino operation with equity-method losses and no analyst coverage. What we see is a debt-free balance sheet loaded with $10.50+ per share in liquid assets, a portfolio of real estate JVs approaching stabilization, 50 acres of prime development land at cost, a monopoly gaming license, and a Live Nation amphitheater opening in 90 days.

At $15.50 per share, the implied valuation of the operating business is approximately 1.4x EBITDA - an absurdly low multiple for any cash-generating asset, let alone one with a monopoly gaming license. The risk/reward is asymmetric: tangible downside protection from the balance sheet, with multiple paths to 60–100%+ upside as catalysts materialize.

This is a patient investor’s opportunity. The thesis requires a willingness to tolerate illiquidity, ignore GAAP noise, and trust that hard assets will eventually be recognized by the market. For those with the temperament and time horizon, Canterbury Park offers a rare combination of deep value, balance sheet safety, and identifiable catalysts in a forgotten corner of the micro-cap universe.