Aztec Land and Cattle (AZLCZ): The Land Compounder No One Owns

A 19th-century cattle empire has quietly compounded at ~28% over the last 10 years. Almost no one has heard of it. Now it's the land beneath the renewable energy grid.

Pull up AZLCZ on any terminal and you’ll get this: a Phoenix company “engaged in cattle ranching services,” founded 1884, no revenue line, no P/E, a $2,000-plus share price, volume in single digits. No index will buy it, no screen will surface it, no analyst is paid to cover it.

Here is what is actually there: a fee-simple land position larger than the city of Chicago, on a sun-drenched high-desert plateau adjacent to the BNSF transcontinental mainline, Interstate 40, and a retired 1-gigawatt coal plant whose 345 kV and 500 kV transmission already exists and has just been freed up. On that land, two of North America’s largest energy companies (AES and Invenergy) are building a wind farm and a solar + storage complex under contracts with the state’s largest, investment-grade utility totaling more than a gigawatt. Not to mention mineral rights, water rights, and a short-line railroad.

It’s Texas Pacific Land, one energy cycle behind. And it’s up more than 50x over the last 27 years.

The Hidden Compounder

Aztec Land & Cattle Company, Limited was born in 1884 when Boston and New York money bought roughly a million acres of northern Arizona grassland from the bankrupt Atlantic & Pacific Railroad for fifty cents an acre, stocked it with 32,000 Texas longhorns under the famous Hashknife brand, and built the third-largest cattle outfit in North America. The cattle are long gone. The land is not. Today Aztec and its affiliates own about 239,000 surface acres in Navajo County and ~318,000 acres of mineral rights - the second-largest private land position in the state.

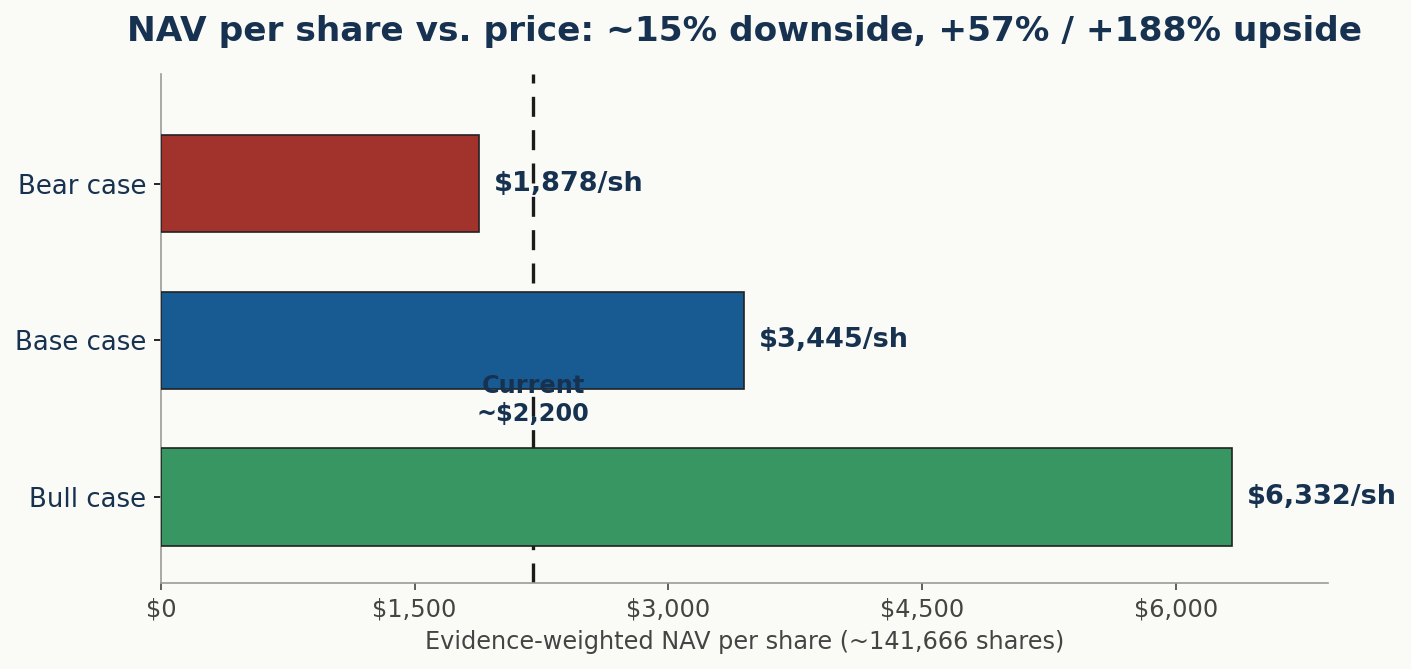

We value the company asset by asset. A bear case ~15% below today’s price, a base case of ~$3,445/share (+57%), and a bull case of ~$6,330/share (+188%).

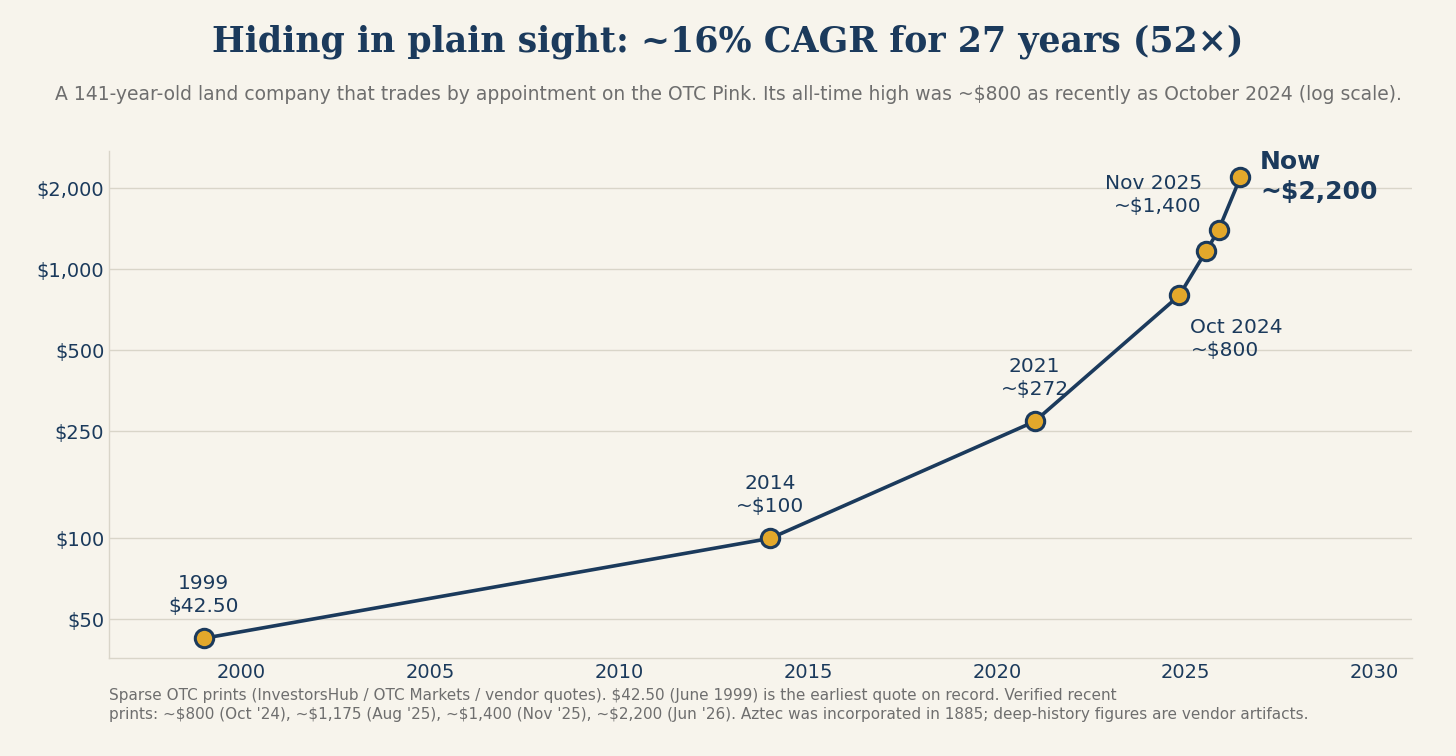

AZLCZ has compounded for roughly half a century - +5,100% since 1999 (~16% CAGR) and +1,200% over the past ten years (~27% CAGR). But you will not find a clean 27-year price chart anywhere - and that absence is itself part of the story.

The stock is so thinly traded (a few shares on a typical day, often none for weeks) that no vendor keeps a continuous daily series: Google Finance only begins around 2007, and there are only sparse prints back to that $42.50 low in 1999. The chart above therefore plots milestone reference points, not a daily history. Data is difficult to find but well supported by archived Oddball Stocks posts (if you know, you know).

The data gap is not a red flag; it is the mispricing. A security this illiquid and this poorly tracked is exactly the kind of thing that can compound for over 25 years while every screen, index and charting service looks straight through it.

History: from longhorns to electrons

In the early 1880s the Atlantic & Pacific Railroad laid track across northern Arizona under a federal land grant of the odd-numbered sections - one square mile each - in a vast checkerboard. When the railroad faltered it sold a million of those acres to eastern investors for $0.50 each. They branded their cattle with a chuckwagon hash-knife, and the “Hashknife Outfit” became legend - 33,000 head, a 150-mile range, a starring role in Arizona’s Pleasant Valley War.

By about 1905 Aztec had sold the cattle and become a landlord, leasing grazing to local ranchers (the Flake family, for whom Snowflake is named, among them). In the early 1960s it made its last big land sale - a parcel to Southwest Forest Industries for a paper mill near Snowflake - and learned the lesson that defines it: the land is worth more held than sold. In 2017 it re-purchased much of that very parcel.

A 19th-century railroad land grant, consolidated patiently across the 20th century, now sits exactly where the energy economy needs flat, sunny, privately-held land next to existing high-voltage wires. The cattle company became a land bank. The land bank is becoming an energy-infrastructure royalty machine.

Stewardship: the Brophy family and the long view

For generations Aztec has been associated with the Brophy family - Irish immigrants who came to the United States in 1879 and became one of Arizona’s defining families. The patriarch, William Henry Brophy, was a merchant and banker; his widow, Ellen Amelia Brophy, endowed Phoenix’s Brophy College Preparatory in his memory in 1928. Today the company is led by Steven Brophy, a native-Arizonan rancher and businessman known, as one recent profile put it, for his quiet stewardship of land and legacy. This is an owner-operator measuring time in generations, not a management team optimizing for the next earnings call.

Brophy’s own words are the clearest statement of this long-term mindset:

On permanence and patience: “We’ve been around 125 years and hope to be around for another 125 years,” “We are content to wait for the future.”

On royalties: “We don’t see that we will be going out of the leasing business for the next 280 years.”

On selling: “Aztec has owned the land since 1884 and we have never wanted to sell it and do not want to sell it now.”

On infrastructure: “We have the water supply, the people supply, the tremendous amount of infrastructure and land in vast quantities and the jobs will blossom.”

On water: “My father was a gentle man but he told me when I was five years old that it was almost all right to kill for water.”

For a controlled, illiquid, deeply discounted compounder, this is the bull case for the steward: an owner that has never wanted to sell, thinks in centuries, and treats the land’s optionality as an endowment to be realized right, not fast.

And speaking of killing for water - read our Water Rights Thesis:

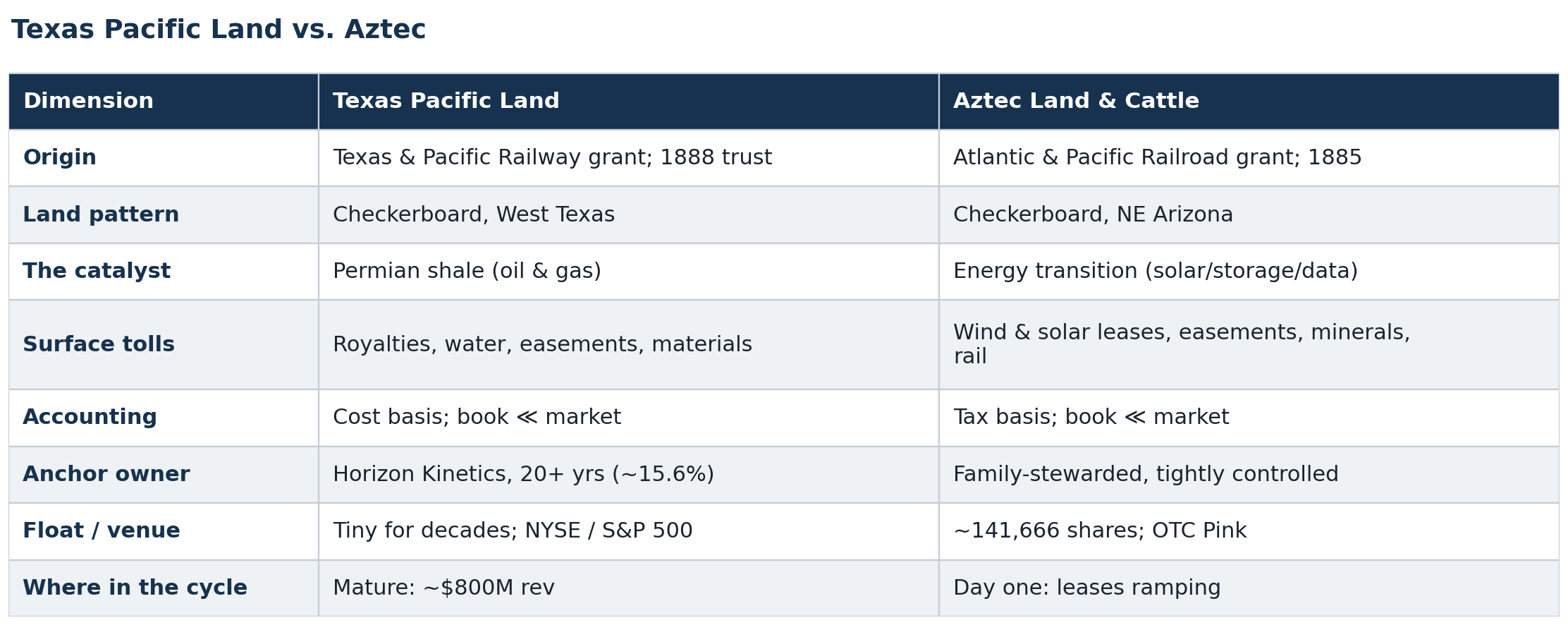

The Texas Pacific Land playbook

Texas Pacific Land was chartered on February 1, 1888 to dispose of ~3.5 million acres of West Texas land grant pledged by the bankrupt Texas & Pacific Railway to its bondholders. Same mechanism as Aztec: a failed 19th-century railroad, a checkerboard of land-grant sections, a vehicle to hold and slowly monetize dirt nobody else wanted. For a century TPL was an obscure, illiquid trust compounding in the dark.

Then the Permian shale revolution arrived, and the dirt TPL sat on turned out to sit atop the most productive oil basin in the world. Every barrel paid TPL a royalty; every operator had to use the surface it owned - water, easements, materials, facilities. TPL owned the board the whole game was played on.

In 2025 TPL generated roughly $798M of revenue and $592M of operating income with 114 employees. TPL was one of the best-performing U.S. equities in existence: it returned 480x over a 25-year period (~28.5% CAGR).

TPL is now pursuing exactly what Aztec is positioned for - solar, wind, power, water - and being re-rated by the Street as energy-infrastructure rather than an oil royalty. The mature flywheel has arrived at the energy-transition use cases. Aztec stands at the trailhead they are walking toward.

The flywheel, precisely. What made TPL a compounder is not simply that it owns land - it is that the landowner captures the upside of everyone else’s capital. Operators fund every well, panel and turbine; the landowner takes a toll off the top with no capex and no commodity risk. The toll mix keeps upgrading on the same non-depleting acres (oil → water → surface → solar → data), nearly all of it drops to free cash against a tiny fixed cost base, and that cash is recycled into a shrinking share count and more land. Value therefore compounds on three vectors at once - more tolls, fewer shares, and a re-rating multiple as the asset is reclassified from commodity royalty to scarce infrastructure. Aztec owns the same kind of board.

The asset footprint

Aztec’s land runs from Holbrook and Joseph City in the north, southwest to Heber, just south of Snowflake/Taylor, the eastern edge tracking SR-77 and the southern boundary the Mogollon Rim. Most is still the original checkerboard, interleaved with BLM and State Trust sections - which is why consolidation matters: every inholding turns scattered squares into developable blocks.

Converging on this ground: the BNSF transcontinental mainline and I-40 across the top; the Apache Railway running south to Snowflake; the Little Colorado River and the aquifers beneath; and at the hinge of it all, the retired Cholla switchyard - two 345 kV lines to Four Corners and a 500 kV line to Coronado.

Developers are not here for the scenery. They are here for the wires - and four utilities now cross this land: power, water, rail, and (since 2024) open-access dark fiber.

Asset-by-asset valuation

Asset 1: Renewable lease portfolio - the contracted core

This is the highest-conviction near-term driver, and where the mispricing is most quantifiable. Over the past 18 months Aztec’s renewable position has shifted from speculative optionality on raw acreage into a contracted, construction-phase revenue stream backed by two of the largest energy companies in North America, both under offtake with Arizona Public Service - the state’s largest regulated utility and a subsidiary of S&P 500 issuer Pinnacle West.

Why interconnection is the asset, not the panels. A utility-scale project needs flat, cheap, sunny land; a willing landowner; and a way to inject power into the grid. The first two are common; the third - interconnection capacity on existing high-voltage transmission - is the bottleneck of the entire U.S. energy transition, with queues running four to seven years. Aztec owns the land wrapped around the retired Cholla node, whose 345 kV and 500 kV capacity has just been freed by the coal units’ retirement.

West Camp Wind (AES). A 504 MW wind farm (~104–112 turbines) ~10 miles southwest of Joseph City, tied to the APS Cholla 500 kV substation, with a sibling project (West Camp 2, ~500 MW + storage) approved by the Arizona Corporation Commission in January 2026. Aztec collects the greater of a minimum rent floor or a percentage royalty on gross revenues.

Hashknife Solar (Invenergy). One of the largest solar projects in Arizona. Phase I is 275 MW + 275 MW/1,100 MWh storage on ~3,000 acres and broke ground December 2024. Phase II adds 200 MW + 200 MW/800 MWh on ~1,200 acres.

Combined the project is 475 MW of solar plus 475 MW / 1,900 MWh of storage on ~4,200 Aztec acres. The project deliberately adopts Aztec’s own 1880s brand (Hashknife).

The March 2026 investor update references a new solar energy project, and Navajo County approved the Lark Point Solar project on Aztec-owned land in late 2024. The development pipeline continues to grow as APS seeks to add 6 GW of new renewable capacity between 2025 and 2031.

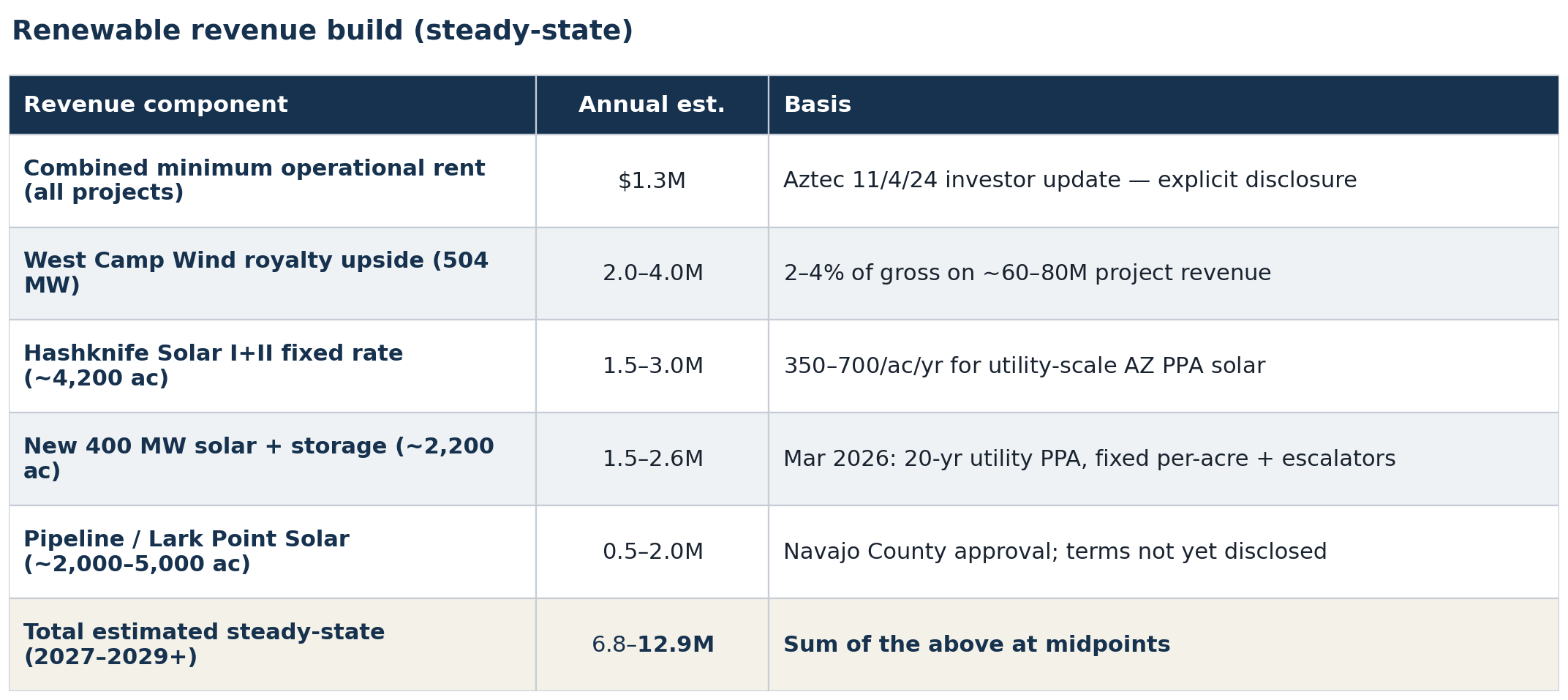

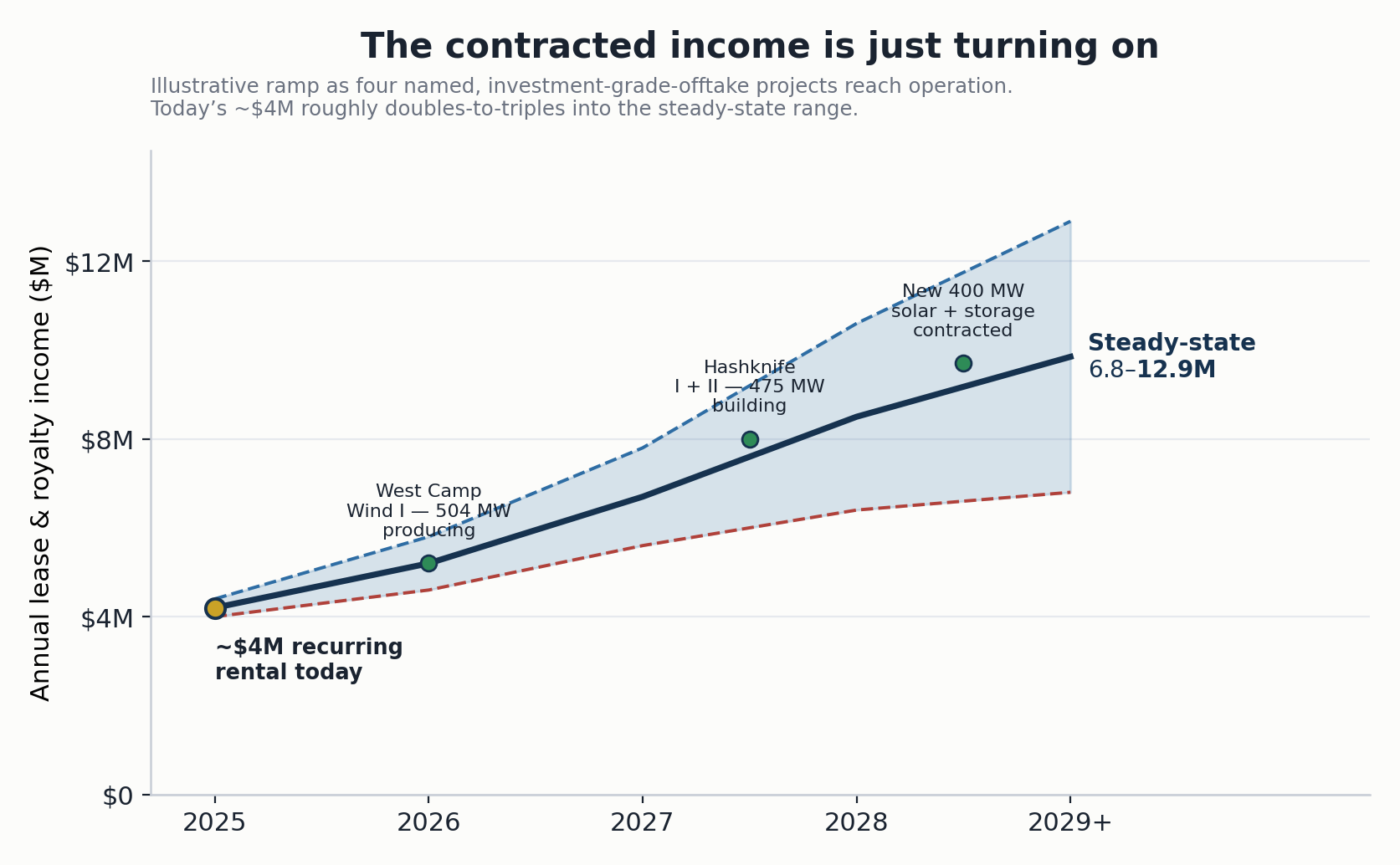

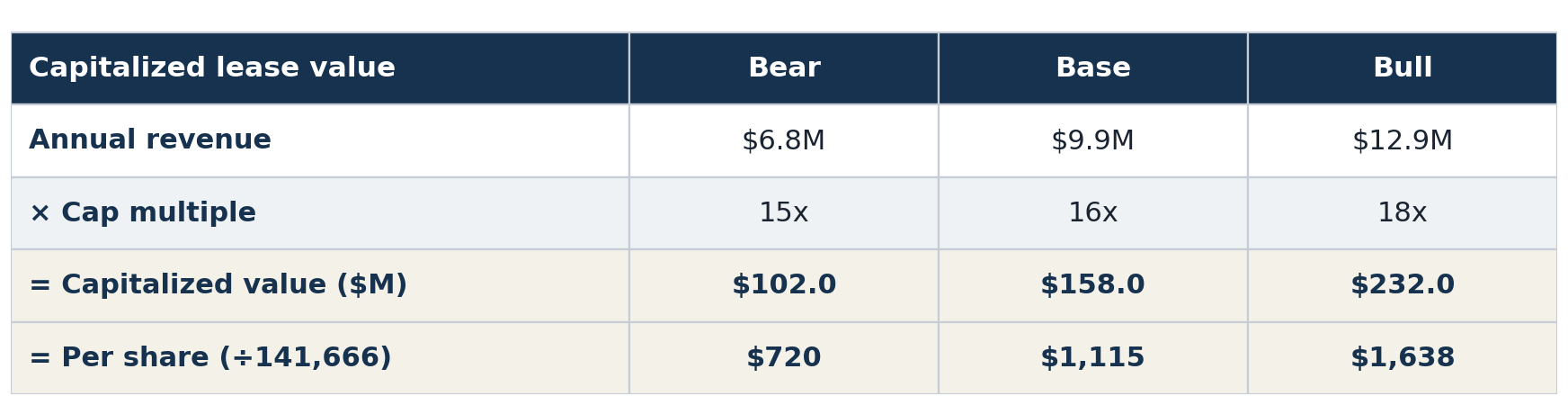

The revenue build. Aggregating the contracted and pipeline projects produces a credible steady-state (2027–2028+) lease-and-royalty stream:

Long-duration, inflation-protected surface-lease income with an investment-grade utility offtaker commands premium capitalization. Comparable contracted renewable-lease portfolios - assembled by infrastructure funds, royalty trusts and land institutions - trade at 12x–18x annual cash flow, with the high end for portfolios that have credit-quality offtake, contractual escalators, and royalty upside. Aztec’s portfolio satisfies all three.

The valuation keys directly off the steady-state range above. The bear takes the low end, ~$6.8M, at 15x (~$102M, $720/sh) with no royalty or pipeline upside. Base ~$9.9M×16 = $158M ($1,115/sh) is the midpoint. Bull ~$12.9M×18 = $232M ($1,638/sh) carries full royalty and storage upside as the projects reach operation across 2026–2029.

The contracted base keeps widening. As of the March 2026 annual meeting, West Camp Wind I (504 MW) began producing power in Q2 2026; Hashknife Solar I and II are both under construction; and a lessee has signed a twenty-year PPA with an Arizona utility for a new 400 MW solar + storage project on ~2,200 acres of Aztec land - construction starting in 2026, a fixed per-acre rate once it begins and an escalating per-acre rate at operations, on a 25-year term.

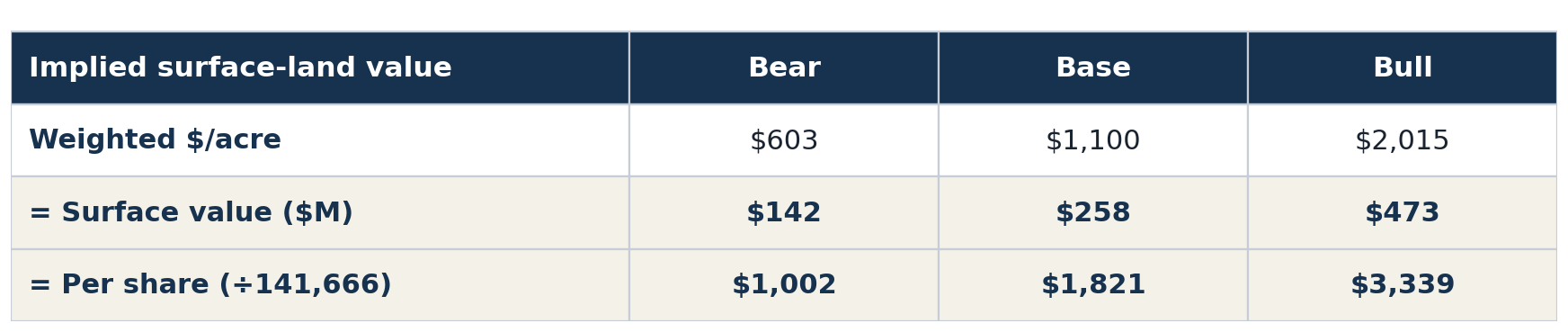

Asset 2: Surface land - segmented, not averaged

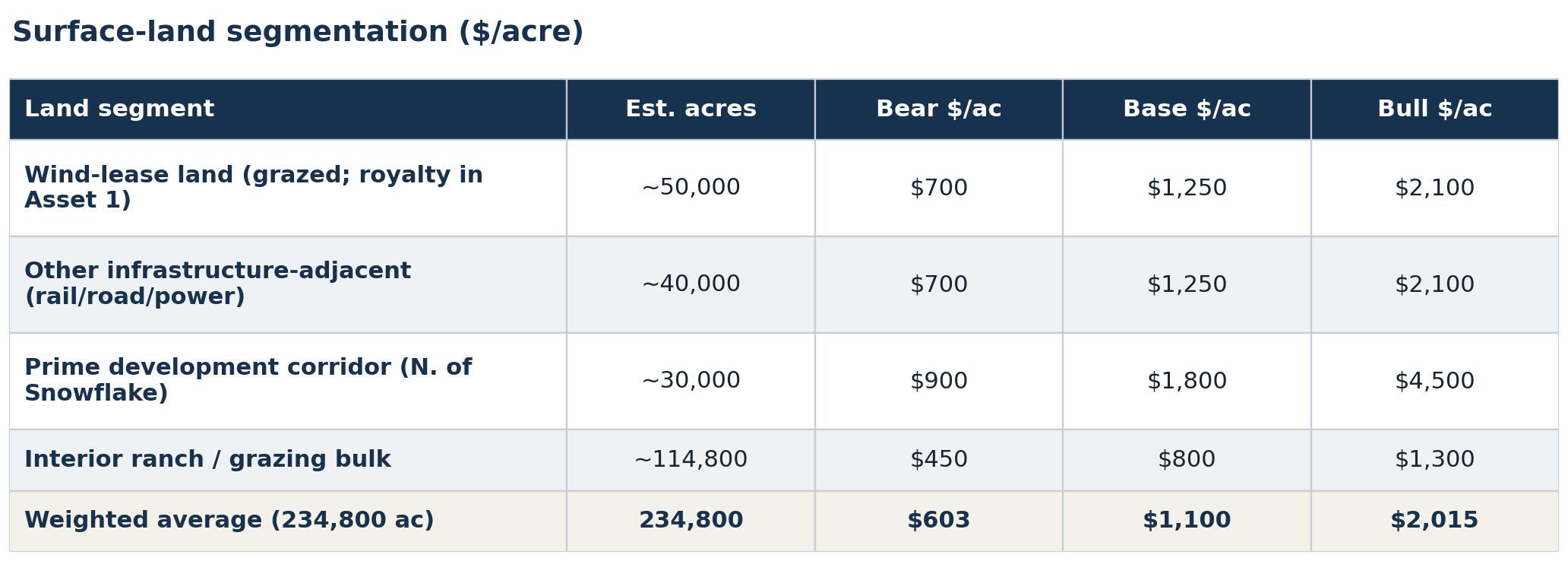

The surface acreage is the largest single value component, and the asset most often misvalued. The error is to apply a single per-acre figure to all 239,000 acres. The land is not homogeneous: a share is under or adjacent to active renewable leases; a share has direct I-40, SR-77 or rail frontage; a share sits in the development corridor running north from Snowflake; the remainder is bulk interior grazing. Each segment has its own comp set and value driver.

Layer 1 - the floor.

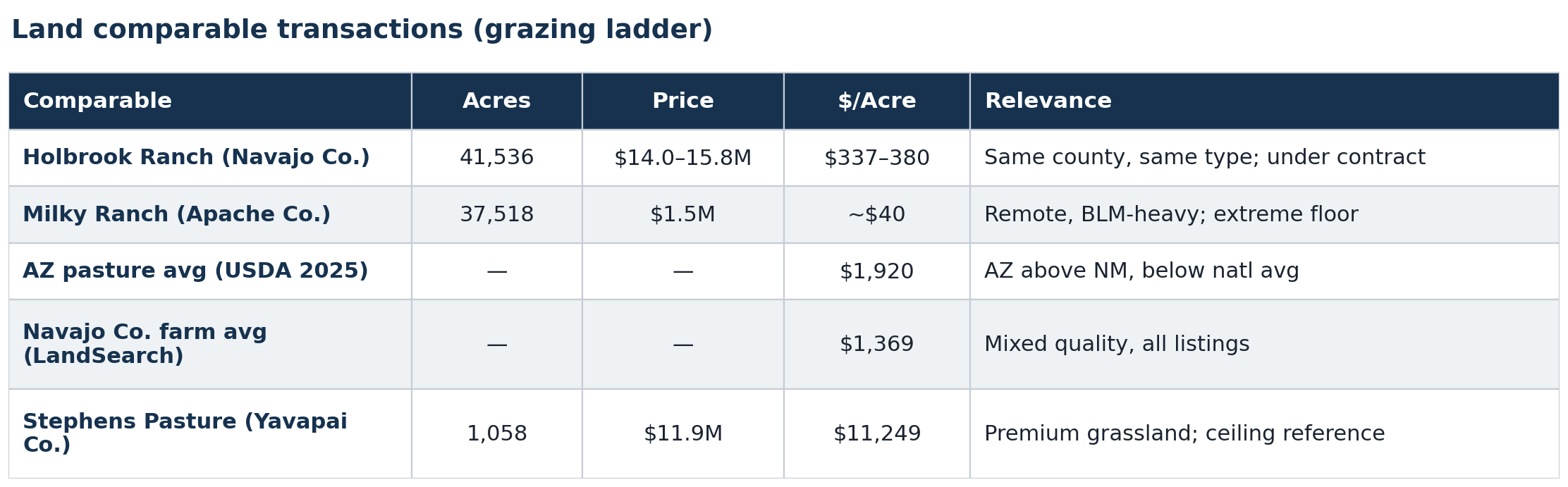

The Holbrook Ranch transaction is the most directly comparable. At 41,536 acres listed under contract at $14.0–$15.8 million, it implies $337–$380 per acre for a large-scale Navajo County ranch with no renewable energy leases, no railroad, and no grid infrastructure. This is the floor for Aztec’s base ranch value.

However, Aztec’s acreage is fundamentally different from the Holbrook Ranch in several respects. First, Aztec’s holdings are approximately 5.7 times larger, and large contiguous blocks command a premium in Arizona where private land comprises only 16% of total state area. Second, Aztec’s land is already generating revenue from renewable leases. Third, the land has railroad access, highway frontage (I-40 and Route 77), and direct proximity to institutional-grade transmission infrastructure. Fourth, the checkerboard pattern, while complex, has been substantially consolidated over 140 years of patient acquisition.

Layer 2 - segmentation by value driver. We first set aside the ~4,200 acres physically under solar panels - those are valued as cash flow in Asset 1, not as land - then split the remaining ~234,800 acres into segments by documented infrastructure access and use intensity:

Layer 3 - the development-corridor option, now in motion. The company submitted a master area plan to Navajo County in 2012 contemplating a gradual transition from purely agricultural zoning to mixed commercial and residential uses on portions of its southern holdings (north of Snowflake). CEO Steven Brophy has publicly stated that the next logical path of development in Arizona runs north of Snowflake and south of Joseph City - directly through Aztec’s land.

Arizona is adding roughly 90,000 new residents per year, and the Phoenix metropolitan area’s northward expansion is pushing development pressure toward previously rural areas. While full-scale residential or commercial development of Aztec’s land is a 10–20+ year horizon event, the option value is non-trivial. Even converting 5,000 acres (roughly 2% of holdings) to entitled residential or commercial lots at $15,000–$50,000 per acre would create $75–$250 million of value.

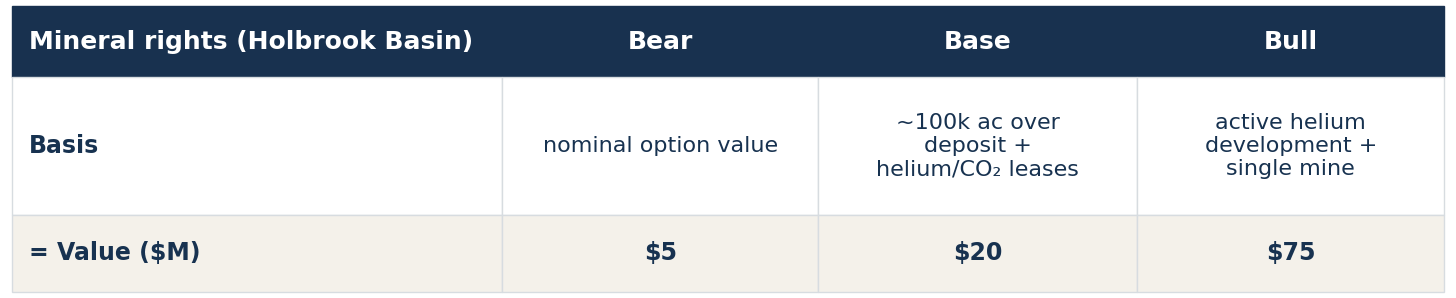

Asset 3: Mineral rights - the Holbrook Basin option

Aztec controls ~318,000 acres of subsurface rights across Navajo and Coconino Counties, carried at near-zero book and largely invisible. The geology is more interesting than the income statement: two distinct subsurface assets each have independent commercial relevance.

The Holbrook Basin potash deposit. The Holbrook Basin hosts one of the most significant undeveloped potash deposits in the United States. The Arizona Geological Survey documented the resource in 2008, estimating that the deposit underlies approximately 600 square miles east of Holbrook.

Multiple companies explored this deposit between 2008 and 2014. American West Potash reported indicated resources on approximately 94,000 acres. Passport Potash acquired strategic positions encompassing over 121,000 acres and entered into exploration agreements with the Hopi Tribe. However, when global potash prices collapsed from over $800 per ton in 2009 to roughly $300 per ton by 2013, commercial development became uneconomic and exploration ceased.

The critical question for Aztec investors is: what portion of the Holbrook Basin potash deposit underlies Aztec’s 318,000 mineral acres? While Aztec has never disclosed the specific overlap, the geographic footprint of the deposit (centered east of Holbrook across Navajo and Apache Counties) substantially overlaps with Aztec’s mineral holdings. Even a partial overlap - say 50,000–100,000 acres - would represent a meaningful option on future potash development if prices return to economically viable levels.

Helium. The Holbrook Basin also contains helium deposits (a former helium-producing area exists near the northeastern extent of the potash deposit) and extensive salt formations. Arizona’s helium resources have attracted renewed interest as global helium shortages have emerged. Additionally, the Permian salt formations have been used for LPG (liquefied petroleum gas) storage near the northwestern extent of the deposit. While speculative, these secondary mineral resources represent additional option value within Aztec’s 318,000 mineral acres.

Mineral rights (Holbrook Basin)

Asset 4: Apache Railway - the right-of-way

Aztec Land & Cattle Company and Midwest Poultry Producers LP purchased the Apache Railway Company out of bankruptcy in late 2015 for ~$4.4M (against a ~$7.2M court-assessed value), preventing the scrapping of a 107-year-old rail line. This acquisition was strategically motivated: the railroad traverses Aztec’s land and connects it to the national freight rail network. Roughly 90% of revenue is now railcar repair, cleaning and storage; ~10% freight.

The Apache Railway is not a significant standalone earnings generator. Its primary value is strategic: it provides multimodal transportation infrastructure to Aztec’s land that would cost tens of millions of dollars and years of permitting to recreate. The West Snowflake Railpark development concept - marketing commercial land along the railroad for industrial and distribution uses - is built on this infrastructure.

The railroad’s interchange with BNSF at Holbrook connects Aztec’s land to the BNSF Southern Transcon, one of the busiest freight rail corridors in North America. This is a direct connection to both domestic markets and international ports (Long Beach, LA, etc.). For any future industrial development on Aztec’s land - whether that involves potash mining, solar panel manufacturing, agricultural processing, distribution, or data center construction materials logistics - the railroad provides a critical competitive advantage.

The bankruptcy court valued the railroad at $7.2 million in 2015 when it had lost its primary customer (the Snowflake paper mill). Since then, the railroad has rebuilt revenue through car repair and storage services. Given the strategic value to Aztec’s broader land development thesis, the irreplaceability of the right-of-way, and the BNSF interchange, we value the railroad base case at $15 million.

Apache Railway

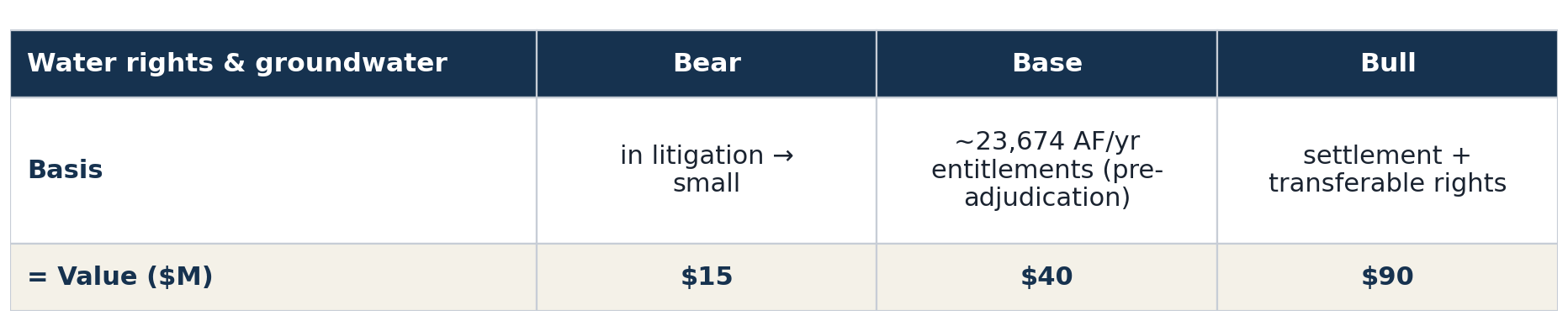

Asset 5: Water rights & groundwater

Water in Arizona is the ultimate scarce resource, and Aztec’s groundwater position is perhaps the least understood and most undervalued component of the asset base.

Historical Context: The APS/Cholla Water Dispute

In 1972, Aztec entered into a contract allowing Arizona Public Service to drill wells and pump groundwater from approximately 7,000 acres of Aztec land for $10 per acre per year (approximately $70,000 annually). For 34 years, the Cholla Power Plant consumed approximately 3.5 billion gallons of groundwater annually from these wells for coal plant cooling operations. When the contract neared expiration in 2007, APS attempted to renew at similar rates. Aztec demanded market-rate pricing. APS filed a condemnation action in Navajo County Superior Court seeking to condemn the 7,000 acres to secure long-term water access.

This litigation is extraordinarily revealing. APS - a regulated utility serving millions of customers - considered the water beneath Aztec’s land essential enough to its 1,000 MW generating station that it pursued eminent domain. Michael Brown, Aztec’s attorney, described it as potentially one of the largest condemnation actions in the history of Arizona. The eventual resolution of this dispute (details are not fully public) effectively established that the water beneath Aztec’s land has significant strategic value to major industrial users.

Current Water Situation

With the Cholla Power Plant retired in March 2025, the 3.5 billion gallons per year previously consumed are no longer being extracted. This represents a significant freed capacity of groundwater that is now available for other uses. The Little Colorado River (LCR) Adjudication - referenced in Aztec’s July 2024 investor update - is a comprehensive legal proceeding to determine water rights in the LCR watershed. A favorable resolution could formally quantify Aztec’s groundwater rights, transforming them from an informal asset into a legally defined, transferable property right.

Water Valuation Framework

Water rights in Arizona are among the most valuable in the Western United States. The Colorado-Big Thompson (C-BT) unit system in northern Colorado, one of the most actively traded water markets, has seen unit prices appreciate at roughly 11.7% annually since 1990, reaching $50,000+ per unit. While direct comparisons between Colorado Front Range water and rural Arizona groundwater are imperfect, the directional trend is clear: water scarcity is intensifying and water rights are appreciating faster than virtually any other real asset class.

Water rights & groundwater

Fiber & Broadband

A critical and entirely new development that has received minimal investor attention is the construction of a 100+ mile, $19.7 million open-access dark fiber middle-mile network through Navajo County, originating in Joseph City and traversing Aztec’s land corridor. Built and funded by Vivacity Infrastructure Group and APS, this provides open-access dark fiber with 99.9% uptime guarantee. Construction began in April 2024 in Holbrook and was available for lease starting in 2025.

APS is partnering on the project, connecting its strategic fiber project in Joseph City. The network will interconnect with existing fiber networks and facilitate future connections to Phoenix, neighboring counties, tribal networks, and an I-40 corridor expansion to Albuquerque, NM.

This infrastructure is transformative for Aztec’s land. Fiber connectivity is a necessary precondition for any modern commercial or industrial development, including data center support facilities, remote operations centers for renewable energy, agricultural technology, and telecommunications. The network runs directly through Aztec’s land corridor, effectively adding a fourth utility connection (after power, water, and transportation) to the property.

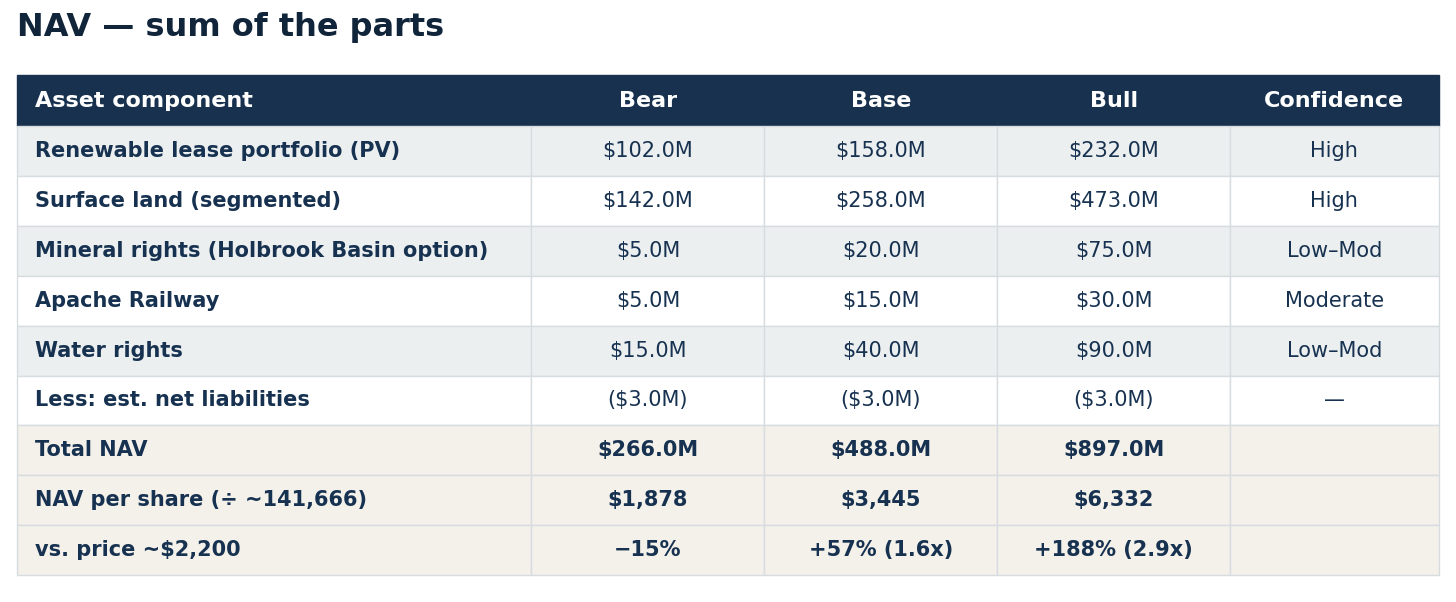

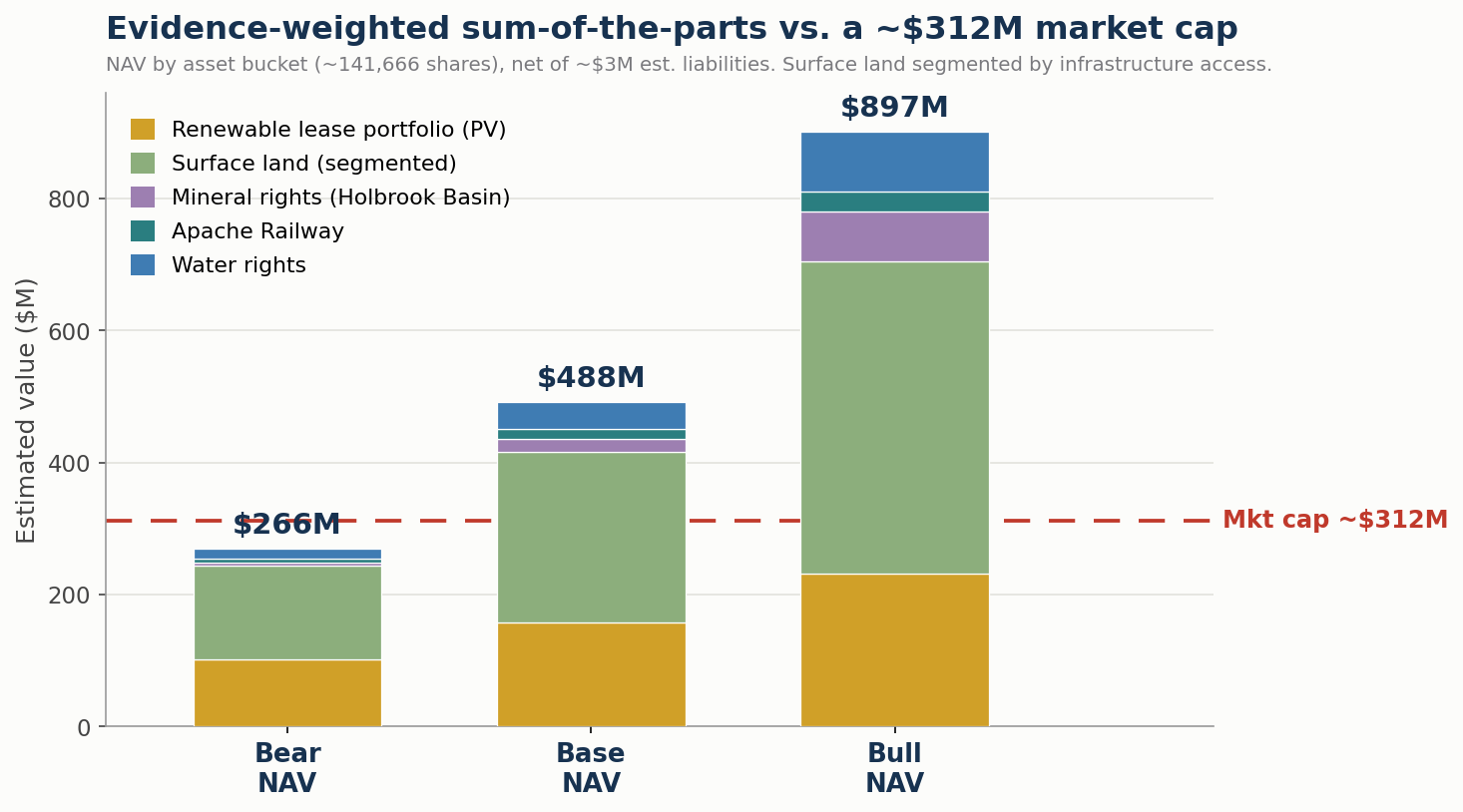

The NAV Summary

Consolidating the assets at base-case estimates, each weighted by confidence. The build is structurally tighter than an aggregate per-acre approach - it segments the land and caps the renewables on contracted income - and it is more defensible because every line is backed by a named project, dated transaction, or third-party disclosure.

The asymmetry. The bear case assumes the contracted, largely-operating renewable build reaches its low-end steady state and values everything else at or near a floor (land at its grazing comp, minerals minimal, the railroad at scrap, water minimal) - and even then sits only ~15% below today’s price. Against that, the base is +57% (1.6x) and the bull +188% (1.9x): the contracted income now sets the floor, so the asymmetry is heavily skewed up. The discount is narrower than a stale share count would suggest, but it is real and it is backed by contracted, ramping lease income, 234,800 acres, a railroad and water - not a per-acre guess.

What the market is missing

The accounting hides the assets. Tax-basis books carry land and minerals at 1885 cost basis.

The classification is wrong. “Cattle ranching services” is a 19th-century label on a 21st-century energy-infrastructure landowner - and investors, indexers and quants act on the label.

The lease portfolio is contracted, not hypothetical. AES and Invenergy are building, under APS offtake, with a disclosed rent floor.

The land isn’t homogeneous. Segmenting by infrastructure access lifts the defensible base value well above the level implied at the current price.

The Holbrook Basin is a free option. Potash, ~10% helium, and CO₂ pore space - each independently monetizable - are valued at roughly zero.

The duration is unpriced - this compounds for decades. The slow, expensive backbone is already sunk: the Cholla 500 kV interconnection, the Apache Railway and BNSF mainline, I-40, gas, and the long-haul fiber that runs the corridor. Aztec leases access to that backbone rather than building it, so each successive wind, solar, storage, mineral, or development deal drops incremental, high-margin ground rent onto a fixed, paid-for asset base. Pair that with a multi-generational owner that reinvests, buys back stock, and refuses to sell and you have a machine that keeps adding contracted cash flows for decades. This is the TPL playbook: a fixed land-and-royalty base that compounded at ~17% for 40 years.

Risks

Liquidity is brutal. With ~141,666 shares and a few traded per day, you cannot build or exit without moving the price. Assume you may be locked in for years - the single largest practical risk. Size accordingly.

You are a minority in a controlled company. Family-stewarded, negligible dividend, no obligation to surface value. You are paid in eventual NAV convergence, not cash along the way - and TPL minorities fought a multi-year governance war over exactly this.

The leases are still ramping. West Camp Wind I began producing in Q2 2026, but Hashknife I and II and the new 400 MW project are under construction; project finance, interconnection, or offtake could still slip. The ~$8–$13M steady state is a 2027–2029 event, not a 2026 one.

Disclosure is thin and tax-basis. You are underwriting an asset base you cannot fully verify from filings. This NAV is a reasoned estimate, not a marked book.

Minerals and water are unproven. Potash needs higher prices; helium/CO₂ need an operator; water is unadjudicated. Treat all as upside, not foundational.

Bottom line

Aztec Land & Cattle is a 141-year-old railroad land grant masquerading as a cattle company - ~239,000 acres of Arizona high desert carried at 1885 cost, wrapped around a retired coal plant’s transmission, now hosting a contracted, investment-grade renewable-lease portfolio, with the Holbrook Basin minerals, real water, and a short-line railroad on top managed by an owner-operator measuring time in generations.

Buy today at cattle land prices; get the contracted solar leases, the minerals, the water, the railroad, the fiber, the power and the flywheel for a fraction of what they are worth. That is the trade that made Texas Pacific Land one of the great compounders of the modern era. Aztec is standing at the same trailhead - illiquid, ignored, and mispriced.

Very interesting topic. I would be very interested to see you cover TPL and LB.

Where were you when it was $100 :(