Alico, Inc. (ALCO): The Juice Is Worth the Squeeze

Forget the oranges - ALCO is a Florida land bank trading at half of NAV

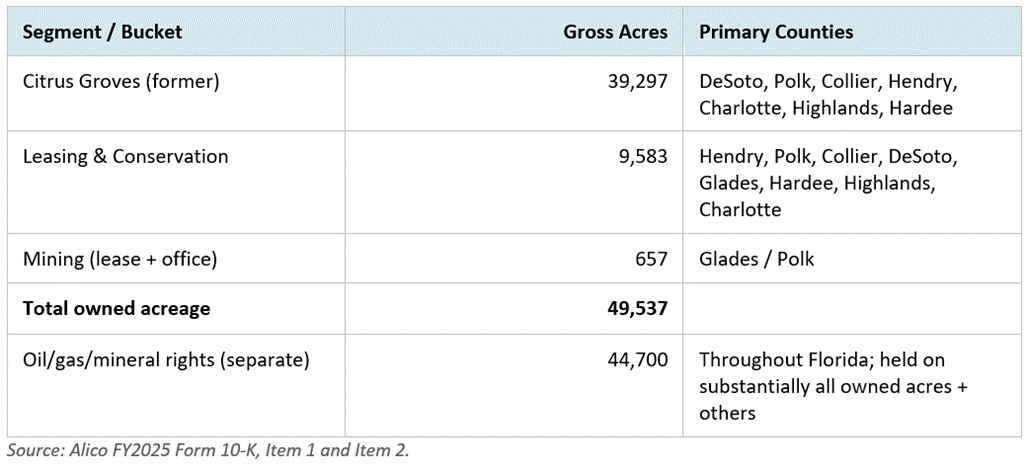

Alico, Inc. (ALCO) is a publicly-traded Florida land holding company with 49,537 owned acres plus 44,700 acres of mineral rights, currently priced as a melting citrus stub instead of what it actually is: a low-leverage, tax-advantaged, rural-to-suburban land bank in the direct growth path of southwest Florida, run by a CEO whose compensation is now tied almost entirely to land monetization.

Management’s own appraised value of $650–750M is conservative once you decompose the portfolio. Our base-case market-based NAV is ~$760M, or roughly $99/share - a 145% premium to the current $40 price. The bull case ($1.0B+, $130+/share) is unlocked by the Corkscrew Grove Villages entitlement compounding through 2026–2028 and a credible reset of ag-land comparables off the FY2025 Joshua Grove signed price of $9,000/acre. The bear case (a botched entitlement, a 1031-trade-replacement screwup, or a Florida hurricane cycle) still rhymes with current book value of ~$32/share.

The market is anchored to two stale narratives that are no longer operative: (1) ALCO is a citrus business - it isn’t, the trees were impaired and the Tropicana contract was terminated by mutual agreement in May 2025; and (2) Florida land company NAV bridges don’t close - but ALCO has now closed $110M+ of land sales over 30 months at prices that validate, not undermine, the appraisal stack. Every quarter from here is mark-to-market evidence.

The Setup

On January 6, 2025, ALCO announced it was winding down its citrus operations and reorganizing as a diversified land company. This was not a soft pivot. By the end of the fiscal year (Sep 30, 2025), the company had: (i) abandoned the trees on ~90% of producing acreage and taken $162.7M of accelerated depreciation, (ii) eliminated 172 of its ~190-person workforce (it now operates with 20 full-time employees), (iii) terminated its Tropicana orange purchase agreement in its entirety, (iv) authorized a $50M share buyback (~16% of the float), (v) increased the CEO’s incentive comp to include real-estate-commission-style bonuses and PSUs at $35/$40/$45 thresholds, and (vi) executed $23.8M of land sales in FY25 followed by $34.6M of additional land sales in the first four months of FY26 - including a $26.8M Hendry grove sale at $9,085/acre that closed January 2026.

In other words: this is not a management team “considering” a transformation. The transformation has substantively occurred. What’s left to happen is the entitlement of the Corkscrew Grove Villages master-planned community in Collier County, the entitlement of Bonnet Lake in Highlands County, and the methodical liquidation of the remaining ~40,000 acres of non-strategic ag land into a strong Florida buyer pool. The company is overcapitalized for what it now is: net debt of $47.4M at FYE25 against management’s own $650–750M appraisal of underlying land - a debt-to-asset ratio under 10%.

The interesting question isn’t whether the assets are worth more than the stock - every competent observer has noticed that. The interesting question is how much more, parcel by parcel, with what evidence, and against what catalysts. That’s what this post answers.

Asset Inventory (FY2025 10-K)

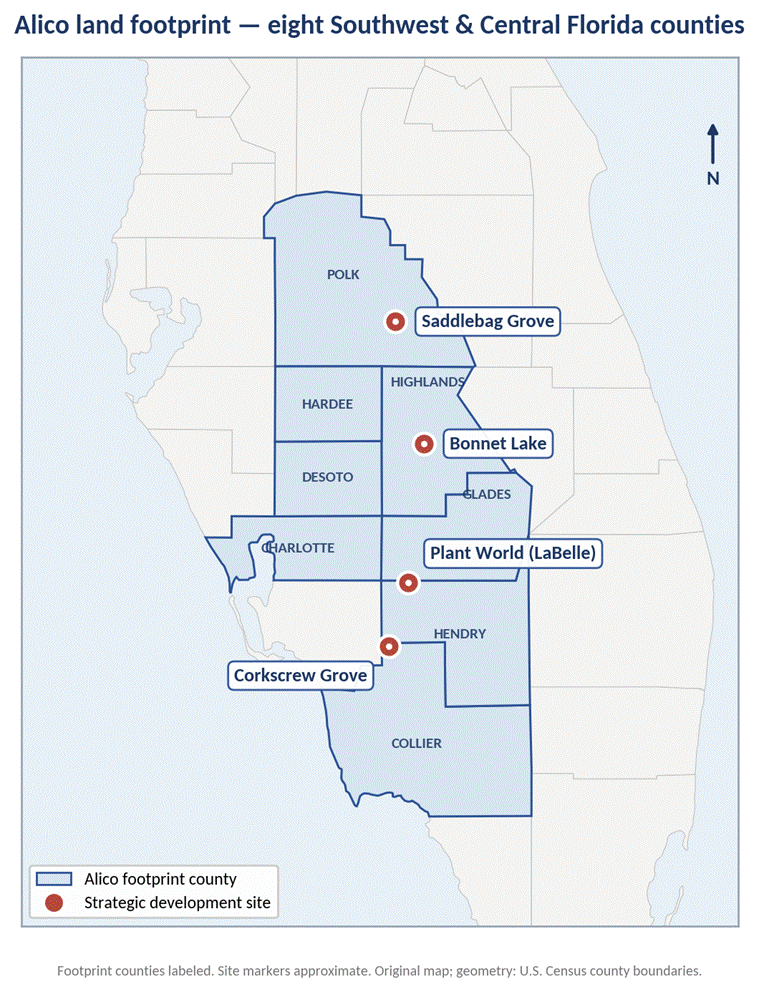

ALCO discloses its land in two segments as of September 30, 2025 - Alico Citrus (which is now a wind-down segment, not an operating one) and Land Management & Other Operations. The eight-county footprint and the breakdown below are the substrate of the entire thesis.

A full interactive map is available here

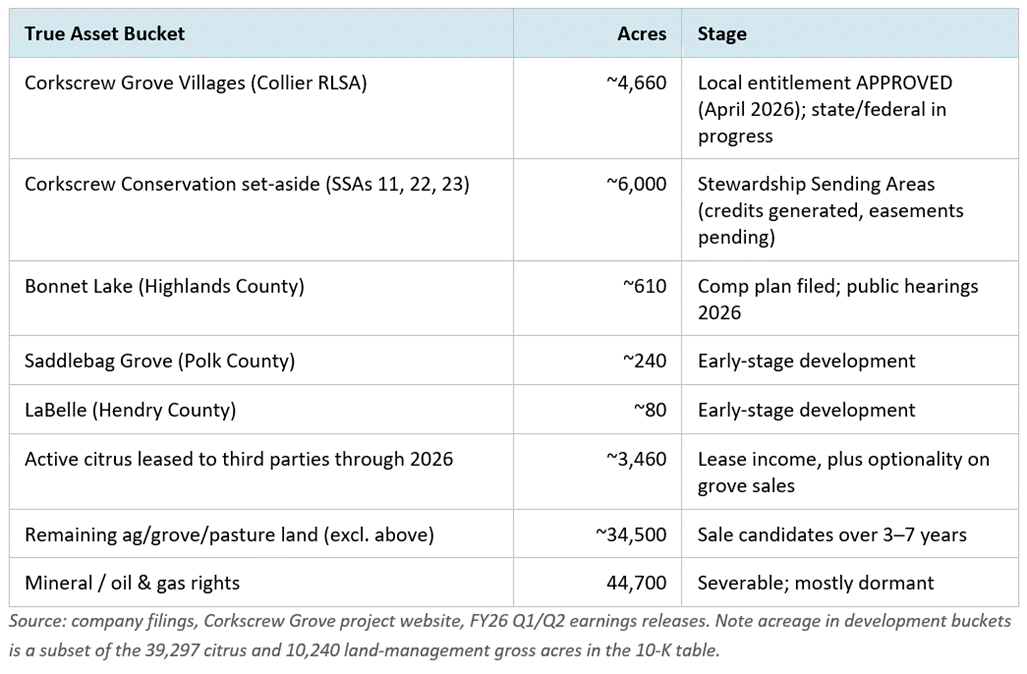

Important: the segment labels are misleading. Roughly 4,660 acres of the “Citrus Groves” bucket is actually the Corkscrew Grove Villages master-planned community in entitlement, which is a wholly different category of asset. Another ~3,460 acres are leased to third-party citrus operators through 2026. The true asset buckets are below.

These classifications matters because the per-acre value of these buckets ranges over almost two orders of magnitude. The Corkscrew development land, once federally permitted, will trade in the same comp set as Ave Maria and Babcock Ranch - finished-lot economics that imply $200,000+ per gross developable acre. The remaining ag land trades in a $9,000–$15,000/acre comp set. Conflating them is the single biggest reason the stock is mispriced.

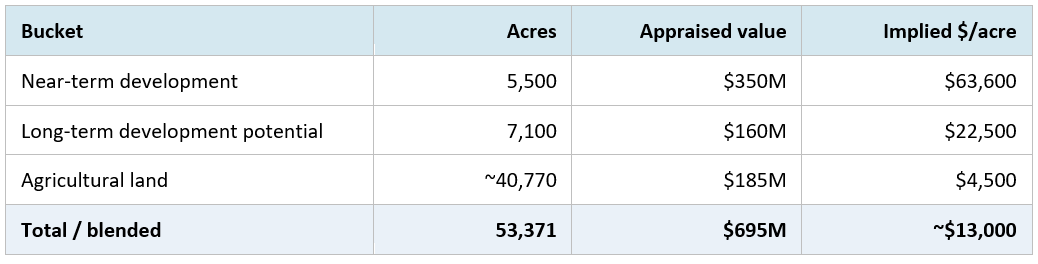

Alico’s own appraisal. The company’s Strategic Transformation investor deck (January 2025) explicitly broke its 53,371-acre footprint into three buckets: (i) 5,500 acres of near-term development land valued at $350M ($63,600/acre), (ii) 7,100 acres of long-term development potential valued at $160M ($22,500/acre), and (iii) ~40,770 acres of agricultural land valued at $185M ($4,500/acre). These figures were derived from third-party appraisers and real-estate experts engaged by the company. Note: this was an appraisal as of January 2025 - before local entitlement of East Village was approved in April 2026.

Asset-by-Asset NAV

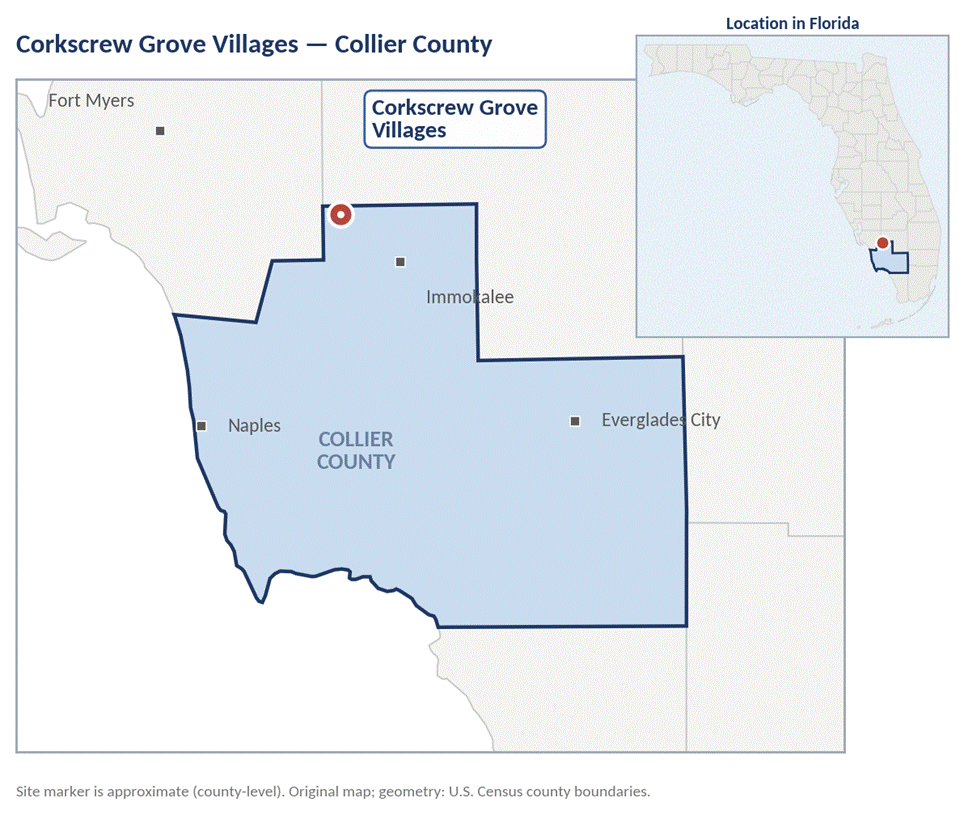

1. Corkscrew Grove Villages - Collier County (~4,660 development acres + ~6,000 conservation acres)

What it is

Two 1,500-acre mixed-use villages (East + West) at the intersection of Collier, Lee, and Hendry counties, accompanied by ~6,000 acres of permanent conservation. Planned for ~9,000 homes (4,500 each village), ~750 affordable housing units for essential workers, ~560,000 sq ft of total commercial space (retail, dining, office, medical, light industrial), an additional 100,000 sq ft of indoor self-storage on the East Village, and ~70,000 sq ft of civic space per village. Located on former Corkscrew citrus groves, with direct access to I-75 via Corkscrew Road and State Road 82 to the north.

Where it is in the entitlement process

This is the single most important active variable in the thesis, and it has been compounding favorably.

Mar 2025: SRA development application filed with Collier County; companion bill (HB 4041) filed to create the Corkscrew Grove Stewardship District.

Jun 2025: DeSantis signs HB 4041 — the district is created. (These districts self-fund roads, drainage, and utilities through assessments on future homeowners — the same vehicle used at Ave Maria and Lakewood Ranch, which trade at far higher per-acre values than ALCO’s mark.)

Mar 2026: County Planning Commission unanimously recommends approval.

Apr 2026: Board of County Commissioners grants final local approval.

Next: state (SFWMD) and federal permits, expected late 2026 / early 2027.

Construction: 2028–2029 at the earliest, with West Village to follow.

Valuation framework

The cleanest way to value entitled Florida RLSA land is to triangulate among (a) finished-lot pricing in comparable master-planned communities, (b) the per-acre price paid by national homebuilders for fully entitled land, and (c) Alico’s own historical investor-deck mark.

Comparable communities. Ave Maria, the original Collier RLSA Stewardship Receiving Area, was entitled for 11,000 residential units on roughly 4,000 acres (~2.75 units/acre). It has been a top-10 master-planned community in the U.S. for multiple years and sells homes from the high $200,000s to over $1 million. Babcock Ranch (Charlotte/Lee), the better-known Florida RLSA-adjacent comp, has been a top-15 MPC for three consecutive years, with 18,000 acres, 19,500 planned residences, and 6,000,000 sq ft of commercial. Its founder Kitson & Partners bought the 91,000-acre Babcock Ranch in 2006 and resold 73,000 acres to the State of Florida for preservation. Corkscrew is structurally similar in form factor - a state-supported, RLSA-vehicle MPC adjacent to a major metro growth path - but smaller and earlier in the curve.

Per-acre yardstick. Florida citrus and transitional land transactions in calendar 2025 (Saunders Real Estate, 79 sales, 20,352 acres) priced 12 “transitional” parcels - those with recognized development potential - between $18,031 and $56,003 per acre. Land in 2024 with explicit residential conversion priced even higher: the most striking comparable being a ~120-acre Lake County parcel that sold for $14.5M ($122,000/acre). Corkscrew is not a 120-acre infill site, but it is in a uniquely advantaged location with state-approved infrastructure financing - closer to the high end of the transitional-comp range than the low end.

Our Corkscrew NAV

Two paths:

Path A (development bucket only - base case): ~4,660 dev acres × management’s own $63,600/acre = $296M. This is the management mark, conservative because it predates the local entitlement approval. A modest re-rate to $80,000/acre on entitlement closure produces $373M.

Path B (homebuilder paper-out comp): 9,000 home sites × $35,000/site of land value paid by national builders in eastern Collier comps × ~75% net-of-development-cost realization = $236M; add commercial (560,000 sq ft × $35/sq ft of land value) = $20M; gross developer land value ≈ $250–280M. Adjusted for time value (5–7 years to full build-out) and discounted at 12%: $175–200M present value of just the residential paper-out - pre any conservation credit monetization.

Conservation conversion option (incremental). The ~6,000 acres of Stewardship Sending Area land surrounding Corkscrew is not zero-value real estate. It generates RLSA stewardship credits (each acre, fully restricted, can produce credits in the 1.2–8 credit range under Collier’s natural-resource-index methodology), and those credits are either retained for Alico’s own SRA entitlement or potentially monetized through future sale to other RLSA participants. Furthermore, this acreage is contiguous to the Devil’s Garden / CREW / Florida Wildlife Corridor footprint and is eligible for Florida Forever bid. The 2023 Devil’s Garden sale (Alico to FDEP) priced 17,229 acres of similar Hendry land at ~$77M, or ~$4,500/acre. At that floor, the 6,000 conservation acres are worth ~$27M in a worst-case bid sale, with significant optionality higher.

Corkscrew total NAV: $200M (bear) - $325M (base) - $425M (bull). I use a base of $320M ($43/share), reflecting (a) Path A management mark with a modest haircut to acknowledge time-to-paper-out, plus (b) $25M conservation credit / easement value.

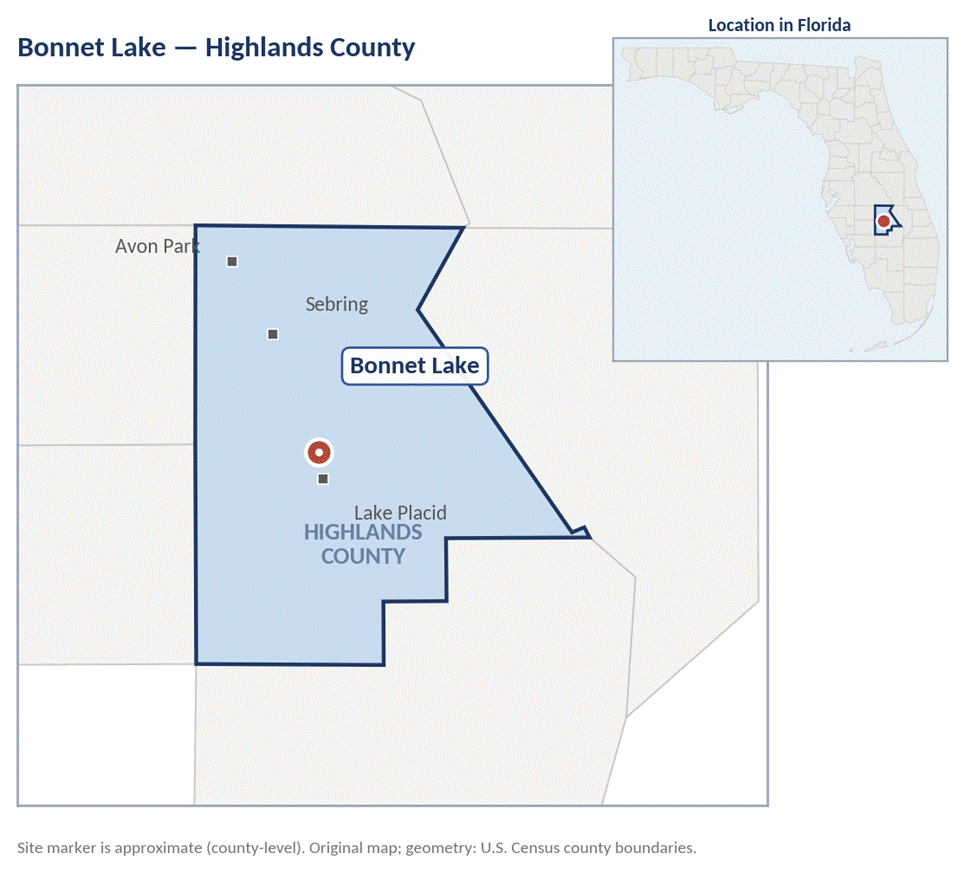

2. Bonnet Lake - Highlands County (~610 acres)

ALCO has a comprehensive plan amendment in process for ~610 acres in the Bonnet Lake area of Highlands County. The CEO has noted public hearings expected in 2026 and community outreach including 400+ residents. Highlands County is not a Collier-class location - but Highlands citrus and transitional land in 2025 traded in the $11,000–$25,000/acre range, with development-potential parcels at the high end.

Bonnet Lake NAV: $15–25M. I use $18M ($2.40/share), or ~$29,500/acre - a modest premium to comparable Highlands transitional land reflecting entitlement progress.

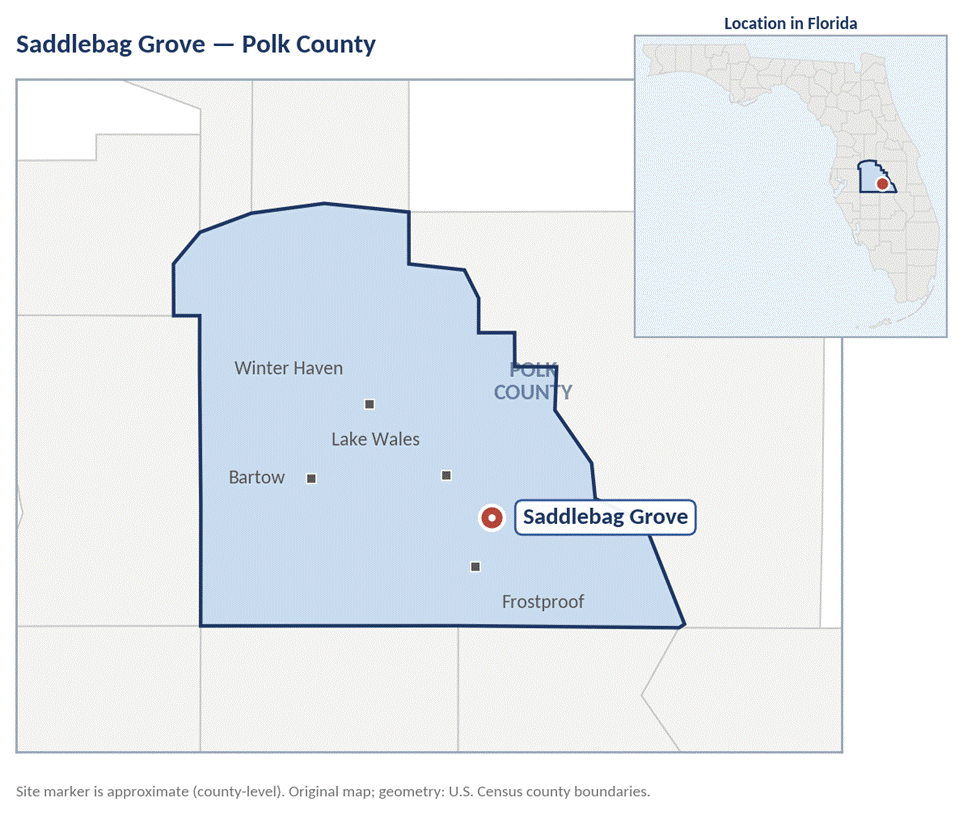

3. Saddlebag Grove - Polk County (~240 acres)

Polk County is one of the most active Florida transitional-land markets in 2025 (25 of the 79 statewide citrus transactions). Polk transitional parcels priced between $18,000 and $56,000/acre depending on road frontage, utility proximity, and upland percentage. At a midpoint of $30,000/acre, 240 acres = $7.2M. I use $7M ($0.95/share).

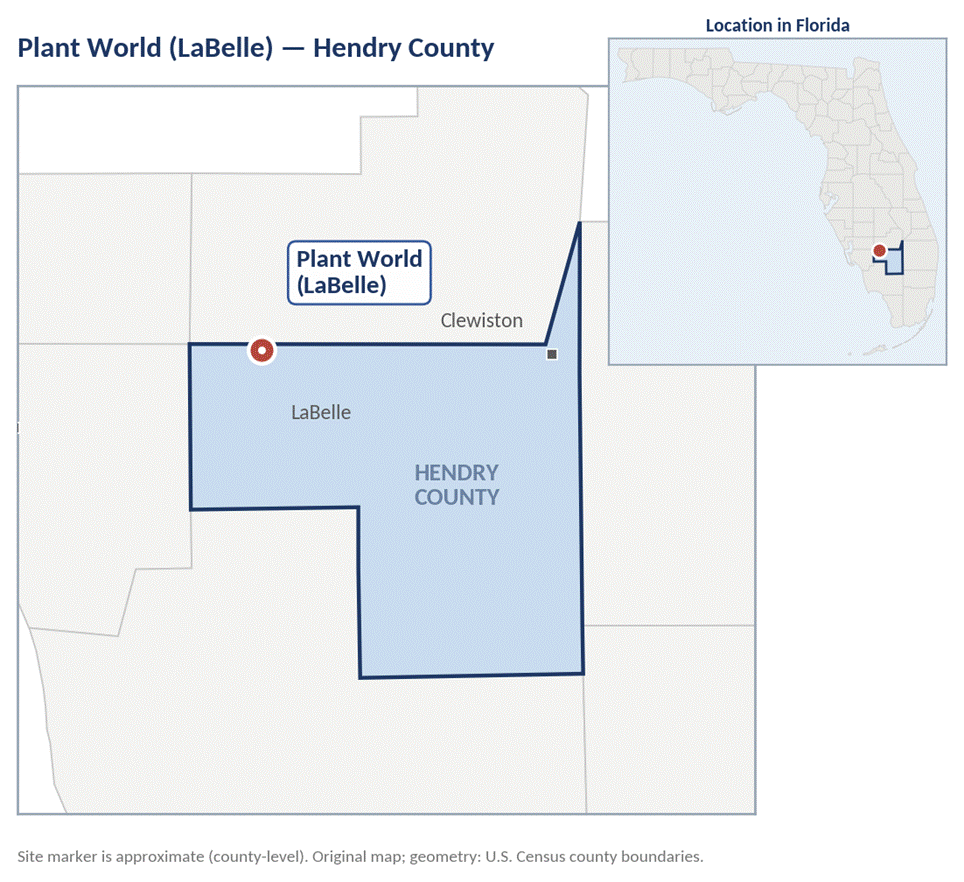

4. LaBelle - Hendry County (~80 acres)

Small parcel; LaBelle is a slower-growth Hendry market. At $15,000–$20,000/acre, 80 acres = $1.4M ($0.18/share). A rounding number, but disclosed as part of management’s near-term development pipeline.

5. Remaining Agricultural Acreage (~34,500 acres net of above)

This is where most of the NAV bridge actually closes. The single most important data point in the entire thesis lives in one 8-K filing from April 22, 2025.

The Joshua Grove signed transaction. On April 22, 2025, Alico and 734 LMC Groves, LLC executed a Purchase and Sale Agreement with Harford Farms LLC for the sale of Joshua Grove - 20,414.39 acres in DeSoto County - for $183,729,510, or exactly $9,000/acre. The agreement was terminated by the buyer on May 1, 2025 because Harford could not satisfy its financing contingency within the 30-day window. No penalties were paid. The grove went back on the market. Two important takeaways: (1) a private buyer signed a binding contract at $9,000/acre on more than 40% of Alico’s total land base - that is a market-validated bid for a third of the company’s portfolio at a single price point; (2) the deal fell apart because of buyer-specific financing, not asset-specific valuation. Subsequent transactions support the $9,000/acre level:

• January 2026: Sale of 2,950 acres of Hendry citrus land for $26.8M = $9,085/acre. • Q1 FY26: Sale of 579 acres of citrus land for $6.1M = $10,535/acre. • FY24: Sale of 17,229 acres of Devil’s Garden (Hendry) to the State of Florida for ~$77M (~$4,500/acre - note this is conservation land, not productive grove). • 2025 Florida citrus transaction average (Saunders): $13,788/acre across 79 sales totaling $204.9M.

Ag-land NAV. 34,500 remaining ag acres × $9,500/acre = $327M (bear case at the Joshua Grove floor). 34,500 × $12,000/acre = $414M (base case, reflecting that not all parcels are pure unimproved DeSoto). 34,500 × $14,000/acre = $483M (bull case, applying the 2025 statewide citrus-land transaction average). I use a base of $380M ($50/share), or ~$11,000/acre.

6. Water Rights - The Asset Nobody Models

Florida’s regulatory framework for water is largely consumptive-use-permit-based and administered by the regional water management districts (SFWMD for most of ALCO’s footprint, SWFWMD for some northern parcels). These permits are not freely transferable like Western water rights - but they are attached to specific acreage and convey with the land. The economic value of ALCO’s water rights is therefore embedded in the per-acre price of its land, plus a series of more visible specific assets:

(a) The 35,000-acre dispersed water storage project. Alico Water Resources, a wholly-owned subsidiary, holds a SFWMD permit to operate a 35,192-acre dispersed water storage site in Hendry County designed to intercept algae-laden discharges from Lake Okeechobee into the Caloosahatchee River. SFWMD valued the contract over its life at ~$124M of taxpayer payments to Alico for water storage. After the 2020 Florida Forever sale of 10,684 acres in the Devil’s Garden footprint, the original specific project was effectively suspended - but the underlying infrastructure footprint, permits, and regulatory relationships remain. This is an asset that does not show up on the balance sheet at meaningful value and has substantial option value if the C-43 reservoir scoping returns to dispersed-storage solutions, which has happened before.

(b) Consumptive-use permits on ag acreage. ALCO holds CUPs on substantially all of its irrigated citrus acreage. As citrus winds down, these permits - to the extent they remain in effect for replacement reasonable-beneficial uses - convey value to buyers of the underlying land, particularly for high-water-demand alternative crops (sod, vegetables, blueberries). They are a key reason ag buyers in Hendry and DeSoto are willing to pay $9,000–$12,000/acre for grove transitions - the water capacity is in place.

(c) Embedded value in the Corkscrew development. The Corkscrew Grove footprint sits within the Immokalee Water and Sewer District service area. Corkscrew’s 9,000 homes’ water-and-sewer connections, when entitled and constructed, will be served through that district - meaning the project does not need to develop its own well field or wastewater treatment. This is a real economic transfer of risk from Alico to the public utility, and a real reduction in the development-capital intensity of the project that most ag-company DCFs don’t model.

(d) Water-quantity scarcity premium. In a state where SFWMD has been progressively constraining new permits and where competing land uses (large-format farm, golf, master-planned community, mining) all demand the same aquifer, holding a CUP on tens of thousands of acres is itself a competitive moat. Buyers don’t pay separately for it, but they refuse to pay full price for parcels without it. This is why, in particular, the Devil’s Garden conservation sales fetched lower per-acre prices than the active grove sales: the state buyer didn’t need the water permits.

Water rights NAV: I do not assign a separate line item, but I bias our ag-land per-acre marks toward the high end of comparables in counties where permits convey ($11–14k/acre rather than $7–9k/acre). The implicit water-rights value embedded in those marks is on the order of $50–80M.

7. Oil, Gas & Mineral Rights (~44,700 acres)

Alico holds mineral rights on substantially all 49,537 owned acres, plus an additional ~44,700 acres of mineral rights held on leased or no-longer-owned acreage. Historically this generated very modest revenue - a few hundred thousand dollars per year of rock-mining royalty (Glades parcel acquired 2006; E.R. Jahna purchase option agreement was for 899 acres at ~$11,500/acre, expiring January 2025). Florida is not a meaningful oil and gas state. I value the entire mineral portfolio at $15M ($2/share), reflecting (a) the discrete value of active mining royalty parcels, (b) sand-and-aggregate optionality in growth-path counties (mining-grade aggregate near Florida construction demand is a real asset), and (c) the embedded value of dormant mineral rights on already-sold acreage - which is non-zero but easily ignored.

8. Operating Lease Income (~46,000 farmable acres at 97% utilization)

Following the citrus wind-down, Alico has transitioned to a land-lease model. Per the May 2026 Q2 earnings release, ~97% of farmable land is generating revenue under agricultural partnerships (sod, cattle, sugarcane, citrus caretaking, mining). FY2026 Adjusted EBITDA guidance is approximately $14M. At 8–10x EBITDA (typical for triple-net rural-land lease income), this stream is worth $110–140M as a going concern, but it is fundamentally embedded in the underlying land value rather than additive to it. I do not double-count. However, it is the bridge that funds operations and entitlement spend while land is monetized, and it materially reduces the urgency to do bad deals.

9. NOLs and Deferred Tax Assets

As of September 30, 2025, Alico has approximately $45.4M of federal NOLs and $42.6M of state NOLs. The company is also actively using Section 1031 like-kind exchanges on land dispositions, deferring gain recognition. The combination of (i) NOLs to shield income that does crystallize, (ii) 1031 to defer the rest, and (iii) the cost basis step-down from accelerated tree depreciation, makes Alico’s after-tax NAV closer to its pre-tax NAV than for most peer companies. I assign $15M ($2/share) to the present value of the NOL/1031 stack - conservatively, reflecting Section 382 risk on a future ownership change.

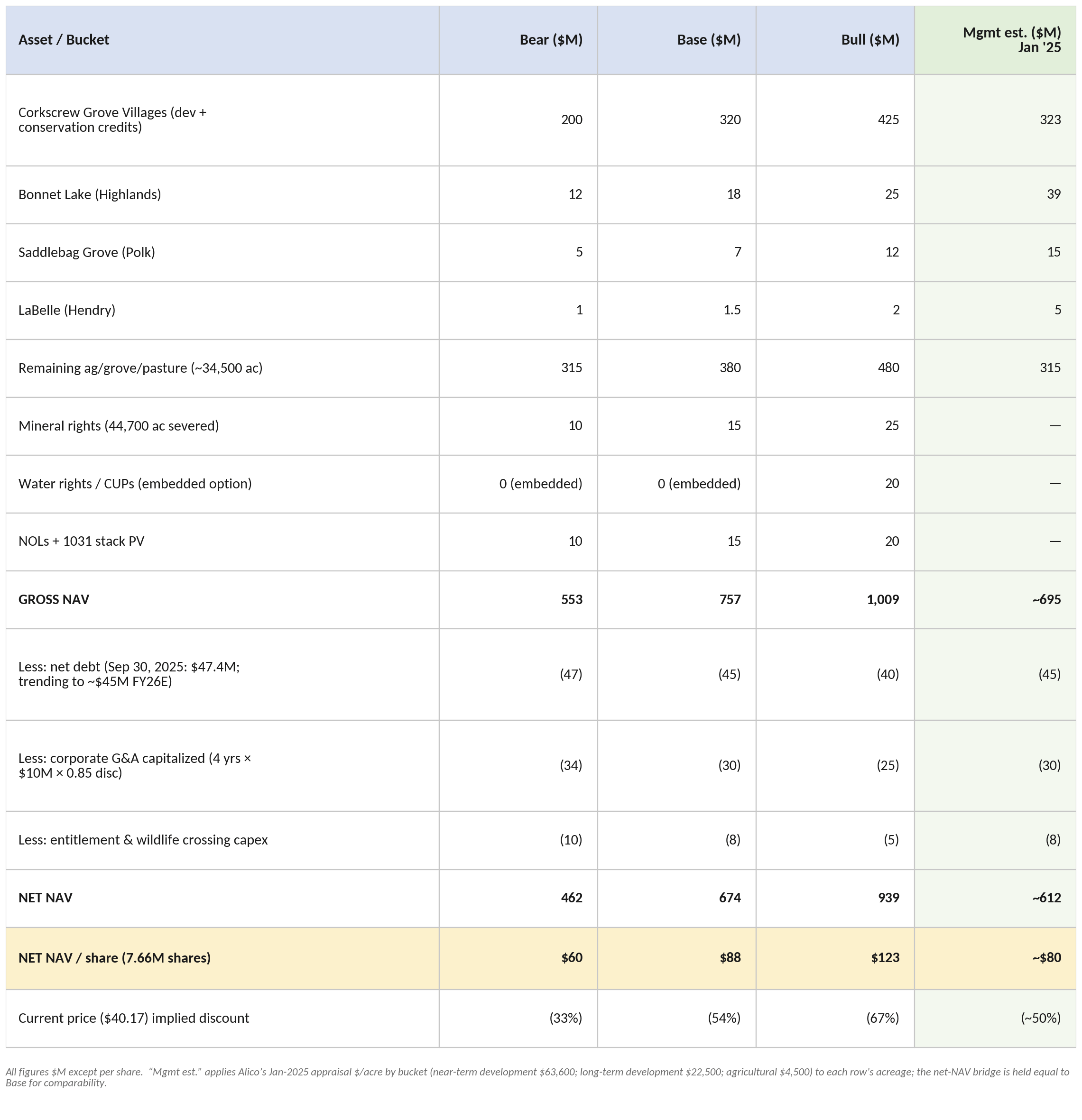

Consolidated Market-Based NAV

I treat our base case ($88/share) as the working number. The market price implies that I should weight our bear case at ~50% and assign zero probability to the bull case - which is inconsistent with the evidence of the past 12 months.

The Mgmt est. column applies Alico’s own January 2025 Strategic Transformation appraisal - near-term development land at $63,600/acre, long-term development at $22,500/acre, and agricultural land at $4,500/acre. The most important point is what it shows in aggregate: management’s own gross land mark of roughly $695M (squarely within their stated $650–750M range) is more than 2x the current $308M market capitalization. On Corkscrew, our Base ($320M) is essentially in line with management (~$323M). We sit below management on the three secondary development sites - Bonnet Lake ($18M vs $39M), Saddlebag ($7M vs $15M), and LaBelle ($1.5M vs $5M).

The severed mineral rights, water/CUPs, and NOL/1031 stack were not part of management’s land appraisal and would lift the gross further if added at our marks. Critically, the two value-creating events since the appraisal - Corkscrew’s local entitlement approval (April 2026) and the ag-land comp reset to $9,000+/acre - have only increased the underlying value relative to this column.

Management & Incentives

This is where the thesis stops being a static NAV exercise and starts being a probability-weighted bet on actually realizing the gap. Three observations on the executive structure:

(1) The CEO’s compensation has been explicitly retooled around land monetization

On December 23, 2024 - fourteen days before the public Strategic Transformation announcement - Alico entered into a Second Amended and Restated Employment Agreement with John Kiernan (President & CEO since July 2019), extending his term through September 30, 2027 and setting up a comp structure with three components: (i) base salary of $525,000; (ii) a real-estate-commission-style bonus tied to land sales executed in FY2025 and beyond, structured around specific performance metrics in the Bonus Agreement; and (iii) a Performance-Based Restricted Stock Unit award of up to 38,000 PSUs vesting through September 30, 2027, with the following price-trigger schedule:

• 5,000 PSUs earned if 30-day trailing avg price exceeds $35 • 12,500 additional PSUs earned if trailing price exceeds $40 (currently hovering at this level) • 20,500 additional PSUs earned if trailing price exceeds $45

These are real, dollar-weighted incentives. At $45 per share - the top tier - Kiernan picks up 38,000 PSUs worth $1.71M, in addition to land-sale commissions that pay him a percentage of monetized acreage. He cannot get the top-tier comp without delivering both a stock price re-rate and real land sale execution. The two are reinforcing, not substitutable.

(2) The board has authorized $50M of buybacks against a $300M float

Authorized in April 2025, expiring April 2028. Through April 2026, the company has repurchased 245,399 shares for $10M (~$40.75/share average). At current prices, the full authorization absorbs ~16% of shares outstanding. The buyback is dimensionally large relative to market cap and is being executed under 10b5-1 plans, meaning continued purchases through quiet periods - a structural source of demand.

(3) The shareholder structure is informed

734 Investors, LLC - owned by Remy Trafelet and George Brokaw - acquired its 50.5% controlling stake in 2013 for $137.8M at $37/share. They have held the position for 12+ years and have not been net sellers. George Brokaw, individually, remains a director and large beneficial owner. This is not a structure where shareholders are passive: they have engineered the strategic pivot through the board, hired Kiernan, retooled his comp, and are now overseeing the monetization. The interest of the controlling shareholder is precisely aligned with the public float at the level of capital-return and land-monetization economics - but there is a control premium concern (more on that below).

What the Market Is Getting Wrong

Misperception #1: “ALCO is a citrus stub.”

Until January 2025, this was correct. It is now obsolete. Citrus revenue declined from $96.6% to $93.8% of total in FY25 and will be near zero in FY26. The Tropicana contract - which represented 87% of consolidated revenue - was terminated by mutual agreement in May 2025. The trees were impaired for $162.7M of accelerated depreciation. The workforce was reduced from ~190 to 20. The company is structurally a land bank. Yet sell-side coverage and screens still classify ALCO under “Food, Beverage & Tobacco” (per Simply Wall St) - the equivalent of categorizing a homebuilder as a lumberyard because they used to buy lumber.

Misperception #2: “Florida land NAV bridges don’t close.”

The classic short critique of any land bank thesis is that the spread between book value, appraised value, and realized value rarely converges. In ALCO’s case, the empirical record contradicts this. Over the trailing 36 months, the company has executed:

17,229 acres of Devil’s Garden to Florida Forever (2023): ~$77M, at appraisal

18,354 acres of ranch and citrus (FY24): $86.2M, gain of $81.4M (i.e., realized prices ~14x the FY24 carrying cost basis)

2,796 acres (FY25): $23.8M, gain of $20.3M (realized prices ~6.8x carrying cost basis) • 2,950 + 579 acres (FY26 YTD): $32.9M

Joshua Grove 20,414 acres signed (April 2025, terminated by buyer on financing - but at a verified market clearing price of $9,000/acre)

The realized-vs-appraised history is positive. Each transaction is mark-to-market evidence that the NAV gap is closing in cash, not just in slide-deck commentary.

Misperception #3: “The Harford Farms termination was a value tell.”

The May 2025 termination of the $183.7M Joshua Grove sale was almost certainly read by the market as a negative signal - the company’s stock has not re-rated since. But the termination was buyer-specific (Harford could not satisfy its financing contingency in 30 days), and the contract price ($9,000/acre on the largest single parcel in the portfolio) was an externally verified valuation event. The market is treating an absence of a closing as evidence of overvaluation. It is, in fact, evidence of a transient credit-market issue for one specific buyer.

Misperception #4: “Florida hurricane and greening risk swamp the land value.”

Hurricane risk is real (Irma 2017, Ian 2022, Milton 2024 all impacted the groves). Greening disease ended the citrus operation. But these are operating risks against the citrus business, which is now closed. The land value below the trees is largely unaffected by greening (the trees can simply be pulled) and is partly insured against hurricane risk by the same factors that increase its value: Florida’s population growth, the demand for housing, the public-sector willingness to absorb conservation acreage at floor prices when private markets soften.

Misperception #5: “Corkscrew entitlement is far off and uncertain.”

Construction is not imminent - 2028 or 2029 is the earliest. But the entitlement progression from January 2025 to April 2026 has been materially better than baseline expectations:

March 2025: SRA application filed

June 2025: Stewardship District signed into law

March 2026: Planning Commission unanimous recommendation

April 2026: Board of County Commissioners approval

Pending: State and Federal permit (~late 2026/early 2027 per management)

Each milestone is a discrete, observable value-creation event. The market discount has compressed from ~70% to ~54% in 18 months as these milestones have hit; the further compression is mechanical as state and federal permits close.

Second- and Third-Order Effects

Second-order: The conservation-development double-monetization

The cleanest way to understand the Corkscrew Grove economics is to think of it as a two-asset structure. The 3,000-or-so developable acres are sold to homebuilders at finished-lot economics ($35,000+/site × 9,000 sites). The 6,000-acre conservation set-aside is monetized through (a) stewardship credits used to entitle the development, and then (b) potential sale or easement of the underlying fee to the State of Florida via the Florida Forever or Florida Wildlife Corridor programs. The Florida Wildlife Corridor program has explicit funding allocations from the legislature; the precedent for Alico land specifically is the 2023 Devil’s Garden $77M sale. An equivalent precedent for the Corkscrew 6,000 acres would generate $25–40M of incremental proceeds at no incremental development cost.

Second-order: Stewardship District pre-funds the infrastructure

The Corkscrew Grove Stewardship District (signed by DeSantis June 2025) is an independent special-purpose unit with the authority to issue tax-exempt municipal bonds to construct project infrastructure (roads, drainage, utilities) and recover the cost through property tax assessments on future homebuyers. This is the same mechanism that funded Ave Maria and Lakewood Ranch. The economic implication is that Alico does not need to finance the infrastructure on its balance sheet; the future homebuyers do, via assessments. This is a substantial reduction in the project’s capital intensity and therefore in the discount rate that should be applied to the developable-acre valuation.

Third-order: Florida’s growth path is doing the work

Eastern Collier County is the most aggressive growth frontier in Southwest Florida. The combined Naples-Marco Island metro area MSA had population growth of ~13% over the past decade, with continued in-migration from the Northeast and Midwest accelerating during and after COVID. Corkscrew sits at the intersection of Collier, Lee, and Hendry counties, with direct access to I-75. Five years from entitlement to first close, Alico is not building into a static market - it is building into a market growing at 1.5%+ population CAGR and a housing shortfall in the affordable-to-mid-priced segments that Corkscrew is purpose-built to serve.

Third-order: Citrus exit reduces operating beta and increases land-buyer optionality

While the citrus production was running, the company’s earnings stream was tied to commodity orange juice pricing, hurricane frequency, and greening progression. With production wound down, the company’s only remaining operating exposure is to (a) Florida residential real estate, (b) ag-land transaction volumes, and (c) interest rates affecting buyer financing. The first two are vastly more macro-stable than orange juice. The third is a cyclical risk but cuts both ways.

Third-order: Tropicana termination unlocks parcel flexibility

While the Tropicana contract was in effect, Alico had a contractual obligation to deliver fruit from specified acreage to a specified buyer - which constrained its ability to retire individual parcels. With the Mutual Contract Termination Agreement of May 2025, Alico now has full discretion to retire, lease, sell, or develop any individual parcel without renegotiating with Tropicana. This is a real reduction in friction cost for the land monetization plan.

Third-order: The buyback × NAV gap geometry

Every dollar of buyback at $40 against a base-case NAV of $88 generates approximately $1.20 of NAV-per-share accretion. The $50M authorization, fully executed at current prices, would retire ~16% of shares and bump the remaining shareholders’ base-case NAV-per-share from $88 to ~$103. Continuing the buyback while the discount persists is itself a value-creation engine.

The Honest Bear Case

Risk #1: Entitlement reversal or delay at the state/federal level

The local Collier approval is in hand. The state SFWMD ERP and federal ACOE 404 permit are not. Either could be challenged on Florida-panther / endangered-species / wetlands grounds, particularly given the project’s location in panther habitat. A serious challenge could push the timeline out 2–4 years and increase mitigation costs. Mitigation: the project is structured to comply with the RLSA framework (which has been litigated and upheld), 6,000+ acres of conservation, and Alico has privately funded a $5M wildlife underpass on SR-82 - a serious commitment to mitigation that the agencies will weight. The legal architecture is unusually strong for a project of this size.

Risk #2: A 1031 misfire or change in tax law

Alico’s land sales over the past three years have relied heavily on Section 1031 like-kind exchanges to defer the recognition of gain. A failed identification, an unsuitable replacement property, or a legislative repeal/modification of Section 1031 (which has been periodically proposed by both parties) would crystallize meaningful federal and state tax on accumulated gains. With $45.4M of federal NOLs and $42.6M of state NOLs available, the immediate cash tax hit on a botched 1031 is partially absorbed - but only partially. Mitigation: ALCO’s tax-deferral toolkit is multi-layered (NOLs + accelerated depreciation step-down + 1031), and the worst-case tax leakage is on the order of $30–50M, not catastrophic against a $750M NAV.

Risk #3: Florida real-estate cycle inversion

Florida residential demand has been historically cyclical, with severe drawdowns in 2007–2010 and milder ones during interest-rate spikes. A sustained 5%+ mortgage-rate environment combined with a Florida-specific buyer pullback would slow Corkscrew velocity at full build-out and pressure ag-land transaction comparables. Mitigation: Alico has the balance sheet to wait. With ~$40M cash, ~$45M net debt, $92.5M of unused credit, and $14M of FY26E EBITDA from operating leases, the company can comfortably hold land through a 3–5 year residential downturn without selling at distressed prices. The Florida Forever and Florida Wildlife Corridor floor bids effectively put a put option under Devil’s-Garden-class conservation acreage.

Risk #4: 734 Investors / control structure asymmetry

The controlling shareholder (734 Investors at ~50.5%) creates an inherent asymmetry. If 734 decides to take the company private in a leveraged transaction at a price below our base NAV, public shareholders would receive less than fair value. The track record of 734’s stewardship since 2013 has been mixed (citrus consolidation in 2014 was poorly timed against the greening cycle), and there is no contractual protection against a take-private at, say, $55–65/share. Mitigation: (a) the public float is concentrated among informed value investors who would push back on an inadequate bid; (b) the Strategic Transformation has now been publicly committed to and the CEO’s PSUs reset at $45 - any going-private bid would need to clear at a substantial premium to that level to avoid embarrassment; (c) a fully discounted take-private at ~$55 is still a 37% premium to current.

Position-Sizing

Sizing framework

ALCO is a small-cap (~$300M market cap), thinly traded (~25,000 shares/day average volume), and structurally illiquid. The position size should reflect this: not a full-conviction concentrated bet, but a meaningful sleeve in a portfolio focused on hard assets at NAV discounts. The asymmetry is attractive - a ~50% discount to base-case NAV with a ~15% downside to book value in a true bear case, against 70–120% upside in the base-to-bull range over 2–4 years. Time-weighted IRR in the base case is approximately 25–35% across an estimated 3-year holding period, assuming the discount halves and the underlying NAV grows at ~8% as Corkscrew entitlement compounds.

Bottom Line

ALCO is a asset-heavy, lightly-levered, tax-advantaged Florida land bank with optionality that is being valued by the market as a wind-down citrus producer. The mismatch is between the company that was and the company that is. The Corkscrew Grove Villages entitlement is the largest single source of NAV crystallization; the Joshua Grove signed price is the clearest validation of the ag-land floor; the Tropicana termination is a structural simplification; and the CEO’s $35/$40/$45 PSU schedule is the cleanest possible management-shareholder alignment device.

The base-case NAV is approximately $88/share - a 120% premium to the current $40. The bull-case NAV is approximately $123/share - a 205% premium. The bear case is approximately $60/share - a 50% premium and still above book value. The asymmetry holds even before considering the option value of (a) the Stewardship District infrastructure financing, (b) the embedded water-rights premium, and (c) the buyback × discount geometry.

This is a thesis where the work is done and the waiting begins. The land doesn’t move. The asymmetry is wide enough that it survives the inevitable surprises.

Author’s note: This memo synthesizes public SEC filings, press releases, comparable-transaction data, and industry reports current as of May 2026. It is not a recommendation, an offer, or a solicitation. All figures are approximate; the NAV ranges are sensitive to assumptions on Corkscrew entitlement timing, ag-land comparables, and balance-sheet evolution.

Was following this couple years ago, good to see the name pop up again, good work