Aztec Land and Cattle (AZLCZ) | Part 1 : Second-Largest Landowner in Arizona

40%+ Discount to NAV | Power, Water, Fiber, Rail, and Scale Create Massive Optionality

Aztec Land and Cattle Company (OTC: AZLCZ) is one of the most mispriced real asset stories in the public markets. Founded in 1884, Aztec is the second-largest private landowner in Arizona, controlling approximately 239,000 contiguous surface acres and 318,000 acres of mineral rights across Navajo and Coconino Counties.

The thesis is simple: the market treats Aztec as a sleepy cattle ranch, valuing the land at a fraction of comparable private-market transactions, while multiple secular tailwinds - renewable energy development, Arizona’s explosive power demand from data centers, and the structural scarcity of large-scale contiguous private land in a state where only 16% of land is privately held - are converging to dramatically accelerate the monetization timeline for these assets. We believe fair value sits meaningfully above the current share price on a conservative, normalized real estate NAV basis, with significant optionality from renewable energy lease escalations, mineral rights, and long-duration development.

COMPANY OVERVIEW

Aztec Land and Cattle Company was incorporated in 1884–1885 by a group of Eastern industrialists and Texan cattlemen who purchased a one-million-acre tract from the Atlantic & Pacific Railroad in northern Arizona for $0.50 per acre. Over the ensuing 140 years, parcels were sold, but beginning in the 1960s, the company shifted strategy toward land consolidation, steadily acquiring adjacent parcels to build an economically usable contiguous block. Today, the company and its affiliates control roughly 239,000 surface acres and 318,000 mineral acres.

The land stretches from Holbrook and Joseph City in the north to Heber and south of Snowflake/Taylor in the south, with Route 77 forming much of its eastern border. Most property exists in a checkerboard pattern interspersed with Bureau of Land Management (BLM) and State Land sections - a legacy of the original railroad land grants - though decades of consolidation have made the holdings substantially more contiguous than they once were.

Corporate Structure

Aztec operates through two primary entities. Aztec Land and Cattle Company, Limited is the publicly traded corporation (AZLCZ on OTC Markets). Aztec Land Company, LLC is a related entity that holds additional acreage and subsidiaries including the Apache Railway Company. Related subsidiaries include Despain LLC (6,443 acres) and East Jeffers LLC (14,143 acres). The company re-domesticated from New York to Delaware in 2023.

Management: The Brophy Family

Steven M. Brophy serves as President, CEO, and Chairman. His family has deep roots in Arizona - they immigrated from Ireland in 1879, and the Brophy name is associated with some of the state’s most significant philanthropic and business institutions (including Brophy College Preparatory in Phoenix). Brophy operates with a long-term, generational mindset. He has publicly stated that the company has never wanted to sell its land and does not intend to. This patient, stewardship-oriented approach is both the company’s greatest strength and the principal source of investor frustration.

Management has been increasingly proactive over the past decade: consolidating land, acquiring the Apache Railway out of bankruptcy, negotiating renewable energy leases, initiating a share buyback program, and engaging with Navajo County on area planning. The cadence of shareholder updates has accelerated meaningfully since 2021, with communications on renewable projects, buybacks, and distribution activity. This is not a management team asleep at the wheel - it is one playing a very long game with irreplaceable assets.

ASSET-BY-ASSET INVENTORY & NET ASSET VALUE

The fundamental challenge in valuing Aztec is that its assets are carried on the balance sheet at historical cost (originally $0.50/acre), bearing no resemblance to current market value. A proper NAV analysis must be built from the ground up.

1. Surface Land: 239,000 Acres

Comparable Transactions

Several data points bracket the value of Aztec’s surface acreage:

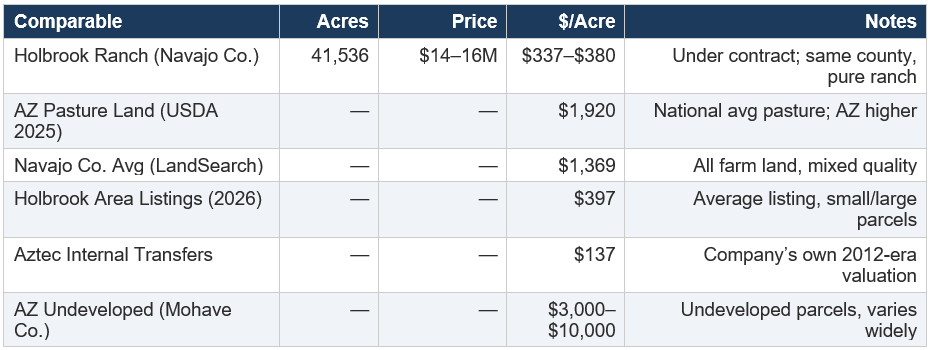

The Holbrook Ranch, a 41,536-acre property in the same county, is currently listed (under contract) at $14–15.8 million, implying roughly $337–$380 per acre for pure ranch land with no renewable energy or railroad optionality. This is the single most relevant comparable for Aztec’s base ranch value. However, Aztec’s holdings are roughly 5.7x larger, contiguous, and come with existing revenue-generating renewable energy leases and infrastructure access that the Holbrook Ranch lacks.

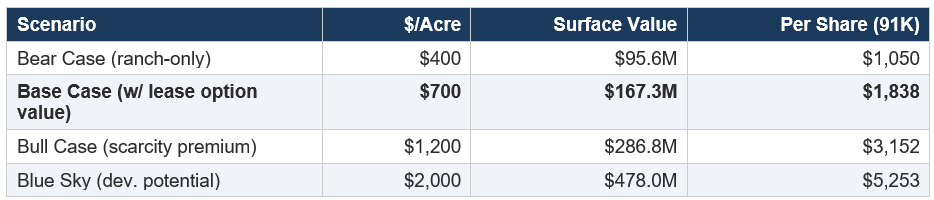

For a conservative base-case ranch valuation, we use $400/acre (a modest premium to Holbrook given Aztec’s size, infrastructure, and revenue). A mid-case uses $700/acre reflecting renewable lease option value and scarcity. An upside case uses $1,200/acre, still below the national pasture average and well below what Arizona land commands in growth corridors.

Surface Land NAV Summary

2. Mineral Rights: 318,000 Acres

Aztec controls approximately 318,000 acres of mineral rights, some of which extend beyond their surface holdings into Coconino County. Historically, there has been interest in potash deposits underlying portions of Aztec’s land, though no commercial extraction has materialized. Mineral rights in Arizona are valued conservatively at $25–$100 per acre for ranch-associated subsurface minerals with no active production, but can reach $500+ in areas with proven reserves.

A conservative valuation of $50/acre across 318,000 mineral acres yields $15.9 million, or approximately $175 per share. A more aggressive $150/acre (reflecting potash option value and the potential for future subsurface leasing) would yield $47.7 million, or $524 per share. We use $50/acre as our base case, recognizing this as a free option with no current cost to maintain.

3. Apache Railway

Aztec and its partners acquired the Apache Railway Company out of bankruptcy. This Class III short-line railroad runs 55 miles off the BNSF Railroad’s transcontinental mainline near Holbrook and serves much of Aztec’s land. The railroad is not primarily a revenue generator - it is a strategic infrastructure asset that provides rail connectivity for potential commercial and industrial development along Aztec’s holdings. The West Snowflake Railpark development concept is built around this asset. We assign a conservative $5–10 million value to this infrastructure, recognizing it as a development enabler.

4. Renewable Energy Leases

This is where the thesis gets interesting. Approximately 61% of Aztec’s revenue in 2023 came from renewable energy development leases. Major projects on or adjacent to Aztec land include:

Wind Energy

The Chevelon Butte Wind Farm (AES) is a facility spanning approximately 42,000 acres of private and state land near Aztec’s holdings. The project’s first phase became operational in 2023. The West Camp Wind Farm (AES) is a planned 504 MW wind energy project sited on approximately 35,000–45,000 acres of majority privately owned land, with construction expected to commence in 2024 and operations by late 2025. Aztec receives per-turbine construction impact fees upon commencement and ongoing operational royalties (the greater of a per-turbine fee or a percentage of revenue). Approximately 112 turbines are planned.

Solar Energy

Navajo County approved the Lark Point Solar project on land owned by Aztec. Multiple solar development leases have been executed, with the most recent shareholder update from March 2026 referencing additional solar energy project activity. Solar lease rates typically range from $250–$2,000 per acre per year nationwide, though rates in Arizona’s high desert can fall on the lower end for non-irrigated pasture land.

Renewable Lease Revenue Model

If we assume 80,000 acres are currently under or committed to renewable energy leases at a blended rate of $30–$50 per acre per year (accounting for a mix of wind royalties, solar lease payments, and development fees), this implies annual lease revenue of $2.4–$4.0 million. At a 15x–20x capitalization rate appropriate for long-duration, inflation-protected lease income, this revenue stream alone is worth $36–$80 million, or $396–$879 per share. As additional projects come online and lease escalators take effect, this value should grow steadily.

5. Grazing Leases & Other Income

Traditional grazing leases generate modest but stable income. These multi-year agreements with local ranchers provide a small but steady cash flow base. Other income includes interest on intercompany notes and occasional land sale proceeds.

WHAT THE MARKET IS MISSING

1. The Renewable Energy Inflection Is Real and Accelerating

When early blog posts analyzed Aztec in 2012–2014, the renewable angle was speculative - a small wind lease generating $140,000 per year. Today, renewable energy accounts for over 60% of corporate revenue, with a 400+ MW wind farm under construction and multiple solar projects in the pipeline. This is not incremental progress; it is a fundamental transformation of the revenue model. AES, one of the world’s largest energy companies, has committed billions to wind and solar development on and around Aztec’s land.

2. Arizona’s Power Crisis Creates Massive Demand for Energy Land

Arizona is experiencing one of the fastest growth rates in electricity demand in the country, driven overwhelmingly by data center construction. In 2025, Arizona’s electricity demand grew by 8% - four times the national average. APS (Arizona Public Service), the state’s largest utility, has received so many data center requests that it has been turning customers away. If every requested data center were accommodated, APS’s demand would jump from 8,200 MW to 19,000 MW.

This is not theoretical. Google is building data centers in Mesa, Arizona with 400 MW of demand. A proposed 1.5 GW development near Buckeye received zoning approval in late 2025. APS plans to install 6 GW of new renewable capacity between 2025 and 2031 to replace retiring coal plants. The retired Cholla Power Plant - located directly adjacent to Aztec’s land near Joseph City - has a 500kV switchyard and high-voltage transmission infrastructure that wind and solar projects on Aztec’s land are actively connecting to. Aztec’s land sits at the intersection of massive power demand and critical grid infrastructure.

3. Structural Land Scarcity in Arizona

Only 16% of Arizona’s land is privately held - the rest is federal, state, or tribal. This is dramatically lower than surrounding states and creates a persistent scarcity premium for large-scale private land. Aztec is the second-largest private landowner in the state, controlling one of the last remaining large-scale contiguous tracts of rural private land available for development. You cannot replicate or manufacture this asset. The checkerboard consolidation took 140 years.

4. Zero Institutional Coverage and OTC Listing

AZLCZ trades on the OTC Pink Sheets with no analyst coverage, no index inclusion, and extremely limited liquidity. The stock is invisible to institutional capital. This structural obscurity is precisely what creates the opportunity - there is no competition to analyze these assets and no mechanism to force price discovery until something catalytic occurs.

5. Balance Sheet Land Is Carried at Historical Cost

Aztec’s 239,000 acres are carried on the balance sheet at decades-old historical cost, bearing no relation to current market value. This makes any financial statement analysis meaningless for valuation purposes. Investors who screen on P/E, P/B, or other accounting metrics will never find this stock. You have to do the NAV work from first principles.

THE AI ANGLE: LONG-DURATION OPTIONALITY

The AI boom is the most powerful demand driver for electricity in a generation. Data centers accounted for 4% of total U.S. electricity consumption in 2024, and that figure is expected to more than double by 2030. Arizona is one of the top target states for new data center construction due to its land availability, low natural disaster risk, favorable tax environment, and expanding renewable energy capacity.

Aztec’s land is not positioned for direct data center construction - these facilities require urban or suburban infrastructure that rural Navajo County currently lacks. However, the AI-driven power demand creates a massive secondary demand for the exact assets Aztec controls: large-scale renewable energy sites with grid connectivity. Every gigawatt of data center capacity built in Arizona requires corresponding renewable energy capacity to be built somewhere. The wind and solar projects on Aztec’s land are supplying exactly this demand. APS’s Cholla substation and the regional 345kV and 500kV transmission lines running through Aztec’s territory are the connective tissue between renewable generation and urban load centers.

Over a 10–20 year horizon, the compounding effect of AI-driven electricity demand on the value of land with grid access and renewable energy potential is substantial. If Arizona adds 6–10 GW of renewable capacity over the next decade, and a meaningful portion of that capacity is built on or near Aztec’s holdings, the cumulative lease revenue and land appreciation could be transformative.

POWER CONNECTIVITY AND WATER SITUATION

Power Infrastructure

Aztec’s land benefits from extraordinary grid connectivity relative to its rural location. The Cholla Power Plant complex, which operated a 1.02 GW coal-fired facility near Joseph City for over 60 years before its retirement in March 2025, sits on or directly adjacent to Aztec’s holdings. The Cholla switchyard features a 500kV bus interconnected with two 345kV lines to Pinnacle Peak, a 500kV line to Saguaro, and additional 345kV and 500kV lines from Four Corners and Coronado. This is institutional-grade transmission infrastructure in a rural setting.

Both the Chevelon Butte and West Camp wind farms are designed to interconnect at or near the Cholla/Sitgreaves substations. New transmission line applications are underway for West Camp 2, including options for a 345kV or 500kV line to the existing APS Sitgreaves Substation or a 500kV connection to the SRP Cholla-Sugarloaf-Coronado line. The existing infrastructure reduces interconnection costs and timelines for new renewable energy projects - a critical competitive advantage in a market where transmission access is the primary bottleneck for new generation.

Water

Water is the perennial concern for any Arizona land investment. Aztec’s land sits atop the Little Colorado River (LCR) basin aquifer. Historically, APS pumped approximately 3.5 billion gallons per year from wells on Aztec’s land (under a lease for roughly $10/acre/year) to supply the Cholla plant’s cooling operations. The contract expired, leading to a notable condemnation lawsuit in 2006–2007 where APS sought to condemn approximately 7,000 acres to secure water access. This litigation highlighted the strategic importance of Aztec’s groundwater resources.

The July 2024 shareholder update referenced the LCR Adjudication - a legal proceeding to determine water rights in the Little Colorado River watershed. The resolution of this process could formally establish and quantify Aztec’s water rights, which would be a significant positive catalyst given that water rights in Arizona are among the most valuable and contested assets in the state. With the Cholla plant retired, the 3.5 billion gallons previously consumed annually are now potentially available for other uses - including renewable energy operations (which use relatively little water) or future development.

Wind energy, critically, requires almost no water to operate. Solar facilities use minimal water for panel cleaning. This makes Aztec’s pivot toward renewable energy leasing an elegant solution: it monetizes the land at premium rates while consuming almost none of the water, preserving that resource for its highest and best future use.

CATALYSTS FOR A FUNDAMENTAL RE-RATING

Near-Term (0–2 Years)

West Camp Wind Farm construction completion and operational revenue commencement will create a step-function increase in lease income, likely making renewable energy over 70–80% of revenue. Additional solar project approvals and lease executions (as indicated by the March 2026 update) will further validate the renewable monetization model. Share buybacks at below-NAV prices are accretive to per-share value. Resolution or advancement of the LCR water adjudication could formally quantify water rights value.

Medium-Term (2–5 Years)

Potential for additional phases of wind and solar development as Arizona continues to build out renewable capacity to meet data center demand. Increasing visibility of Arizona’s land scarcity premium as the state’s population continues growing by 90,000+ residents annually. Possible mineral lease development or potash exploration as commodity markets evolve. Railpark development along the Apache Railway corridor could begin generating industrial lease income.

Long-Term (5–20 Years)

Navajo County is one of the last frontiers for development in Arizona as growth pushes north from the Phoenix metropolitan area. The company’s 2012 area plan contemplated gradual rezoning of portions of holdings from agricultural to mixed commercial and residential use. At even modest development densities on a small portion of the acreage, the value creation would be orders of magnitude above current valuations. This is a truly generational optionality that is currently priced at zero.

WHY THESE ARE TRULY SCARCE ASSETS

Not all land is created equal. What makes Aztec’s holdings genuinely irreplaceable, rather than merely large, is the combination of several characteristics that cannot be assembled from scratch:

Contiguity at scale. 239,000 acres of substantially contiguous private land in a state where 84% of land is government-owned. This took 140 years of consolidation. No developer can replicate it.

Grid infrastructure. Direct access to 500kV and 345kV transmission from the retired Cholla complex. Transmission is the #1 bottleneck for renewable development nationwide. This advantage is permanent and structural.

Rail connectivity. 55 miles of short-line railroad connecting to the BNSF transcontinental mainline. Industrial and commercial development requires multimodal transport access that is exceptionally rare in rural Arizona.

Proven renewable resource. Demonstrated wind and solar resource quality, validated by AES committing over $1 billion in development capital to projects on the land. The wind and solar resource has been measured and certified.

Water rights. Groundwater resources in the LCR basin that previously supported a 1 GW power plant’s cooling needs. With the Cholla retirement, this water capacity is freed up.

Strategic location. Situated between Holbrook (I-40 corridor) and Snowflake/Taylor, along the natural growth axis of northern Arizona development.

Comparable publicly traded land companies like LandBridge (NYSE: LB), which owns approximately 315,000 surface acres in the Permian Basin, trade at over $4 billion in enterprise value and generate revenue of $1,159 per legacy acre. While LandBridge’s acreage sits in the oil-rich Delaware Basin and is not directly comparable, the valuation framework demonstrates what the public market is willing to pay for strategically located land with optionality. Aztec’s market cap of $146 million implies roughly $611 per surface acre with zero value for mineral rights, railroad, or renewable optionality - a fraction of comparable asset values.

RISKS AND CONSIDERATIONS

Liquidity. AZLCZ is one of the most illiquid publicly traded securities in existence.

Time to monetization. The primary risk is patience. Full value realization may take 10–20+ years. Investors receive minimal cash returns while waiting, though the recent initiation of small distributions and buybacks is encouraging.

Governance. As a closely held company with limited disclosure, shareholders have minimal influence over management decisions. Trust in the Brophy family’s stewardship is essential.

Regulatory. Changes to renewable energy policy (e.g., the 2025 One Big Beautiful Bill Act repealing certain federal solar subsidies) could slow development timelines. However, projects already under lease or construction are largely insulated.

Water. Arizona’s structural water scarcity is a double-edged sword - it constrains development potential but also makes existing water rights extraordinarily valuable.

Concentration. Revenue is heavily concentrated among a few large renewable energy lessees, creating counterparty risk.

VALUATION CONCLUSION: IS THIS FAIRLY VALUED?

At $1,610 per share, Aztec trades at approximately our bear-case NAV, which strips out all optionality and values the land as a pure ranch at prices comparable to the Holbrook Ranch transaction. In our view, this is not a fair valuation because it assigns zero value to:

• The existing renewable energy lease portfolio generating majority revenues • 318,000 acres of mineral rights • The Apache Railway and its development-enabling infrastructure • 500kV/345kV grid connectivity from the Cholla complex • Groundwater resources previously supporting a 1 GW power plant • Optionality from Arizona’s fastest-in-nation electricity demand growth • The structural scarcity of 239,000 contiguous private acres in a state with 16% private land

Our base-case NAV of $2,667 per share represents approximately 65% upside from current levels. Given the time value of money and the long-duration nature of these assets, a discount of 15–20% to our base NAV is reasonable to account for illiquidity and monetization timeline risk, implying a fair range of $2,100–$2,300 today with significant additional upside as renewable revenue ramps and development catalysts materialize.

Asymmetric Upside: What Creates It?

The asymmetry in Aztec comes from the fact that the downside is well-protected by hard asset values (the land is real, it is not going away, and it generates income), while the upside scenarios are genuinely transformative. If Arizona’s renewable buildout accelerates as expected, if the LCR water rights are favorably adjudicated, if even a small portion of the land is eventually rezoned for development, or if a strategic acquirer recognizes the value of a 239,000-acre contiguous block with grid infrastructure in a power-starved state - any of these scenarios could drive the stock to multiples of its current price. The risk/reward is compelling: limited fundamental downside with multiple paths to substantial value creation.

WHAT DOES AZTEC LOOK LIKE IN THE FUTURE?

In five years, Aztec will likely be a diversified land management company generating $5–10 million annually in renewable energy lease revenue, with multiple wind and solar projects operational across tens of thousands of acres. The share buyback program will have reduced the float further, concentrating value among remaining shareholders. Water rights will likely be formally quantified through the LCR adjudication.

In ten to twenty years, the combination of Arizona’s population growth (currently adding roughly 90,000 residents per year), northward development pressure from the Phoenix metro area, and the state’s insatiable demand for energy infrastructure could transform Aztec from a land company into something resembling a small-scale LandBridge - a platform monetizing surface, mineral, water, and infrastructure rights across a vast and irreplaceable land base. The transition from pure ranch to diversified real asset platform is already underway. The market simply hasn’t priced it yet.